Summary

- The U.S. bond market has enjoyed a 30-plus-year bull run that has driven interest rates to historic lows, leaving many investors with paltry yields and exposed to risk.

- With the U.S. economy continuing to slowly but steadily improve, we believe interest rates are likely to rise relatively soon at both the short and long ends of the yield curve.

- Against this backdrop, we believe investors should take an active approach to duration management and favor assets that have historically benefited from a rising rate environment.

The ultralow yield environment of recent years has been challenging for many income investors – and it’s about to get more challenging. With the U.S. economy gradually improving and interest rates poised to rise, many traditional bond investments are vulnerable to potentially significant price declines going forward (perhaps most notably, those that are shorter-duration in nature). As a result, many investors may need to rethink their approach to income investing.

In a recent interview, Eric Stein and Andrew Szczurowski, co-portfolio managers for Eaton Vance Short Duration Strategic Income Fund, discussed these issues and how investors might seek to navigate a changing interest-rate landscape.

Why have yields been so low in the U.S. and other developed markets?

Eric: There are several reasons. In general, global economic growth has been sluggish over the past year or so, and growth prospects in the key developed markets of Europe and Japan have been particularly lackluster. Both of those regions have been grappling with deflationary pressures and have implemented large-scale quantitative easing programs that have pushed yields down to artificially low levels.

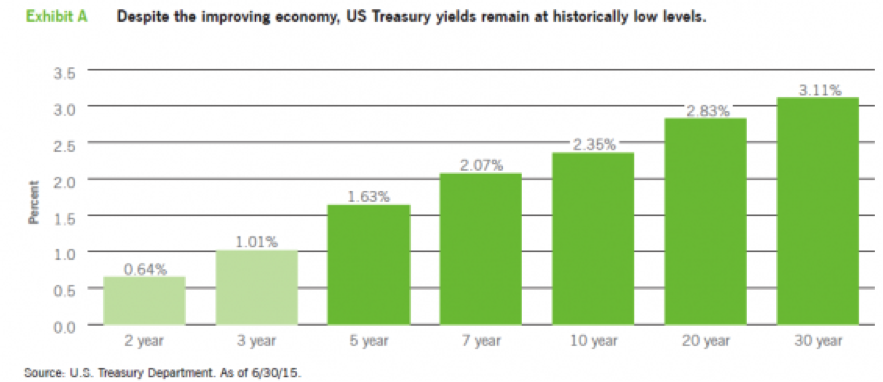

In the U.S., the bond market has enjoyed a 30-plus-year bull run that has driven prices way up and yields way down (Exhibit A). That trend was accelerated in recent years by the bold steps the U.S. Federal Reserve (Fed) took to stimulate the economy following the 2008 financial crisis. The Fed aggressively slashed short-term interest rates and completed multiple rounds of its own quantitative easing, which involved buying trillions of dollars of Treasurys and mortgage-backed securities to suppress longer-term rates. These extraordinary measures worked in that they helped keep the financial crisis from spiraling further out of control, but they left many income investors with paltry yields and potentially overvalued bonds on a forward-looking basis.

But the U.S. ended its quantitative easing policies in late 2014, and the U.S. economy has been gradually improving. So why haven’t yields here picked up much?

Andrew: At the short end of the yield curve, it’s largely because the Fed hasn’t raised its benchmark short-term interest rate since 2006. In fact, the central bank has kept the federal funds rate anchored near zero – the lowest it’s ever been – since 2008. The Fed doesn’t want to tighten prematurely. In terms of longer-term rates, if you look at the yield on the 10-year Treasury, it was only 2.35% as of June 30, 2015. That seems astonishingly low given the relatively healthy state of the U.S. economy.

