SUMMARY

- Municipal bonds outperformed nearly all other asset classes in 2014.

- After a year of strong gains, we think municipal bonds remain attractive entering 2015.

- Municipal bond investors should focus on taxable-equivalent yields, valuations, credit quality and supply/demand dynamics.

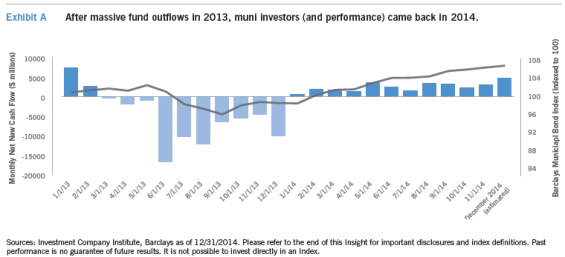

After a very challenging year for the municipal bond (muni) market in 2013, munis staged a dramatic comeback in 2014, outperforming nearly all other asset classes, including U.S. Treasurys, investment-grade and high-yield corporate bonds, and domestic equities.

So what comes next after an impressive year of outperformance?

Muni bond returns benefited largely from declining interest rates in 2014, a scenario that few market participants expected. While munis’ performance in 2014 appeared stunning relative to 2013, it was our belief that investors overlooked several reasons why munis were so compelling at 2013 year-end, including the impact of higher tax rates and a steep muni yield curve.

Our assessment of the market proved to be correct and, unfortunately, those who fled munis in 2013 missed out on a great investment opportunity (Exhibit A).

With longer-term interest rates unlikely to continue their downward trend in 2015, investors might ask why they should stay the course with munis in 2015. We believe the basic tenets of holding munis have not change. These include providing federal tax-exempt income, diversification and relative credit stability. In addition, for 2015, we think that there are several timely reasons why investors should favor muni bonds, including:

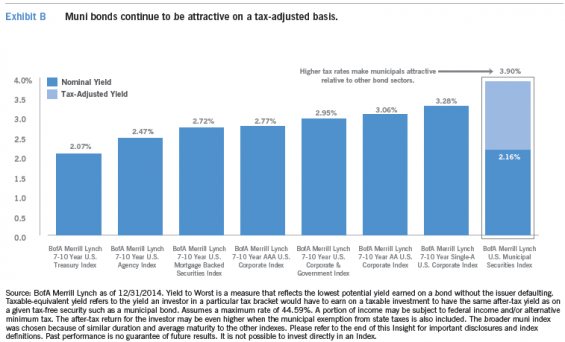

- Munis continue to be attractive on a tax-adjusted basis.

- Valuations continue to be attractive.

- Issuers’ credit quality continues to be a positive.

- Munis may still benefit from favorable supply/demand dynamics.

- Intermediate- and long-term munis may outperform based on Fed action.

- When is a 2% coupon really closer to a 4% coupon? The federal tax-exempt status of income from muni bonds creates a taxable-equivalent rate for munis that is higher than comparable duration Treasurys and corporate bonds.

- As of December 31, 2014, munis (as measured by the BofA Merrill Lynch U.S. Municipal Securities Index) were yielding 2.16% on a pretax basis. Under the current maximum rate of 44.59%, which includes the new tax from the Affordable Care Act and itemized deduction limitations, the taxable-equivalent rate climbs to 3.90%.

- With higher tax rates that remain in effect for the 2014 and 2015 tax years, we think munis continue to be attractive on a tax-adjusted basis compared to other fixed-income alternatives, as the chart above illustrates.

- In his 2015 State of the Union address, President Obama called for increasing tax rates on long-term capital gains and qualified dividends. Although the likelihood of these tax increases gaining approval in Congress appears to be very low, the president’s proposal shows that future tax hikes, particularly around investment income, are possible.

- With a divided government at the federal level, we do not anticipate comprehensive tax reform that would impact the tax-exempt status of municipal bonds in 2015.

