Sell-off in Corporate Credit Creates Income Opportunities for 2015

SUMMARY

- In 2014, U.S. short-term rates inched up in anticipation of Fed tightening, while global weakness reduced upward pressure on long-term rates.

- Lower U.S. long-term rates were a tail wind for most fixed-income sectors.

- We expect a flattening yield curve in 2015, and view this as a positive for floating-rate loans, high-yield bonds and municipal bonds relative to U.S. Treasurys.

- Investors should be prepared for more price volatility; a longer-term focus can help bridge choppy patches that may be more technically than fundamentally driven.

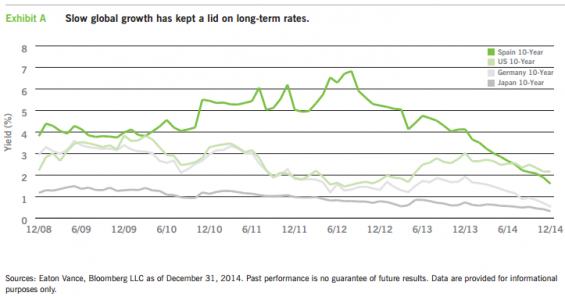

The broad backdrop for the bond market in 2014 consisted of divergent macro forces in the U.S and the rest of the world. In the U.S., as signs increased that the recovery was gaining steam, the market looked to signals from the U.S. Federal Reserve (the Fed) for clues about when it would formally begin to tighten monetary policy by raising the federal funds (fed funds) rate. But in Europe, Japan and China, central banks pursued looser policies as the global economy weakened – except for the U.S., at least so far. This divergence can be seen most dramatically in the excess yield of U.S. 10-year debt compared with Spain, Germany and Japan. This is the first time in five years the U.S. has yielded more than Spain (Exhibit A), while the spread over German debt widened to 163 basis points (bps), compared with a five-year average spread of 44 bps.

This sets the stage for a flattening yield curve, with U.S. short-term rates creeping up in anticipation of Fed tightening, while continuing global weakness reduces upward pressure on long-term rates. The flattening we anticipate would be a continuation of a trend we have seen in the past year. The income investment strategies that we feel are most attractive this year are those that sold off in the fourth quarter of 2014 and are likely to fare well in a flattening scenario. First, we review 2014 performance.

A good year for bonds

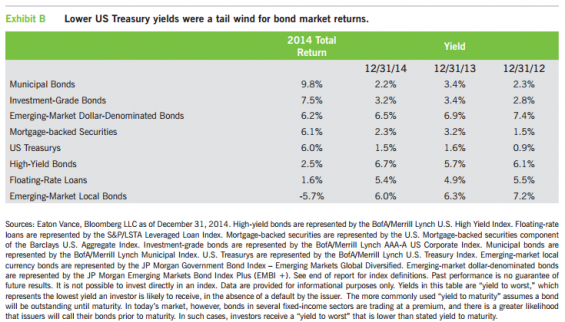

In general, bond market performance in 2014 benefited from the 87-bps decline in the 10-Year U.S. Treasury yield over the course of the year. Not only was there a lack of substantial pressure from the global economy to put a floor on rates, but the re-emergence of market volatility in October brought back “flight to quality” as a force that helped boost Treasury prices and lower yields. As a result, most fixed-income sectors posted positive total returns for the year, in marked contrast to 2013, when only high-yield bonds and floating-rate loans were in the black (Exhibit B).

The last two years offer a lesson in how investor sentiment can drive short-term swings in bond prices, even when the economic environment has not changed substantially, as was the case in 2013 and 2014. For example, total return on municipal bonds swung from -2.9% in 2013 to 9.8% in 2014. Our generally positive view of the municipal sector has been fairly consistent over the past two years, as we have seen steady improvement in the financial condition of many state and local governments. (An extensive look at our take on municipals was in the November 24, 2014 issue of Barron’s.) Indeed, the sector was one of our top recommendations in this report one year ago.

The 2013 underperformance of the municipal market was largely driven by negative headlines about the difficulties faced by a relative handful of issuers such as Detroit and Puerto Rico. Last year, however, as the brightening view of the municipal landscape gained more acceptance and the impact of the new 2013 tax rates sunk in, the tide of investment flows reversed into the sector. In investment jargon, these were technically driven price moves, where supply and demand were a greater factor in the changes than the fundamentals.

