High-Yield Bonds: Equity-Like Returns Without Equity-Like Volatility

A timeless (and timely) case for high-yield bonds

SUMMARY

- High-yield bonds have historically provided high current income with lower volatility than equities.

- The current fixed-income market offers a favorable environment, with benign default rates, strong corporate balance sheets and improving economic conditions.

- With interest rates expected to begin to rise from historic lows this year, high-yield bonds offer a cushion that may protect fixed-income investors from the adverse impact of rising rates and the risk of negative total returns.

Why allocate to high-yield bonds?

High-yield bonds occupy a special niche within the fixed-income market. These bonds, which are issued by companies with below-investment-grade credit ratings, offer higher yields to compensate investors for accepting exposure to additional credit risk. Generally, the lower the bond rating, the higher the yield.

Traditionally, companies with poorer credit ratings have issued high-yield debt to finance mergers or buyouts to help meet expanding capital needs. However, in recent years, more high-yield bonds have been issued to refinance existing debt. Companies have taken advantage of low interest rates and investors’ increased appetite for higher-yielding income investments to lock in relatively cheap financing. Situations where companies refinance their debt at more favorable rates generally put them in better financial health. Consequently, they tend to involve significantly less risk of default.

High-yield bonds are attractive to a wide range of investors because of their unique set of attributes. They appeal to investors who seek equity-like returns at much lower volatility levels than equities and to those who seek income with relatively low interest-rate sensitivity.

Better risk-adjusted returns than equities.

High-yield bonds have compared favorably as an investment alternative to equities. For the 10-year period ended 12/31/2014, high-yield bonds (as represented by the BofA Merrill Lynch US High Yield Index) returned approximately 8% per year, with about 10% annualized volatility, or standard deviation. Over the same period, U.S. stocks (as represented by the S&P 500 Index) also returned around 8% per year, but with nearly 15% annualized volatility.

Less volatility over the long term.

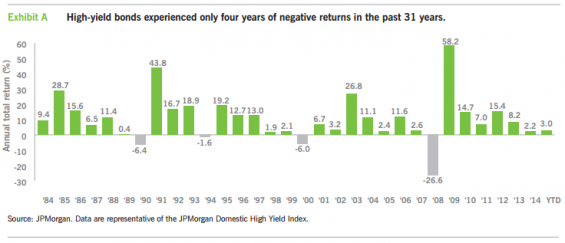

Despite being issued by companies that are seen to be at greater risk of a loan default, high-yield bonds, also known as “junk bonds,” have had only four years of negative total returns in the 31 years since 1984. Stocks, in comparison, have had five years of losses since 1984, using the S&P 500 Index as a proxy.

Less interest-rate risk.

High-yield bonds also tend to have shorter durations than most other fixed-income investments. Duration measures a bond’s sensitivity to interest-rate movements. This means that high-yield bonds are less likely than other fixed-income investments to be adversely affected by rising interest rates. Their performance during previous periods of rising rates bears this out.

Positive performance as rates rise.

During periods when 5-year U.S. Treasury yields rose 70 basis points (7/10 of a percentage point) or more in three months, high-yield bonds have averaged a gain of 2.5%, compared with a 3.0% return for the S&P 500 Index and a loss of 1.4% for investment-grade bonds (Source: JPMorgan).

Buffered by its yield.

The higher yields generated by high-yield bonds may also help to buffer potential losses as interest rates rise and bond prices fall. Even when affected by unfavorable interest-rate movements, high-yield bonds have this additional cushion.

Role of high-yield bonds in a portfolio

Before examining the current investment climate and the case for high-yield bonds today, there are certain timeless advantages that high-yield bonds may offer as part of a diversified portfolio. In brief:

High-yield bond coupons are higher and result in higher potential income than investment-grade bonds.

As company fundamentals improve, high-yield bonds can potentially appreciate in price.

High-yield bonds tend to have low correlations with other asset classes and, therefore, can add diversification1 to a portfolio.

These bonds tend to have shorter maturities, making them less sensitive to interest-rate movements. Their higher coupons can provide a cushion against possible losses when rates rise. Rising rates are often a sign of improving economic conditions, which tend to benefit company performance and boost demand for high-yield bonds.

Why high-yield bonds are compelling now

For the past five years, the high-yield market generally has been improving.

