Everywhere I go I’m asked, “Will there be inflation or deflation? Are we in a bull or bear market? Is the bond bull market over and will interest rates rise?”

The flippant answer to all those questions is “Yes.” And that can be the correct answer as well, but it depends on what your time frame is and what tools you use to measure the markets and inflation. One of the newer members of the Mauldin Economics team is Jawad Mian, who writes a powerful global macro letter from his base in Dubai. He has been making the case for the “end of the deflation trade” (or more properly the return of a reflationary period) and the knock-on effects that would cause. Longtime readers know that I am in the secular deflation camp and ask me why there’s such a seeming difference my views and Jawad’s.

The answer is that Jawad and I are more or less on the same page over the longer term; the difference lies in the time frame of our perspective writings. I tend to think and forecast about longer periods of time, whereas Jawad’s main audience is portfolio managers and traders who are focused on the next 6 to 18 months. I tend to think in secular cycles, while Jawad is focused on the cyclical horizon. When you read the section below that Jawad writes, you will find a fairly upbeat analysis.

And that difference opens up a very important discussion for this week’s letter. I will start off by explaining why I think we are still in a long-term secular bear market in US stocks, even while I can clearly see that we are also in a powerful cyclical bull market. It is important to know both, because there are quite different investment approaches that are appropriate for different combinations of secular and cyclical cycles.

Then we turn to Jawad, who will discuss why we could see a reflationary macro regime emerge in much of the developed world and where the resulting opportunities might lie. I will finish up with why I think that this reflationary period will be temporary, with a potential for a serious round of deflation further out in the future, even though I readily acknowledge that “temporary” could mean a few years. But the looming reality over the longer term is that the coming war over a return of deflation will be fought by central banks everywhere. It will truly be World War D.

Why start with equity markets when we are talking about deflation and inflation? Because we need to see the connections!

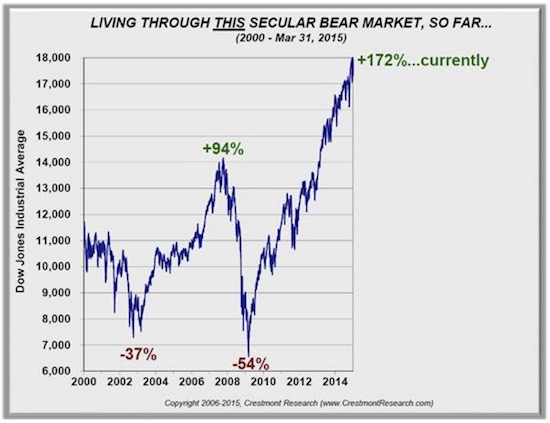

Secular Bear Markets

I first wrote about a coming secular bear market in 1999. I was early, of course. The market went up (a lot!) for the next year. Over the next few years I began to do some work looking at secular bear markets not in terms of price but in terms of valuations. My now very good friend Ed Easterling of Crestmont Research was doing similar analysis, and we compared notes. Then we published a series of reports in this letter, which I later adapted in two chapters (co-authored by Ed) of my book Bull’s Eye Investing in 2003.

I believe secular bull and bear markets should be seen in terms of valuation, and cyclical bull and bear markets in terms of price. A secular bull market should be approached with a more aggressive, relative return style of trading, while a secular bear should have an absolute return focus with appropriate risk controls. That difference in trading style is necessary because of how valuations will trend in the two different types of markets.

