With the Fed’s recent remarks regarding their near term plan or lack thereof for short term rates, investors continue to be surrounded by uncertainty as to the timing and velocity of future interest rate movements. This uncertainty creates the question of how one can protect one’s capital base, while earning decent returns.

One of the ways to answer this question lies in recalling some of that high school math we never thought we’d need in real life. Remember when x and y axes were introduced, and the concepts of points in two-dimensional space were a real challenge? Today, if you’re building roofs or making stairs, you’re intimately familiar with “run and rise”, the triangles that show how high you go vertically for every unit of horizontal movement. For us bond folks, it’s the slope of the yield curve we get when we plot the same parameters of how far and how high.

Unlike in carpentry, our slopes change. It’s in this change that we can find some solutions to the dilemma of uncovering value. Let’s take a look at the curves as they are now and see if we can come up with ways to both protect principal and earn decent returns.

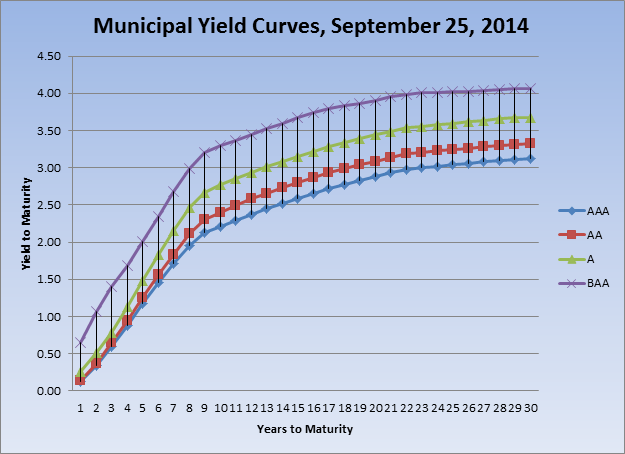

The chart above illustrates that the front end of the municipal curve slopes sharply upward until just at year eight (2022). After year eight, the curve begins to flatten until it becomes virtually horizontal out in year 23 (2037). In absolute terms, for each year of extension out to 2022, you pick up 22 basis points for AAA, 28 for AA, and 31 for A rated municipal bonds. At 20 years ,the numbers drop to 14, 16, and 17 respectively until they become one or two a year.

So does any of this mean anything to investors? Well, if you want to protect yourself it certainly does. You’re not rewarded much for extending into the long end of the municipal yield curve, so why do it? You expose yourself to greater losses in dollar value for each basis point in higher yields, and time is less of an ally as well. If you stay inside the eight-year range, then you’ll earn at least 2%, while limiting your exposure to the possibility of rising interest rates.

The variables associated with all municipal bonds are: coupon, maturity, yield to maturity, and rating. Having argued that the best value and most defensive maturities in municipal bonds fall in the eight year and shorter range, we now turn our attention to the other factors.

Virtually all-individual investors and many of their advisors prefer those bonds referred to in the trade as “current coupons”. That is to say, they buy bonds priced at or near par, which is exactly the wrong thing to do. An aversion to and misunderstanding of the premium paid for the larger coupons prevents them from earning the much higher total returns available with those larger coupons.

Mutual fund managers and other large fund investors insist on those larger coupons because they understand the net total return is always larger with premium bonds, even after netting the amortization. In fact, the benchmark scales published daily by Municipal Market Data, a Thompson Reuters company, presume a 5% coupon. The reason for the preference expressed by the professionals is quite simple. The cash flows from the larger coupons more than offset the amortization paid in every case. So, total return is largely determined by cash flow, premium bonds act better in declining markets, and owners of premium bonds will never run afoul of the IRS de minimis rules for discounts, which is a whole other topic.

One of the professional money manager’s key tools to manage interest rate exposure is “Duration”, which may be defined as the weighted average maturity of a security’s cash flows, where the present value of the flows serve as the weights. The greater the Duration, the higher the percentage price volatility. Simply stated, duration gives you the change in dollar price for every one basis point change in yield. Inasmuch as higher coupons generate higher cash flows, they produce lower durations. Buy bigger coupons.

Briefly, yield to maturity is the offering yield, which produces a dollar price resultant from a present value calculation of that yield. It goes without saying that one should seek the highest yield one can, while taking into consideration that the dealer offering the bonds may or may not be willing to adjust the price to accommodate your interest. It never hurts to ask.

Finally, ratings. A plethora of books and articles have discussed the rating agencies and their role in the collapse of markets in 2008, and this is not a forum to go over old ground. Rather it is a place to discuss, in brief, their presence in the municipal market and how to use the ratings to your advantage.

There are three major agencies providing municipal bond ratings at present, Moody’s, Standard & Poor’s (S&P), and Fitch Ratings. These firms are all recognized as quite competent, have excellent research analysts, and usually issue ratings that are virtually identical. The four highest categories range from AAA to BBB, with gradations in each category below AAA. Examples are AA+, A-, BBB+, etc.

For the average investor, we do not recommend the purchase of BBB rated bonds. This is not to suggest that there may not be value in the category, but rather that the analysis of the risks associated with these bonds requires more sophistication and analytical tools than normally available to the average investor.

There are two major types of municipal bonds: 1) those secured by some tax pledge, either general obligation or by some specific tax, and 2) revenue bonds secured by a stream of cash flows from some governmental enterprise. Revenue bonds normally receive their income from water, sewer, and electric, and other local utilities. These are frequently referred to as “essential service” revenue bonds to differentiate them from other revenue issues, and they usually provide real value for investors.

In general, investors really don’t need the protection afforded them by AAA bonds, and there are better rewards found in dipping down to AA and A rated issues. The spread between AAA and A rated bonds in our 2022 maturity is 50 basis points, and if one looks hard for the right A rated essential services revenue bond, the rewards may even be better. So, that’s the conclusion: a 5% coupon A rated revenue bond inside 2022 for the time being. Let the Fed do its thing and earn all that nice tax tree income in the meanwhile.

And, finally, remember that not all bonds are created equal.

Good Fortune!

Bob Andres is editor of The Andres Review and founder of Andres Capital. Bob’s career includes stops as: chief investment officer at Merion Wealth Partners, chief investment strategist at Envestnet (PMC division), co-founder at Martindale Andres & Co., a firm he grew to $2.4 billion before its sale, President at Merrill Lynch Mortgage Capital, etc. He has been quoted and featured in various media: CNBC, Fox Business, Barron’s, Institutional Investor, etc.

© Andres Capital Management