Market technicals also played a significant role in explaining performance in the high-yield bond and floating-rate loan markets over the past two years. As noted, high yield bonds and floating-rate loans led the pack in 2013, but were near the bottom last year. In this case, the two had been beneficiaries in 2013 of the global search for yield, as investors poured money into the sectors. But in 2014, concerns about increasing levels of risk in the market – i.e., issuance by some less-creditworthy borrowers at the margin – led to a turnaround in flows. Nevertheless, high-yield had a total return of 2.5% and floating-rate, 1.6% – positive, but well below their respective coupon income. Again, technicals outweighed fundamentals, as corporate America generally continued along the same improvement track over the two-year period.

Credit sectors have fared well in earlier rising-rate cycles

Considering the potential impact of a flattening yield curve serves a useful purpose, because investment discussions often talk about “rising rates” without mention of where on the yield curve that may happen. Except for the historic intervention of quantitative easing, which ended in October, the Fed largely manages monetary policy at the short end of the yield curve.

Exhibit C (top) shows that certain credit-sensitive fixed-income sectors have small, but positive, correlation with changes in the fed funds rate, meaning that historically, total returns of these sectors have actually been positive when the Fed has raised short-term rates. The implication is that if the Fed tightens this year, as is now expected, and long-term U.S. rates remain tethered by continuing relatively weak global growth, capital losses are not likely to be realized in certain fixed-income credit sectors. Exhibit C (bottom) shows a different picture when the 10 Yr. U.S. Treasury yield has risen. During those periods, all sectors have lost value, except floating-rate and high-yield. Floating-rate loans have near-zero duration, while high-yield bonds have relatively high cash flows that cushion the impact of rising rates on price.

Investment implications for 2015

- Floating-rate loans– As discussed, floating-rate loans have historically done well in periods of rising rates – whether at the short or long end of the yield curve. Given very low average historical credit losses, yields are relatively attractive at greater than 5% as of December 31, 2014. The sector has recently experienced a sell-off, in part due to negative headlines, and prices have fallen below par, meaning there is room for capital appreciation. At this phase of the credit cycle, we favor high-quality issuers who are most likely to meet their obligations and provide the income stream investors expect.

- High yield – High-yield bonds should be relatively unharmed in a flattening-yield-curve environment, due to a restored “yield cushion.” Thanks to price volatility in the fourth quarter of 2014, yields increased to 6.7% at yearend. Another plus for the sector is that default rates, an important indicator and component of total return for high-yield debt, are near historic lows.

- Municipal – We believe general improvements in state and local government finances are likely to continue and that tax rates remain a major concern for investors. In our opinion, the sector remains attractive relative to U.S. Treasurys. The longer end of the municipal yield curve appears to offer slightly better value, with 30-year AAA municipals yielding 100% of equivalent-duration U.S. Treasurys, although the longer end is vulnerable if long-term Treasury rates rise significantly. This is not our expected scenario, but investors who are concerned about potential price volatility might consider an intermediate to slightly longer duration portfolio, an opportunistic muni credit approach, or a laddered muni bond portfolio – one which holds bonds with a sequence of maturities from short to long. As the shorter-term bonds mature, the principal can be invested in longer-maturity bonds with higher yields, helping to cushion the impact of potential price declines in the portfolio due to rising interest rates.

- Emerging market– This sector sold off in 2013. Last year, we expected more of a recovery but got a mixed one: Local currency-denominated bonds lost 5.7%, while dollar-denominated emerging-market bonds had a total return of 6.2%, largely because of the strength of the U.S. dollar. Both dollar and non-dollar have attractive yields, with the latter also offering exposure to other currencies and a hedge against the dollar. Bear in mind that emerging-market debt historically has been volatile. Local currency debt currently may be best-suited for longer-term investors, given our current expectation of continuing near-term strength in the U.S. dollar.

Keeping volatility in perspective

We anticipate volatility will continue to be a factor in 2015 for all market sectors. The phenomenon isn’t new – and bond market sector leadership has a long history of changing year to year. But sharper moves – price gaps, if you will – are becoming more routine. This has largely been attributed to lower inventories of bonds now being held by primary dealers (those who deal directly with the Fed) in response to new regulation. By making markets in bonds, such dealers have helped supply liquidity that has tended to smooth out price movements.

