After Slow Start, the U.S. Should Regain Steam

March 27, 2015

I’ve had a rough week. It began with a Sunday flight down to Florida for a round of client visits. I was the only business type on the airplane; the rest of the cabin was filled with spring breakers. Half of them were families with very young children (there were 12 strollers and car seats gate-checked) and the other half were college students. The behavioral differences between the two were, unfortunately, not that great.

While not as raucous, the client meetings were also a bit stressful at times. We have had a fairly positive outlook for the United States, but the numbers for the first quarter have not lived up to expectations. Some who attended our sessions are concerned that we’ve been the victim of another “head fake,” where growth surges for a while only to fall back to lackluster levels. This scenario would not be a positive one for equity markets, and U.S. stocks have consequently started the year slowly.

We can’t change the past, but we remain pretty confident about the future. Some transitory factors have complicated things, and the U.S. economy has had to adjust to significant shifts in commodity prices and exchange rates. But the underlying momentum of American growth remains solid.

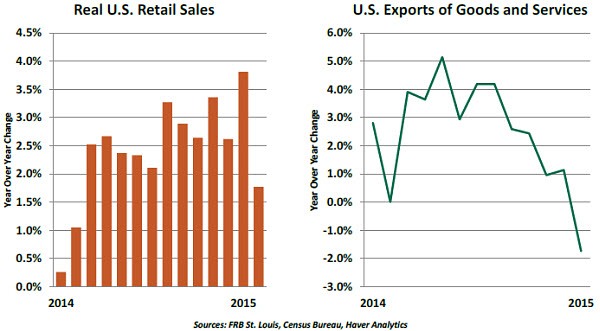

Recent readings on business activity in this country have been pretty lackluster. Retail sales have fallen for the past two months, even after removing the influence of falling energy prices on gasoline and automobile purchases. Industrial output has been slow, and exports have faltered.

Weather has heavily influenced recent trends. The impact of the harsh Midwestern winter of 2014 is clearly visible in the progressions above, as is the strong recovery that followed. This year, bad weather focused more on the Northeast, but we are expecting to see a comparable bounce in the data as climatic conditions normalize.

The two more-significant transitions that we’ve been working through also appear to be settling. Both have produced negative impacts at first, but both are expected to produce positive outcomes for the United States as the year progresses.

The first is the realignment of the U.S. dollar, which has appreciated by about 15% over the past 12 months against a trade-weighted collection of currencies. This has certainly hindered the growth of American exports, although the California port strike this winter also caused severe interruptions in shipping patterns.  Central banks moving in opposite directions initiated the correction in the foreign exchange market. The Federal Reserve has been leaning toward tightening, while a battery of other world central banks has been easing aggressively. Since the Fed offered a somewhat more- moderate tone at its March meeting, the dollar has eased a bit.

Central banks moving in opposite directions initiated the correction in the foreign exchange market. The Federal Reserve has been leaning toward tightening, while a battery of other world central banks has been easing aggressively. Since the Fed offered a somewhat more- moderate tone at its March meeting, the dollar has eased a bit.

U.S. officials have not complained much about their dollar’s strength, as it creates an opportunity for some of the world’s more-challenged markets to export their way to better health. The eurozone, in particular, is hoping for that outcome. Fundamental conditions in continental Europe are stabilizing, and markets there have performed powerfully. Should that trend continue, American firms will see better sales into that region.

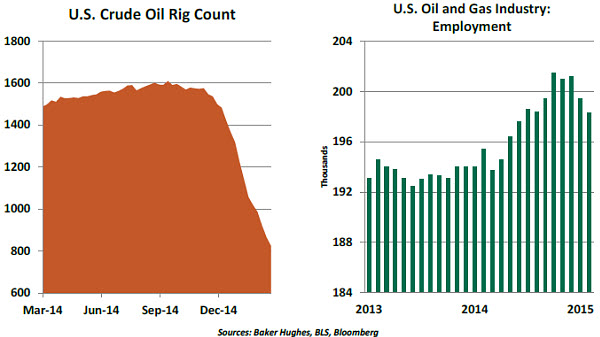

The second significant realignment has been the drop in energy prices. The reaction of U.S. producers has been swift and, in some cases, severe. The number of rigs actively engaged has fallen by nearly half since last summer; spending on oil field equipment has dropped; and employment in parts of the energy sector is falling. Some marginal participants in the industry are facing financial hardship.

