Yield Curve Flattening and Volatility LIkely to Continue in 2015

SUMMARY

- The U.S Federal Reserve (the Fed) has nudged down its rate-hike expectations, but higher volatility persists as the market tries to anticipate each move by the central bank.

- A flatter yield curve from rates rising at the short end and “tethered” at the long end still appears likely this year.

- We believe it remains a good environment for fixed-income sectors like floating-rate loans and high-yield bonds, which have been less sensitive to rising rates.

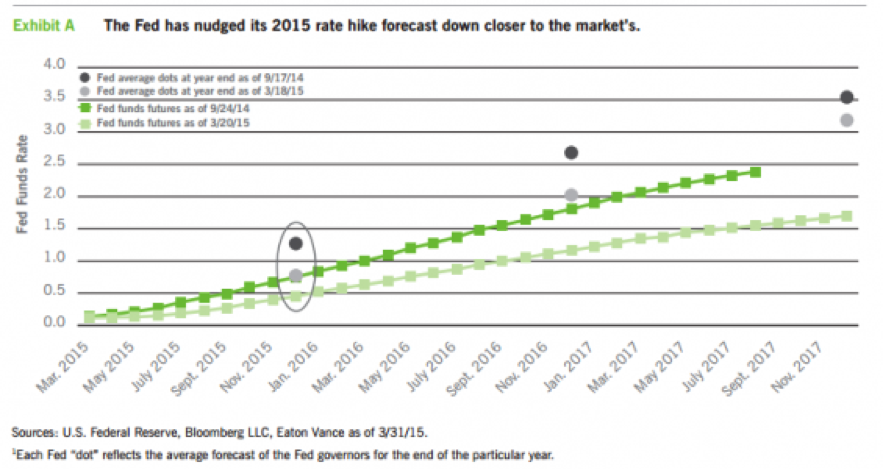

The Fed nudges down expectations

The Fed’s average forecast for rate hikes has been consistently higher than the market’s expectations. Exhibit A shows two sets of fed funds forecasts by the Fed and the market, one from September 2014 and one in mid-March.1 In September, the Fed projected a fed funds rate of 1.27% as of the end of the year vs. 0.75% by the market. By March, the Fed had lowered its December 2015 forecast to 0.77%, while the market’s fell to 0.44%. The market is still lower, but the Fed has narrowed the gap.

We believe that by bringing its forecasts down closer to the market – but still higher – the Fed is seeking to manage volatility while laying the groundwork for rate increases. The Fed said it is awaiting “further improvement in the labor market” and wants to be “reasonably confident that inflation will move back to its 2 percent objective over the medium term.”

Stocks and bonds both rallied in the wake of the Fed’s March 18 meeting, while the currency markets were roiled. Volatility is the natural outcome of the Fed’s latest pledge to be more “data dependent” in conducting its monetary policy. As long as the Fed and the market differ about what the data mean, elevated volatility is likely to persist.

A tethered long end

Exhibit B shows that the last volatility spike comparable to the recent round occurred in the first half of 2013, when the market reacted to the Fed’s initial plans to end quantitative easing – the so-called “taper tantrum.” At that time, a pronounced increase in the MOVE Index (a gauge of bond-market volatility), was accompanied by a doubling of the 10-year U.S. Treasury yield to over 3%.

In contrast to 2013, we believe the latest round of volatility does not signal a significant increase in long-term U.S. rates. Slow global growth and accommodative monetary policies in Europe, Japan and China have helped to push down long-term rates dramatically, and this has served as a tether for U.S. long-term rates.

The gray area in Exhibit B represents the excess spread of Spanish 10-year debt relative to 10-year U.S. Treasury yields – the narrowing of that spread over the past two years has been dramatic, and since October 21, Spanish debt has yielded less than the 10-year U.S. Treasury yield. Given this dynamic, plus the relatively attractive fundamentals in the U.S. (including modest inflation), there would appear to be ample demand from global investors for U.S. debt – and enough to limit a significant rise in long-term U.S. rates. We did see a backup in rates in February, with the yield on the U.S. 10-year Treasury hitting 2.2% on March 3, but the rally in the wake of the Fed’s meeting pushed rates back down to 1.9%.

Value in a rising rate environment

As we noted last quarter, floating-rate loans and high-yield bonds are two fixed-income sectors that historically have fared well in rising rate environments, both at the short and long end of the yield curve. Floating-rate loans and high-yield bonds also had subpar performance in 2014, thanks to a sell-off in the fourth quarter due to risk aversion on the part of investors. We believe this sets up a compelling investment case in 2015. The overall credit health of the two sectors remains relatively sound, despite limited exposure to energy companies, which may be adversely affected by continuing low oil prices.

In fact, floating-rate loans started the year with a 2.1% total return for the quarter, based on the S&P/LSTA Leveraged Loan Index (see definitions at end of report), a pace well in excess of the 4.9% annual average for the 10 years ended March 31, 2015. High-yield bonds are off to a similarly fast start: 2.5%, compared with a 10-year average annual return of 8.2% as of March 31, 2015, based on the Barclays U.S. Corporate High Yield Index. With index yields of 5.2% for floating-rate loans and 6.2% for high-yield bonds, as of March 31, 2015, we believe both sectors offer value, especially since the prospect of rising short-term rates remains very much with us.

