SUMMARY

- The municipal bond market is dramatically different since 2008 due to structural changes, low interest rates and higher taxes.

- These changes have increased the volatility in the municipal bond market, requiring skillful navigation.

- We think municipal investors should consider a go-anywhere, flexible approach that embraces volatility to help generate total return.

Structural changes have increased volatility

The municipal market is vast: approximately 60,000 different issuers, over one million CUSIPs and about $3.7 trillion outstanding. Navigating this disparate universe is tremendously difficult for individual investors and their advisors. Key changes to the municipal market after the 2008 financial crisis have made this task profoundly more difficult, such as:

- Higher tax rates.

- The disappearance of AAA-rated monoline insurers.

- Increases in bank regulation.

- Declining broker-dealer inventories.

- An uptick in credit stresses, including Detroit, Chicago and Puerto Rico.

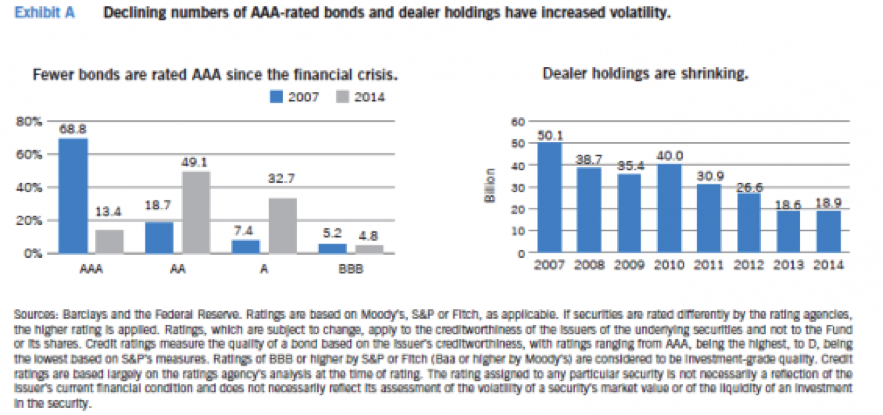

Looking first at municipal bond insurance, seven insurers carried AAA ratings in 2007; none of those insurers are AAA-rated today. As a result, the number of municipal bonds carrying AAA ratings has declined sharply (Exhibit A). Without the backing of a bond insurer, research and relative-value analysis have become top concerns for municipal bond investors.

Declining broker-dealer inventories have also increased the challenges for individual investors. Due to increased regulations, dealers are allocating less capital to municipal bond holdings (Exhibit A), leaving the market without a key stabilizing force during periods of stress and volatility.

Since the financial crisis, there has also been an uptick in credit stresses in the municipal market, with Puerto Rico, Chicago and Detroit among the most notable. The resulting volatility is due to ownership composition of the municipal bond market. According to the Investment Company Institute, individual (or retail) investors are the largest holders of municipal securities. These investors hold 35% of municipal bonds directly and another 36% indirectly through vehicles like mutual funds and exchange-traded funds (ETFs). As the market is heavily retail-driven, negative headlines about these credit stresses tend to have a greater influence on prices.

Shifting leadership requires active management

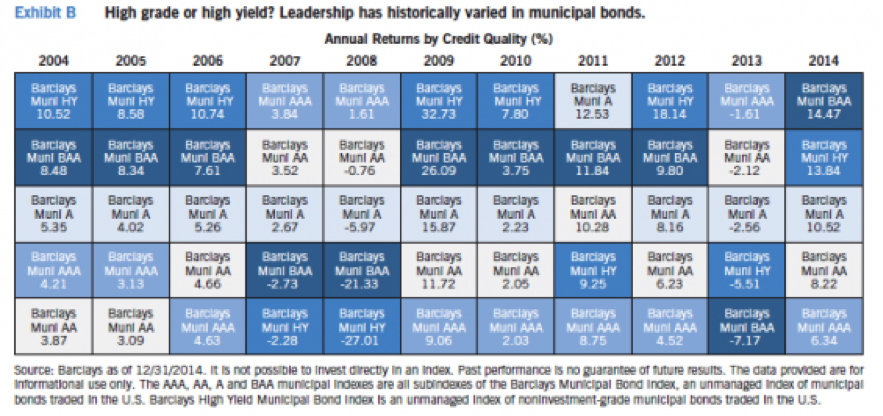

Due to increased volatility in this retail-driven market, we think that investors may want to maintain a greater amount of flexibility with municipal bonds. Municipal returns can come from a number of different areas. For example, Exhibit B shows that annual returns of municipal bonds by credit rating can shift remarkably from year to year.

Having the flexibility to move in and out of holdings based on credit rating is important in our estimation. Investors may need the ability to swap in and out of high grade and high yield based on spread changes across the entire credit spectrum.

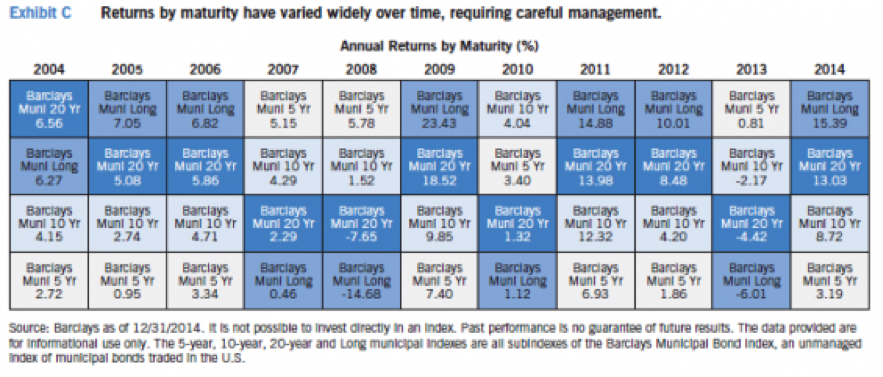

Changes in the yield curve have also historically resulted in leadership changes in the municipal market (Exhibit C). Just as they should watch credit exposure closely, investors should continuously monitor a steepening or flattening of the yield curve and have the flexibility to react accordingly.

