Shareholder Activism Continues to Attract Assets and Boost Activity

While shareholder activism has been maligned in the past by the corporate world as a way to reap short-term gains at the expense of long-term shareholders, the practice is now enjoying an increasingly positive reputation. This change in perception is based on the beneficial long-term results of activist campaigns and the current view of activists as champions of shareholder value. Accordingly, the recent performance of activist-related investments, as well as their role in providing low-correlated returns has drawn significant interest from the institutional investment world. This influx of capital into activist hedge funds has continued to drive activity in the space.

Executive Summary

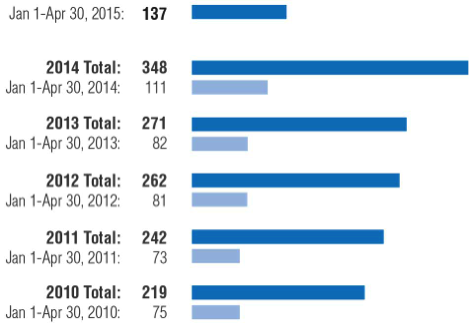

Shareholder activism has become a significant force in the corporate world. Activist activity, in terms of the number of announced activist campaigns increased nearly 30% in 2014 over the 2013 level. And, according to FactSet, the level of activity so far in 2015 is outpacing 2014 with 111 campaigns announced as of April 30, 2015 compared to 82 campaigns at the same point in 2014, up 35%.

In addition, activist engagement at targeted companies is attracting greater amounts of assets into activist hedge funds. By the end of 2014, these funds had $120 billion in assets, also up nearly 30% from 2013. The surge in assets is driving demand for new activist activity, continuing the cycle.

Growth and Performance of Activist Funds

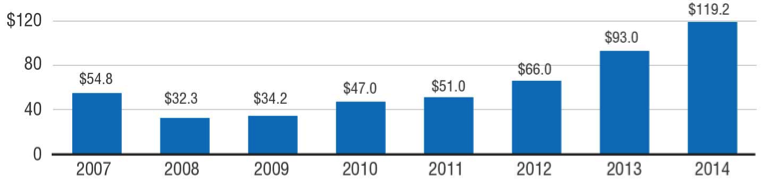

The activism landscape has been exploding in size and activity. As shown in Chart 1, assets under management at dedicated activist hedge funds in the United States grew to $119.2 billion in 2014, up almost 30% from the end of 2013. According to the Economist magazine1 assets have grown 500% in the past 10 years.

Not surprisingly, the number of public activism campaigns also surged in 2014 by over 28% from 271 to 348 according to financial data provider FactSet. The Economist magazine estimated in a February 2015 article that one in seven of the companies in the S&P 500 index have been involved in an activist campaign over the past five years and half have had an activist fund on their register at some point during that timeframe. Also of interest, research firm, Activist Insight, reports that more than two-thirds of activist campaigns are not public.

Chart 1: Activist Fund Assets Under Management

(in Billions)

Source: Hedge Fund Research

In addition, the five-year annual return for the HFRI Activist Index was 10.28% as of the end of May 2015 compared to 5.88% for the HFRI Equity Hedge (Total) Index over the same time period. 2 As a result, institutional investor interest has been intensifying and activist funds have been inundated with capital. This has generated more activist engagements as this money is put to use.

The Activist’s Playbook

Activists would consider most companies to be a legitimate target for scrutiny, however, they tend to avoid companies in regulated industries including financial services companies, where it’s difficult to impact the balance sheet.

What do activist investors look for in a target company? Basically, activists are looking for companies where there is an obvious path to affecting positive change. This is a company-by-company bottom up analysis that is nearly sector agnostic. Chart 2 illustrates the growing momentum of activist campaigns since 2010.

Chart 2: Activist Campaign Activity

Source: FactSet, Activist Campaign Activity tracks publicly disclosed activist campaigns based on the date the campaign was announced.

The most obvious target for an activist is share price weakness. A declining stock price, especially a prolonged depreciation in the value of a company’s shares, is a flashing neon sign begging an activist shareholder to uncover what has gone wrong at the company.