The wide swings in crude oil prices seen over the past 40 years have not been conducive to the kind of long-term investments that form the core of a strong energy policy. Refining capacity, alternative fuels, conservation, export channels and exploration all take time to develop, but funding for them can often be limited by short-term swings in the markets. Policy-makers should give this paradox some careful thought.  Still ahead is the spending that households are expected to do with their gasoline dividends. These have been slow in evolving, but past episodes of this kind suggest that they will emerge over time. Beyond this “energy dividend,” other important tailwinds for U.S. growth remain in place. Very strong employment markets, very accommodative monetary policy, recovering government spending, and a healthy banking system all suggest good performance.

Still ahead is the spending that households are expected to do with their gasoline dividends. These have been slow in evolving, but past episodes of this kind suggest that they will emerge over time. Beyond this “energy dividend,” other important tailwinds for U.S. growth remain in place. Very strong employment markets, very accommodative monetary policy, recovering government spending, and a healthy banking system all suggest good performance.

So I’ve taken a bit of buffeting for my optimism, but I’m staying the course. I also took a bit of buffeting from the young man behind me on the flight home from Florida, who decided to practice his tap dancing for two hours on the back of my seat. It’s been a rough week.

Aegean Tension

On February 20, the Greek government reached agreement with its European creditors to extend its current bailout program to late June. Athens promised to “implement reforms” in that time, and in return the creditors would release the final €7.2 billion aid tranche. Some were quick to conclude that the crisis had passed and order had been restored.

One month later, the two sides are still arguing over the details. This week, Greek Prime Minister Alexis Tsipras again promised to come up with a list of reform details – but now we have added warnings from both sides that Athens will run out of cash by mid-April. This could trigger capital controls and even the exit of Greece from the eurozone.

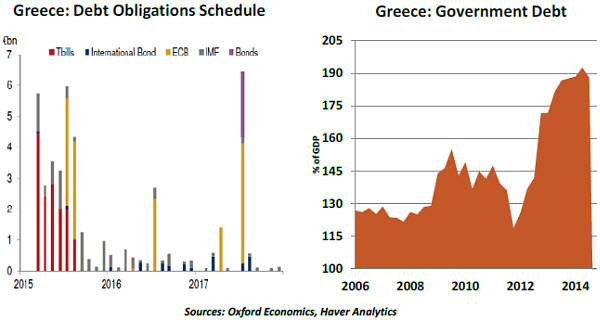

Greece faces two major financial problems. There is a near-term liquidity crunch that will likely be resolved in the coming weeks. But there is also a longer-term solvency crisis – the elephant in the room that is not yet being discussed but will become the focus of more drama before the end of June.

Athens has some hefty debt service payments to meet in the coming weeks. Its only source of borrowing for the past few years has been the issuance of short-term government bills. Approximately €2.4 billion in such bills will need to be rolled over in April, with a similar amount in May and an even larger amount in June. The market reception for such issues may not be very warm.  For the past month or so, the government reportedly has been funding itself by borrowing short-term money from state entities such as social security funds, ministries and state-owned companies. While it waits for that €7.2 billion aid payment, Athens is also looking for the return of about €1.9 billion in profits made by the European Central Bank (ECB) on holdings of Greek bonds; the ECB wants to see real reform underway before contemplating that request.

For the past month or so, the government reportedly has been funding itself by borrowing short-term money from state entities such as social security funds, ministries and state-owned companies. While it waits for that €7.2 billion aid payment, Athens is also looking for the return of about €1.9 billion in profits made by the European Central Bank (ECB) on holdings of Greek bonds; the ECB wants to see real reform underway before contemplating that request.

However, none of this helps with the longer-term solvency issue. If and when the current bailout program ends in June, Greece still will not be in a position to fund itself in the market at affordable rates. A very large International Monetary Fund (IMF) debt repayment is due in June, with another in September; major repayments to the ECB itself are also due over the course of the third quarter 2015.