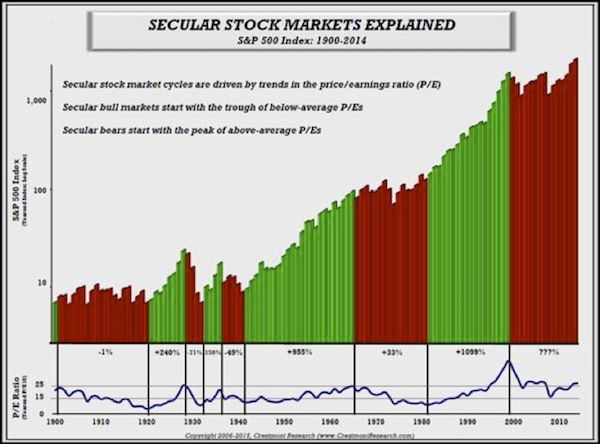

Let’s look at the updated charts that Ed sent me over the weekend from his fabulous, data-rich website. In general, secular cycles are long-term trends in valuation.These cycles include numerous interim surges and falls in price that reflect shorter-term psychology and economics. The long-term secular cycles can be seen in this first graph, with secular bears represented in red and secular bulls shaded green. The driver of these cycles is the relative valuation of the stock market as reflected in the price/earnings ratio (P/E). When P/E trends higher, it multiplies earnings growth and generates periods of above-average returns. When P/E trends lower, it offsets some or all of earnings growth and delivers periods of below-average returns. P/E is the blue line underlying the secular cycles on the chart.

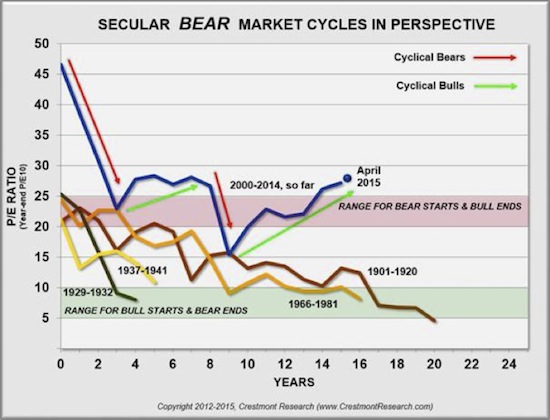

The P/E segments for all of the red-bar secular bears can be overlaid on a chart with time in years across the bottom and the level of P/E on the side (see chart below). First, secular bears tend to start in the red zone of high P/Es and decline to the green zone of low P/Es. This downshift into a secular bear is caused by a trend in the inflation rate from low, stable inflation to levels of either high inflation or deflation.

Second, this chart includes red and green arrow-lines that highlight the shorter-term cyclical bears and bulls during the current secular bear. The chart demonstrates that longer-term secular periods have cyclical bears and bulls within them, offering very profitable trading opportunities.

Third, the current level of the market P/E indicates that the stock market is fairly high. It is now well above the peaks of past secular bears and nowhere near the levels needed for a secular bull market start.

Even after more than 15 years in a secular bear market, the current secular trend has a ways to go to reach lower valuation levels. How can that be true after such a long period? In part, it’s because this secular bear started at such high levels. The current secular bear has experienced the same amount of P/E decline that many of the past secular bears experienced over longer and shorter periods, but the current secular bear started at twice the historical highs.

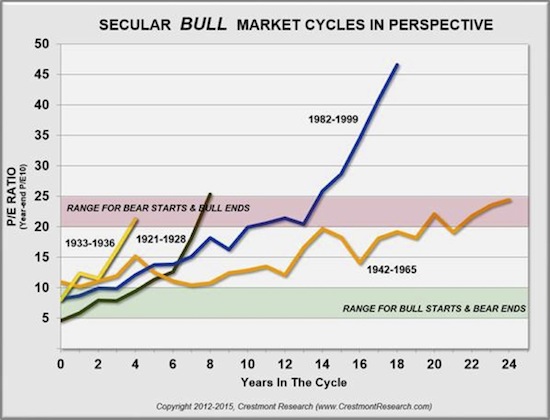

Bears start where bulls end and vice versa. As the secular bull market version of the previous chart shows, the late 1990s bubble took that secular bull market to unprecedented heights. A return from a period of either high inflation or deflation to low, stable levels of inflation will result in a rising trend in P/E during secular bull markets .

The “difference” between Jawad’s and my view on the inflation/deflation question is so important because turns within cycles have a major impact on pricing and valuations.

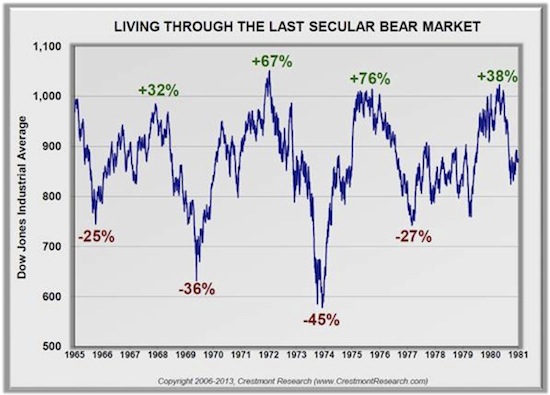

Yet even though we are in a secular bear that has come a long way with quite a ways to go, this secular bear looks and acts like previous secular bears. For example, here’s the daily graph for the previous secular bear in the 1960s and ’70s.

