Following a yearlong environment of relatively stable corporate bond spreads, we are beginning to see increased market volatility and a widening of these credit spreads. The plunge in oil prices, the rise in the U.S. dollar, and geopolitical uncertainty all contribute to wider spreads as they represent a proxy for market risk. It’s worth pointing out that credit spreads have remained firm despite a fourfold increase in corporate issuance since the financial crisis. This can be attributed to several factors:

Why have corporate bond spreads stayed tight?

QE. The actions by the Federal Reserve Bank to keep interest rates artificially low supposedly to spur economic growth—opinions as to the actual success and impact of this policy remain widely varied—combined with increasing the Fed’s balance sheet by four trillion dollars through the purchase of U.S. treasuries and mortgage-backed securities.

- The latter serving to create artificial demand by removing large amounts of securities from the marketplace. Recently both the ECB and Japan have implemented similar policies.

De-Leveraging. An ongoing climate of general corporate de-leveraging resulting in stronger balance sheets and in turn improved over-all credit quality.

Flows. Despite the meteoric rise in the various stock indices, investor money continues to flow into fixed-income funds and ETFs.

Fear. The seemingly never ending geopolitical tensions continue to fuel a flight to safety trade.

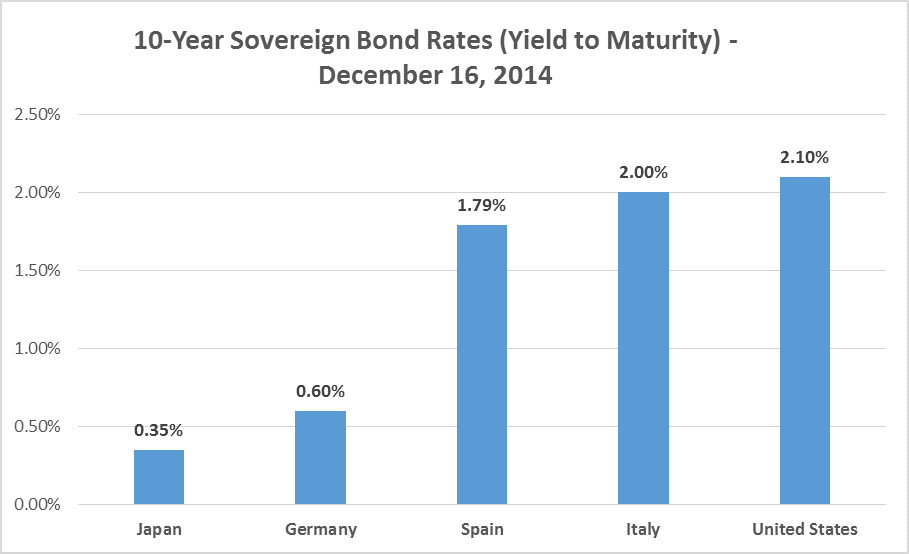

Comparative Economies, Currencies and Sovereign Rates. The USA is the place to shop this holiday season… with a strong dollar, higher rates than other industrialized nations and the only economy chugging along an upward path, the money keeps rolling in.