Outside of share weakness, the following five areas are typical activist targets.

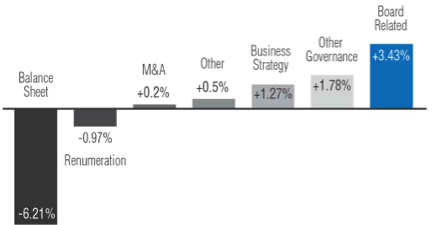

- Board Representation. According to Activist Insight, 2014 saw the greatest increase in board-related activist activity, up almost 3.5% from 2013’s level of activity. A weak board of directors can provide the opportunity for the activist to gain representation on the board, helping to affect the board’s governance policies and to pave the way for getting proposed changes implemented. Also, gaining majority slates has been getting easier, a feat that used to be extremely rare.

- Mergers & Acquisitions (M&A). The same report from Activist Insight notes that 49% of activist campaigns in 2014 were associated with M&A activity. This figure includes the opportunity to create value through a spin-off. When a sum-of-the-parts calculation reveals that breaking up the company can produce more shareholder value than keeping the company intact, management should expect an activist knock on the door.

- Dividends and Share Buybacks. Always a part of the toolbox, activists look for cash-heavy companies that could improve shareholder value by paying a dividend or buying back shares.

- Operational Efficiency. If a company’s core operations are underperforming their peers, there may be a need for more focus on the core business or a sale of non- core business lines that compete for management attention. An activist will explore cost-cutting opportunities to improve margins.

- Weak leadership. Like ineffective boards, a weak or complacent management team can produce a target for activist shareholders. A report commissioned by law firm Schulte Roth & Zabel in 2014 to explore the opinions of shareholder activists and corporate executives, found that 60% of U.S. activists and 76% of U.S. executives think management and board changes will be an important catalyst for activism in 2015.3

Chart 3 below shows the year-over-year change in activity for each activist strategy.

Chart 3: Year-Over-Year Change of Each Activist Strategy 2014/2013

Source: Activist Insight

Trends in Activism

Changing attitudes toward shareholder activism

While the arrival of an activist still evokes some level of dread for a company’s management team and board of directors, they have begun to be viewed as a catalyst for positive change. A 2015 survey of institutional investors by FTI Consulting found that 76% view activism favorably and 84% believe that activism adds value.4

In fact, merger and acquisition advisors have been instructing management teams confronted by a shareholder activist to engage with them in a constructive way rather than trying to fend them off.

Activist investors are also beginning to be viewed as more long-term oriented. In an often-cited study of activist hedge fund activity from 1997-2007 by Harvard Law professor Lucian Bebchuk, et al, the authors found that even five years after an activist intervention, there was improvement in the long-term operating performance of the target company.5

Further support comes from the stock performance of target companies, with an average increase of 25% over the two-year period following the activist’s sale, according to a 2015 report from the Alternative Investment Management Association (AIMA).6

Companies are on the alert for activists

Increasingly, companies are evaluating their vulnerabilities by analyzing their competitive position relative to peers. The companies that lag, whether in stock price performance, valuation metrics, capital efficiency, innovation, etc., are often activist targets.

The 12th annual What Directors Think survey released in February 2015, indicates board members believe that shareholder engagement is increasing in importance and 62% said that “clear protocols” for this were in place for their board.7

Proactive and transparent outreach to key shareholders about the company’s long-term strategy is crucial to having these large stakeholders willing to support the board during an activist campaign. A recent report from consulting firm Strategy& states, “A chief weapon of activists is their ability to tell a better story than a company’s management–it is their best route to the hearts and minds of shareholders.”8

However, there is still a lot of room for improvement as only about 10% of respondents in the What Directors Think survey said they had undertaken any sort of role playing or coaching with respect to an activist encounter.

Activist investors are becoming more sophisticated

As shareholder activism evolves, newer tactics are being put into play, such as partnering with a strategic acquirer or taking on a co-investing alignment with a pension fund, mutual fund or other institutional investor.