The cycles are very evident. Note the dramatic magnitude of their swings. Here’s the same format of chart for the current secular bear. Notice there are very similar patterns and magnitude… and new highs in the middle of the secular period.

Right now, many of you are scratching your heads and wondering how we get to lower valuations. Maybe this time is different! Or perhaps we’ll see a longer secular bear market until we return to a “normal” economic environment; and then earnings, prices, and valuations will begin to more closely resemble historical patterns. Remember, rising periods of inflation have historically compressed valuations.

World War D

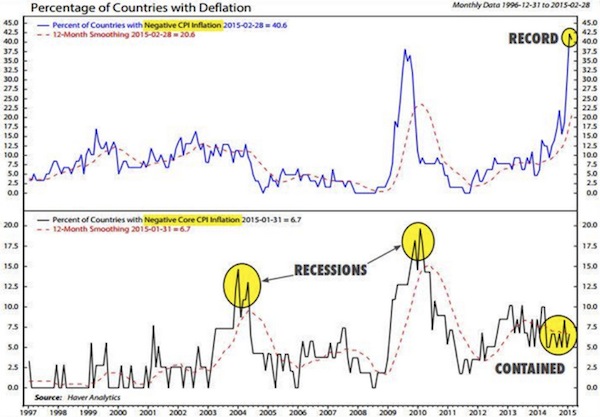

While deflation fears have persisted since the 2008 meltdown, they intensified last year, with global inflation readings falling to their lowest level since 2009. The collapse in oil prices, combined with generally soft macro data and a rising dollar, is aggravating concerns about the inflation outlook. Inflation expectations have plunged, and sovereign bond markets have rallied sharply, with yields of less than zero in parts of Europe. Negative-yield bonds now account for some €1.5 trillion of debt issued by governments in the euro area, equivalent to almost 30% of the total outstanding. Many expect even more of the global bond market to fall into negative yield territory. Half of all government bonds in the world today yieldless than 1%.

Many fear that the current deflation outbreak will turn into a “vicious circle of deflation,” in which consumption is postponed and investment plans are curtailed in anticipation of lower prices. These behaviors contribute to a further drop in demand and additional reductions in prices. The burden of debt increases, since falling incomes make it more difficult to service existing debt as real interest rates rise. Thus, economic growth slows and inflation declines further, hurting consumption and investment even more – hence, the vicious deflationary spiral.

As Christine Lagarde warned in January 2014, “Deflation is the ogre that must be fought decisively.” It is no surprise then that global short-term nominal interest rates are reaching the zero lower bound. Oil-price-induced weak inflation readings have forced aggressive reactions from policymakers, with at least 24 central banks already engaging in some form of monetary easing in 2015. According to my friend David Rosenberg, nearly 90% of the industrialized world economy is presently anchored by zero rates. There is a global focus on fighting deflation.

Why is inflation still nonexistent? And what do we make of all this unprecedented monetary policy? Is debt deflation the biggest risk to the global economy? What are some of the major implications for investors? In the next section Jawad parses the economic data and surveys the macro landscape to offer his cyclical (1 to 2 years) outlook, and then I consider the secular (5 to 10 years) outlook, with a particular emphasis on the threat of deflation.

A Little Less Deflation, A Little More Reflation, Please

By Jawad Mian

Deflation is not always sinister.

I believe the deflation scare of 2014 will give way to a global economic surprise in 2015. The type of deflation likely to be observed this year will benefit the global economy and provide a welcome boost to real household incomes. In my mind, the collapse in oil prices is good deflation; a decline in demand, wages, or forward expectations causes bad deflation. Once the shock of the speed of the recent drop in oil prices is overcome, cheaper oil will undoubtedly be an important net positive for the world economy later in the year.

There is little evidence that expectations of future price declines are suppressing employment, wages, consumer spending intentions, or even global manufacturing activity. Global recruitment difficulties are back at 2006 levels, and there is mounting evidence that wage gains should begin to accelerate where they are needed most: the US, Germany, and Japan.