Regardless of the cause, we believe that greater volatility makes it more important than ever for long-term investors to prepare for it – to stay the course and resist action unless price declines reflect deteriorating fundamentals. Referring back to the recent municipal market volatility, investors who sold in 2013 based on negative headlines and technical factors would have missed the comeback in 2014. Staying the course is easier said than done, but volatility should be an occasion for investors to remind themselves of their objective and time horizon. If it is medium- to longer-term, the downside of “capitulating” to a patch of negative investor sentiment should be carefully considered.

Of course, volatility can be an investor’s friend, by providing attractive price entry levels for fundamentally sound investments. We touch on two strategies that seek opportunities that volatility may provide:

- Absolute return– Absolute return strategies typically pursue long and short value opportunities across global bond markets. They seek to generate return that has low correlation to both stock and bond markets – a prudent strategy when either market sells off. Such strategies tend to do better in volatile markets, but less so in steady-state or trending markets.

- Multisector income – Given that leadership can shift quickly in the bond market, multisector strategies are designed to take advantage of an expanded global opportunity set that is continually in flux. Multisector strategies seek total return by investing in value opportunities in individual securities across diverse U.S. and international income sectors. Returns can vary significantly from broad bond market benchmarks like the Barclays U.S. Aggregate Bond Index.

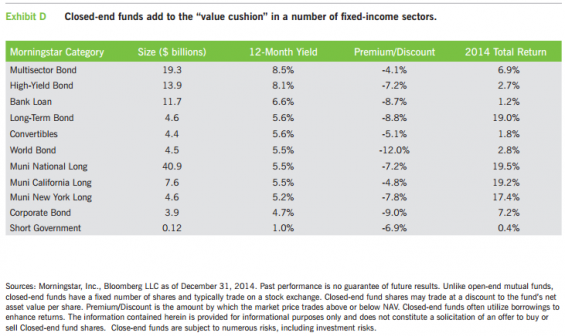

Value in closed-end funds

The closed-end funds in Exhibit D are examples of diverse income sectors being offered with a “value cushion” -- where the market price of a fund share is below the net asset value of the bonds in the fund’s portfolio. For example, the Morningstar U.S. closed-end national muni fund universe on December 31, 2014 traded at a 7.2% discount to NAV, for a yield of 5.5% and a taxable-equivalent yield at the top 43.4% rate of 9.7%.1 Another good example is the closed-end fund multisector bond universe, which had an 8.5% yield at yearend.

Looking ahead

We believe 2015 is likely to bring higher short-term rates and a flatter yield curve, along with greater overall volatility in the bond market. We feel investors will be best positioned for this environment by sticking with issues of qualilty companies or jurisdictions within each income sector.

We believe that bond picking and active professional management will be especially valuable in 2015. For example, a number of high-yield bonds were issued by energy companies. If low oil prices persist, it will be particularly important for portfolio managers to separate the winners from the losers in the sector. In our view, 2014 gave rise to excellent income opportunities, and we look forward to helping you pursue these in the new year.

1Taxable-equivalent yield refers to the yield an investor in a particular tax bracket would have to earn on a taxable investment to have the same after-tax yield as on a given tax-free security such as a municipal bond. In this example, we assume the investor is in the current maximum federal tax bracket of 43.4% (which includes the new tax from the Affordable Care Act). The investor would need a taxable yield of 9.7% to match the after-tax yield on a municipal bond of 5.5%. A portion of income may be subject to federal income and/or alternative minimum tax.

Index Definitions

BofA/Merrill Lynch U.S. High Yield Index is an unmanaged index of below-investment-grade U.S. corporate bonds.

The S&P/LSTA Leveraged Loan Index is an unmanaged index of the institutional leveraged loan market.

BofA/Merrill Lynch U.S. Mortgage-Backed Securities Index is an unmanaged index of the U.S. mortgage-backed securities market.

BofA/Merrill Lynch AAA-A US Corporate Index consists of U.S. dollar-denominated investment-grade corporate debt securities rated between AAA and A.

BofA/Merrill Lynch U.S. Treasury Index is an unmanaged index of U.S. Treasury securities with remaining maturities between 7 and 10 years.

BofA/Merrill Lynch Municipal Index tracks the performance of U.S. dollar-denominated investment-grade tax-exempt debt publicly issued by U.S. and its territories, and their political subdivisions, in the U.S. domestic market. Securities must have at least a one-year term remaining to maturity and a fixed coupon schedule.

JPMorgan Government Bond Index - Emerging Markets Global Diversified (GBI-EM) is an unmanaged index of local currency bonds with maturities of more than one year issued by emerging-market governments.

