After its debt recovery act is struck down, Puerto Rico faces significant short-term and long-term liquidity challenges.

Author: Municipal Insight Committee

SUMMARY

- Puerto Rico faces several near-term challenges, paramount of which is perilously low liquidity, particularly at its numerous public corporations.

- Over the long term, the Commonwealth of Puerto Rico will need to address its considerable debt load, significantly underfunded pension plans and increasing health care costs.

- We think that investors need to be mindful of the risks Puerto Rico headlines pose to the broader muni market.

Puerto Rico’s fiscal challenges are once again making headlines in the municipal bond market. Earlier this month, a federal district court struck down a law passed in June 2014 to grant the Commonwealth’s public agencies eligibility for debt restructuring. The ruling leaves Puerto Rico with no definitive forum to restructure its debts, and investors are now considering what the broader effects on the muni market may be.

While we believe the federal district court’s decision is a slight positive for bondholders, we recognize that the ruling does not change the underlying fact that Puerto Rico faces major challenges with its heavy debt load and continued economic decline. With the constant flow of news regarding Puerto Rico’s creditworthiness, we want to share our views on the Commonwealth, the island’s short- and long-term challenges, and what muni investors should be mindful of going forward.

How Puerto Rico found itself in “no man’s land”

Puerto Rico’s debt woes are not a new development. The Commonwealth is burdened by more than $70 billion in debt, which includes the debt of its various public corporations and agencies:

- Puerto Rico Electric Power Authority (PREPA)

- Puerto Rico Highways and Transportation Authority (PRHTA)

- Puerto Rico Aqueduct and Sewer Authority (PRASA)

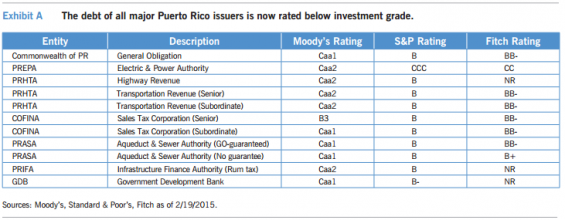

On February 12, 2015, Standard & Poor’s downgraded its rating on the Commonwealth of Puerto Rico general obligation (GO) and related public corporations, including sales tax debt from the Puerto Rico Sales Tax Financing Corporation, known as COFINA, to B with a negative outlook (Exhibit A). Prior to the downgrade, GO debt was rated BB and COFINA was rated BBB. The below-investment-grade rating on all Puerto Rico debt is largely due to consistent budget deficits, a weak economy, high unemployment and a shrinking population. Further, liquidity at the Government Development Bank of Puerto Rico (GDB), the territory’s financing arm, has declined sharply and substantial demands for funds are on the horizon.

Because Puerto Rico and its agencies are not eligible for Chapter 9 of the bankruptcy code, and because PREPA was perilously close to a payment default, the Commonwealth in June 2014 passed the Puerto Rico Public Corporation Debt Enforcement and Recovery Act (the Recovery Act), designed to grant PREPA, PRHTA and PRASA the ability to restructure their debt. The Recovery Act excluded Puerto Rico’s GO debt as well as COFINA.

Can the Recovery Act recover?

When the Recovery Act was passed, it was viewed as a negative for bondholders; Puerto Rico was essentially changing the rules and the provisions of the Recovery Act were very debtor-friendly at the expense of creditors. But, in a February 6, 2015 ruling, Judge Francisco A. Besosa found that the Recovery Act was unconstitutional.

While some initially trumpeted the ruling as a win for investors, taking a longer-term view, we think the lack of a delineated framework for restructuring should be troubling for bondholders. We liken it to playing a game without a referee. Puerto Rico has already vowed to appeal the ruling, meaning negotiations could drag on unless Puerto Rico wins congressional approval for access to Chapter 9 of the U.S. Bankruptcy code. The island’s representative in Congress, Pedro Pierluisi, has proposed that Puerto Rico focus its efforts on working toward congressional approval.

Puerto Rico’s short-term liquidity strains: PREPA and PRHTA

While the federal district court ruling is significant, Puerto Rico faces a near-term challenge with PREPA, as there is a sizable debt service payment due on July 1, 2015. As such, we think PREPA is still likely to default in 2015, regardless of whether or not the Restructuring Act is revived. According to the forbearance agreement reached with PREPA creditors, the power authority must submit a restructuring plan by March 2015, although this deadline is likely to be pushed back to June 2015. We think a PREPA default could have an impact on the broader muni market, depending on the recovery rate that bondholders receive.