The US created nearly 3 million jobs in 2014, and real wages have risen more over the past year than at any other point since 2009. Strong momentum in the labor market, ongoing recovery in the US housing market, positive wealth effects from a buoyant stock market, and declines in energy prices should all combine to generate strong consumer-led growth.

It is getting more difficult to attract and retain labor. The tighter labor market has led Walmart, the nation’s largest private employer, to increase wages for 500,000 of its most poorly paid workers. The company plans to spend about $1 billion a year to raise the pay of all employees (1.3 million) to at least $9 an hour, and to at least $10 an hour by next February. I believe Walmart’s bold initiative will lead to higher wages being set for entry-level jobs throughout the retail sector, a trend that may impact over 15 million people.

A look at interest rates, currency values, and reduced energy costs suggests that Europe and Japan will receive a significant reflationary boost. Europe’s economic turnaround is in its early stages and could provide a positive growth surprise over the next two years. The liquidity spigots are wide open, and the largely recapitalized banking system is responding to credit demand, as indicated by the latest ECB bank lending survey. Money supply and bank lending have continued to recover, with loan growth in the euro area about to turn positive for the first time since 2012.

The recent German consumer confidence reading was the highest it has been since 2001. German unemployment is near post-reunification lows, and real wages are growing at the fastest pace in over 20 years. IG Metall, Germany’s largest union, just settled on a 3.4% annual pay rise for its workers in southern Germany. More importantly, the deal is seen as a bellwether for salary negotiations in the rest of the country. Reports suggest that 32 regional contracts (covering seven unions and about 6.5 million workers) expire this year.

This is an essential part of euro-area rebalancing that should support growth in neighboring countries by way of a competitive boost. The Spanish labor market has enjoyed its best year since 2007, and the eurozone’s overall unemployment rate has fallen to a 33-month low.

Deflation is in the process of ending in Japan. The Bank of Japan has successfully cheapened the yen to its most competitive level since 1973 on a real effective exchange-rate basis. Export volumes are rising, and Japan’s balance of payments on tourism has turned positive for the first time in a long time. According to Peter Tasker, in terms of discretionary spending, the tourist boom is equivalent to an increase in the Japanese population of 1.4 million.

With the jobless rate down to 3.4%, Japan should be able to finally achieve some real wage growth this year. Just as Prime Minister Abe has been able to produce a genuine shift in the corporate governance climate in Japan, I firmly believe that Abe will be able to cajole corporate leaders to hike salaries as well, so as to “spread the warm winds of economic recovery to everyone throughout the country.” Last month, Toyota granted its employees their largest wage increase in more than a decade.

The global manufacturing sector has expanded for 28 consecutive months. Based on Markit’s recent Global Purchasing Managers Index (PMI) survey, the rate of output growth accelerated as companies scaled up production to meet rising levels of new work and new export orders. As US economic growth should now be driven more by consumption (which represents two-thirds of the US economy) rather than capital expenditures (capex), this implies stronger global trade, a wider US trade deficit, and a softer US dollar going forward.

The cyclical path of least resistance for commodities may also turn up later this year. A pickup in global PMIs suggests that we may have seen the worst of commodity price deflation. Oil excess supply remains elevated, but prices appear to have bottomed. According to Aurelija Augulyte, a senior analyst at Nordea Markets, even if you hold the dollar and oil prices at current levels, the base effects will effortlessly push the inflation up in the second half of this year.

Global core inflation appears to have already troughed. The number of nations where CPI fell month-over-month has collapsed from 23 in December and 33 in January to just 9 in February. I suspect downside pressure on global inflation readings will soon be exhausted.

In the US, core inflation has surprised positively three months in a row. The core CPI held at 1.8% year on year in April, up from 1.6% in January. Core CPI was at a 2.3% annual rate in the first quarter, up from a 1.6% pace in 2014. The Fed’s preferred measure of inflation (core personal consumption expenditure index) has been roughly stable for two years, around 1.5%.

Forward-looking indicators suggest that core inflation in Europe should also soon turn positive and begin to trendhigher. It will become difficult for policymakers to maintain their ultra-dovish tone, with economic momentum improving and inflation rising later in the year. The cyclical upswing will dial back central bank aggression, in my view. Interest rates around the world will remain low, however, to help reduce the budget costs of a large public debt burden.

