SUMMARY

- An increasing number of investors each year may be surprised on Tax Day after being subjected to AMT, which erases standard deductions many taxpayers use.

- Originally designed to tax the very wealthy, over time AMT has tended to ensnare taxpayers with income below $1 million.

- Investors hit by AMT may want to consider municipal bonds that are exempt from it.

The reality of Alternative Minimum Tax (AMT) is setting in for an increasing number of U.S. taxpayers. Tax Policy Center estimates that 4.2 million taxpayers were subject to AMT in 2014, a number it projects will increase to 6.1 million in 2023. By disallowing a list of standard deductions many taxpayers typically utilize, AMT’s bite can be significant for the unprepared.

The good news is that investors who may face AMT can take straightforward steps ahead of time to mitigate the effects of the tax. One potential solution is municipal bonds that are exempt from AMT – and the funds that invest in them. By understanding AMT and how certain muni bonds are relieved of the tax, investors facing AMT may be able to keep more of what they earn.

What is AMT?

AMT is a parallel tax system created to prevent tax avoidance by high-income earners. Congress enacted a minimum tax in 1969 after 155 taxpayers with adjusted gross incomes (AGI) above $200,000 (about $1.45 million in 2015 dollars) legally paid no federal income tax in 1966. The minimum tax was an attempt to ensure the highest income earners could not use excessive tax exemptions, preferences or loopholes to escape tax payments.

AMT was formally established in 1982 to replace the minimum tax. Taxpayers must first calculate taxes based on standard tax rules. Once that is complete, a taxpayer must add back deductions not allowed under AMT to determine their AMT income (AMTI). After subtracting an AMT exemption amount, taxpayers must compare these two rates and pay the higher of the two. Because of the complexity and extra steps necessary to calculate AMTI, there is no easy way for a taxpayer to determine if they are subject to AMT.

AMT has two brackets to consider. For 2015, AMT rates are 26% for the first $185,400 of AMTI ($92,700 in the case of a married individual filing a separate return) and 28% on income above that level. For comparison, regular federal income tax rates start at 10% and go as high as 39.6%.

Who is affected by AMT?

AMT erases many standard deductions, and taxpayers have historically had to pay AMT if they:

- Have more than three children.

- Face high state and local taxes.

- Have large capital gains.

- Exercised incentive stock options, but did not sell the stock during the year.

AMT’s growing reach

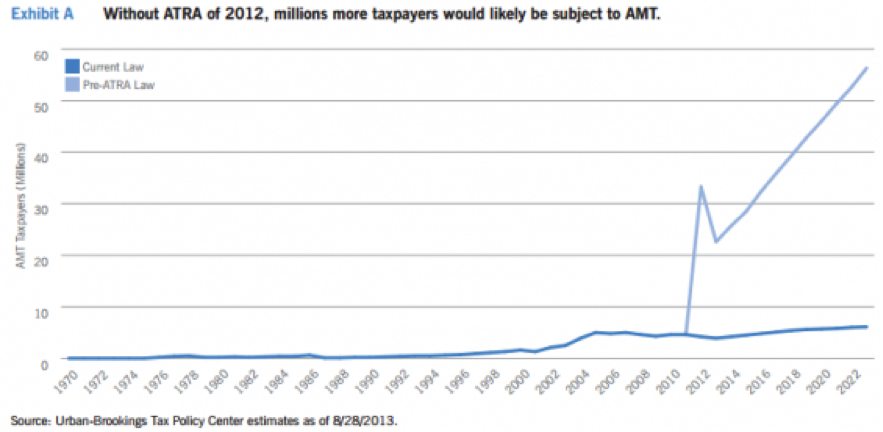

Although Congress created the minimum tax specifically for the highest income earners, it did not initially index the tax for inflation. As inflation has increased over the years, a greater number of earners are now ensnared by AMT. The number of taxpayers owing AMT increased from 20,000 in 1970 to about 4.3 million in 2011.

If not for the American Taxpayer Relief Act (ATRA) of 2012, which permanently indexed AMT, many of these projections would be exponentially higher. In 2014, an estimated 4.2 million taxpayers paid $27.2 billion in AMT. Without the ATRA, those numbers would have ballooned last year to 25.7 million taxpayers owing $67 billion. By 2023, Tax Policy Center estimates that 47.8% – nearly half – of all taxpayers would have been subject to AMT without ATRA (Exhibit A).

But ATRA’s success in linking AMT to inflation will not prevent the number of taxpayers owing AMT from growing. Tax Policy Center estimates that 6.1 million taxpayers will be subject to AMT by 2023, owing $47.6 billion during that tax year.

And AMT, which originally targeted the wealthiest taxpayers in the U.S., now has a far broader reach in terms of income levels. Tax Policy Center estimates that 32.3% of those earning $200,000 to $500,000 and 61.6% of those earning $500,000 to $1 million paid AMT in 2014. Of those with incomes over $1 million, Tax Policy Center estimates that only 20.8% paid AMT last year.

What can investors do to avoid AMT?

