Who will get caught skinny-dipping?

“You only find out who is swimming naked when the tide goes out.”– Warren Buffett

SUMMARY

- Following a six-plus-year bull market for all major asset classes, it has become very difficult to find true bargains in many areas.

- Equities in general have arguably become the best house in a low-return neighborhood, but they are not outright cheap.

- Until the opportunity set changes, we believe investors should favor shares of companies with management teams that allocate capital well.

More than six years into a bull market for all major asset classes, it has become very difficult to find true bargains.

The natural instinct for many equity investors is to talk about how attractively valued stocks are versus U.S. government bonds. This is essentially what is happening whenever you hear someone discussing risk premiums or the Fed model, or comparing dividend yields to the 10-year Treasury yield. Equities have arguably become the best house in a low-return neighborhood, so to speak, but they are not outright bargains.

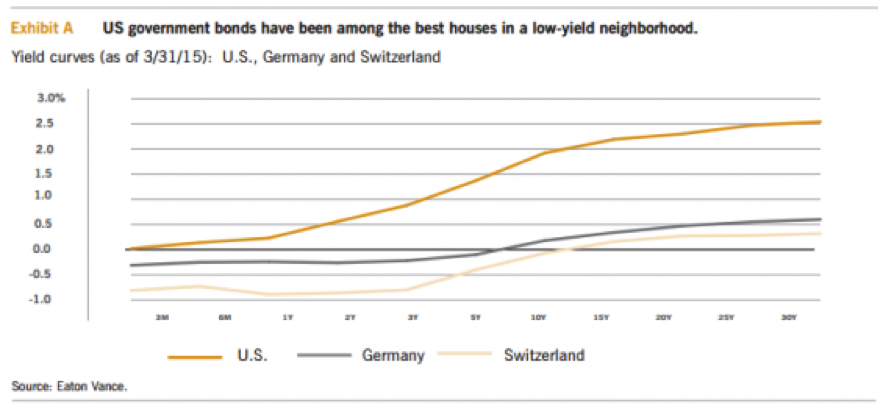

The same line of reasoning can be seen within the fixed-income markets. As of late March 2015, municipal bonds yielded 110% of long-dated Treasurys, despite being tax free. In fact, at roughly 2.00%, 10-year U.S. government bonds have been attractive relative to German bunds, which recently yielded around 0.20% for 10-year money. And, bunds have been cheap when compared to Swiss government obligations, which recently had an astounding yield of -0.10% for 10-year maturities. (Exhibit A.)

It has become a race to the bottom. All prices are set by the lowest common denominator – in this case, an asset with a negative yield. Putting the yield of the Swiss 10-year bond into a language that equity investors can better understand, this is akin to an infinite price/earnings (P/E) ratio. Yes, plenty of things look cheap when compared to an asset with an infinite valuation.

Re-energizing the energy sector?

One area within the equity market where investors might expect to find real bargains is the energy sector, where oil prices have basically been cut in half over the past nine months. With this in mind, we recently sent four of our investors to an investment conference in Louisiana where the senior management teams from most of the public oil companies in the U.S. were present. We were not the only ones with that idea. Attendance was at record levels, and the mood was closer to hope than despair. Bargain hunting is not a group activity.

Exploration and production companies’ capital spending budgets have been cut by roughly 40% so far. Oil service companies have been slashing prices by up to 30% to retain business and keep their employees and equipment operating. A number of companies in the energy sector have leveraged balance sheets and collapsing cash flows, courtesy of fallen oil prices.

Despite all of this, companies in the sector have been having no trouble raising fresh capital. Roughly $60 billion of debt has been issued year-to-date. Equity secondary offerings have been around $10 billion. Energy ETFs and sector mutual funds have been seeing massive daily inflows. Private equity companies have been raising multibillion dollar funds to pursue distressed energy companies. Ideally, poor-performing companies would be allowed to die so that stronger performers could take their place. This is not happening, as many “zombie” energy companies have been given new life with the support of easy access to capital.

The waiting game

When capital is apparently abundant but bargains are not, what is an investor to do? Wait. Many investors make the mistake of treating the market opportunity set as static. It is not. Markets are volatile, and the opportunity set is constantly changing. The choices on the menu six, 12 and 24 months from now will likely be different – perhaps quite different – than those available today.

In the meantime, we believe investors should favor the shares of companies with management teams that allocate capital well. This is the point in the cycle when skilled capital allocators can potentially distinguish themselves. As Warren Buffett has said, “You only find out who is swimming naked when the tide goes out.” We suspect there are currently a lot of skinny-dippers.

About Risk

Investments in equity securities are sensitive to stock market volatility. Equity investing involves risk, including possible loss of principal. Investments in foreign instruments or currencies can involve greater risk and volatility than U.S. investments because of adverse market, economic, political, regulatory, geopolitical or other conditions. In emerging countries, these risks may be more significant.

Past performance is no guarantee of future results.

©2015 Eaton Vance Distributors, Inc. | Member FINRA/SIPC | Two International Place, Boston, MA 02110 | 800.836.2414 | eatonvance.com