Two Pillars Support US Growth: Consumers and Corporates

With both the US economy and equity market recording generally solid growth since the financial crisis ended in 2009, some investors may be wondering if the fundamentals that underpinned the recovery have started to weaken. Grant Bowers, portfolio manager, Franklin Equity Group, believes the US economy’s foundation remains sound. He discusses how he believes two pillars—consumer spending and corporate earnings—will continue to support US economic growth, and gives his take on equity valuations and investment opportunities in the current market environment.

Grant Bowers

Vice President, Research Analyst

Franklin Equity Group®

Portfolio Manager, Franklin Growth Opportunities Fund

Looking toward the remainder of 2015, we expect the US economy will strengthen and US equity markets should likely remain positive. Economic growth in the first quarter retreated due to what we feel were transitory issues, including headwinds from a rising dollar, work stoppages at West Coast ports and harsh winter weather, leading to a 0.7% drop in the US gross domestic product during first-quarter 2015.1 We still maintain, however, that the two main pillars of the US economy—consumer spending and corporate earnings—will continue to be supported by moderate economic growth.

Despite a small decline in May, consumer confidence for the first five months of 2015 has been at a higher average level than at any time since May 2004.2 A relatively low unemployment rate and moderate inflation have helped maintain consumers’ upbeat mood. Meanwhile, real disposable personal income—personal income adjusted for inflation and taxes—increased 6.2% in the first quarter of 2015, compared with 3.6% in the fourth quarter of 2014.3 We believe the improving job market, rising personal income, and improving economic sentiment will benefit consumer spending going forward.

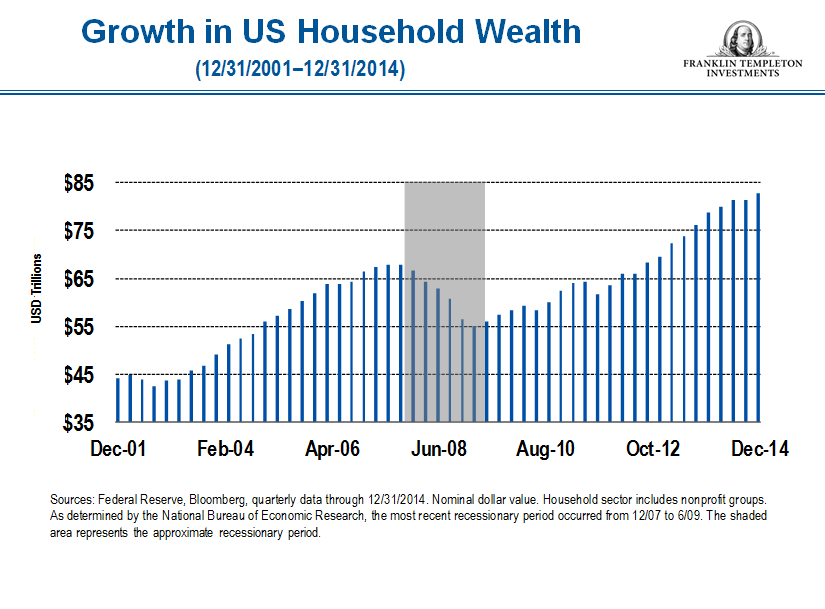

US consumers also have more money in their pockets because, in general, they have aggressively shed their personal debts and increased their savings rate since the financial crisis. We see this as a fundamental, although often overlooked, driver of consumer spending strength in the years ahead.

Corporate Cash Climbs

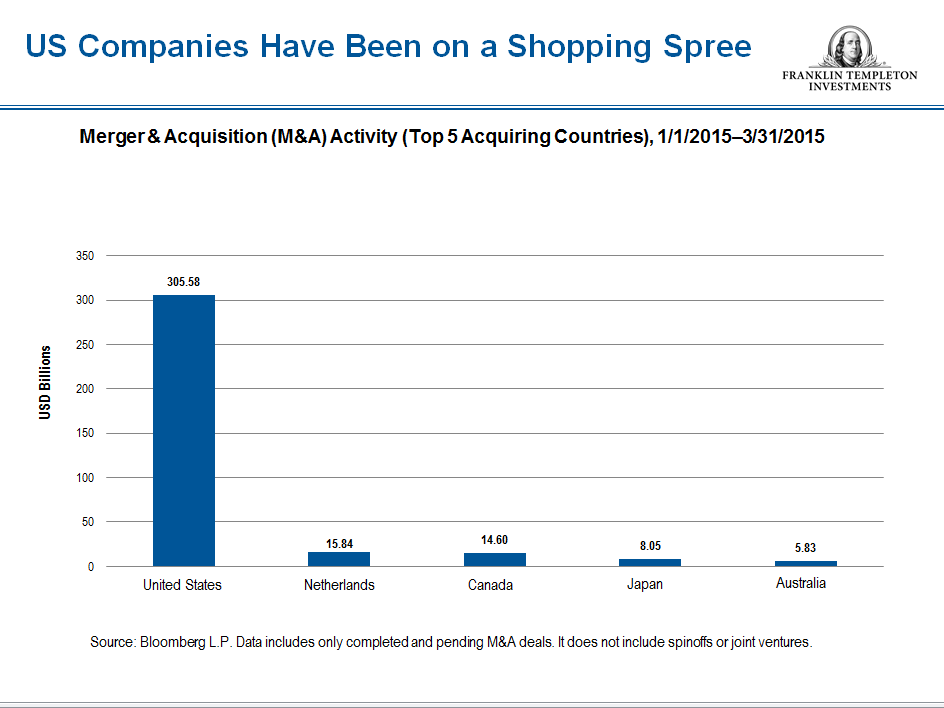

Meanwhile, many US companies have also cleaned up their debts and generated strong earnings in recent years. The result: US companies have stockpiled large amounts of cash on their balance sheets.

