The Strange Case of the Current Small-Cap Cycle

Through much of this long recovery for equity prices following the market bottom on March 9, 2009, specifically the period from 2011-2014, many active small-cap approaches, our own included, struggled to beat their benchmarks. The initial years of the cycle (2009-2010) were strong on both an absolute and relative basis for the majority of our Featured Funds. However, the last four calendar years saw many of our portfolios coming up short on a relative basis.

We can accept relative underperformance for a one-year period with equanimity. A three-year period is more difficult to swallrow because it represents to us the threshold between the short and long terms. However, we could ultimately accept that too, provided we saw strong signs of market or economic changes that looked likely to benefit our disciplined approach. A five-year underperformance period, on the other hand, is another matter entirely. (It bears mentioning that the respective five-year average annual total returns for both our flagship, Royce Pennsylvania Mutual Fund ("PMF") (+12.8%), and the Russell 2000 (+15.5%) were well in excess of their respective historical rolling monthly five-year averages of 9.8% and 7.6% since the small-cap index's inception on 12/31/78.)

This most recent underperformance period led us to attempt to answer two critical questions that are important to us and that we know have been on the minds of our investors: First, what forces have helped to shape the current cycle and contributed to the relative advantage for the small-cap index? Second, what signs, if any, reveal that some of these forces may be ebbing or reversing?

Three specific market conditions have resulted in relative performance challenges: when small-cap stocks are generating returns well above their long-term averages, when there is lowerthan- usual volatility for small-cap stocks, and/or when credit spreads—or the cost of capital—is declining. When only one of these conditions was present, our relative performance often suffered, if only in the short run. Yet for much of the past five years, each of these three conditions converged.

Before looking more closely at these developments, we want to emphasize that our belief in the cyclical nature of financial markets is fundamental and unshakeable. We were not surprised to find, then, that all three were showing signs of abating at the end of 2014. And while we cannot predict future performance patterns, we are nonetheless encouraged by many of our Featured Funds' long-term histories, especially following similar underperformance periods.

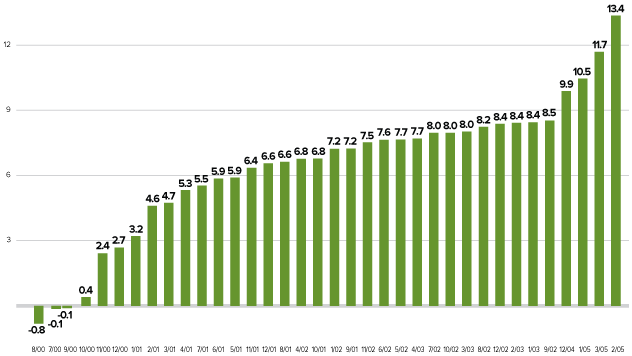

Credit Spreads* and Royce Returns

The availability of capital for businesses expands and contracts over time. In 2008, capital was understandably both quite scarce and very expensive. Contrast this with 2013 when capital was widely available.

One metric used to assess the price, or cost, of capital is the difference in yield between U.S. Treasury bonds and high-yield bonds. When this yield differential, or yield spread, is high, the cost of capital is also, which often causes problems for highly leveraged businesses.

When the cost of capital declines and the yield spread drops, it creates a potential advantage for the kind of highly leveraged stocks that we typically avoid. Yet many high-leverage stocks find homes in the Russell 2000. When the cost of capital was declining (and the yield spread was narrow), these stocks contributed to the index's stellar performance. The reverse held true when the cost of capital rose, expanding the yield spread. As a result, our relative performance has often correlated with movements in high-yield credit spreads. As shown in the table below, from 1996-2014 PMF slightly underperformed when the credit spread range contracted, typically had a slight excess return when this range was narrow (and more stable), and had a more decisive advantage when the range widened—that is, when the cost of capital rose.