Source: Ned Davis Research

The clouds of deflation will part.

Even though headline inflation may continue lower in the months ahead, given the extent of the decline in the price of oil, I find reassuring evidence that core inflation in major economic blocs will stabilize as we approach mid-year.

I believe the basic assessment of deflation expectations will completely change, and the market will slowly recognize that there is another economic equilibrium that is very far from the current state.

There are green shoots of economic improvement around the world that augur well for the inflation outlook, but most investors remain too blinded by the oil crash to even notice them. James Paulsen, chief investment strategist at Wells Capital Management, provides an insightful take on our cultural obsession with deflation. I quote (with some edits for brevity):

Today, after more than three decades of disinflation, chronic deflation in the dominant technology sector, and a world which hovers near zero inflation, most are increasingly obsessed with the potential for a deflationary spiral. Despite universal expectations of falling inflation or deflation, however, several forces are emerging which likely ensure serious deflation will not result.

First, emerging world economies were primarily a supply story adding to disinflationary forces in the last decade. However, emerging economies are rapidly transitioning toward a major demand story which will probably prove much larger than the post-war baby boom. Second, balance sheets within the US have been significantly retrofitted since the 2008 crisis. Banks have perhaps never been as strongly capitalized as they are today and have unprecedented lending capacity. Corporate profits are at record highs, business balance sheets are strong, and cash flows are immense. US household net worth is almost 20% higher than its previous record and the debt service burden is at a new low. Household and corporate pent-up demands are considerable (due to the pause in spending during the crises of the 2000s) and the credit creation process is just beginning to revive.… Finally, a cultural obsession with depression and deflation evident since the 2008 crisis has produced unprecedented and massive economic policy stimulus despite a continuous economic recovery in the US for more than five years. When a culture becomes universally obsessed with a problem, it generally solves it!

The reason central bank action has been insufficient to overwhelm the forces of deflation thus far is that government deficits globally have been contracting since 2010.

When central banks have had loose monetary conditions in previous economic cycles, governments have been keen to spend this money to boost growth (and thus inflation); however, in this cycle, we have seen governments retrench their spending. In other words, fiscal tightening has acted as a counterweightto unprecedented monetary easing.

Emergency measures to reduce government borrowing have actually worsened the debt arithmetic and prolonged the economic malaise felt in major regions of the world. The romantic fixation with balanced budgets is counterproductive when deflationary pressures are building. When the private sector is deleveraging, the public sector must increase its borrowing and spend fortuitously to restore economic balance and boost aggregate demand. The main lesson from our recent travails is that lowering interest rates and engaging in QE is no panacea for growth in a low-inflation world, especially when fiscal policy is pulling in the opposite direction.

The IMF estimates that the effect of the fiscal multiplier at the zero lower bound exceeds the “normal times” multiplier by a large margin. Budget cuts of 0.5%–1% of GDP typically act as an economic drag of around two to four times that amount, so a reversal of fiscal austerity should prove very stimulative. In my view, investors are grossly underestimating the potential for favorable fiscal policies to boost growth in a very easy monetary policy environment.

Budget plans for the world’s major economies in 2015 show that, for the first time since 2009, fiscal policy won’t be a drag, according to Jeffrey Kleintop of Charles Schwab.

He highlights a few recent examples of changes in global fiscal policy:

- Japan has postponed the planned 2015 consumption tax increase.

- China has started to announce new spending projects intended to keep the economy from slowing more sharply.

- In the US, federal spending has increased for five straight months after being flat for five years, rising 5.5% year-over-year in October.

- France and Italy have been given more time by the European Commission to meet their deficit reduction targets, which means they won’t need to implement substantial spending cuts (tax cuts in France and Italy are more likely this year).

- Germany should ramp up spending after initially proposing to balance its budget in 2015, while…

- Europe will likely approve and begin to implement some version of President Juncker’s plan to provide more than €300 billion in spending initiatives.

I view the gradual move toward greater fiscal expenditure as a paradigm shift that will upset deflation expectations and overly subdued growth estimates in the developed world.