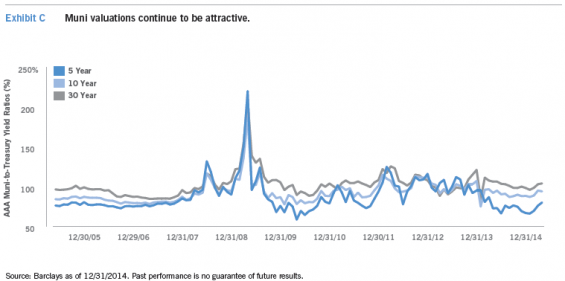

- After munis outperformed other fixed-income sectors in 2014, such as corporate bonds and U.S. Treasurys, investors may think that munis are too rich on a valuation basis. However, we think muni bond yields still appear attractive compared to Treasurys.

- As of December 31, 2014, AAA-rated municipals on the long end of the curve yielded over 100% of similar-maturity Treasury securities. Historically, when investors have purchased municipal bonds at high ratios, they have experienced outperformance, although past performance is no guarantee of future results.

- Historically, when Treasury yields rise, muni-to-Treasury ratios that are classified as cheap have tended to cushion the adverse impact of rising rates.

- We think muni-to-Treasury ratios may still have to adjust to a new world of higher tax rates. For example, investors in certain federal tax brackets historically believed that a 30-year muni with a muni-to-Treasury ratio of 85% was rich. With higher tax rates on investment income, we think that the ratio would have to be lower in order for 30-year munis to be considered rich.

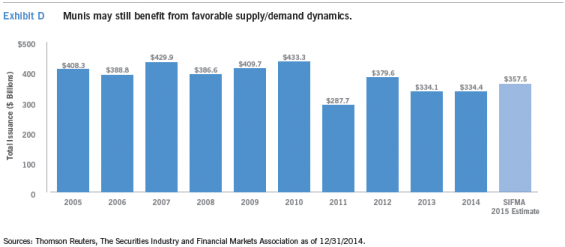

- Over the past few years, a decline in muni bond issuance has been a positive tail wind. Looking ahead in 2015, a survey of underwriters and dealers by the Securities Industry and Financial Markets Association (SIFMA) shows that issuance is expected to climb to $357.5 billion in 2015.

- We think that this expected pickup in issuance will not be overwhelming to the market. However, looking beyond this year, we also recognize there are significant infrastructure requirements that have been deferred, as state governments and municipalities have favored austerity since the financial crisis of 2008.

- State and local budgets have improved as the financial crisis moves further back in the rearview mirror. These dynamics could help drive muni bond issuance in the future; that greater supply could become a headwind for the market. That said, historically, there has been a long lead time before new issues are brought to market, so we do not anticipate outsized issuance in 2015.

- Meanwhile, we expect demand for muni bonds to remain strong. Investor demand is typically robust leading up to Tax Day in April, as investors come to realize the full impact of higher tax rates. In addition, increased volatility in the general fixed-income market may create a flight to quality, where we think munis may benefit from their stable and, in many cases, improving credit quality.

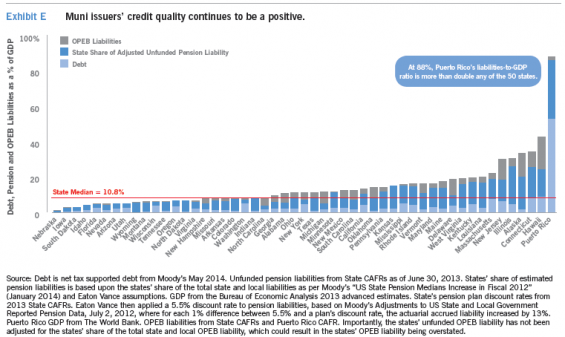

- Thanks to an improving U.S. economy, the credit outlook for the majority of muni issuers is positive. Historically, muni credit has generally improved as the economy has strengthened.

