The Case for Hedge Fund Strategies in a Rising-Rate Environment

By Dr. Sudhir Krishnamurthi, Ronald van der Wouden, and Kenneth LaPlace from The Rock Creek Group, LP (Rock Creek). Dr. Krishnamurthi, Mr. van der Wouden, and Mr. LaPlace are portfolio managers of the Wells Fargo Advantage Alternative Strategies Fund.

As the Federal Reserve (Fed) begins to normalize monetary policy by raising interest rates, yields will rise and prices will decline. Historically, this equation has been positive for alternative investments and more challenging for some areas of fixed-income investments.

Rising yields and declining prices pose risks to fixed-income investments, especially those that are longer duration, as price moves inversely with yields, and price declines can often more than offset any increase from a higher coupon.

Conversely, hedge fund managers tend to hedge out their duration (interest-rate risk) and therefore can often limit a negative impact on performance when interest rates rise. While we have limited data in terms of rising-rate interest environments over the past two decades, every historical scenario we analyzed shows that hedge fund investments outperformed traditional fixed-income investments in past rising-rate environments.

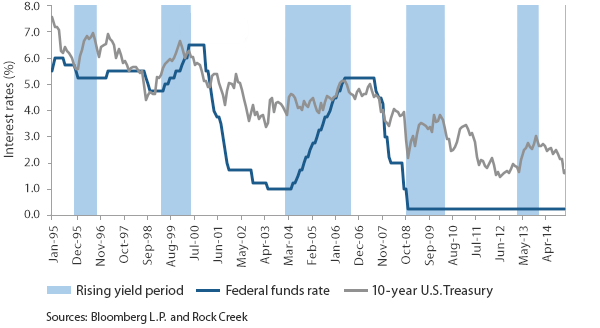

The graph below shows the 10-year Treasury return over the past 20 years. The highlighted periods of rising yields for the U.S. Treasury indicate challenging environments for fixed-income investments. These periods often coincided with Fed rate increases or when there was anticipation of such increases.

Past performance is no guarantee of future results.

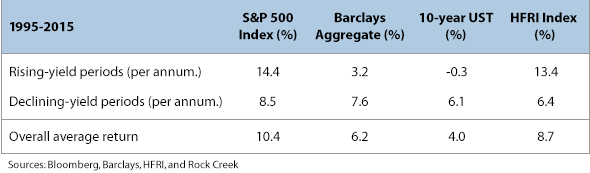

In the following table and graph, an analysis of the performance of the HFRI Hedge fund index over the past 20 years, from 1995 to 2015, shows that hedge funds have outperformed fixed income during periods of a rising 10-year U.S. Treasury yield.

Past performance is no guarantee of future results.

Past performance is no guarantee of future results.

The sources of hedge fund returns in rising interest-rate environments

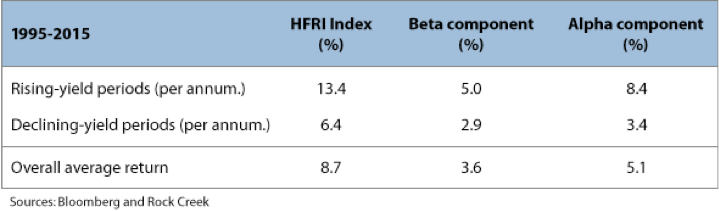

Others have highlighted this trend, but we would like to go one step further to examine the sources of return for hedge funds. We broke down hedge fund returns during rising and declining yield environments into a beta component and an alpha component.

Past performance is no guarantee of future results.

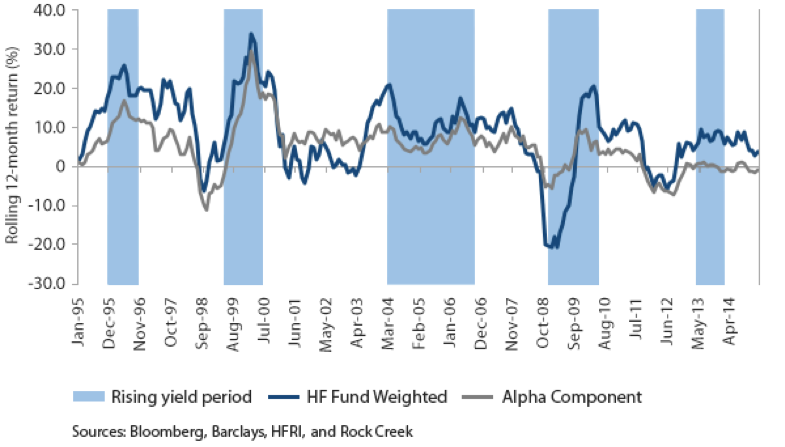

The beta component reflects the return that investors can achieve from investing in markets, while the alpha component reflects the return achieved by managers’ skills in investments, such as stock selection, sector rotation, geographic orientation, varying market exposure, shorting, etc. The alpha component is essentially the value add of hedge funds, and unsurprisingly, the majority of hedge funds’ returns over the past 20 years were derived from the alpha component, and most were additive. A less-discussed and perhaps more important finding that this analysis illustrates is that the alpha component is significantly higher in rising-yield periods, indicating that this environment provides an even better investment opportunity set for hedge funds. It is worth noting that in this analysis, the manager’s skill in increasing or decreasing a portfolio’s market exposure is held constant across different yield environments. As a result, manager’s changes to beta will show up as part of the alpha component. This is an interesting aspect of the analysis that we may explore in the future.