The government has called for relief in the form of a debt swap where the interest is tied to Greek economic performance and which the ECB has been swift to rule out. There has also been tentative talk of extending the maturities and lowering the interest rates on some of the debt coming due. Either way, without a new bailout program – which would be the third such deal since 2010 – Greece will not be solvent.

Tsipras’ populist/nationalist government was elected on a mandate of changing the terms of the aid program. It has already begun turning away from the spirit of prior agreements by increasing welfare payments and delaying the privatization of state-owned assets. There seems to be little urgency to tackle the structural reforms of labor markets, tax collection and private enterprise, all of which external observers see as critical to the country’s future.

Meanwhile, German Chancellor Angela Merkel has her own domestic political challenges, with members of her own government restive over the apparently endless funding being paid to a country that is slow to implement change. With both sides playing to their constituents back home, it is not surprising that the public discourse is rancorous.

But if the two cannot agree behind closed doors on the best way to resolve near-term liquidity problems, it bodes ill for their ability to craft one final aid program that will please the taxpayers in both Berlin and Athens. And failure could mean that Greece bids antío to the eurozone.

Climbing Out of a Money Pit

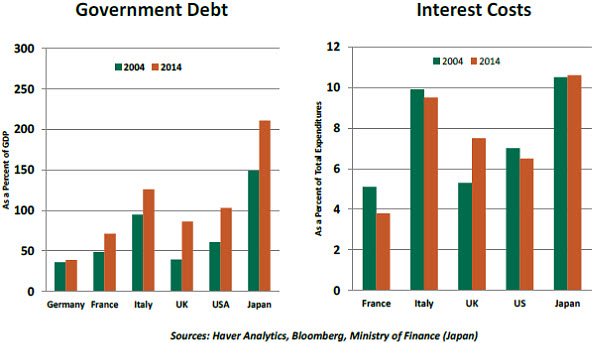

While Greece has been the poster child for mismanagement of public finances, it is certainly not the only nation facing questions about debt sustainability. Government debt of many major economies grew rapidly following the financial crisis. The low-interest-rate environment eased the path of borrowing and servicing the debt for governments, and their new issues were eagerly snapped up by investors seeking safe havens. But this rosy situation will certainly change when interest rates normalize in the years ahead.

Debt can expose countries to worrisome challenges if they have borrowed too much and face significant economic shocks. They may find themselves unable to meet their obligations, which is the precursor to a disruptive economic situation. Therefore, it is important to ask if the debt of a given country is sustainable.

The IMF has its own technical definition. In simple terms, debt is sustainable if it can be fully serviced. Interest expenditures related to the debt incurred constitute debt service. Interest costs as a percent of total expenditures are noticeably high in major industrialized nations, despite a low-rate environment. The main message is that as interest rates move up, the cost of servicing debt stands to increase even if the debt itself holds steady.  Growth is the surest and most-positive way to reduce debt. It broadens the tax base and reduces the level of debt relative to gross domestic product. But economic momentum in many industrialized nations has been unimpressive. Inflation, though not preferred, is another path to reduce the real stock of debt. Inflation is also weak, and some countries are facing a deflationary situation, albeit temporary.

Growth is the surest and most-positive way to reduce debt. It broadens the tax base and reduces the level of debt relative to gross domestic product. But economic momentum in many industrialized nations has been unimpressive. Inflation, though not preferred, is another path to reduce the real stock of debt. Inflation is also weak, and some countries are facing a deflationary situation, albeit temporary.

Inflation, deficit, debt and growth are related. If interest rates increase and governments are already running a deficit, it becomes more difficult to service and contain debt. Expanded austerity, which can be harmful to growth, may be necessary.

If inflation rises, bond holders demand higher nominal interest rates on new debt. Higher interest rates are not favorable for economic growth. Conversely, if the country is running a primary surplus (excluding interest payments), the interest rate bond holders seek may be lower.

Factoring in all of these interactions paints a complex picture of debt management. While much of the focus of recent government policy around the world has been on restoring growth and containing annual deficits, the level of debt cannot be ignored. No country wants to find itself in the difficulties Greece currently faces; limiting that risk in the future requires a strong commitment to discipline today.

(c) Northern Trust