- On a year-over-year basis, state tax revenues have increased in 17 out of the last 18 quarters (according to the Rockefeller Institute, data through the second quarter of 2014). And as the chart above shows, most state’s long-term liabilities are manageable. The positive environment has contributed to a current muni default rate of 0.29% (according to Municipal Market Advisors).

- We think muni issuers’ strong credit quality reflects their resiliency in the midst of broader economic themes, which may be a negative for certain other asset classes (e.g., the adverse impact of oil price declines on certain high-yield bond issuers). On a relative basis, we think munis offer a particularly compelling source of income.

- Looking ahead, Puerto Rico could be the so-called elephant in the room, given the high likelihood of a restructuring at PREPA (the islands publicly owned utility) in 2015. We do think broad investor reaction to a PREPA restructuring will be muted; however, if additional Puerto Rico entities were to initiate debt restructurings, it could cause a broad sell-off in munis. In this scenario, we would consider that a potential value opportunity.

- Aside from Puerto Rico, there are other credit risks muni investors should be mindful of. As a result of new accounting rules, unfunded pension liabilities will now appear on governmental balance sheets and mandated lower discount rates will increase unfunded pension liabilities. Additionally, a potential downgrade of Illinois’ credit rating to the BBB-rating category could generate negative headlines for the market.

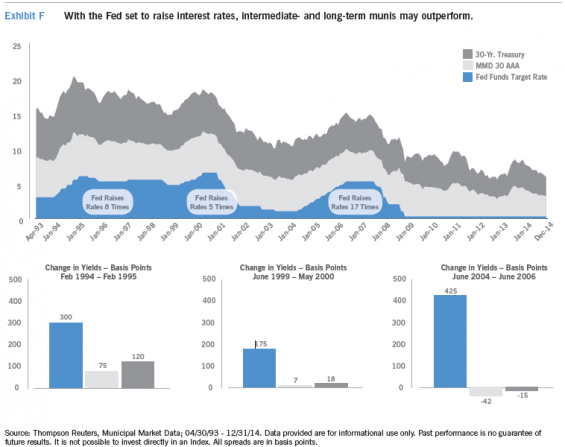

- We believe the Federal Reserve (Fed) will raise rates in 2015, the first time the Fed has increased the fed funds rate since 2006. Because of this shift in monetary policy, we expect short-term U.S. rates to increase more than long-term U.S. rates (which we believe will remain low due to continuing overall slow global growth), resulting in a flatter yield curve.

- Muni bond yields tend to move with U.S. Treasury yields. So, in the possible scenario of a flattening yield curve with short-term rates rising, we think intermediate- and long-term bonds may outperform short-term bonds.

- Investors may be concerned that a potential rising fed funds rate will lead to increased volatility for long-term municipal bonds. However, as the chart above shows, rising short-term fed funds rates have not historically led to an expected high level of volatility for long-term municipal bonds.

Get back to the basics of muni bond investing

It is unlikely muni bonds will experience the same kind of price appreciation we saw in 2014. However, we do not think that is a reason to abandon the asset class in 2015. On the contrary, we think muni bonds should be an anchor of a portfolio, and the reasons are clear:

- They provide income that is exempt from federal taxes.

- The credit quality of most muni issuers is stable.

- Muni bonds may provide diversification and volatility reduction to an overall portfolio.

- Muni valuations are relatively attractive versus other fixed-income asset classes.

With volatility in the bond markets expected to increase in 2015, we think investors should consider muni bonds as part of their overall asset allocation. However, credit research remains very important. With more than 60,000 issuers, over one million CUSIPs and about $3.7 trillion outstanding, we believe skilled professional management and credit research are absolutely necessary to sort through the diverse muni landscape.

Index Definitions

30-Year AAA Municipal Market Data (MMD) Index is an index of AAA-rated general obligation bonds.

BofA Merrill Lynch 7-10 Year AA U.S. Corporate Index is an unmanaged index that tracks the performance of U.S. dollar-denominated investment-grade corporate debt publicly issued in the U.S. domestic market with a remaining term to final maturity greater than or equal to 7 years and less than 10 years and rated AA1 through AA3, inclusive.