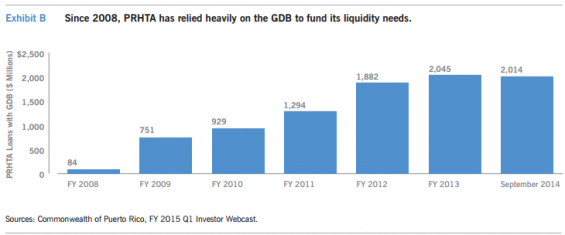

The island’s highway authority is another major near-term challenge. Historically, PRHTA has relied heavily on the GDB for operating liquidity, which has resulted in PRHTA loans representing more than 20% of the GDB’s loan book, as Exhibit B shows. Since late 2014, Puerto Rico has been working to borrow between $2 billion and $2.9 billion to repay the funds the highway authority borrowed from the GDB. Puerto Rico Infrastructure and Finance Authority (PRIFA) plans to sell bonds backed by higher taxes on imported petroleum, using the potential proceeds to pay off the PRHTA debt and, in turn, improve the GDB’s liquidity position.

However, we feel that placing a $2 billion bond deal with investors will be a significant challenge. Puerto Rico’s $3.5 billion bond deal – placed less than a year ago – has underperformed significantly, with bonds having traded down from $93 at issuance to around $82 currently.

Puerto Rico’s long-term liquidity: Dire straits

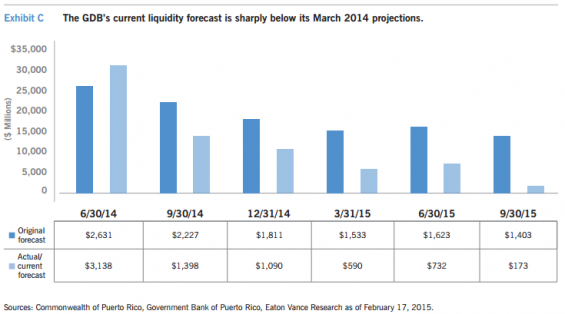

In our mind, completion of the PRIFA bond deal is of the utmost importance to the Commonwealth and the GDB, as the GDB’s liquidity position appears to be untenable. Puerto Rico’s fiscal 2015 revenues year-to-date are $117 million behind fiscal year 2014 collections. And in fiscal year 2014, Puerto Rico’s revenues ultimately missed budget by $568 million.

By its own estimates, if another miss of this magnitude is realized in 2015, the GDB and Commonwealth liquidity could be exhausted early in fiscal year 2016 (Exhibit C). If the PRIFA deal is completed, Puerto Rico may gain some breathing room. Unfortunately, solving the short-term liquidity challenge does little to help Puerto Rico’s longer-term fiscal position, in our view.

Generally speaking, Puerto Rico’s fixed costs are rising at a time when revenues are flat to declining. First, COFINA debt service costs are expected to increase from $655 million in 2015 to $800 million in 2020, and COFINA debt service eventually peaks at $1.8 billion in 2041. Debt service on GO bonds is also increasing at a rapid pace, and in fiscal 2016, the island’s GO debt service will increase by $612 million. Combined with the increases in COFINA debt service, Puerto Rico’s general fund will remain under considerable stress. The story is similar with the GDB: Maturing debt is set to increase from $477 million in fiscal 2015 to $882 million in fiscal 2016.

Don’t overlook pension and health care challenges

The media and investors have rightfully focused on the liquidity issues facing the Commonwealth and the potential restructuring of PREPA and PRHTA, as these are the most immediate challenges facing Puerto Rico’s lawmakers. However, less attention has been paid to the pension and health care costs that the island must eventually address.

Let’s take the pension issue first. As of the latest data available through June 30, 2013, Puerto Rico’s Employee Retirement System (ERS) has an unfunded liability of $23 billion, which equates to a lowly 3.1% funded ratio. If the pension assets are depleted, the Commonwealth’s “pay-as-you-go” annual contribution would be approximately $1.6 billion, which compares to a $638 million contribution in 2013.

Meanwhile, Puerto Rico’s health insurance program is another strain on the island’s finances. The Commonwealth states, “The fiscal stability of the Commonwealth’s health insurance program is one of the largest budgetary challenges facing the Commonwealth.” In Puerto Rico’s latest disclosure, it estimates that without significant changes and the renewal of ACA funds through Congress, “The annual deficit of the health insurance program could rise to as much as $2 billion by fiscal year 2019, from $59 million in fiscal year 2014.” Even when considering the numerous challenges Puerto Rico faces, the potential budgetary hole in the health insurance program is shocking to us.

Puerto Rico’s current solution: Overhaul the tax system

Liquidity is the short-term challenge, while rising debt service, declining revenues, and pension and health care costs are a long-term strain for a Commonwealth with no economic growth. So, what are lawmakers doing to address these challenges?

Puerto Rico Governor Alejandro García Padilla has proposed a complete overhaul to Puerto Rico’s tax system. It is widely accepted that Puerto Rico suffers from tax evasion – the governor noted in a statement that only 12,000 residents file tax returns with annual income of $150,000 or higher, “which is in stark contrast to the luxury cars and houses we see on our streets.”

