China Moves Cautiously Toward a New Normal

March 13, 2015

Chinese Premier Li Keqiang surprised very few when he outlined this year’s growth goals at the recent National People’s Congress. His speech codified the government’s growth target of around 7% for the year and maintained the commitment to creating more than 10 million jobs in 2015 and maintaining a 4.5% unemployment rate.

More importantly, he acknowledged that China would have to adjust to a “new normal.” The country is in the midst of a delicate rebalancing from investment-led to consumption-led growth. The state faces the tall order of sustaining targets for expansion while undertaking sometimes- painful reforms.

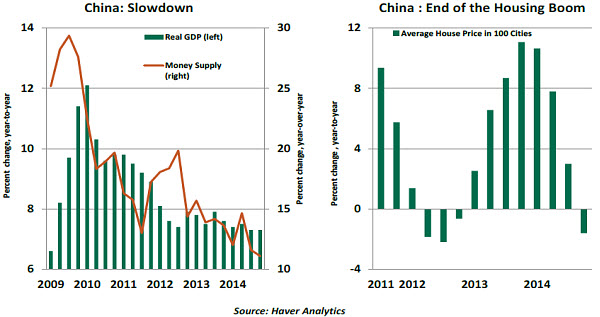

Despite the beneficial influence of low oil prices, China may be challenged to meet its growth objective in 2015, with signs of an accelerating slowdown present in the combined January-February statistics. (The two-month perspective, which covers the Lunar New Year period, was required to adjust for significant seasonality around the holiday.)

The data point to serious fundamental weakness caused by reverberations from the weakening real estate sector. Thus far this year, nearly every economic indicator, including industrial production, urban investment and retail sales, is growing more slowly on a year-over-year basis. The result has fueled speculation that first-quarter annualized gross domestic product (GDP) will come in below 7%.

This year, the Central Committee intends to reform local government financing, state-owned enterprises and the banking sector. On almost all fronts, new policies will highlight the Catch-22 China faces of creating lasting change without disrupting social stability.

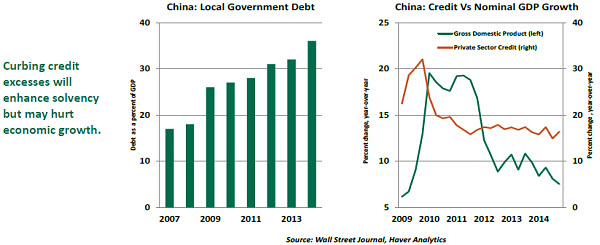

This challenge is especially pronounced in the case of local government finances, where authorities are saddled with short-duration, high-interest debt. Regional leaders have shown a proclivity to utilize off-balance-sheet entities known as local government financing vehicles (LGFVs) to circumvent restrictions on direct borrowing. With the health of this debt coming into some question, the central government was tasked with determining how much debt the sovereign should back.

Beijing has responded to the issues by proposing an initial restructuring of 1 trillion yuan ($160 billion) in local government debt. The figure is small, considering that total debt of regional governments in China is estimated at 24 trillion - 30 trillion yuan. But it should help in the short term by reducing interest costs and offering a little budgetary wiggle room. Longer-term, the underlying root of the problem still needs to addressed: local governments have tended to overuse leverage to meet growth targets. As this practice is curbed, public investment may diminish.

Comprehensive banking reform, which will re-shape how households invest and borrow, is definitely needed. Credit growth has far outstripped GDP growth over the past several years, and some are concerned that this is not sustainable. However, more-sensible banking practices may, in the short run, make it harder to reach economic objectives.

Beijing has likely judged that the banking sector is key to maintaining growth stability. The People’s Bank of China’s (PBoC) end-2014 loan officer survey noted that demand for credit was the weakest since the Global Financial Crisis. In response, the PBoC cut benchmark interest rates and reserve requirements to stimulate loan demand. The central bank faces the task of balancing systemic concerns with the need for economic growth, but the wisdom of encouraging overleveraged borrowers to add additional debt can be debated. The efficacy of these actions is also in question as highly leveraged companies lose their appetite for additional debt.

As for state-owned enterprises, the government has proposed some promising reforms. However, while outlining measures to make the firms profitable enough to go public by 2025, Beijing has not really addressed the overarching power the state-owned companies can exert. In fact, the plans as proposed would consolidate companies, creating even-larger enterprises and concentrating power even further. Call for large-scale privatization appears to be shelved for now, perhaps out of concerns for the potential instability that would follow.  On other fronts, the anti-corruption campaign that has ensnared countless officials will continue taking its toll on the economy. The fear of prosecution has a direct impact on spending as ostentatious displays of wealth — from luxury purchases to lavish Lunar New Year celebrations — are scaled back. Statements out of China indicate no slowdown in the campaign; in fact, most signposts point to the opposite conclusion. As with many of the reform measures, the short-term impact will be a drag on the economy, but the long-term benefits of a successful and balanced campaign could include lower socio-economic tensions.

On other fronts, the anti-corruption campaign that has ensnared countless officials will continue taking its toll on the economy. The fear of prosecution has a direct impact on spending as ostentatious displays of wealth — from luxury purchases to lavish Lunar New Year celebrations — are scaled back. Statements out of China indicate no slowdown in the campaign; in fact, most signposts point to the opposite conclusion. As with many of the reform measures, the short-term impact will be a drag on the economy, but the long-term benefits of a successful and balanced campaign could include lower socio-economic tensions.

The old adage about living in interesting times seems to be the order of the day for China. As the United States and European Union move steadily toward recovery, the engine that powered the world through the global economic morass of recent years is slowing down. Slowing growth is inevitable as an economy matures; the real question revolves around the efficacy of the government’s policy response. China must take advantage of its opportunity to address its structural vulnerabilities and retool the economy.