Municipal bonds look like a good value to us as well, especially after a sell-off late in the first quarter that left 30-year municipal bond yields at 110% of U.S. Treasury bonds, compared with a 103% average over the 10 years ended March 31, 2015 according to Barclays.1 It remains tough sledding for emerging-market local currency bonds, which have been hurt by the strong dollar and rate environment, and which lost 3.9% in the first quarter. However, for investors who can tolerate the volatility of the sector, a yield in excess of 6.3% on the JP Morgan Government Bond Index – Emerging Markets (GBI-EM) Global Diversified represents what we view as fair compensation.

Room for upside surprise

While the trend recently has been toward lowered expectations for the timing and magnitude of rate hikes, we believe that the economic data could contain surprises on the upside. For example, while the Fed’s current favored inflation gauge – Core Personal Consumption Expenditures (Core PCE) – stood at 1.4% in February, shy of its 2% longer-term target, inflation expectations were at 1.9%, based on the five-year forward five-year breakeven rate on TIPS bonds. Capacity utilization was at 78.9% in February, not far off the pre-recession peak of 80.8%.

Focusing on value and on sectors that have historically withstood rising short-term rates appears to us to be a strategy worth considering. We look forward to helping you pursue the opportunities that arise in this environment as 2015 progresses.

Barclays U.S. Corporate High Yield Index is an unmanaged index of below-investment-grade U.S. corporate bonds.

S&P/LSTA Leveraged Loan Index is an unmanaged index of the institutional leveraged loan market.

JPMorgan Government Bond Index-Emerging Markets (GBI-EM) Global Diversified is an unmanaged index of local currency bonds with maturities of more than one year issued by emerging-market governments.

Unless otherwise stated, index returns do not reflect the effect of any applicable sales charges, commissions, expenses, taxes or leverage, as applicable. It is not possible to invest directly in an index. Historical performance of the index illustrates market trends and does not represent the past or future performance of any investment.

1The municipal/Treasury ratio compares 30-year U.S. Treasurys with 30-year municipal bonds, as defined by International Thomson’s Municipal Market Data (MMD). The MMD produces daily generic AAA yield curves that are a commonly used proxy for trading levels in the Municipal market. The generic high grade curves apply to non-AMT bonds of at least $2 million in size, with an assumed 10yr par call. MMD is a registered trademark of Thomson Financial.

Important Information and Disclosure

This material is presented for informational and illustrative purposes only as the views and opinions of Eaton Vance as of the date hereof. It should not be construed as investment advice, a recommendation to purchase or sell specific securities, or to adopt any particular investment strategy. This material has been prepared on the basis of publicly available information, internally developed data and other third party sources believed to be reliable. However, no assurances are provided regarding the reliability of such information and Eaton Vance has not sought to independently verify information taken from public and third-party sources. Any current investment views and opinions/analyses expressed constitute judgments as of the date of this material and are subject to change at any time without notice. Different views may be expressed based on different investment styles, objectives, opinions or philosophies. This material may contain statements that are not historical facts, referred to as forward-looking statements. Future results may differ significantly from those stated in forward-looking statements, depending on factors such as changes in securities or financial markets or general economic conditions. Actual portfolio holdings will vary for each client.

Investing entails risks and there can be no assurance that Eaton Vance, or its affiliates, will achieve profits or avoid incurring losses. It is not possible to invest directly in an index. Past performance is no guarantee of future results.

About Risk

An imbalance in supply and demand in the income market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. Investments in income securities may be affected by changes in the creditworthiness of the issuer and are subject to the risk of nonpayment of principal and interest. The value of income securities also may decline because of real or perceived concerns about the issuer’s ability to make principal and interest payments. As interest rates rise, the value of certain income investments is likely to decline. An imbalance in supply and demand in the municipal market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. There generally is limited public information about municipal issuers. As interest rates rise, the value of certain income investments is likely to decline. Investments involving higher risk do not necessarily mean higher return potential. Diversification cannot ensure a profit or eliminate the risk of loss.

Elements of this commentary include comparisons of different asset classes, each of which has distinct risk and return characteristics. Every investment carries risk, and principal values and performance will fluctuate with all asset classes shown, sometimes substantially. Asset classes shown are not insured by the FDIC and are not deposits or other obligations of, or guaranteed by, any depository institution. All asset classes shown are subject to risks, including possible loss of principal invested.

The principal risks involved with investing in the asset classes shown are interest-rate risk, credit risk and liquidity risk, with each asset class shown offering a distinct combination of these risks. Generally, considered along a spectrum of risk and return potential, U.S. Treasury securities (which are guaranteed as to the payment of principal and interest by the U.S. government) offer lower credit risk, higher levels of liquidity, higher interest-rate risk and lower return potential, whereas asset classes such as high-yield corporate bonds and emerging-market bonds offer higher credit risk, lower levels of liquidity, lower interest-rate risk and higher return potential. Other asset classes shown, such as municipal and investment-grade bonds, carry different levels of each of these risk and return characteristics, and as a result generally fall varying degrees along the risk/return spectrum.

Costs and expenses associated with investing in asset classes shown will vary, sometimes substantially, depending upon specific investment vehicles chosen. No investment in the asset classes shown is insured or guaranteed, unless explicitly stated for a specific investment vehicle. Interest income earned on asset classes shown is subject to ordinary federal, state and local income taxes, excepting U.S. Treasury securities (exempt from state and local income taxes) and municipal securities (exempt from federal income taxes, with certain securities exempt from federal, state and local income taxes). In addition, federal and/or state capital gains taxes may apply to investments that are sold at a profit. Eaton Vance does not provide tax or legal advice. Prospective investors should consult with a tax or legal advisor before making any investment decision.

©2015 Eaton Vance Distributors, Inc. | Member FINRA/SIPC | Two International Place, Boston, MA 02110 | 800.836.2414 |