When the Fed Begins to Tighten, Quality Stocks Matter

By Jeff Moser, portfolio manager and chief operating officer at Golden Capital Management, LLC, a subadvisor of Wells Fargo Advantage Funds.

The wait is on for the Federal Reserve (Fed) to tighten money supply. After six years of slow and steady economic recovery, the Fed has finally signaled its intent to raise (or normalize) interest rates.

The Fed’s past policy action, known as quantitative easing (QE), in response to the 2008–2009 financial and real estate crisis, was a huge provider of liquidity into the banking system, U.S. economy, and financial markets. As a result, lower-quality, higher-risk assets were tremendous beneficiaries of the massive liquidity injected into the U.S. banking system. The boost to low-quality securities was most powerful at the start of QE, but the effect weakened as monetary stimulus declined.

The question for investors now is what sort of companies stand to benefit the most as Fed stimulus exits the system?

When the Fed begins to tighten money supply and remove liquidity, equity investors will likely transition from favoring low-quality companies to higher-quality ones. Quality seems like a simple concept; however, it is not as easily defined as other investment terms such as valuation or relative strength. There can be many aspects to quality, and a comprehensive investment process should attempt to analyze and invest in multiple dimensions.

Moreover, not all quality stocks are created equal. In a potentially rising-interest-rate environment, investors should look for these five indications of quality:

1. Seek high-quality stocks with earnings stability.

Relative volatility of changes in earnings per share (EPS) is a measure of quality. Comparing the volatility of 12-month EPS of a company with the median volatility of EPS within its sector provides an indication of the relative stability of a company’s EPS as compared with its sector peers. A lower ratio indicates a relatively greater level of EPS stability. A broader and more diverse customer base, often a strong indicator of quality, allows for more EPS stability.

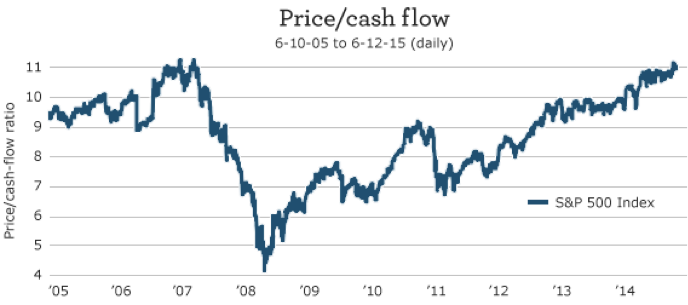

2. Choose stocks with attractive free cash flow at a reasonable price.

Free-cash-flow yield is also a measure of quality; it compares a company’s past 12 months’ free cash flow with its current market price. It begins with cash flow from operations and adjusts that figure by subtracting capital expenditures. The resulting free cash flow is available for other investment, debt reduction, share repurchases, and dividends. Strong and sustained free cash flow is a measure of quality showing strong sales but can also be helped by smart management that avoids overinvesting at what might be the peak of a cycle.

For the broader market, free cash flow comes with an increasingly high price. However, if you look carefully, there are still attractively valued companies that are relatively undiscovered.