Further, the amount of effort and the expense involved in the research and due diligence on target companies has increased significantly. Activists now routinely hire outside consultants and advisors to help in conducting highly-detailed analysis on the target company and in developing long-range, comprehensive plans of action.

Steve Wolosky, a partner at law firm Olshan, Frome & Wolosky said, “Activists’ diligence on target companies is outpacing the information that company directors, themselves, know about their company.”9

Activists are targeting larger companies

While activist targets used to be small- and mid-cap companies, today there is activity across the capitalization spectrum. The ability to meaningfully engage larger companies has been driven by the greater amounts of capital that activist funds now have at their disposal.

There is also more potential for these larger companies to be “fat and sleepy” and, consequently, not optimizing shareholder value.

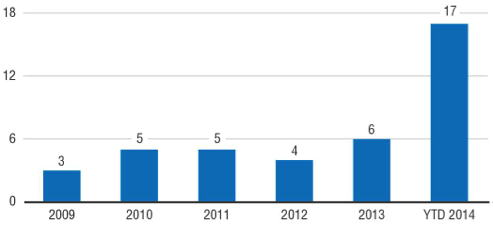

Chart 4: Activists Campaigns At Companies With A Market Cap Greater Than $25B*

Source: SharkRepellent as of 12/15/2014.

*Represents the following campaign types: Board control and representation, enhance corporate governance, maximize shareholder value and remove directors and officers.

The “lazy money” is waking up

In February 2015, the Economist magazine reviewed the activist landscape and pointed out that the majority of an S&P 500 company’s investors are passive index funds, or essentially “software programs.” They also refer to this investor base as “lazy money” since it relies on proxy advisors to recommend how to vote its shares.

Similarly, in an article he wrote recently for a UCLA publication, David Karp, a partner at the law firm Wachtell, Lipton, Rosen & Katz, called attention to the fact that proxy advisor Institutional Shareholder Services “is functionally the largest voting shareholder in U.S. public companies despite holding no economic interest in these companies.”10

However, in early March 2015, The Wall Street Journal reported that both Vanguard and BlackRock are becoming more involved in corporate governance issues for the companies in their portfolios. The article quotes from a letter sent by Vanguard’s Chairman and CEO, F. William McNabb III to hundreds of its portfolio companies. “In the past, some have mistakenly assumed that our predominantly passive management style suggests a passive attitude with respect to corporate governance. Nothing could be further from the truth.”11

Activist campaigns are being initiated with smaller positions

It used to be that an investor needed to acquire a 5-10% stake in a company in order to wield any influence over management. That has changed recently to where a 2-3% stake can be successful in bringing about change. This is partly the result of the trend discussed previously of large institutional investors or fund managers quietly partnering with activists and thereby contributing additional pressure in the campaign.

Additionally, there are investors who track activist activity either as a “wolf pack activist” or more benignly as an “activist follower.” The activist follower is an investor who invests according to how activists invest. Wolf packs are activist investors who loosely coordinate to invest in a company and amass a large amount of stock, and therefore influence, “under the radar screen.” In this scenario, the separate activists can buy shares at better prices than if the same amount of stock were purchased by a single investor. At the same time, the target company isn’t tipped to the activist position that is building. This activity, however, is only “alleged” because it is illegal in practice.12

Tax-advantaged yield vehicles are growing in popularity

Over the last year and a half, activists have been trying to encourage companies to monetize their real estate assets by converting them to a REIT or MLP structure. This structure increases shareholder value as funds from operations multiples are greater than those that value a company on an EBITDA (earnings before interest taxes depreciation and amortization) basis. This is due to the requirement to pay out most of it’s earnings as dividends, thereby paying little to no corporate tax.

It used to be that an investor needed to acquire a 5-10% stake in a company in order to wield any influence over management. That has changed recently to where a2-3% stake can be successful in bringing about change.

This is a trend that is driven by investor demand for attractive yield securities in a low interest rate environment in addition to rising real estate values. The trend also transcends sectors – it involves any company that has real estate assets that could be serviced through a yield vehicle. Obvious examples would be restaurants, retailers, casino operators and hotels. Less apparent examples would be data storage companies and paper companies, which are looking to convert their mills into MLPs.

