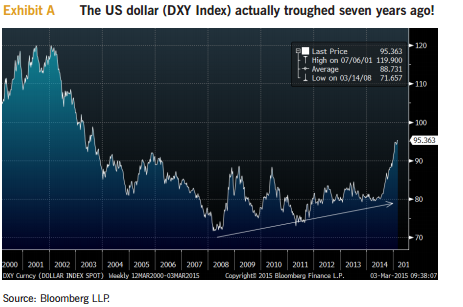

Our May 2013 report was titled “The Dollar isn’t the Peso anymore,” and in that report we rebutted the argument that the U.S. dollar was doomed because the U.S. government was “printing money.” We pointed out that despite the general consensus that the USD was a weak currency, the DXY Index had actually troughed in the spring of 2008 (see Exhibit A).

Now in the seventh year of the U.S. dollar rally, we still look for a stronger USD ahead. Many observers, including the Fed, continue to worry about inflation, but the USD is being supported by the deflation of the global credit bubble. A strong USD and disinflation/deflation seem more likely than inflation so long as global overcapacity forces nations to fight for market share and depreciate their currencies.

The ongoing deflation of the global credit bubble

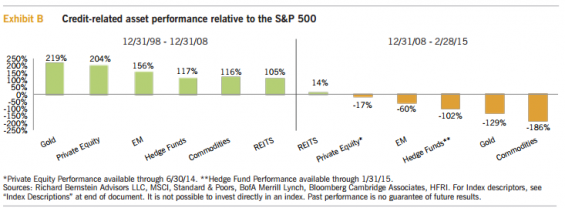

Investors apparently still don’t fully understand the deflation of the global credit bubble, and continue to focus on credit-related asset classes. Exhibit B highlights the relative performance versus the S&P 500 of credit-related asset classes during the credit bubble and afterward. Whereas credit-related asset classes handily outperformed as the credit bubble inflated, they have generally underperformed since the credit bubble began deflating in 2008.

The secular investment strategy within our portfolios remains to underweight or avoid credit-related asset classes. The fact that credit-related asset classes have yet to be “discredited” despite their significant and extended underperformance suggests that the ultimate capitulation in these asset classes still lies ahead.

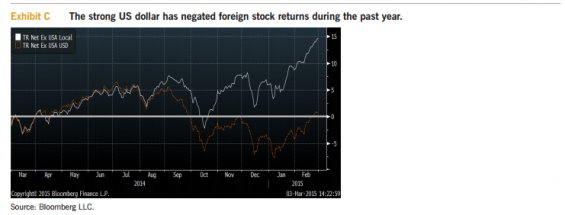

Strong dollar hurting non-US returns

For many years, currency was not an important consideration when USD-based investors invested outside the U.S. because the USD was either weakening (which contributed to USD returns of foreign assets) or was stable. However, the recent rapid appreciation of the USD has significantly curtailed USD returns of non-U.S. assets, and has made them somewhat less attractive relative to USD assets.

Exhibit C shows the performance of the MSCI All Country ex US Index in local currency terms versus that of the MSCI All Country ex US in USD terms. The performance difference between the two during the past year has been significant. Whereas in local terms non-U.S. stocks have returned over 14%, non-U.S. stocks have been only marginally positive in USD terms (+0.9%).

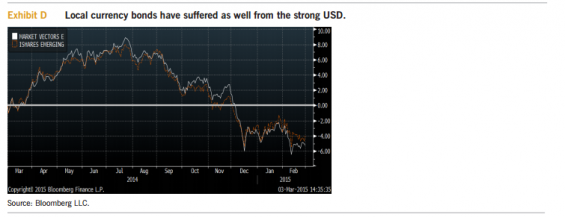

The same has been true for local currency bond funds. Exhibit D looks at the past year’s performance for two of the major local currency bond ETFs (LEMB and EMLC). Both have produced negative total returns over the past year.

The Fed

Some members of the FOMC seem to feel that interest rates need to be “normalized” in order to avert future inflation. It’s our guess that proponents of such normalization of interest rates are using models that underestimate the open structure of the U.S. economy. If the U.S. were a closed economy, then the risk of inflation would likely be considerable given the improvements in the U.S. labor markets and credit conditions. However, the U.S. is a very open economy, and the excess capacity around the world continues to exert deflation on the world’s economy.