The question on many investors’ minds is “What do companies plan to do with this cash in the years ahead?” Areas where corporations have put this cash to work include: continued dividend increases and share buybacks, which return capital back to shareholders; ongoing investment and capital expenditures as well as research and development; and increasing productivity and lowering cost structures.

We think the most meaningful effect of extra corporate cash, however, has been the merger and acquisition (M&A) activity that has occurred in the market recently. We have seen M&A activity accelerate over the last two years, and we believe that trend will continue going forward as US companies continue to acquire strategic assets or consolidate fragmented industries.

But it’s not all good news for US companies. The recent strength in the US dollar versus other currencies such as the euro and yen has created a bit of a headwind to US earnings growth for many multinational corporations. While we believe the current strength in the dollar will likely persist going forward, we don’t see it as a meaningful detractor from earnings growth for many companies over the long term. We still believe corporate earnings will likely continue growing at a modest pace.

Taking Stock

We think the current economic environment, combined with low inflation and low interest rates, provides a solid fundamental backdrop for US equities to continue to perform well throughout 2015 and into 2016. Slow but steady growth has supported a healthy economy, and we believe the market could be stronger for longer than many expect. That said, current valuations in the US market are not as cheap as they were several years ago, but, in our view, they still remain reasonable. We are still finding pockets of opportunity in companies that are growing faster than the overall market and we believe appear poised to deliver sustainable growth over a multi-year time period. These investment opportunities are across all industries and sectors, but we are primarily focusing on what we believe to be high-quality business models that are benefiting from multi-year secular growth trends.

For example, we continue to find attractive opportunities in the health care sector, where very strong secular tailwinds are driving increased usage or consumption of health care in the United States and globally. The combination of aging demographics, better treatment options and new drug innovation are creating an attractive backdrop for investment. Health care companies have also continued to expand their research and development efforts, resulting in innovative discoveries as well as cures and treatments for many diseases. These opportunities are not just in the pharmaceutical and biotech space; we also believe prospects are bright for businesses that provide health care services, tools or diagnostics.

Interest Rates

After years of ultra-accommodative monetary stimulus following the 2008 financial crisis, the US Federal Reserve (Fed) appears poised to raise borrowing costs this year for the first time since mid-2006. With US inflation currently tame and labor market pressures— particularly compensation—still nascent, Fed Chair Janet Yellen reiterated in March that when much-anticipated interest-rate hikes start, they are likely to be small and gradual. We view the prospect for rising rates as a reflection of the healthy economy. Even with the prospect for rising rates in the future, our outlook for US equity markets remains positive. However, we would not be surprised to see periods of market volatility as the Fed prepares to raise interest rates and geopolitical risks remain unresolved. As long-term investors, we find that volatility often brings investment opportunity.

This information is intended for US residents only.

Grant Bowers’s comments, opinions and analyses are for informational purposes only and should not be considered individual investment advice or recommendations to invest in any security or to adopt any investment strategy. Because market and economic conditions are subject to rapid change, comments, opinions and analyses are rendered as of the date of the posting and may change without notice. The material is not intended as a complete analysis of every material fact regarding any country, region, market, industry, investment or strategy.

What Are the Risks?

Franklin Growth Opportunities Fund

All investments involve risks, including possible loss of principal. Growth stock prices reflect projections of future earnings or revenues, and can, therefore, fall dramatically if the company fails to meet those projections. Smaller, mid-sized and relatively new or unseasoned companies can be particularly sensitive to changing economic conditions, and their prospects for growth are less certain than those of larger, more established companies. Historically, these securities have experienced more price volatility than larger company stocks, especially over the short term. To the extent the fund focuses on particular countries, regions, industries, sectors or types of investment from time to time, it may be subject to greater risks of adverse developments in such areas of focus than a fund that invests in a wider variety of countries, regions, industries, sectors or investments. These and other risks are described more fully in the fund’s prospectus.

Investors should carefully consider a fund’s investment goals, risks, sales charges and expenses before investing. To obtain a summary prospectus and/or prospectus, which contains this and other information, talk to your financial advisor, call us at (800) DIAL BEN®/342-5236 or visit franklintempleton.com. Please carefully read a prospectus before you invest or send money.

1 Source: US Department of Commerce, Bureau of Economic Development, 6/3/2015.

2 Source: University of Michigan, Survey of Consumers. Survey was conducted in May 2015.

3 Source: US Department of Commerce, Bureau of Economic Analysis, news release dated 4/29/2015.

© Franklin Templeton Investments