Household Debt Ratios Still Present Challenges

The easy monetary policy stances of the European Central Bank (ECB), Bank of Japan, Bank of Canada and Reserve Bank of Australia aim to stimulate economic growth. Consumer spending is a major driver of growth in these industrialized economies.

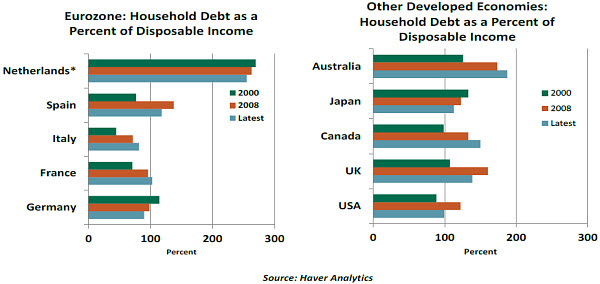

Accommodative monetary policy will be more successful in delivering its objectives if household balance sheets are healthy. An overview of household debt in major industrialized nations suggests that deleveraging shows progress in the United States, United Kingdom and Spain. But leverage has increased or held close to the peak among other industrialized economies, despite the number of years that have passed since the Global Financial Crisis.

The charts below illustrate how household deleveraging has proceeded across countries.

At the outset, it is important to cautiously compare absolute leverage ratios across countries. Data definitions are not entirely harmonious across countries. For example, the Canadian measures include the debt of unincorporated businesses that is usually part of corporate debt in other countries.

Still, the trends over time are telling. Household borrowing in the United States, United Kingdom, Spain and Germany has moderated since 2008; these countries are among those showing the best economic performance.  Mortgage debt is the largest component of household debt in advanced economies. Research indicates a correlation between increases in housing debt and real estate prices across countries. If policy encourages homeownership, it translates into higher home prices and an increase in household debt.

Mortgage debt is the largest component of household debt in advanced economies. Research indicates a correlation between increases in housing debt and real estate prices across countries. If policy encourages homeownership, it translates into higher home prices and an increase in household debt.

A number of countries are still experiencing a spiral of very strong real estate prices and an associated rise in mortgage lending. Some might suggest that this sort of secured debt should be viewed differently than revolving borrowing like credit cards. But the severe correction in U.S. home prices during 2008-2009 serves as a warning on this front. Authorities in Canada and Australia, among other countries, remain concerned about the state of the property markets and the financing associated with it.

Of the selected industrialized nations noted here, McKinsey estimates that household debt- service ratios in Australia, Netherlands, Spain and France are between 18% and 26%, while in Germany, Italy, Canada and the United States, they are in the 8% to 13% range. Highly indebted households will be hard-pressed to maintain consumer spending, even if central banks continue to maintain an accommodative posture.

Past borrowing of indebted households leaves little room for more in times of hardship, as it lowers their creditworthiness. Although signs of a disorderly unwinding of household imbalances are not on the radar screen of the industrialized economies, it is important to note that elevated debt leaves households more sensitive to adverse financial conditions, diminishes their capacity to borrow and caps the growth of consumer demand.

The experience of the United States and United Kingdom suggests that countries that have reduced the household debt ratio and debt-service burden are likely to come out ahead in the race toward full employment.

Lower Borrowing Costs in Europe – A Boon for U.S. Firms?

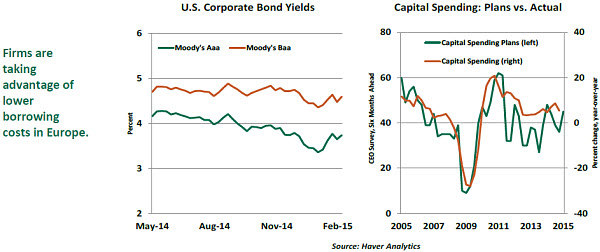

U.S. capital spending decelerated sharply in the last quarter of 2014 after two strong quarterly increases. There should be a small setback in capital spending from reductions in spending in the energy industry, but the share of this sector is modest. Business equipment spending could get a lift from spillovers from the ECB’s quantitative easing program, as the cost of funds has changed in the eurozone.

Following the ECB’s announcement of the €1.1 trillion quantitative easing program, sovereign bond yields in the eurozone declined to new lows. Investing in German bonds up to five years currently involves negative returns. Reportedly, the average yield on corporate bonds issued in Europe of late is a mere 1.08%. By contrast, investment-grade corporate bonds are trading above 3.50% in the United States.

With returns falling in Europe, U.S. companies have begun to exploit European investors’ demand for higher-yielding assets. Dealogic data indicate that €26.6 billion of bonds from U.S. borrowers have been issued in Europe this year, up significantly from the same period a year ago. Coca-Cola, Kellogg’s, AT&T and Berkshire Hathaway are some of the firms engaged in raising funds in Europe. Midsized companies are also reportedly planning to sell bonds in Europe.

Will this strategy translate into an increase in capital spending? If firms simply seek to realign their cost structures on the expectation of a stronger dollar and monetary policy tightening in the United States in the months ahead, then there is no net gain in capital spending. However, recent data point to a constructive influence on capital outlays.

The CEO Confidence Survey of March 2015 shows an increase in expectations of higher capital expenditure plans during the next six months. This index is strongly correlated with the year-to-year change in the equipment-spending component of U.S. real GDP. Shipments of non-defense capital goods also rose in January.

Despite the likely reduction in energy-related investment spending, the early signals for growth in capital spending are positive and should be reinforced by the feedback from overall growth of the economy.