Governments in what seems to be a growing number of countries do not want to shutter productive capacity because it would be politically unacceptable. Rather, governments would prefer to depreciate their currencies in order to try to undercut other countries and gain market share. Growing market share and increasing prices are generally mutually exclusive strategies. With the competition for global market share intensifying (i.e., recent data suggest that Japan is starting to gain market share versus Korea and China), it seems imprudent to us to “normalize” interest rates in order to fight future inflation.

However, if the Fed were to indeed “normalize” interest rates, it could escalate currency tensions around the world. The combination of the Fed prematurely increasing U.S. interest rates and non-U.S. governments depreciating foreign currencies could be quite volatile for non-U.S. assets. This may be an issue that USD-based investors haven’t fully considered given the continued inflows to nondollar assets.

The dollar isn’t the peso

The dollar isn’t the peso, and is unlikely to be a weak currency in the foreseeable future. The Fed might exacerbate the strength in the USD should it prematurely tighten monetary policy. Investors in nondollar assets have been spoiled for many years by a weakening or stable dollar. They now need to be fully aware of potential currency risks in a deflationary environment.

Our Funds are positioned accordingly.

Index Definitions

The following descriptions, while believed to be accurate, are in some cases abbreviated versions of more detailed or comprehensive definitions available from the sponsors or originators of the respective indexes. Anyone interested in such further details is free to consult each such sponsor’s or originator’s website.

The past performance of an index is not a guarantee of future results.

Each index reflects an unmanaged universe of securities without any deduction for advisory fees or other expenses that would reduce actual returns, as well as the reinvestment of all income and dividends. An actual investment in the securities included in the index would require an investor to incur transaction costs, which would lower the performance results. Indexes are not actively managed and investors cannot invest directly in the indexes.

MSCI All Country World Index (ACWI) ex US: The MSCI ACWI ex US Index is a widely recognized, free-float-adjusted, market-capitalization weighted index designed to measure the equity market performance of developed and emerging markets excluding the United States.

S&P 500: Standard & Poor’s (S&P) 500 Index. The S&P 500 Index is an unmanaged, capitalization-weighted index designed to measure the performance of the broad U.S. economy through changes in the aggregate market value of 500 stocks representing all major industries.

EM Equity: MSCI Emerging Markets (EM) Index. The MSCI EM Index is a free-float-adjusted, market-capitalization-weighted index designed to measure the equity market performance of emerging markets.

Gold: Gold Spot USD/oz. Bloomberg GOLDS Commodity. The Gold Spot price is quoted as U.S. dollars per troy ounce.

U.S. Dollar: InterContinentalExchange (ICE) US Dollar Index (DXY). The ICE US Dollar Index, indicating the general international value of the USD, averages the exchange rates between the USD and six major world currencies, using rates supplied by some 500 banks.

Commodities: S&P GSCI Index. The S&P GSCI seeks to provide investors with a reliable and publicly available benchmark for investment performance in the commodity markets, and is designed to be a “tradable” index. The index is calculated primarily on a world production-weighted basis and is comprised of the principal physical commodities that are the subject of active, liquid futures markets.

Private Equity: The Cambridge Associates LLC U.S. Private Equity Index is an end-to-end calculation based on data compiled from 1,152 U.S. private equity funds (buyout, growth equity, private equity energy and mezzanine funds), including fully liquidated partnerships, formed between 1986 and 2014.

REITS: THE FTSE NAREIT Composite Index. The FTSE NAREIT Composite Index is a free-float-adjusted, market-capitalization-weighted index that includes all tax-qualified REITs listed on the NYSE, AMEX and NASDAQ National Market.

Hedge Fund Index: HFRI Fund Weighted Composite Index. The HFRI Fund Weighted Composite Index is a global, equal-weighted index of over 2,000 single-manager funds that report to the HFR (Hedge Fund Research) database. Constituent funds report monthly net-of-all-fees performance in USD and have a minimum of $50 million under management or a twelve (12)-month track record of active performance. The Index includes both domestic (U.S.) and offshore funds, and does not include any funds of funds.

