Why global currency investing still makes sense

Why global currency investing still makes sense – even amid a strong dollar

We believe there are three reasons why many investors should remain committed to a diversified global currency strategy – even if the US dollar remains strong.

By: Michael A. Cirami, Eric Stein, John R. Baur, Matthew F. Murphy, Jr., Bradford Godfrey

SUMMARY

- While the dollar has been strong and is likely to remain so, global currency investing is a relative proposition, and we expect there to be multiple opportunities in the space.

- U.S. dollar-based investors can manage and potentially benefit from the risk inherent in non-euro European currencies.

- Different countries’ currencies have historically reacted positively to broad USD strength, and active management can potentially exploit opportunities as they arise.

In recent months, financial headlines have highlighted a strong rise in the U.S. dollar (USD). Drivers of this gain have included widespread anticipation that the U.S. Federal Reserve (Fed) will raise short-term interest rates in 2015, along with an improving U.S. economy and weaker economic growth in Europe, Japan, China and other major emerging markets.

It does not appear that the trends pushing the USD higher are likely to reverse in the foreseeable future. This has led many U.S.-based investors to question their long-term commitment to a strategy of owning foreign currencies. However, we believe there are three key reasons why many investors should remain committed to allocating capital to a diversified basket of global currencies – even in an environment where the USD continues to be strong.

1: While the dollar has been strong and is likely to remain so, global currency investing is a relative proposition, and we expect there to be multiple opportunities in the space.

Because currencies trade in pairs, investing in a given currency is always a relative proposition. If an investor is “long” one currency, he or she is also inherently “short” the currency that was exchanged for the one held.

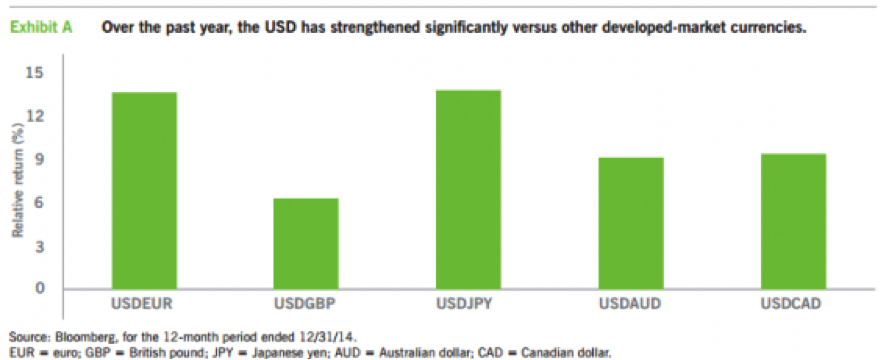

- Examples of this relationship were evident during the latest 12-month period – a year in which, true to the headlines, the USD strengthened significantly versus other developed-market currencies, particularly the euro and the Japanese yen. (See Exhibit A.)

- In the emerging-market space, the USD has certainly been strong, but not nearly as dominant. This supports our view that as the Fed eventually tightens its monetary policy, country-level fundamentals are likely to matter more and more when investing in currencies.

- In the frontier-market space, there are a number of potential opportunities, as some countries have been growing at relatively high rates and implementing multiple reforms that are starting to attract more investor capital. Examples include:

-Sri Lanka: has experienced strong growth, as it is rebuilding from decades of civil war that ended in 2009.

-Serbia: is working with the International Monetary Fund (IMF) to implement important policy reforms as it seeks to join the European Union.

Takeaway: There are still many opportunities for dollar-based investors to potentially achieve gains in non-U.S. currencies. In general, we believe it is best to avoid developed-market currencies at this point and to rely on active managers with the flexibility to select from the most attractive investments around the world, including in the emerging and frontier spaces.

2: USD-based investors can manage and potentially benefit from the risk inherent in non-euro European currencies.

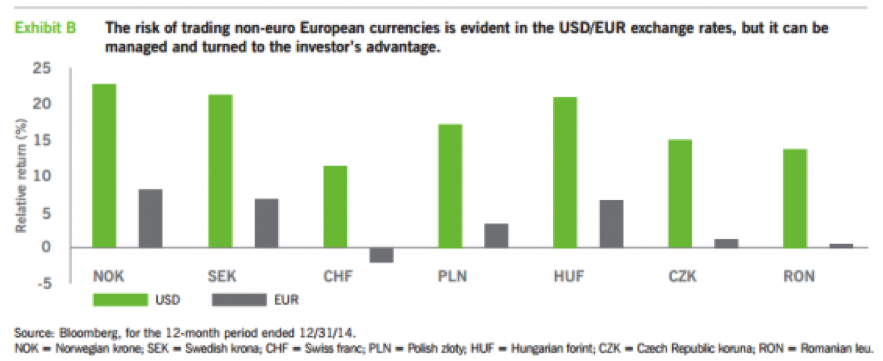

- U.S.-based investors that exchange their USD holdings for non-euro European currencies are subject to the volatility and potential for loss in the USD/EUR exchange rates. (See Exhibit B.)