Why so low? One reason is that U.S. inflation and inflation expectations have remained fairly tame, despite the improving economy. Also, strong foreign demand for U.S. government bonds has helped depress yields here. For example, many income-seeking investors in Europe would rather buy Treasurys than even lower-yielding government bonds in, say, Germany or Switzerland. And, the U.S. is still considered the safest, most liquid market in the world to park cash. That’s why the governments of China and other countries have continued to buy and hold massive amounts of Treasurys.

What’s your outlook for the U.S. economy going forward?

Eric: The U.S. economy has been slowly but steadily improving over the past few years, and we expect that to continue, barring an unforeseen shock to the economy. Home prices have risen, as has industrial capacity utilization. The labor market has gotten better, as reflected in recent unemployment and payroll data. We’ve even started to finally see some wage growth, which had been notably absent for some time.

Granted, GDP growth for the first quarter of 2015 was weak, suggesting that the economy hit a soft patch, but that was not entirely unexpected. First-quarter growth was most likely distorted by what the Fed called “transitory” factors, such as West Coast port strikes, severe winter weather and adjustments to the negative impact of a stronger U.S. dollar on exports. With oil prices lower and general financial conditions (excluding the dollar) pretty easy, we believe consumer spending and other data going forward should revert to showing a U.S. economy that is gradually strengthening. The second quarter has shown a meaningful uptick, with the housing and labor markets particular areas of strength for the economy.

And what does that outlook mean for U.S. interest rates?

Andrew:At the short end of the curve, which is most sensitive to Fed action and the economy, the Fed is being very data-dependent. We’ve been saying for a while now that we believe the Fed is likely to tighten monetary policy at its September 2015 meeting. That’s our base case scenario, and the economic data recently has given us no reason to alter that view. For example, the wage growth that’s begun to materialize in some of the data lately is something the Fed had been hoping to see. Also, the recent halt in the dollar’s meteoric rise makes it easier for the Fed to hike short-term rates sooner rather than later. The main reason the Fed could delay its first rate hike past September would be due to overseas events (e.g., Greece or China).

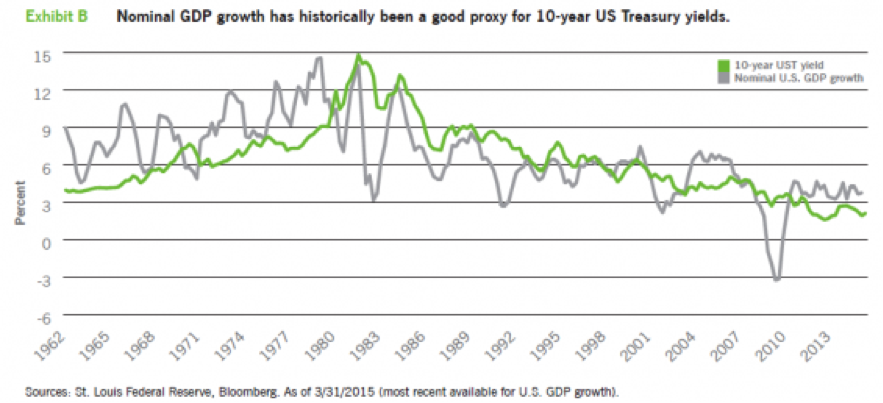

Interest rates are also likely to rise at the longer end of the yield curve if the economy continues to gain momentum. Take the 10-year Treasury, for example. Although demand for longer-dated Treasurys has remained strong (putting downward pressure on yields), over the long term, nominal U.S. GDP growth has historically been a pretty good proxy for 10-year Treasury yields (Exhibit B).

Eric: The bottom line is that rates have been more or less stuck at historic lows for an extended period, and it’s only a matter of time before they rise. We believe we’re getting closer to that point.

How can investors successfully navigate a rising rate environment in the period ahead?