Rising interest rates can lead to expanded opportunities for hedge fund managers

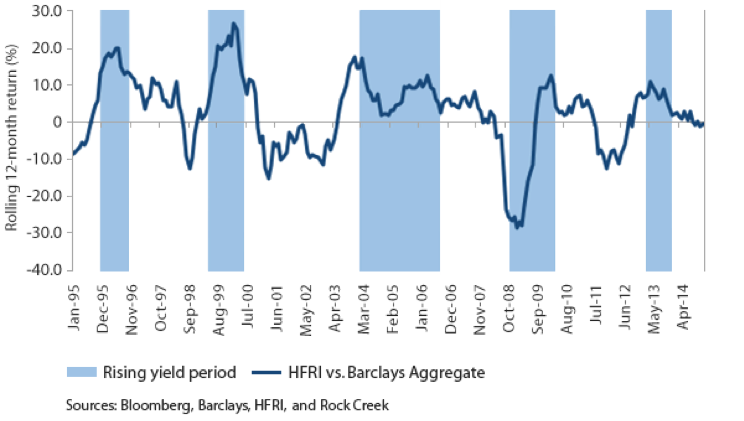

Additionally, the graph below shows rolling hedge fund returns versus the return of the alpha component in rising-yield periods.

Past performance is no guarantee of future results.

This analysis highlights that not only do hedge funds tend to perform well during and in the run-up to periods when the Fed tightens monetary policy but also that the investment opportunity set for skill-based, active hedge fund management expands during these periods. As markets are anticipating that the Fed will begin to introduce tightening measures in the second half of 2015, we believe vehicles that invest in hedge funds, such as liquid alternative mutual funds, are well positioned to take advantage of this environment and can provide a strong alternative to fixed-income investments now and in the upcoming years of monetary policy normalization.

|

Dr. Sudhir Krishnamurthi is a senior managing director at Rock Creek and has been with the firm since its inception in 2002. Dr. Krishnamurthi has been an industry leader in alternatives investing. Prior to joining Rock Creek, he served as director of the World Bank’s investment management department. |

|

Ronald van der Wouden is a managing director at Rock Creek and joined the firm in 2005. His primary focus is on portfolio and risk management and analytics. Prior to joining Rock Creek, he served as co-head of risk management at the World Bank Treasury. |

|

Ken LaPlace is also a managing director at Rock Creek and has been with the firm since 2003. His primary focus is on manager research. Prior to joining Rock Creek, Mr. LaPlace worked at Cambridge Associates. |

This website is accompanied by current prospectuses for Wells Fargo Advantage Funds®.

The fund does not invest directly in hedge funds but pursues similar strategies to those typically used by hedge funds. The fund invests using alternative investment strategies such as equity hedged, event driven, global macro, and relative value, which are speculative and entail a high degree of risk. Stock values fluctuate in response to the activities of individual companies and general market and economic conditions. Bond values fluctuate in response to the financial condition of individual issuers, general market and economic conditions, and changes in interest rates. Changes in market conditions and government policies may lead to periods of heightened volatility in the bond market and reduced liquidity for certain bonds held by the fund. In general, when interest rates rise, bond values fall and investors may lose principal value. Interest-rate changes and their impact on the fund and its share price can be sudden and unpredictable. Foreign investments are especially volatile and can rise or fall dramatically due to differences in the political and economic conditions of the host country. These risks are generally intensified in emerging markets. The use of derivatives may reduce returns and/or increase volatility. Borrowing money to purchase securities or cover short positions magnifies losses and incurs expenses. Short selling is generally considered speculative, has the potential for unlimited loss, and may involve leverage. Certain investment strategies tend to increase the total risk of an investment (relative to the broader market). This fund is exposed to high-yield securities risk, mortgage- and asset-backed securities risk, convertible securities risk, loan risk, and smaller-company securities risk. Consult a fund’s prospectus for additional information on these and other risks.

Please visit our blog, AdvantageVoice, for additional viewpoints from Wells Fargo Asset Management’s investment strategists, portfolio managers, and practice management experts. You can also follow us on Twitter at @WFAssetMgmt for real-time updates. Are you an advisor or institutional investor? Check out our website for investment professionals.

The views expressed are as of July 30 and are those of Dr. Sudhir Krishnamurthi, Ronald van der Wouden, and Kenneth LaPlace from The Rock Creek Group, LP (Rock Creek), and Wells Fargo Funds Management, LLC. The information and statistics in this report have been obtained from sources we believe to be reliable but are not guaranteed by us to be accurate or complete. Any and all earnings, projections, and estimates assume certain conditions and industry developments, which are subject to change. The opinions stated are those of the authors and are not intended to be used as investment advice. The views and any forward-looking statements are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally, or any mutual fund. Wells Fargo Funds Management, LLC, disclaims any obligation to publicly update or revise any views expressed or forward-looking statements.

Wells Fargo Funds Management, LLC, a wholly owned subsidiary of Wells Fargo & Company, provides investment advisory and administrative services for Wells Fargo Advantage Funds®. Other affiliates of Wells Fargo & Company provide subadvisory and other services for the funds. The funds are distributed by Wells Fargo Funds Distributor, LLC, Member FINRA, an affiliate of Wells Fargo & Company.

Not FDIC Insured • No Bank Guarantee • May Lose Value

© Wells Fargo Asset Management