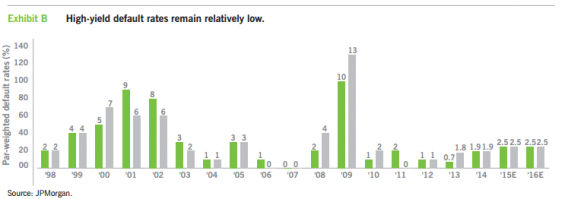

1. Low default rates.

The default rate has been below 2% in each calendar year since 2010, and as low as 0.6% in 2013 and early 2014, before rising to 3% with the default of TXU and Caesars, two large high-yield bond issuers. Ex-TXU and Caesars, the current default rate is about 1%. This compares favorably to the 10.3% default rate that was briefly reached in 2009, in the early aftermath of the credit crisis. It also stands well relative to the asset class’s long-term average default rate of 3.9%.

2. Healthy balance sheets.

Corporate balance sheets of below-investment-grade firms are generally in good shape and likely to improve as the economy gradually continues to recover.

3. Higher-quality issues.

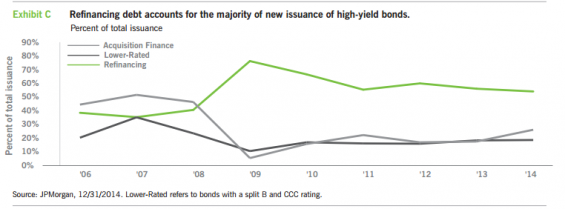

The quality of new high-yield bond issues has been relatively good for several years, with 54% of issues currently being used to refinance debt, which is generally a positive scenario, bolstering company financial health. Conversely, fewer high-yield bonds being issued are lower-rated or being used to finance acquisitions and buyouts.

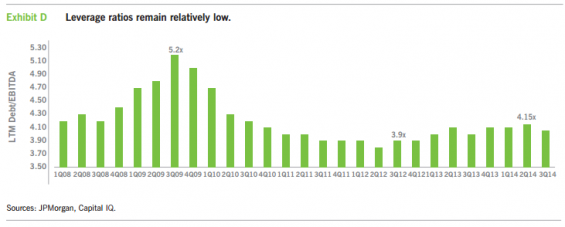

4. Low leverage and high interest coverage.

Another positive trend is that the leverage ratio of debt to EBITDA* now stands at around 4, which is roughly where it’s been for about four years, after peaking at about 5.2 in mid-2009. This is a reflection of the diligent work by many corporations to strengthen their balance sheets, as well as more prudent stances taken by financial institutions and by investors in general.

While leverage remains low, the interest coverage ratio of EBITDA-to-interest expense remains near all-time highs. It currently stands at around 4.5. This is perhaps the most important measure of a company’s ability to service its debt obligations.

Signals to watch

With all that said, it is important to be mindful of market changes and the risks of deteriorating credit standards as the credit cycle changes at some point. For instance, a rise in the issuance of CCC-rated lower-quality debt could be a warning that the credit cycle is nearing an end. These riskier bonds tend to accompany an upswing in aggressive leveraged buyouts and indicate an increase in the high-yield market’s overall risk exposure.

Are risks priced appropriately?

Eaton Vance is mindful of quality within the high-yield market and the importance of being compensated appropriately or sufficiently for higher levels of risk. If yields are only rising incrementally for much higher levels of risk, it may be wise to pass rather than take on higher or excess levels of risk. In brief: Ask if you are being paid appropriately or if risk is being appropriately priced.

Eaton Vance’s approach to high yield

- Eaton Vance has a 32-year track record of managing high-yield investments and delivering solid risk-adjusted returns.

- Consistency and continuity are hallmarks of our leadership and investment process.

- We seek to capitalize on inefficiencies in the high-yield bond market through rigorous fundamental credit research and market factor analysis.

- Our attention to risk-adjusted measurements and our goal of maintaining strong risk-adjusted returns throughout market cycles are important in capturing attractive up-market returns, while seeking to limit down-market losses.

1Diversification cannot ensure a profit or eliminate the risk of loss.

*EBITDA stands for earnings before interest, taxes, depreciation and amortization, and is a key indicator of a company’s financial health.

Appendix

Index Definitions

Unless otherwise stated, index returns do not reflect the effect of any applicable sales charges, commissions, expenses, taxes or leverage, as applicable. It is not possible to invest directly in an index. Historical performance of the index illustrates market trends and does not represent past or future performance.

JPMorgan Domestic High Yield Index is an unmanaged index that is designed to mirror the investable universe of the U.S. dollar domestic high-yield corporate debt market.

S&P 500 Index is an unmanaged index commonly used to measure the performance of the broad U.S. stock market.