The market is a composite personality, and right now investors have developed a “collective consciousness” that is still agonizing over the threat of deflation, even as the inflation environment has been changing substantially. It may not seem like it now, but I believe monetary authorities have overcome the threat of deflation on a cyclical horizon. They have been successful in changing people's perceptions and breaking the deflationary mindset, even if this shift is not yet reflected in the level of global government bond yields.

Government bonds in the major economies remain unattractive from a long-run valuation perspective. Globally, bond yields have fallen to levels not seen for centuries. How long can bond yields remain in their current prostrate position in the face of better economic health in 2015 and possibly into 2016?

I can imagine the world looking very different from the way the market currently expects it to. Since 2008, the global economy has never looked as good as it does today. We are finally entering a growth environment where no region of the world acts as a considerable drag (particularly in the case of Europe and Japan). The expanding strength in numerous international equity markets could be an important signal heralding far more durable global economic growth prospects.

Since 2011, we have seen deflationary trends dominate: the US dollar rising, global growth slowing, commodities crashing, inflation falling, global bond yields declining, and US stocks outperforming the rest of the world. If I am correct in thinking that the market’s deeply entrenched macro concerns regarding deflation will dissipate, all these trends should reverse. A global capital-rotation already appears to be underway that favors markets that have been long-time laggards versus the US stock market. I believe global equity market leadership might be inclined to shift to Europe and Asia.

I also think there is a major revaluation risk to owning government bonds at this stage of the investment cycle. With macro risks waning and inflation expectations slowly rising, I suspect global bond returns have probably crested. As the world emerges from the perceived threat of deflation, bond yields should rise toward equilibrium levels.

To learn more about Jawad and to receive his letter, Stray Reflections, click here.

It’s All About That Debt, ’Bout that Debt, ’Bout that Debt

John again. Now that you have explored Jawad’s thinking on global prospects for a reflationary period, I am going to summarize why I think we have not seen the end of deflation. (I have written about this theme before and will likely delve into it again – it’s important.)

First, normally, financial crises such as we had in 2008–09 bring about a period of deleveraging. This time, there been no debt reduction, and debt levels have skyrocketed throughout the world. Only in a few countries where there were housing bubbles have we even seen consumers retrench. The world is awash in debt! And ironically, the demand for even more debt seems to be insatiable, driving down yields.

In countries all over the world, debt is rising faster than global GDP, which means that at some point the carry cost of that debt is going to have to be reconciled. That is an economic law that was first noticed when the Medes were trading with the Persians. That is true for individuals, corporations, and governments. Of course, governments can monetize that debt if it is in a currency they control, but that course will typically weaken currencies (and thus buying power and value), which is default by another name.

All this was best articulated by Irving Fisher in his writing in the ’30s on the connection between debt and deflation.

The presence of too much debt, as Lacy Hunt and others have demonstrated, will slow the potential growth of GDP, which makes paying off that debt more difficult.

At some point, there will be another recession, with the accompanying bear market; and if there has been no resolution of the debt burden, there will be another debt crisis, and it will be massively deflationary. Central banks will respond with more QE than anyone can possibly imagine today. When will this happen? Two years? Three? Five? No one knows, but this eventuality is baked into the debt cycle.

Given what we have learned about the reaction of central banks and given that the debt problem is global, this next crisis will be unlike anything we have experienced.

I expect US rates to sink to new lows in a period that is also likely to see the final drop in yields of the 30+ year-long bond bull market.

In the meantime, we trade the cyclical cycles and look for yield and safety where we can.