JPMorgan Emerging Markets Bond Index Plus (EMBI+) is an unmanaged free float-adjusted market-capitalization-weighted index designed to measure the debt market performance of U.S. dollar-denominated emerging markets.

BofA Merrill Lynch Indexes: BofA Merrill Lynch™ indexes not for redistribution or other uses; provided “as is,” without warranties, and with no liability. Eaton Vance has prepared this report, BofA/Merrill Lynch does not endorse it, or guarantee, review, or endorse Eaton Vance’s products.

Unless otherwise stated, index returns do not reflect the effect of any applicable sales charges, commissions, expenses, taxes or leverage, as applicable. It is not possible to invest directly in an index. Historical performance of the index illustrates market trends and does not represent the past or future performance.

About Risk

An imbalance in supply and demand in the income market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. Investments in income securities may be affected by changes in the creditworthiness of the issuer and are subject to the risk of nonpayment of principal and interest. The value of income securities also may decline because of real or perceived concerns about the issuer’s ability to make principal and interest payments. As interest rates rise, the value of certain income investments is likely to decline. An imbalance in supply and demand in the municipal market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. There generally is limited public information about municipal issuers. As interest rates rise, the value of certain income investments is likely to decline. Investments involving higher risk do not necessarily mean higher return potential. Diversification cannot ensure a profit or eliminate the risk of loss.

Elements of this commentary include comparisons of different asset classes, each of which has distinct risk and return characteristics. Every investment carries risk, and principal values and performance will fluctuate with all asset classes shown, sometimes substantially. Asset classes shown are not insured by the FDIC and are not deposits or other obligations of, or guaranteed by, any depository institution. All asset classes shown are subject to risks, including possible loss of principal invested.

The principal risks involved with investing in the asset classes shown are interest-rate risk, credit risk and liquidity risk, with each asset class shown offering a distinct combination of these risks. Generally, considered along a spectrum of risk and return potential, U.S. Treasury securities (which are guaranteed as to the payment of principal and interest by the U.S. government) offer lower credit risk, higher levels of liquidity, higher interest-rate risk and lower return potential, whereas asset classes such as high-yield corporate bonds and emerging-market bonds offer higher credit risk, lower levels of liquidity, lower interest-rate risk and higher return potential. Other asset classes shown, such as municipal and investment-grade bonds, carry different levels of each of these risk and return characteristics, and as a result generally fall varying degrees along the risk/return spectrum.

Costs and expenses associated with investing in asset classes shown will vary, sometimes substantially, depending upon specific investment vehicles chosen. No investment in the asset classes shown is insured or guaranteed, unless explicitly stated for a specific investment vehicle. Interest income earned on asset classes shown is subject to ordinary federal, state and local income taxes, excepting U.S. Treasury securities (exempt from state and local income taxes) and municipal securities (exempt from federal income taxes, with certain securities exempt from federal, state and local income taxes). In addition, federal and/or state capital gains taxes may apply to investments that are sold at a profit. Eaton Vance does not provide tax or legal advice. Prospective investors should consult with a tax or legal advisor before making any investment decision.

About Eaton Vance

Eaton Vance Corp. is one of the oldest investment management firms in the United States, with a history dating to 1924. Eaton Vance and its affiliates offer individuals and institutions a broad array of investment strategies and wealth management solutions. The Company’s long record of exemplary service, timely innovation and attractive returns through a variety of market conditions has made Eaton Vance the investment manager of choice for many of today’s most discerning investors. For more information, visit eatonvance.com.

The views expressed in this Insight are those of the author and are current only through the date stated at the top of this page. These views are subject to change at any time based upon market or other conditions, and Eaton Vance disclaims any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Eaton Vance are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Eaton Vance fund.

This Insight may contain statements that are not historical facts, referred to as forward-looking statements. Future results may differ significantly from those stated in forward-looking statements, depending on factors such as changes in securities or financial markets or general economic conditions.

Before investing, investors should consider carefully the investment objectives, risks, charges and expenses of a mutual fund. This and other important information is contained in the prospectus and summary prospectus, which can be obtained from a financial advisor. Prospective investors should read the prospectus carefully before investing.

©2015 Eaton Vance Distributors, Inc. | Member FINRA/SIPC | Two International Place, Boston, MA 02110 | 800.836.2414 |eatonvance.com.