SUMMARY

At Eaton Vance, we believe that investors seeking enhanced portfolio diversification should think beyond stocks and bonds. With that in mind, absolute return strategies may provide an attractive option for investors to:

- Complement core asset classes, particularly stocks and bonds.

- Better navigate the inevitable ups and downs in the markets.

- Lower overall portfolio risk, without sacrificing return potential.

In a recent interview, Eric Stein, co-director of the Eaton Vance global income group, discussed the potential benefits of absolute return strategies, the role they can play in investor portfolios and more.

What are the potential advantages of absolute return investing, as compared to a traditional portfolio?

A defining feature of absolute return strategies is that they do not conform to typical style boxes. These strategies are not managed to any market-based benchmarks. Instead, they’re designed to produce positive absolute returns in any environment, independent of the ups and downs in the stock and bond markets. That may appeal to investors seeking greater consistency in their portfolio returns over time.

Another key potential advantage of absolute return investing is its ability to help manage risk. During the severe market decline of 2008, for example, a traditional portfolio balanced between stocks and bonds may not have supplied the diversification and the downside protection that many investors may have wanted. Absolute return strategies have historically exhibited very low correlation to traditional equities and fixed income. So, an appropriate allocation to such a strategy in volatile times may help to lessen portfolio risk and limit investor losses, which were substantial in many cases in 2008.

How is an absolute return investing strategy typically incorporated into a portfolio?

In a conventional portfolio allocation, investors generally have equities, fixed income and cash. When it comes to alternatives, however, many portfolios are lacking. Some portfolios may include alternative asset classes, like real estate and commodities, but fewer investors seem to incorporate alternative investment strategies, like absolute return. This may be partly because most of these strategies have only been available to the average investor for a relatively short period of time and may be unfamiliar to many. That being said, since the 2008 financial crisis, alternative strategies have grown in popularity.

It depends on each investor’s risk tolerance of course, but I think a portion of many investors’ portfolios should be allocated to absolute return strategies. These strategies may have a historical risk/return profile similar to traditional core fixed-income assets, but they have often achieved that profile from very different sources of return. That’s where I believe these types of strategies can add value to a portfolio in the form of meaningful diversification benefits.

How is absolute return investing used to potentially lower portfolio volatility and risk?

As an absolute return portfolio manager, you aim to generate positive returns from year to year and to maintain a strategy that has low correlation to trends and beta in traditional equity and fixed-income markets. If you’re successful, your strategy can help bring down overall risk in a diversified investor portfolio, particularly during bouts of volatility in the markets. Over time, the goal is to reduce risk, but to do so without sacrificing the portfolio’s long-term return potential.

The exact approach used to reach that goal may vary from one absolute return strategy to another. Our approach involves forecasting the expected risks and returns across the different markets and market sectors. We want to make sure we fully understand the various risks that we’re taking, and that the strategy is likely to get adequately rewarded for those risks. Markets generally move faster than forecasts do, so we dial our desired risk level up and down accordingly as market conditions warrant.

Why is it important for investors to guard against potential volatility?

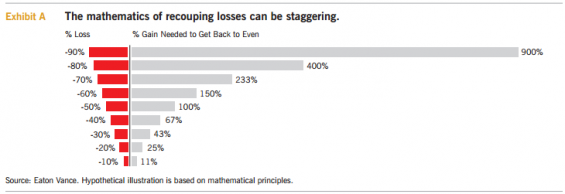

Market volatility can have a dramatic, negative impact on long-term wealth preservation and creation. For example, the mathematics of recouping large investment losses can be staggering and take years to recover. (See Exhibit A on the following page.) In our judgment, the most damaging effect of recurring market volatility is that it causes investors to react emotionally and to make the wrong decisions at the wrong time. As a result, investors’ response to volatility is perhaps a bigger risk than the actual volatility itself.

Even during periods of muted volatility, investors should remember that volatility is an ever-present, unpredictable threat. Any number of factors – geopolitical tensions or more gridlock in Washington, to name just a couple – could trigger an unexpected surge in volatility. In the event of something like that, investors may benefit from having an absolute return strategy with low correlation to stocks and bonds. The strategy will likely lag the stock market during strong market rallies, but by helping to preserve capital in volatile markets, you may be better positioned to build wealth over the long term.

Are absolute return strategies global in nature?