The new tax code presented would replace the island’s current Sales and Use Tax with a Value-Added Tax (VAT), which bases taxes paid on consumption rather than income. The proposal eliminates income taxes for 850,000 taxpayers and lowers the tax rates for corporations by 25%. Instead, citizens will pay taxes on what they purchase.

There are several takeaways from the proposal. First, if the overhaul gained enough support to pass, it would take both time and money to implement. Auditor KPMG estimates that implementing a VAT would cost more than $108 million in fiscal 2015. Beyond that, there could be resistance to adoption. For example, KPMG notes that past changes to the tax system were announced without implementation guidance or a scheduled rollout.

Further, we think one of the key assumptions is overly optimistic. KPMG estimates that a VAT of 16% with 75% compliance would pull in additional annual revenues of $3.2 billion after COFINA payments. We think the estimate of 75% may be too aggressive, as the current tax laws have roughly 55% compliance, and invariably people and corporations may adjust their behavior to escape paying taxes. Additionally, we question the view that Puerto Rico, which currently sees annual tax revenues of less than $9 billion, can increase this amount by more than 30% by switching to a VAT tax system.

Will Puerto Rico affect the broader muni market?

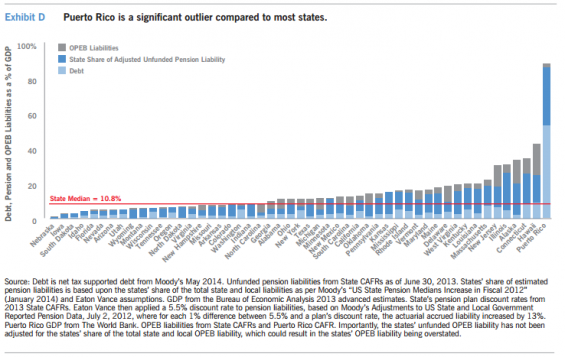

We think that Puerto Rico’s unique credit challenges have limited bearing on the credit outlook of the remainder of the muni market. With more than 60,000 issuers, over one million CUSIPs and about $3.7 trillion outstanding debt, making generalizations about the broad muni market’s outlook is challenging, if not impossible. For example, while most states’ long-term liabilities are manageable, Puerto Rico remains a significant outlier, as Exhibit D shows.

Despite the negative headlines and fears of a Puerto Rico default, credit spreads for the muni market have contracted and net flows into municipal bond funds were positive in 2014 and remain so year-to-date in 2015. Although Puerto Rico still faces significant challenges to repair its ailing economy, we think a focus on credit selection may help investors find value in a market that is largely being shunned.

As mentioned, we do believe that PREPA is likely to default in 2015. However, any other Puerto Rico default could potentially have a destabilizing effect on the broader muni market. For example, when Detroit filed for bankruptcy in 2013, there was no impact on the credit quality of other muni issuers. However, the headline risk of the bankruptcy pressured the broader market. If a similar scenario related to Puerto Rico were to occur, we could consider any broad weakness as a potential opportunity for long-term muni investors. Credit research will remain paramount, and we believe an experienced, skilled investment manager can help navigate the muni market during times of volatility.

About Eaton Vance

Eaton Vance Corp. is one of the oldest investment management firms in the United States, with a history dating to 1924. Eaton Vance and its affiliates offer individuals and institutions a broad array of investment strategies and wealth management solutions. The Company’s long record of exemplary service, timely innovation and attractive returns through a variety of market conditions has made Eaton Vance the investment manager of choice for many of today’s most discerning investors. For more information, visit eatonvance.com.

About Risk

An imbalance in supply and demand in the municipal market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. There generally is limited public information about municipal issuers. As interest rates rise, the value of certain income investments is likely to decline. Longer-term bonds typically are more sensitive to interest-rate changes than shorter-term bonds. Investments in income securities may be affected by changes in the creditworthiness of the issuer and are subject to the risk of nonpayment of principal and interest. The value of income securities also may decline because of real or perceived concerns about the issuer’s ability to make principal and interest payments. A portion of municipal bond income may be subject to alternative minimum tax. Income may be subject to state and local tax.

The views expressed in this update are those of the authors and are current only through the date stated at the top of this page. These views are subject to change at any time based upon market or other conditions, and Eaton Vance disclaims any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Eaton Vance are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Eaton Vance fund. Eaton Vance does not provide legal or tax advice. The discussion herein is general in nature and is provided for informational purposes only. There is no guarantee as to its accuracy or completeness. Individuals should consult their own legal and tax counsel as to matters discussed.

Before investing, investors should consider carefully the investment objectives, risks, charges and expenses of a mutual fund. This and other important information is contained in the prospectus and summary prospectus, which can be obtained from a financial advisor. Prospective investors should read the prospectus carefully before investing.

©2015 Eaton Vance Distributors, Inc. | Member FINRA/SIPC | Two International Place, Boston, MA 02110 | 800.836.2414 |eatonvance.com