- As a result, we believe it is prudent for investors to hedge out this USD/EUR risk when investing in non-euro European currencies in an effort to isolate desired exposures, protect their portfolios and capture potential gains.

- As an added incentive, the European Central Bank (ECB) is likely to further loosen its monetary policy in an attempt to weaken the euro, which may help non-euro European currencies strengthen against the euro.

Takeaway: U.S.-based investors must be aware of the risks inherent in trading non-euro European currencies. In our view, it is best to rely on active management in seeking to minimize the risk of loss, reduce overall volatility and participate in gains stemming from the ECB’s potential policy moves.

3: Different countries’ currencies have historically reacted positively to broad USD strength, and active management can potentially exploit opportunities as they arise.

Better economics and tighter monetary policy in the U.S. have historically benefited some foreign currencies based on their ties to the U.S. economy and their mix of commodity imports and exports. There are several parts to this argument:

- Historically, when the U.S. is doing well, countries that serve as its supply chain have generally benefited the most. Mexico and some emerging Asian countries are prime examples.

- Historically, oil has fallen in a strong USD environment, which bodes well for large oil importers whose industries can benefit from lower input costs, drive growth cyclically higher, narrow current account deficits or improve surpluses, and attract capital that leads to an appreciating currency. Examples include India and Korea.

- On the flip side, oil exporters are forced to accept a lower price for their primary export, which constricts growth, triggers a decline in USD reserve balances and widens current account deficits or lessens surpluses. This, in turn, tends to deter capital and leads to a depreciating currency in countries such as Russia and Nigeria.

- However, the above are not hard-and-fast rules, as valuations, carry and momentum all matter in currency investing. Active management is required to determine which currencies offer the most attractive risk/return profiles.

Takeaway: It may not be advisable to abandon foreign currency investing simply because the tail winds of the past – a loose Fed, a lackluster U.S. economy and strong growth throughout the emerging markets – have abated. Proven active managers can take advantage of mispricings across the entire opportunity set through disciplined investment decision-making.

Conclusion

Despite the broad, recent upward moves in the U.S. dollar and the likelihood of continued strength in the dollar, we believe the case for maintaining a globally diversified, actively managed currency portfolio remains sound. In our judgment, U.S.-based investors are likely best served by active managers that can:

- Exploit the entire global opportunity set of currencies, including developed markets, emerging markets and frontier markets.

- Manage and potentially benefit from swings in the USD/EUR exchange rate through its effect on non-euro European countries.

- Utilize their experience managing through multiple cycles, especially when the cycle appears to have passed an inflection point, where the factors pushing many foreign currencies higher versus the USD have waned.

About Risk

Currency: The value of foreign currencies as measured in U.S. dollars will fluctuate and may be unpredictably affected by changes in foreign currency rates and exchange control regulations, application of foreign tax laws, governmental administration of economic or monetary policies, intervention by U.S. or foreign governments or central banks, and relations between nations. Foreign: Investments in foreign instruments or currencies can involve greater risk and volatility than U.S. investments because of adverse market, economic, political, regulatory, geopolitical, or other conditions. In emerging or frontier countries, these risks may be more significant. Income Market: An imbalance in supply and demand in the income market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. Interest Rate: As interest rates rise, the value of certain income investments is likely to decline. Nondiversified: A nondiversified fund may be subject to greater risk by investing in a smaller number of investments than a diversified fund.

No Fund is a complete investment program and you may lose money investing in a Fund. Regulatory changes may adversely affect securities markets and market participants, as well as the Fund’s ability to implement its strategy. A Fund may engage in other investment practices that may involve additional risks and you should review the Fund prospectus for a complete description.

Past performance is no guarantee of future results.

About Eaton Vance

Eaton Vance Corp. is one of the oldest investment management firms in the United States, with a history dating to 1924. Eaton Vance and its affiliates offer individuals and institutions a broad array of investment strategies and wealth management solutions. The Company’s long record of exemplary service, timely innovation and attractive returns through a variety of market conditions has made Eaton Vance the investment manager of choice for many of today’s most discerning investors. For more information, visit eatonvance.com.

The views expressed in this Insight are those of the authors and are current only through the date stated at the top of this page. These views are subject to change at any time based upon market or other conditions, and Eaton Vance disclaims any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Eaton Vance are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Eaton Vance fund.

This Insight may contain statements that are not historical facts, referred to as forward-looking statements. Future results may differ significantly from those stated in forward-looking statements, depending on factors such as changes in securities or financial markets or general economic conditions.

Before investing, investors should consider carefully the investment objectives, risks, charges and expenses of a mutual fund. This and other important information is contained in the prospectus and summary prospectus, which can be obtained from a financial advisor. Prospective investors should read the prospectus carefully before investing.

©2015 Eaton Vance Distributors, Inc. | Member FINRA/SIPC | Two International Place, Boston, MA 02110 | 800.836.2414 | eatonvance.com