Criticism of Activist Campaigns

While the improved perception of activist shareholders was discussed earlier, there are still critics who believe the existence of activists is a nuisance, at best, and more likely a destructive force for the target company and the economy.

Most notably, Martin Lipman, a founding partner at Wachtel, Lipton, Rosen & Katz has been an outspoken opponent of the practice for four decades. Mr. Lipman has acknowledged that some shareholder activism is appropriate, but he criticizes any campaign with a short-term objective. “With the increase in activist hedge fund attacks, particularly those aimed at achieving an immediate increase in the market value of the target by dismembering or overleveraging, there is a growing recognition of the adverse effect of these attacks on shareholders, employees, communities and the economy.”13

Short-termism is a common complaint by activism’s detractors and a 2015 survey of institutional investors by FTI Consulting noted that 61% believed the threat of activism discouraged companies from making decisions for the long term.14

But the data on activist holding periods is inconsistent. The law firm Schulte Roth & Zabel survey found that average holding periods are shortening with only 36% of activist investments held for a year or more, down from 60% in the firm’s 2012 survey.15 And, a January 2015 report from J.P. Morgan cites data from research provider SharkRepellent showing that 47% of activist investments are less than six months while only 16% hold the target shares for two or more years.16

However, the report from AIMA cites that the average holding period for an activist hedge fund is two years. Activists also are incented to have a longer-term investment period considering the time and effort associated with the research and creation of an action plan, which is often long-term in nature. Further, if a member of the activist hedge fund is named to the target company’s board, it limits the fund’s ability to sell as an insider.17

Another criticism involves the distraction that an activist campaign creates for management, the board of directors, employees and even customers and suppliers of the target company. As well as being time consuming, addressing an activist campaign can also be costly. The report from Strategy& indicates that legal and advisory costs of a proxy battle can run from $10-$20 million dollars.18

Lastly, corporate bondholders can sometimes come out on the losing end of a shareholder activist campaign. The strategies that activists pursue are designed to benefit the equity shareholder, sometimes at the expense of the bondholder.

Outlook for Shareholder Activism

While the Schulte Roth & Zabel survey of activists and corporate executives found that 52% believe the current success and popularity of activism will eventually limit future opportunities, 98% expect volume to increase in 2015 (50% think it will significantly increase and 48% think it will somewhat increase).

In a video interview with online publication The Deal in November 2014, David Rosewater of Schulte Roth & Zabel said, “There’s always cyclicality, but I don’t think that activism is anything but here to stay.” From the standpoint of the number of campaigns and the size of the companies being impacted, we concur that shareholder activism looks to continue its growth trajectory in 2015.

References

1 “Sometimes ill mannered, speculative and wrong, activists are rampant. They will change American capitalism for the better,” The Economist, February 7, 2015.

2 Id.

3 “2014 Shareholder Activism Insight Report,” Schulte Roth & Zabel, October 2014.

4 “2015 Shareholder Activist Landscape,” FTI Consulting, Inc., 2015.

5 Bebchuk, Lucian A. and Brav, Alon and Jiang, Wei, The Long-Term Effects of Hedge Fund Activism (December 2014). Forthcoming, Columbia Law Review, Vol. 114, June 2015; Columbia Business School Research Paper No. 13-66.

6 “Unlocking Value: The Positive Role of Activist Hedge Funds,” AIMA, February 24, 2015.

7 “12th Annual What Boards Think,” Corporate Board Member, February 2015.

8 “Shareholder Activism Strategies for Mitigating Risk and Responding Effectively,” Strategy&, March 12, 2015.

9 “2015 Private Fund Report: The Role of Activist Funds,” The Lowell Milken Institute for Business Law and Policy at UCLA School of Law, 2015.

10 Id.

11 Grind, Kirsten and Lublin, Joann S. “Vanguard And BlackRock Raise Voices,” The Wall Street Journal, March 4, 2015.

12 Brav, Alon and Dasgupta, Amil and Mathews, Richmond D., Wolf Pack Activism (November 18, 2014). Robert H. Smith School Research Paper No. RHS 2529230.