Andrew: Simply stated, rising rates are not good for traditional bond investments. A rising fed funds rate is especially problematic for short-duration ones that invest largely in two- to three-year investment-grade corporates and earn very little yield these days – the math is simply not in their favor. In our view, there’s very little room left for traditional short-term bond strategies to earn returns above zero going forward. So, many investors may need to do something different. But that doesn’t necessarily mean avoiding interest-rate risk and trying to mitigate losses. To us, it also means treating rising rates as an opportunity, rather than just a threat. With that in mind, we would advocate a multisector short-duration strategy that is highly flexible, but managed according to some parameters and guidelines.

Eric: In our strategy, for example, we currently favor sectors and asset classes that have historically tended to benefit from an improving U.S. economy and a rising rate environment. Specifically, high-yield corporate bonds and floating-rate loans may perform relatively well against that backdrop. Negative-duration assets are also worth considering – for instance, mortgage-backed securities that would benefit from slowing mortgage refinancing as interest rates rise. In terms of currencies, with the Fed set to hike, we have been long the U.S. dollar versus other major developed-market currencies.

We also think it’s important to take a very active approach to duration management and to have broad, diversified duration exposure. By that, we mean select exposures to different parts of the yield curve and across different parts of the globe.

About Risk

Investments in foreign instruments or currencies can involve greater risk and volatility than U.S. investments because of adverse market, economic, political, regulatory, geopolitical or other conditions. In emerging countries, these risks may be more significant. An imbalance in supply and demand in the income market may result in valuation uncertainties and greater volatility, less liquidity, widening credit spreads and a lack of price transparency in the market. Investments in income securities may be affected by changes in the creditworthiness of the issuer and are subject to the risk of nonpayment of principal and interest. The value of income securities also may decline because of real or perceived concerns about the issuer’s ability to make principal and interest payments. Derivative instruments can be used to take both long and short positions, be highly volatile, result in economic leverage (which can magnify losses), and involve risks in addition to the risks of the underlying instrument on which the derivative is based, such as counterparty, correlation and liquidity risk. If a counterparty is unable to honor its commitments, the value of Fund shares may decline and/or the Fund could experience delays in the return of collateral or other assets held by the counterparty. As interest rates rise, the value of certain income investments is likely to decline. The value of commodities investments will generally be affected by overall market movements and factors specific to a particular industry or commodity, including weather, embargoes, tariffs, or health, political, international and regulatory developments. Because the Fund may invest significantly in a particular geographic region or country, value of Fund shares may fluctuate more than a fund with less exposure to such areas. Investments rated below investment grade (typically referred to as “junk”) are generally subject to greater price volatility and illiquidity than higher-rated investments. A nondiversified fund may be subject to greater risk by investing in a smaller number of investments than a diversified fund. No Fund is a complete investment program and you may lose money investing in a Fund. The Fund may engage in other investment practices that may involve additional risks and you should review the Fund prospectus for a complete description. Past performance is no guarantee of future results. Diversification cannot ensure a profit or eliminate the risk of loss.

The views expressed in this Insight are those of Eric Stein and Andrew Szczurowski and are current only through the date stated at the top of this page. These views are subject to change at any time based upon market or other conditions, and Eaton Vance disclaims any responsibility to update such views. These views may not be relied upon as investment advice and, because investment decisions for Eaton Vance are based on many factors, may not be relied upon as an indication of trading intent on behalf of any Eaton Vance fund.

This Insight may contain statements that are not historical facts, referred to as forward-looking statements. A Fund’s actual future results may differ significantly from those stated in forward-looking statements, depending on factors such as changes in securities or financial markets or general economic conditions, the volume of sales and purchases of Fund shares, the continuation of investment advisory, administrative and service contracts, and other risks discussed from time to time in the Fund’s filings with the Securities and Exchange Commission.

Before investing, investors should consider carefully the investment objectives, risks, charges and expenses of a mutual fund. This and other important information is contained in the prospectus and summary prospectus, which can be obtained from a financial advisor. Prospective investors should read the prospectus carefully before investing.

©2015 Eaton Vance Distributors, Inc. | Member FINRA/SIPC | Two International Place, Boston, MA 02110 | 800.836.2414 | eatonvance.com