Average of One-Year PMF Excess Returns by Credit Spread Rate of Change

From 12/31/96 through 12/31/14 (%)

| CREDIT SPREAD RATE OF CHANGE |

AVERAGE EXCESS RETURN |

|

|---|---|---|

| Tercile 1 (Credit Spreads Narrow) | -12.2 to -0.9 | -3.8 |

| Tercile 2 (Credit Spreads Stable) | -0.9 to 0.8 | 0.2 |

| Tercile 3 (Credit Spreads Widen) | 0.8 to 14.1 | 7.0 |

We are therefore encouraged by the recent increase in the cost of capital. From a peak of 21.8% at the end of 2008, yield spreads contracted all the way down to 3.4% in the early summer of 2014 and have already begun to widen. They stood at 5.0% at the end of 2014.

Volatility is an Ally

Low volatility environments have historically been challenging for most active managers, including ourselves. The reason is that differentiation lies at the core of active management. We evaluate multiple aspects of a company and then judge whether or not the current stock price reflects the long-term prospects we see.

Opportunities to purchase what we deem to be attractively undervalued companies occur more frequently when stock prices are volatile. The following table shows that over the past 36 years, our investment approach with PMF on average generated excess returns versus the Russell 2000 in most market environments—except those with the lowest volatility. But for most of the last five years, volatility has been falling and has remained low, which has created a more difficult environment for active managers to outpace their benchmarks.

Average of Five-Year Monthly Rolling Statistics

From 12/31/78 through 12/31/14 (%)

| QUNTILES | |||||

|---|---|---|---|---|---|

| FUND | 1 | 2 | 3 | 4 | 5 |

| Russell 2000 Standard Deviation | 14.19 | 17.50 | 20.09 | 21.90 | 23.55 |

| Russell 2000 Performance | 14.91 | 14.34 | 12.00 | 7.20 | 3.86 |

| PMF Performance | 12.88 | 15.77 | 15.07 | 12.25 | 7.22 |

| PMF Excess Return vs. Russell 2000 | -2.03 | 1.43 | 3.07 | 5.06 | 3.36 |

It's worth pointing out that since the second quarter of 2014 U.S. small-caps have seen increased volatility. If the trend continues, it should create more opportunities for us to buy at attractive prices.

How Long Can High Returns Last?

From the inception of the Russell 2000 (12/31/78) through the end of 2014, there were 373 monthly trailing five-year return periods. In 27% of those periods, five-year average annual total returns were greater than 15%. The five-year period ended 12/31/14 was one of these periods, with the small-cap index returning 15.5%. While such high return periods are not the norm, they have historically been challenging for active mangers such as ourselves. In fact, when trailing five-year returns for the Russell 2000 were 15% or greater, PMF underperformed 51% of the time.

Our expectation going forward is for something closer to small-cap's five-year average annual total rolling return of 7.6%. Such periods, as can be seen in the table below, were favorable to our approach.

Five-Year Rolling Returns

Russell 2000 Average Annual Total Returns from 12/31/78 through 12/31/14 (%)

| < 5% | 5% - 10% | 10% - 15% | > 15% | |

|---|---|---|---|---|

| Number of Periods | 81 | 101 | 90 | 101 |

| % of Periods | 22% | 27% | 24% | 27% |

| PMF Average Excess Return | 3.56% | 4.64% | 0.76% | -0.13% |

...So What Happens Next?

In our experience, markets are cyclical. Most trends reverse, though they can linger for longer than initially anticipated (or desired). The three trends we have examined—narrow credit spreads, lower-thanaverage volatility, and higher-than-usual small-cap returns—all showed signs of reversing in the latter part of 2014.

We view these shifts as part of the eventual normalization of the financial markets, by which we mean lower average annual returns with higher volatility. We see these developments as being accompanied by an eventual increase in the cost of capital, driven both by higher interest rates and wider credit spreads, which is a natural result of an ongoing economic expansion. A higher cost of capital usually has a significant and negative effect on highly leveraged businesses.