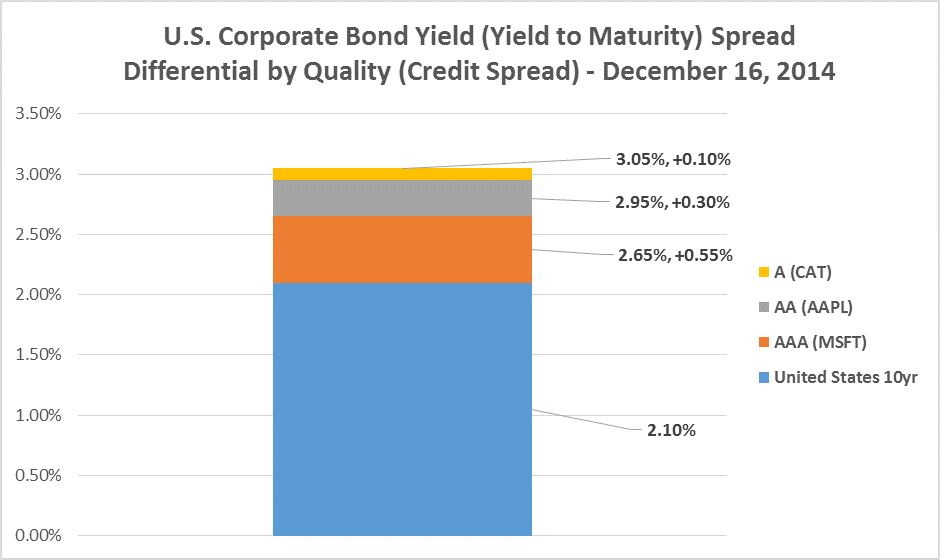

What Is Credit Spread? Virtually all credit products such as corporate bonds, government agency bonds (e.g. Fannie-Mae and Freddie-Mac) and mortgage-backed securities are measured in spread terms against U.S. Treasury bonds yields, which serve as the highest quality benchmark. This denotes the spread differential in yield between U.S. Treasury securities and non-treasury securities that have similar maturities but different quality (i.e. credit) ratings. This value is expressed in basis points (i.e. 1/100th of 1 percent of yield). For example, a corporate bond offered at 50 basis points over a corresponding treasury issue yielding 2.10 to maturity (i.e. 2.10ytm) produces a yield of 2.60ytm.

Current spread widening factors:

Oil. The precipitous decline in the price of oil from $110 to $57 dollars a barrel impacts bond spreads throughout the entire energy sector. Spreads are widening the most in small companies with high production costs. Many of these names reside in the high yield or junk bond markets where energy related names make up over 15 percent of the high yield bond index.

Event risk. The risk that the credit quality and subsequent credit rating of a company will drop suddenly due to events or news related to a possible restructuring or takeover.

In this environment of cheap money, M&A activity continues to thrive with rising stock prices and readily available financing. Also, the growth of investor activism on the part of hedge funds and pension funds has created heightened sensitivity for potential credit related issues. The industries with the greatest merger activity continue to be biotech/pharma and telecom/media/technology.

These transactions are typically financed by issuing large amounts of new debt, which ultimately weaken the new entity’s credit profile. Additionally, the acquiring companies often carry a lower credit bond rating.

Dodd-Frank . . . can we be frank? The continuing enforcement of regulations for increased capital requirements on the part of market makers (i.e. large banks and broker-dealers such as Goldman Sachs and Citibank) intended to reduce leverage and risk taking in the system has produced the unintended consequences of decreased principal market activity, a huge reduction in inventories (i.e. the amount of bonds held at risk on the firm’s books), wider bid-offer spreads, and ultimately less liquidity for all market participants. This is creating a less stable and less dependable marketplace, which has yet to be truly tested in a period of rising interest rates or major exogenous shocks.

Opportunities. The recent spread widening in various industry sectors highlights some interesting investment strategies if one can identify the industry leaders with the strongest balance sheets in those sectors. Companies like Royal Dutch Shell, Conoco, Apache, and Verizon are surely going to be around for a while and are likely to see their spreads tighten as the oil situation eventually stabilizes, which would lead to outperformance versus the benchmark 10-year U.S. Treasury.

All of these factors serve to point out that participation in the bond markets requires continued diligence and an informed advisor. While many may refer to credit spreads as historically thin, one may wish to look at the yield on the current benchmark rate—the United States 10-Year Treasury. The incremental yield pickup in the investment-grade universe is not insubstantial when the relative levels of the benchmark are examined. Getting an extra 100 basis points on an A-rated credit is not too bad when the benchmark yield is just over 200 basis points. Remember, Not All Bonds Are Created Equal.

Good Fortune!