Market Vectors Emerging Markets Local Currency Bond ETF (EMLC): The Market Vectors Emerging Markets Local Currency Bond ETF (EMLC) is an exchange-traded fund incorporated in the USA. The Fund seeks investment results that correspond with the performance of the J.P. Morgan Government Bond Index - Emerging Markets Global Core.

iShares Emerging Markets Local Currency Bond ETF: The iShares Emerging Markets Local Currency Bond ETF is an exchange-traded fund incorporated in the U.S. The ETF seeks to track the Barclays Emerging Markets Broad Local Currency Bond Index.

Unless otherwise stated, index returns do not reflect the effect of any applicable sales charges, commissions, expenses, taxes or leverage, as applicable. It is not possible to invest directly in an index. Historical performance of the index illustrates market trends and does not represent the past or future performance of any fund.

This information was prepared by and has been reprinted with the permission of Richard Bernstein Advisors LLC. The views expressed herein are those of Richard Bernstein Advisors LLC. Information provided and views expressed are current only through the month stated on top of each page. The opinions herein are not necessarily those of the Eaton Vance organization and may change at any time without notice. The information contained herein has been provided for informational and illustrative purposes only and is not intended to be, nor should it be considered, investment advice or a recommendation to buy or sell any particular security. Investors should consult an investment professional prior to making any investment decision. While information is believed to be reliable, no assurance is being provided as to its accuracy or completeness.

The information in this material may not be relied upon as an indication of trading intent on behalf of any Eaton Vance Fund. It is not to be construed as representative of any Fund’s underlying allocation. This Insight may contain statements that are not historical facts, referred to as forward-looking statements. Future results may differ significantly from those stated in forward-looking statements, depending on factors such as changes in securities or financial markets or general economic conditions.

Nothing contained herein constitutes tax, legal, insurance or investment advice, or the recommendation of or an offer to sell, or the solicitation of an offer to buy or invest in, any investment product, vehicle, service or instrument. Such an offer or solicitation may only be made by delivery to a prospective investor of formal offering materials, including subscription or account documents or forms, which include detailed discussions of the terms of the respective product, vehicle, service or instrument, including the principal risk factors that might impact such a purchase or investment, and which should be reviewed carefully by any such investor before making the decision to invest. Specifically, and without limiting the generality of the foregoing, before acquiring the shares of any mutual fund, it is your responsibility to read the fund’s prospectus. Links to appearances and articles by Richard Bernstein, whether in the press, on television or otherwise, are provided for informational purposes only and in no way should be considered a recommendation of any particular investment product, vehicle, service or instrument or the rendering of investment advice, which must always be evaluated by a prospective investor in consultation with his or her own financial advisor and in light of his or her own circumstances, including the investor’s investment horizon, appetite for risk and ability to withstand a potential loss of some or all of an investment’s value.

About Risk

Equity investing is subject to stock market volatility. Smaller companies are generally subject to greater price fluctuations, limited liquidity, higher transaction costs and higher investment risk than larger, established companies. Investments in foreign instruments or currencies can involve greater risk and volatility than U.S. investments because of adverse market, economic, political, regulatory, geopolitical or other conditions. In emerging or frontier countries, these risks may be more significant. Smaller companies are generally subject to greater price fluctuations, limited liquidity, higher transaction costs and higher investment risk than larger, established companies. Investing involves risks including possible loss of principal.

Investing is an inherently risky activity, and investors must always be prepared to potentially lose some or all of an investment’s value. Past performance is, of course, no guarantee of future results.

About Eaton Vance

Eaton Vance Corp. is one of the oldest investment management firms in the United States, with a history dating to 1924. Eaton Vance and its affiliates offer individuals and institutions a broad array of investment strategies and wealth management solutions. The Company’s long record of exemplary service, timely innovation and attractive returns through a variety of market conditions has made Eaton Vance the investment manager of choice for many of today’s most discerning investors.

Richard Bernstein Advisors LLC serves as subadvisor to three Eaton Vance mutual funds.

Richard Bernstein is chief executive officer of Richard Bernstein Advisors LLC, a registered investment advisor.

For more information on Richard Bernstein Funds, click here or visit eatonvance.com/Bernstein.

Before investing, investors should consider carefully the investment objectives, risks, charges and expenses of a mutual fund. This and other important information is contained in the prospectus and summary prospectus, which can be obtained from a financial advisor. Prospective investors should read the prospectus carefully before investing.

©2015 Eaton Vance Distributors, Inc. | Member FINRA/SIPC | Two International Place, Boston, MA 02110 | 800.836.2414 |eatonvance.com