The Swiss National Bank’s surprise decision

“Francogeddon” … “tsunami” … “carnage” … The hyperbole after the Swiss National Bank (SNB) unexpectedly ended its three-year currency ceiling peg to the euro yesterday was not misplaced. The immediate impact has been profound across a range of markets. The longer-time ripples are only beginning to become apparent. This is what we’ve gleaned so far:

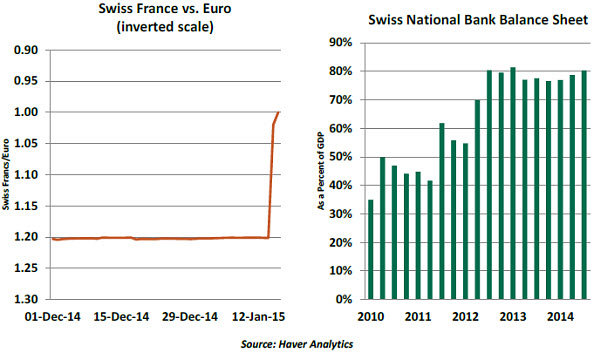

What happened yesterday?

- The SNB scrapped the cap, introduced in September 2011, that held the Swiss franc (SFr) to no more than SFr1.20 per euro. The cap had limited Sfr appreciation at the height of the eurozone crisis and remained binding since then.

Defending the move, SNB Chair Thomas Jordan said the cap was “unsustainable” and that the only way to exit such a policy is to take the market by surprise. And that it did.

- The SNB also announced a cut in its benchmark overnight deposit rate to -0.75%. This is the furthest a major central bank has ever pushed its policy rate into negative territory.

- The SFr promptly shot up nearly 30% against the euro before settling around parity into this morning. This was an unprecedented rate of change for a major, heavily traded currency and as such, was very unsettling.

Why change now?

When the cap was enacted, Swiss policymakers had feared the currency appreciation created by safe-haven inflows would trigger deflation (because import prices would fall) and recession (because Swiss exports would become more expensive and less competitive).

But intervention to hold down the SFr has boosted the SNB’s balance sheet to around 85% of Swiss gross domestic product (GDP). (By comparison, the Federal Reserve’s balance sheet is about 25% of U.S. GDP.) This magnitude apparently made the SNB’s Jordan uncomfortable, but only a few days ago one of Jordan’s deputies described the cap as the cornerstone of Swiss policy.

The European Central Bank’s (ECB) upcoming policy meeting on January 22 may have been a catalyst. The SNB is believed to be in close communication with the ECB; speculation is therefore rife that the ECB will be announcing a major quantitative easing program next week. The SNB must have been concerned about the consequences of a much weaker euro and even more flows into SFr assets, which would have meant even more intervention to maintain the cap.

What are the immediate impacts?

- A new wave of volatility has hit foreign exchange, commodity, bond and stock markets. This has added to concerns about falling energy prices, and global disinflation to create uneasiness among investors.

- The Swiss stock market fell about 10% yesterday and dropped further today.

- Swiss 10-year yields turned negative today at -0.003% – the first time a major country has ever seen this occur.

- Coupled with expectations of a major ECB announcement next week, the SNB bombshell has triggered new record lows on German and other core eurozone government bond yields.

- Greek 10-year yields shot to almost 10% and the yield curve remains inverted, with three-year yields at 11.9%. Two of its banks (Eurobank and Alpha bank) requested emergency central bank funding for the first time in more than a year. It is likely that the banks’ concerns about the impact on their SFr-denominated mortgages were a key factor.

How will Switzerland be affected?

The stronger Sfr will have a broad range of influences. About 40% of Switzerland’s annual exports go to the eurozone, so there will likely be a wave of profit warnings from Swiss companies. The Swiss tourism industry will also take a hit.

Swiss real GDP growth had been forecast at about 1.9% for 2015. That will now be revised markedly downward. And the two large Swiss banks, which have substantial asset holdings denominated in euros and dollars, could see earnings and capital impaired.

What other areas bear watching?

- Central and eastern European (CEE) mortgage markets will be hurt. Of these, the most vulnerable appears to be Poland. SFr-denominated mortgages reportedly equal around 7% – 8% of Polish GDP, suggesting a sharp rise in the SFr will hit mortgage payers hard. The zloty and Polish stock market have taken a hit, and further consolidation in Poland’s banking sector may be in the cards.

- Austrian and Italian banks have been the heaviest lenders into central/eastern Europe. Lenders in Hungary had already been forced by that country’s government to convert SFr mortgages into forints; lenders in other CEE countries may have to follow.

- Smaller currency brokerages could be devastated. At least two have already folded. Larger houses will likely be able to absorb the losses, but the ripple effects will still be felt across the industry.

The SNB’s move raises the stakes even further for the ECB, which meets on Thursday. A quantitative easing program is expected, but its size could have a significant influence on where currency and interest-rate markets settle. We’ll return with coverage of that outcome next week.

© Northern Trust