Yes, most are to some extent. By remaining unconstrained to any benchmarks or style boxes, many of these strategies have a flexible approach to investing long and short in overseas markets. As such, they may provide a way for investors to gain or increase global exposure, thereby helping to potentially counterbalance performance swings in their U.S. equity and fixed-income holdings. That’s particularly true, I think, for investors who choose an experienced absolute return manager – one with access to a wide investment universe to seek out the most compelling opportunities, wherever they may be.

So, what exactly do these strategies invest in?

Speaking just for our strategy, we invest broadly across the global fixed-income markets. We take both long and short positions in asset classes that are typically unrepresented or underrepresented in investor portfolios, such as foreign and U.S. currencies and sovereign debt. This includes exposure to emerging and frontier markets, as well as the U.S. and other developed markets. To a lesser degree, the strategy may also have long and short positions in global equities and/or commodities.

Our exposures are determined largely through our top-down analysis of macroeconomic and political trends within individual countries, and may offer return potential in both improving and deteriorating markets. We carefully consider risk and potential reward for each investment opportunity we evaluate.

In your opinion, is it best to invest in an absolute return strategy via a mutual fund structure?

Yes, I believe so. Historically, a problem for the average investor has been that, in order to participate in these strategies, you had to have a high net worth of at least $1 million. So, the majority of retail investors were basically shut out. While we’ve been managing our strategy for many years as a ’40 Act mutual fund,1 after the financial crisis, many other fund companies realized they could also deliver this type of strategy to mainstream investors via a ‘40 Act fund. Mutual funds are professionally managed portfolios that offer daily liquidity, independent pricing and a high degree of regulation and transparency.

1A ‘40 Act mutual fund refers to a fund registered under the Investment Company Act of 1940, which can be marketed and sold to an unlimited number of investors regardless of their income or net worth.

About Eaton Vance

Eaton Vance Corp. is one of the oldest investment management firms in the United States, with a history dating to 1924. Eaton Vance and its affiliates offer individuals and institutions a broad array of investment strategies and wealth management solutions. The Company’s long record of exemplary service, timely innovation and attractive returns through a variety of market conditions has made Eaton Vance the investment manager of choice for many of today’s most discerning investors.

About Risk

Volatility: While certain Funds have a targeted annual performance volatility range, its actual, or realized, volatility for longer or shorter periods may be materially higher or lower than the target range depending on market conditions. No Fund is a complete investment program and you may lose money investing in a Fund. Regulatory changes may adversely affect securities markets and market participants, as well as the Fund’s ability to implement its strategy. A Fund may engage in other investment practices that may involve additional risks and you should review the Fund prospectus for a complete description.

Investments in foreign instruments or currencies can involve greater risk and volatility than U.S. investments because of adverse market, economic, political, regulatory, geopolitical or other conditions. In emerging countries, these risks may be more significant. An imbalance in supply and demand in the income market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. Investments in income securities may be affected by changes in the creditworthiness of the issuer and are subject to the risk of nonpayment of principal and interest. The value of income securities also may decline because of real or perceived concerns about the issuer’s ability to make principal and interest payments. Derivative instruments can be used to take both long and short positions, be highly volatile, result in economic leverage (which can magnify losses), and involve risks in addition to the risks of the underlying instrument on which the derivative is based, such as counterparty, correlation and liquidity risk. The value of commodities investments will generally be affected by overall market movements and factors specific to a particular industry or commodity, including weather, embargoes, tariffs, or health, political, international and regulatory developments. As interest rates rise, the value of certain income investments is likely to decline. Investments rated below investment grade (typically referred to as “junk”) are generally subject to greater price volatility and illiquidity than higher-rated investments.

Diversification cannot ensure a profit or eliminate the risk of loss.

The views expressed in this Insight are those of Eric Stein and are current only through the date stated at the top of this page. These views are subject to change at any time based upon market or other conditions, and Eaton Vance disclaims any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Eaton Vance are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Eaton Vance fund.

This Insight may contain statements that are not historical facts, referred to as forward-looking statements. A Fund’s actual future results may differ significantly from those stated in forward-looking statements, depending on factors such as changes in securities or financial markets or general economic conditions, the volume of sales and purchases of Fund shares, the continuation of investment advisory, administrative and service contracts, and other risks discussed from time to time in the Fund’s filings with the Securities and Exchange Commission.

Before investing, investors should consider carefully the investment objectives, risks, charges and expenses of a mutual fund. This and

other important information is contained in the prospectus and summary prospectus, which can be obtained from a financial advisor. Prospective investors should read the prospectus carefully before investing.

©2014 Eaton Vance Distributors, Inc. | Member FINRA/SIPC | Two International Place, Boston, MA 02110 | 800.836.2414