In other words, investors and their advisors need the ability to tactically shift positions as needed, whether that means across the credit spectrum or yield curve. We think that it depends on where an experienced municipal bond investor can find compelling value opportunities.

Take a total return approach to municipal bonds

The absolute low level in interest rates also deserves attention. Due to their federal tax-exempt income, municipal bonds have been favored as a source of stable income generation. As such, the municipal bond market has historically had a buy-and-hold mentality. But in this low rate environment, investors are looking to do more than just clip their coupon.

With interest rates as low as they have been over the past few years, a total return approach warrants some attention. Due to inefficiencies created by its retail investor-driven nature, the municipal bond market can be a sensible source of alpha. A lack of transparency and dearth of readily available information on the municipal bond market allows us to find what we believe are compelling opportunities.

As part of this total return strategy, we want to be buying bonds at the time they are not appropriately valued by retail investors. For example, this may include taxable municipal bonds, short-dated corporate-backed municipal bonds, and health care and transportation issues. We also look for opportunities when negative headlines arise and generate volatility, like those we experienced with Detroit, Chicago and Puerto Rico over the past two years.

Stay flexible and opportunistic in today’s municipal bond market

Going forward, the perfect storm of rising interest rates, higher taxes and negative credit headlines may increase volatility in the market. Most municipal bond investment strategies are prospectus-constrained into specific areas of the municipal market. These constraints may include credit quality (high grade or high yield) and duration (long, intermediate or short). Investors may want the latitude to seek municipal sectors, credit tiers and maturities.

In our view, a flexible, total return approach is an appropriate adaptation of a municipal bond strategy for what we think is a more volatile future. This type of approach can serve as a core position for investors looking for tax-advantaged investments. Due to the opportunistic nature, the strategy may be complementary to an existing core municipal bond strategy, allowing a portion of the portfolio to shift focus to where there may be opportunities.

At Eaton Vance, we have embraced this opportunistic, go-anywhere style that allows us to take advantage of volatile markets. We think that in order to truly be opportunistic, investors need to do more than simply take advantage of situations as they arise. In our view, opportunistic means conducting thorough, rigorous research in order to recognize market inefficiencies, and then seeking to capitalize on them. Investors may benefit from the credit research, skill and expertise of experienced professional management to help implement this approach.

About Indexes

Unless otherwise stated, index returns do not reflect the effect of any applicable sales charges, commissions, expenses, taxes or leverage, as applicable. It is not possible to invest directly in an index. Historical performance of the index illustrates market trends and does not represent the past or future performance of any investment.

If you like the views expressed in this Insight, you might be interested in learning more about the following strategy:

About Risk

An imbalance in supply and demand in the municipal market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. There generally is limited public information about municipal issuers. As interest rates rise, the value of certain income investments is likely to decline. Longer-term bonds typically are more sensitive to interest-rate changes than shorter-term bonds. Investments in income securities may be affected by changes in the creditworthiness of the issuer and are subject to the risk of nonpayment of principal and interest. The value of income securities also may decline because of real or perceived concerns about the issuer’s ability to make principal and interest payments. Investments rated below investment grade (typically referred to as “junk”) are generally subject to greater price volatility and illiquidity than higher-rated investments. Derivative instruments can be used to take both long and short positions, be highly volatile, result in economic leverage (which can magnify losses), and involve risks in addition to the risks of the underlying instrument on which the derivative is based, such as counterparty, correlation and liquidity risk. If counterparty is unable to honor its commitments, the value of Fund shares may decline and/or the Fund could experience delays in the return of collateral or other assets held by the counterparty. No Fund is a complete investment program and you may lose money investing in a Fund. The Fund may engage in other investment practices that may involve additional risks and you should review the Fund prospectus for a complete description.

About Eaton Vance

Eaton Vance Corp. is one of the oldest investment management firms in the United States, with a history dating to 1924. Eaton Vance and its affiliates offer individuals and institutions a broad array of investment strategies and wealth management solutions. The Company’s long record of exemplary service, timely innovation and attractive returns through a variety of market conditions has made Eaton Vance the investment manager of choice for many of today’s most discerning investors. For more information, visit eatonvance.com.

Before investing, investors should consider carefully the investment objectives, risks, charges and expenses of a mutual fund. This and other important information is contained in the prospectus and summary prospectus, which can be obtained from a financial advisor. Prospective investors should read the prospectus carefully before investing.

The views expressed in this Insight are those of the author and are current only through the date stated at the top of this page. These views are subject to change at any time based upon market or other conditions, and Eaton Vance disclaims any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Eaton Vance are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Eaton Vance fund. Eaton Vance does not provide legal or tax advice. The discussion herein is general in nature and is provided for informational purposes only. There is no guarantee as to its accuracy or completeness. Individuals should consult their own legal and tax counsel as to matters discussed.

©2015 Eaton Vance Distributors, Inc. | Member FINRA/SIPC | Two International Place, Boston, MA 02110 | 800.836.2414 |eatonvance.com