Source: Compustat North America via FactSet

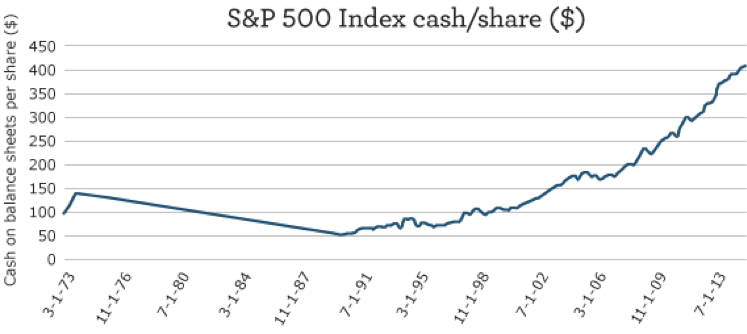

3. Don’t downplay the importance of balance-sheet strength (cash).

Higher levels of cash generally translate into greater financial flexibility. Cash can be used for a myriad of purposes, including productive investment (for example, capital purchases and replacement and acquisitions), debt reduction, share repurchases, and dividends. Debt is another method of financing these projects, but as debt levels increase, so do its demands on cash flow and earnings. Debt financing has a limit. Equity is a third method of financing projects. The equity level on the balance sheet reflects retained earnings, which may be held in cash, as well as the value of outstanding stock. During the Fed’s QE phase, especially in 2009 to 2010, companies lacking balance-sheet strength (high debt, cash-strapped, raising capital via share issuance or debt as opposed to organic growth) benefited from cheap credit and higher share prices. As the Fed withdraws stimulus and begins to tighten policy, credit will become more expensive and investors are likely to look to companies that can leverage their own strengths to grow their businesses, manage their balance sheets, and return capital to shareholders.

Cash on balance sheets has increased over the past several years. It is important to pay attention to how companies are likely to use that cash going forward.

Source: Bloomberg

4. Consider investment in companies with moderate inventory levels.

Inventory accruals measure the year-over-year change in inventory levels relative to total assets. Rising inventories may be an incidental result of slowing sales or an intentional inventory build. In the latter, there is a risk of overestimating future sales, which could lead to future earnings disappointments. Additionally, there are costs and risks associated with inventories due to carrying costs and obsolescence. The semiconductor industry is an example of a fast-paced, fast-changing industry where inventory levels are significantly influenced by product advantages and capacity utilization.

5. Remember the benefit of increasing dividends or share repurchase programs.

Share repurchases are accretive to current shareholders (increases the value of their holdings), while the issuance of shares dilutes share value. Share repurchases are also sometimes viewed as management’s belief that a stock is undervalued, while the issuance of shares is viewed as a sign of overvaluation. Repurchasing shares is an alternative to paying dividends, and the transaction does not result in double taxation like a dividend. The repurchase yield (that is, the percentage decline in shares outstanding) is analogous to a dividend yield. We add the dividend yield to the change in shares outstanding to get a more complete view of the total payout to investors.

When the Fed was providing liquidity, carrying out its program of quantitative easing, and interest rates were falling, low quality was a significant and sometimes dominant theme. We expect that high-quality characteristics will benefit stocks in a rising-rate environment, realizing it may not be the sole or dominant theme to the degree that low quality was in the QE and falling-rate environment. That being said, we expect higher-quality stocks with improving fundamentals to provide investors with upside opportunity and protect against downside risk in a rising-interest-rate environment.

Please visit our blog, AdvantageVoice, for additional viewpoints from Wells Fargo Asset Management’s investment strategists, portfolio managers, and practice management experts. You can also follow us on Twitter at @WFAssetMgmt for real-time updates. Are you an advisor or institutional investor? Check out our website for investment professionals.

The views expressed are as of June 30, 2015 and are those of Jeff Moser, and Wells Fargo Funds Management, LLC. The information and statistics in this report have been obtained from sources we believe to be reliable but are not guaranteed by us to be accurate or complete. Any and all earnings, projections, and estimates assume certain conditions and industry developments, which are subject to change. The opinions stated are those of the authors and are not intended to be used as investment advice. The views and any forward-looking statements are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally, or any mutual fund. Wells Fargo Funds Management, LLC, disclaims any obligation to publicly update or revise any views expressed or forward-looking statements.

Wells Fargo Funds Management, LLC, a wholly owned subsidiary of Wells Fargo & Company, provides investment advisory and administrative services for Wells Fargo Advantage Funds®. Other affiliates of Wells Fargo & Company provide subadvisory and other services for the funds. The funds are distributed by Wells Fargo Funds Distributor, LLC, Member FINRA, an affiliate of Wells Fargo & Company.

Not FDIC Insured • No Bank Guarantee • May Lose Value

© Wells Fargo Asset Management