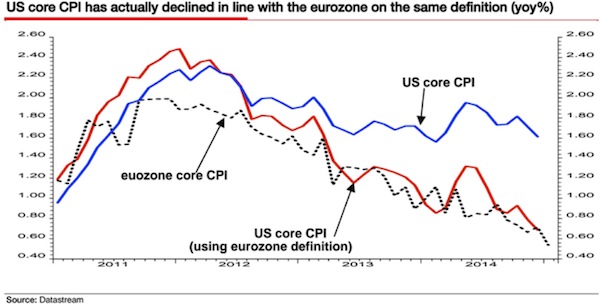

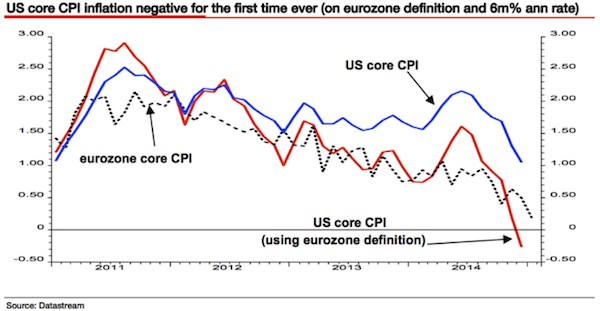

One last point. Inflation, as I have written about in detail, is an artificial construct, and we have changed the way we measure it over the years. The CPI is just one method, and it is not used universally. If the US used the same measuring tools that Europe does, our central bankers would be having heart palpitations right now, as using the Eurozone definition of inflation would show the US in outright deflation.

Look at these charts from my friend Albert Edwards, from a few months ago. The difference in the formula for how you figure inflation in the US and the Eurozone is largely how you deal with the housing component. Today, the same definition shows the US to be in a deflationary zone. By the way, that same measure would have meant that Greenspan should have been a LOT more aggressive in raising rates. It is likely we would have avoided the housing bubble had he done so, or at least it would have been not so big. But that’s a guess.

So, it makes a difference what measures you use, what index methodology you choose, and how you account for value. If you can change the data, you can make it say what you want it to say and support your case, whatever that might be.

Secular versus cyclical matters. We invest mostly in the shorter cyclical term, but the secular patterns tell us where the tail risk lies.

Here and There, New York, New Hampshire, Vermont, and NYC

I am on the road, making a few one-day business trips. Tomorrow I go to Virginia Beach to see my old friend Mark Finn for the afternoon, before taking a late flight to Dallas. Sunday I go to New York City, where I will be for five days, before going to New Hampshire for a speech and then on to Vermont Sunday afternoon to be with my partners and the management team of Mauldin Economics. Then it’s back to Dallas, where I’m trying to put the rest of my summer together. I know I will be heading up to New England later in August and of course there is the annual fishing trip the first Friday of August in Maine.

For what it’s worth, I will be at the NYSE next Monday to be part of the closing bell ceremony, where Monty Bennett, the chairman of a new public company whose board I am on, Ashford Inc., will ring the bell before we go over to Bobby Van’s and hang with the Friends of Fermentation. I see steaks. Ashford Inc. is involved in the hotel business and managing REITS. I have to admit I am learning a great deal more than I think I am contributing. Getting into the nitty gritty of this company has been a fascinating learning experience about a simple idea – renting a hotel room – that is a very complex business to do right. And, diving deep into Ashford’s numbers, I see all sorts of correlations with other economic data. Intriguing.

By way of a short teaser, I’ve been reading the galleys for my latest book, which should be out in a few weeks. We are going to be offering this book in a slightly different manner than previous books as part of a marketing experiment. I’m quite proud of it and look forward to sharing it with you.

Again, if you’d like to know more about what Jawad writes, you can go here. Jawad has attracted a lot of interest from serious traders and investors around the world, and deservedly so. He left a successful career as a portfolio manager to follow his passion for independent macro research and trading. As he often reminds me, “There is nothing more important to investment success than the freedom to express your own views.” I am really pleased that he wanted to join our team, and I enjoy my frequent interchanges with him. I always learn a lot.

It’s time to hit the send button. I’m in Boston tonight and see Legal Seafood in my near future. Looking over the harbor on this beautiful day, I see sailboats and ferries scurrying everywhere. Back in Texas it is raining and flooding, although Dallas seems to be avoiding the real problems. Houston, however, was built on a swamp, and swamps flood. Not much they can do about it. It was a problem when I lived there in the late ’60s as a student at Rice, and it will still be a problem in another 40 years. Some of us wish we could shift that rain out West, and most wouldn’t even mind if some hit California. Last year at this time there were open worries about many of our lakes drying up. Now the water is over the dams. But that’s Texas for you.

Next week I am going to get a little controversial. I recently had a well-received op-ed in the Investors Business Daily on what policies the US needs to implement to spur economic growth. I am going to develop that theme here. There will be something to please and annoy everyone. Have a great week!

Your never seeming to get to slow down analyst,

John Mauldin

[email protected]

The article Thoughts from the Frontline: World War D—Deflation was originally published at mauldineconomics.com.