Normal tax planning strategies may not necessarily help those investors potentially subject to AMT. Because any number of items may be the trigger for the tax, consulting with a tax advisor all year (instead of only around Tax Day) may help identify ways to mitigate the impact of AMT. For example, individuals could work with their tax advisor on the timing of exercising incentive stock options to minimize the tax liability.

However, one frequently overlooked aspect of AMT is that tax-exempt bonds could suddenly become taxable. One pitfall that AMT-impacted investors make is assuming that tax-exempt municipal bonds will help them skirt AMT. This is not always the case.

What does AMT allow?

Taxpayers cannot claim as many deductions for AMT if they itemize, as these deductions must be added back into your income. Itemized deductions that are allowed under AMT include:

- Medical and dental expenses more than 10% of the regular tax AGI.

- Charitable donations.

- AMT investment interest to the extent of net AMT investment income.

- Qualified housing interest.

In general, the income earned on municipal bonds (and funds that own them) is exempt from federal income taxes. Depending on circumstances, interest on these bonds may also be exempt from state and local income taxes. However, some municipal bonds are issued for not-for-profit 501© (3) organizations and private activity issuers, including certain housing agencies, airports and stadiums. These bonds lose their tax-free status under AMT as their use is considered outside of government purposes.

Let’s consider a hypothetical situation of an investor who received $100,000 of tax-exempt income from a private activity bond, but was also subject to AMT. When calculating taxes for the year, the investor would be forced to add back the $100,000 in tax-exempt income and would then have to pay AMT, which could be 28% depending on that individual’s situation. In effect, a tax-exempt bond turned into a taxable bond, completely wiping out all benefits of the tax exemption.

Nevertheless, many municipal bond investors (including mutual funds) buy private activity bonds because these bonds tend to offer a yield that is higher than similar AMT-free bonds. But once AMT is factored in, the after-tax yield comparison between these bonds is not favorable. With municipal bond mutual funds that hold private activity bonds, the impact on the return of an AMT-subject shareholder is less significant, but still meaningful.

Am I affected by AMT?

Taxpayers could owe AMT for tax year 2015 if their taxable income is more than:

- $53,600 for single filers and heads of household.

- $83,400 for a married couple filing a jointly.

If you pay AMT, consider AMT-free muni bonds

AMT can be complex and costly. But since the tax is projected to generate more than $27 billion in revenue in 2014 and more than $47 billion by 2023 (Source: Tax Policy Center), we think it is unlikely Congress will permanently eliminate AMT. If you can take steps to mitigate some of AMT, we think that would be a prudent move.

AMT-free bond funds are a potential solution to this growing problem. Generally speaking, mutual funds offer greater diversification than investors could realize by purchasing individual bonds. By specifically picking bonds that avoid AMT, these AMT-free bond funds may help investors subject to the minimum tax keep more of what they earn. Investors should consult their tax advisor before making any taxrelated investment decisions.

About Risk

An imbalance in supply and demand in the municipal market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. There generally is limited public information about municipal issuers. As interest rates rise, the value of certain income investments is likely to decline. Longer-term bonds typically are more sensitive to interest-rate changes than shorter-term bonds. Investments in income securities may be affected by changes in the creditworthiness of the issuer and are subject to the risk of nonpayment of principal and interest. The value of income securities also may decline because of real or perceived concerns about the issuer’s ability to make principal and interest payments. Investments rated below investment grade (typically referred to as “junk”) are generally subject to greater price volatility and illiquidity than higher-rated investments. Derivative instruments can be used to take both long and short positions, be highly volatile, result in economic leverage (which can magnify losses), and involve risks in addition to the risks of the underlying instrument on which the derivative is based, such as counterparty, correlation and liquidity risk. If a counterparty is unable to honor its commitments, the value of Fund shares may decline and/or the Fund could experience delays in the return of collateral or other assets held by the counterparty. No Fund is a complete investment program and you may lose money investing in a Fund. The Fund may engage in other investment practices that may involve additional risks and you should review the Fund prospectus for a complete description.

About Eaton Vance

Eaton Vance Corp. is one of the oldest investment management firms in the United States, with a history dating to 1924. Eaton Vance and its affiliates offer individuals and institutions a broad array of investment strategies and wealth management solutions. The Company’s long record of exemplary service, timely innovation and attractive returns through a variety of market conditions has made Eaton Vance the investment manager of choice for many of today’s most discerning investors. For more information, visit eatonvance.com.

The views expressed in this Insight are those of the authors and are current only through the date stated at the top of this page. These views are subject to change at any time based upon market or other conditions, and Eaton Vance disclaims any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Eaton Vance are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Eaton Vance fund. Eaton Vance does not provide legal or tax advice. The discussion herein is general in nature and is provided for informational purposes only. There is no guarantee as to its accuracy or completeness. Individuals should consult their own legal and tax counsel as to matters discussed.

Before investing, investors should consider carefully the investment objectives, risks, charges and expenses of a mutual fund. This and other important information is contained in the prospectus and summary prospectus, which can be obtained from a financial advisor. Prospective investors should read the prospectus carefully before investing.

©2015 Eaton Vance Distributors, Inc. | Member FINRA/SIPC | Two International Place, Boston, MA 02110 | 800.836.2414 | eatonvance.com