13 Lipton, Martin. “The Threat to the Economy and Society from Activism and Short-Termism-Updated,” Harvard Law School Forum on Corporate Governance and Financial Regulation, January 27, 2015.

14 “2015 Shareholder Activist Landscape,” FTI Consulting, Inc., 2015

15 Id. at 3.

16 “The Activist Revolution,” J.P. Morgan, January 2015.

17 Id. at 9.

18 Id. at 8.

Disclosure

The fund’s investment objectives, risks, charges and expenses must be considered carefully before investing. The statutory prospectus and, if available, summary prospectus contains this and other important information about the investment company, and it may be obtained by calling 1-855-9VISIUM. Read it carefully before investing.

Mutual fund investing involves risk. Principal loss is possible. Event-driven investments carry the risk that an expected event or transaction may not be completed, or be completed on less favorable terms than expected. Investments in debt securities typically decrease in value when interest rates rise. This risk is usually greater for longer-term debt securities. Investments in lower-rated and non-rated securities present a greater risk of loss to principal and interest than higher rated securities. The fund may make short sales of securities, which involves the risk that losses to those securities may exceed the original amount invested by the Fund. Investments in foreign securities involve greater volatility and political, economic and currency risks and differences in accounting methods. These risks are greater for emerging markets. Investments in micro, small and medium capitalization companies involve less liquidity and greater volatility than investments in larger companies. The Fund may use certain types of investment derivatives such as futures, forwards, and swaps. Derivatives involve risks different from, and in certain cases, greater than the risks presented by more traditional investments. The Fund may purchase IPOs (initial public offerings) which can fluctuate considerably and could have a magnified impact on fund performance when the Fund’s asset base is small. The Fund may invest in other investment companies and ETFs and will bear its share of fees and expenses, in addition to indirectly bearing the principal risks of those underlying funds. The Fund may have a higher turnover rate which could result in higher transaction costs and higher tax liability which may affect returns.

Opinions expressed are subject to change at any time, are not guaranteed and should not be considered investment advice.

Nothing contained in this communication constitutes tax or investment advice. Investors must consult their tax advisor or legal counsel for advice and information concerning their particular situation.

Correlation is a statistical measure of the degree to which the movements of two variables (stock/option/convertible prices or returns) are related.

EBITDA: Earnings before interest, taxes, depreciation and amortization is an approximate measure of a company’s operating cash flow based on data from the company’s income statement. Calculated by looking at earnings before the deduction of interest expenses, taxes, depreciation, and amortization.

HFRI Equity Hedge (Total) Index - Equity Hedge: Investment Managers who maintain positions both long and short in primarily equity and equity derivative securities. A wide variety of investment processes can be employed to arrive at an investment decision, including both quantitative and fundamental techniques; strategies can be broadly diversified or narrowly focused on specific sectors and can range broadly in terms of levels of net exposure, leverage employed, holding period, concentrations of market capitalizations and valuation ranges of typical portfolios. EH managers would typically maintain at least 50% exposure to, and may in some cases be entirely invested in, equities, both long and short.

HFRI ED - Activist Index: Activist strategies may obtain or attempt to obtain representation of the company’s board of directors in an effort to impact the firm’s policies or strategic direction and in some cases may advocate activities such as division or asset sales, partial or complete corporate divestiture, dividend or share buybacks, and changes in management. Strategies employ an investment process primarily focused on opportunities in equity and equity related instruments of companies which are currently or prospectively engaged in a corporate transaction, security issuance/repurchase, asset sales, division spin-off or other catalyst oriented situation. These involve both announced transactions as well as situations which pre-, post-date or situations in which no formal announcement is expected to occur. Activist strategies are distinguished from other Event Driven strategies in that, over a given market cycle, Activist strategies would expect to have greater than 50% of the portfolio in activist positions, as described.

The S&P 500 Index is a broad based unmanaged index of 500 stocks, which is widely recognized as representative of the equity market in general. You cannot invest directly in an index.

The Visium Event Driven Fund is distributed by Quasar Distributors, LLC.