BofA Merrill Lynch 7-10 Year AAA U.S. Corporate Index is an unmanaged index that tracks the performance of U.S. dollar-denominated investment-grade corporate debt publicly issued in the U.S. domestic market with a remaining term to final maturity greater than or equal to 7 years and less than 10 years and rated AAA.

BofA Merrill Lynch 7-10 Year Single-A U.S. Corporate Index is an unmanaged index that tracks the performance of U.S. dollar-denominated investment-grade corporate debt publicly issued in the U.S. domestic market with a remaining term to final maturity greater than or equal to 7 years and less than 10 years and rated A1 through A3, inclusive.

BofA Merrill Lynch 7-10 Year U.S. Agency Index is an unmanaged index that tracks the performance of U.S. dollar-denominated U.S. agency senior debt issued in the U.S. domestic market with a remaining term to final maturity greater than or equal to 7 years and less than 10 years.

BofA Merrill Lynch 7-10 Year U.S. Corporate & Government Index is an unmanaged index that tracks the performance of U.S. dollar-denominated investment-grade debt publicly issued in the U.S. domestic market, including U.S. Treasury, U.S. agency, foreign government, supranational and corporate securities with a remaining term to final maturity greater than or equal to 7 years and less than 10 years.

BofA Merrill Lynch 7-10 Year U.S. Mortgage Backed Securities Index is an unmanaged index that tracks the performance of U.S. dollar-denominated fixed-rate and hybrid residential mortgage pass-through securities publicly issued by U.S. agencies in the U.S. domestic market with an average life greater than or equal to 7 years and less than 10 years.

BofA Merrill Lynch U.S. Municipal Securities Index is an unmanaged index that tracks the performance of U.S. dollar-denominated investment-grade tax-exempt debt publicly issued by U.S. states and territories, and their political subdivisions, in the U.S. domestic market.

BofA Merrill Lynch 7-10 Year U.S. Treasury Index tracks the performance of U.S. dollar-denominated sovereign debt publicly issued by the U.S. government in its domestic market with a remaining term to final maturity greater than or equal to 7 years and less than 10 years.

About Eaton Vance

Eaton Vance Corp. is one of the oldest investment management firms in the United States, with a history dating to 1924. Eaton Vance and its affiliates offer individuals and institutions a broad array of investment strategies and wealth management solutions. The Company’s long record of exemplary service, timely innovation and attractive returns through a variety of market conditions has made Eaton Vance the investment manager of choice for many of today’s most discerning investors. For more information, visit eatonvance.com.

About Risk

An imbalance in supply and demand in the municipal market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. There generally is limited public information about municipal issuers. As interest rates rise, the value of certain income investments is likely to decline. Longer-term bonds typically are more sensitive to interest-rate changes than shorter-term bonds. Investments in income securities may be affected by changes in the creditworthiness of the issuer and are subject to the risk of nonpayment of principal and interest. The value of income securities also may decline because of real or perceived concerns about the issuer’s ability to make principal and interest payments. A portion of municipal bond income may be subject to alternative minimum tax. Income may be subject to state and local tax.

The views expressed in this insight are those of the authors and are current only through the date stated at the top of this page. These views are subject to change at any time based upon market or other conditions, and Eaton Vance disclaims any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Eaton Vance are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Eaton Vance fund. Eaton Vance does not provide legal or tax advice. The discussion herein is general in nature and is provided for informational purposes only. There is no guarantee as to its accuracy or completeness. Individuals should consult their own legal and tax counsel as to matters discussed.

Before investing, investors should consider carefully the investment objectives, risks, charges and expenses of a mutual fund. This and other important information is contained in the prospectus and summary prospectus, which can be obtained from a financial advisor. Prospective investors should read the prospectus carefully before investing.

©2015 Eaton Vance Distributors, Inc. | Member FINRA/SIPC | Two International Place, Boston, MA 02110 | 800.836.2414 | eatonvance.com