Wilshire 5000 Index is a market-capitalization-weighted index composed of more than 6,700 publicly traded companies in the U.S. stock market.

About Asset Class Comparisons

Elements of this report include comparisons of different asset classes, each of which has distinct risk and return characteristics. Every investment carries risk, and principal values and performance will fluctuate with all asset classes shown, sometimes substantially. Asset classes shown are not insured by the FDIC and are not deposits or other obligations of, or guaranteed by, any depository institution. All asset classes shown are subject to risks, including possible loss of principal invested.

The principal risks involved with investing in the asset classes shown are interest-rate risk, credit risk and liquidity risk, with each asset class shown offering a distinct combination of these risks. Generally, considered along a spectrum of risks and return potential, U.S. Treasury securities (which are guaranteed as to the payment of principal and interest by the U.S. government) offer lower credit risk, higher levels of liquidity, higher interest-rate risk and lower return potential, whereas asset classes such as high-yield corporate bonds and emerging-market bonds offer higher credit risk, lower levels of liquidity, lower interest-rate risk and higher return potential. Other asset classes shown carry different levels of each of these risk and return characteristics, and as a result generally fall varying degrees along the risk/return spectrum.

Costs and expenses associated with investing in asset classes shown will vary, sometimes substantially, depending upon specific investment vehicles chosen. No investment in the asset classes shown is insured or guaranteed, unless explicitly stated for a specific investment vehicle. Interest income earned on asset classes shown is subject to ordinary federal, state and local income taxes, excepting U.S. Treasury securities (exempt from state and local income taxes) and municipal securities (exempt from federal income taxes, with certain securities exempt from federal, state and local income taxes). In addition, federal and/or state capital gains taxes may apply to investments that are sold at a profit. Eaton Vance does not provide tax or legal advice. Prospective investors should consult with a tax or legal advisor before making any investment decision.

About Risk

An imbalance in supply and demand in the income market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. There can be no assurance that the liquidation of collateral securing an investment will satisfy the issuer’s obligation in the event of nonpayment or that collateral can be readily liquidated. The ability to realize the benefits of any collateral may be delayed or limited. Investments in income securities may be affected by changes in the creditworthiness of the issuer and are subject to the risk of nonpayment of principal and interest. The value of income securities also may decline because of real or perceived concerns about the issuer’s ability to make principal and interest payments. Borrowing to increase investments (leverage) will exaggerate the effect of any increase or decrease in the value of Fund investments. Investments rated below investment grade (typically referred to as “junk”) are generally subject to greater price volatility and illiquidity than higher-rated investments. As interest rates rise, the value of certain income investments is likely to decline. Bank loans are subject to prepayment risk. Investments in foreign instruments or currencies can involve greater risk and volatility than U.S. investments because of adverse market, economic, political, regulatory, geopolitical or other conditions. In emerging or frontier countries, these risks may be more significant. Changes in the value of investments entered for hedging purposes may not match those of the position being hedged. No Fund is a complete investment program and you may lose money investing in a Fund. A Fund may engage in other investment practices that may involve additional risks and you should review a Fund prospectus for a complete description.

About Eaton Vance

Eaton Vance Corp. is one of the oldest investment management firms in the United States, with a history dating to 1924. Eaton Vance and its affiliates offer individuals and institutions a broad array of investment strategies and wealth management solutions. The Company’s long record of exemplary service, timely innovation and attractive returns through a variety of market conditions has made Eaton Vance the investment manager of choice for many of today’s most discerning investors.

The views expressed in this Insight are those of the authors and are current only through the date stated at the top of this page. These views are subject to change at any time based upon market or other conditions, and the authors disclaim any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Eaton Vance are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Eaton Vance fund.

This Insight may contain statements that are not historical facts, referred to as forward-looking statements. A Fund’s actual future results may differ significantly from those stated in forward-looking statements, depending on factors such as changes in securities or financial markets or general economic conditions, the volume of sales and purchases of Fund shares, the continuation of investment advisory, administrative and service contracts, and other risks discussed from time to time in the Fund’s filings with the Securities and Exchange Commission.

Before investing, investors should consider carefully the investment objectives, risks, charges and expenses of a mutual fund. This and other important information is contained in the prospectus and summary prospectus, which can be obtained from a financial advisor. Prospective investors should read the prospectus carefully before investing.

©2015 Eaton Vance Distributors, Inc. | Member FINRA/SIPC Two International Place, Boston, MA 02110 |800.836.2414| eatonvance.com