We thought it might be instructive to look at relative performance following historical underperformance periods. We identified 36 five-year spans from the Russell 2000 inception when PMF underperformed the Russell 2000 by 3.0% or more on an average annual basis. We then looked at the relative performance, as measured by excess returns, in the subsequent five-year periods. In 92% of them (33 of the 36), the Fund outpaced its benchmark. Moreover, the average excess return for all 36 subsequent average annual five-year periods was a healthy 6.4% per year.

Past performance is no guarantee of future results. That being said, and looking closely at history, particularly within the context of the highly anomalous period we have just endured, we suspect that investors may be able to appreciate why we are so optimistic about the prospects for both the relative and absolute performance of our disciplined, value-oriented approaches.

PMF vs. Russell 2000

Subsequent 5-Year Excess Return Following Each Monthly Rolling 5-Year Period of Relative Underperformance in Excess of 300 BPS (%)

Royce Pennsylvania Mutual Fund [PENNX]

Average Annual Total Returns as of Quarter-End 12/31/14 (%)

| QTR* | 1 YR | 3 YR | 5 YR | 10 YR | 15 YR | 20 YR | 30 YR | 40 YR | ||

|---|---|---|---|---|---|---|---|---|---|---|

| Pennsylvania Mutual | 5.30 | -0.70 | 15.45 | 12.80 | 7.97 | 10.74 | 11.32 | 11.55 | 16.28 | |

| Russell 2000 | 9.73 | 4.89 | 19.21 | 15.55 | 7.77 | 7.38 | 9.63 | 10.27 | N/A | |

| Annual Operating Expenses: 0.93% | ||||||||||

* Not Annualized

Important Performance and Expense Information

All performance information reflects past performance, is presented on a total return basis, reflects the reinvestment of distributions, and does not reflect the deduction of taxes that a shareholder would pay on fund distributions or the redemption of fund shares. Past performance is no guarantee of future results. Investment return and principal value of an investment will fluctuate, so that shares may be worth more or less than their original cost when redeemed. Shares redeemed on or before 1/30/15 within 180 days of purchase, and after 1/30/15 within 30 days of purchase, may be subject to a 1% redemption fee. All redemption fees are payable to the Fund and are not reflected in the performance shown above; if such fees were reflected, performance would be lower. Current month-end performance may be higher or lower than performance quoted and may be obtained here. Operating expenses reflect the Fund’s total annual operating expenses for the Investment Class as of the Fund’s most current prospectus and include management fees, other expenses, and acquired fund fees and expenses. Acquired fund fees and expenses reflect the estimated amount of the fees and expenses incurred indirectly by the Fund through it’s investment in mutual funds, hedge funds, private equity funds, and other investment companies.

Important Disclosure Information

This material is not authorized for distribution unless preceded or accompanied by a current prospectus. Please read the prospectus carefully before investing or sending money. Royce Pennsylvania Mutual Fund invests primarily in small-cap stocks, which may involve considerably more risk than investing in larger-cap stocks. (Please see "Primary Risks for Fund Investors" in the prospectus.) The Fund's broadly diversified portfolio does not ensure a profit or guarantee against loss. The Fund may invest up to 25% of its net assets in foreign securities (measured at the time of investment), which may involve political, economic, currency, and other risks not encountered in U.S. investments. (Please see "Investing in Foreign Securities" in the prospectus.) Russell Investment Group is the source and owner of the trademarks, service marks, and copyrights related to the Russell Indexes. Russell® is a trademark of Russell Investment Group. The Russell 2000 is an unmanaged, capitalization-weighted index of domestic small-cap stocks. It measures the performance of the 2,000 smallest publicly traded U.S. companies in the Russell 3000 index. The performance of an index does not represent exactly any particular investment, as you cannot invest directly in an index. Standard deviation is a statistical measure within which a fund's total returns have varied over time. The greater the standard deviation, the greater a fund's volatility. Please read the prospectus for a more complete discussion of risk.

* Credit spread data source: B of A Merrill Lynch US High Yield Master II Option-Adjusted Spread