Gold this week broke above its 50-day moving average as a fresh round of negative news from around the globe rekindled investors’ interest in the yellow metal as a safe haven. The Fear Trade, it seems, is in full force.

Below are just a few of the recent news items that have made some investors skittish, which has supported gold prices:

- China, the world’s second-largest economy, continues to slow. Its preliminary purchasing managers’ index (PMI) reading, released today, came in at 47.8, a 77-month low. This follows China’s decision last week to devalue its currency, the renminbi, close to 2 percent. For the first time in a year, the Shanghai Composite Index fell below its 200-day moving average.

- Crude oil has been on an eight-week losing streak, the longest in 29 years. West Texas Intermediate (WTI) slipped below $40 per barrel in intraday trading today, the first time it’s done so since 2009.

- U.S. stocks are undergoing an ugly selloff. They just had their worst week since September 2011 and are on track to post their worst month since May 2012. The Dow Jones Industrial Average, down 10 percent since its all-time high, is nearing correction territory. All 10 S&P 500 Index sectors were off this week.

We can also add to this list the high levels of margin lending on the New York Stock Exchange (NYSE) right now. At the end of every month, the exchange discloses margin amounts, and it appears that everyone is leveraged. Real margin debt growth since 1995 is twice as much as real S&P 500 growth.

Cartson Ringler is a market analyst and founder of Ringler Consulting and Research in Germany. Speaking with the Gold Report this week, he highlighted the precariousness of high margin debt in domestic equities:

We saw a huge bull market from 2009 to 2015 on the S&P 500 when it went to around 2,080 from 666. That market is really mature. One number that scares me is the high margin debt on NYSE. When the big market crash happened in 1987, we saw $38 billion in margin debt, but as of June 2015, NYSE margin debt was more than $504 billion. Everyone is dancing until the music stops. So I’m shorting the S&P 500, while building my basket of different precious metals producers.

Should the $504 billion—an all-time high, by the way—worry us, as Ringler suggests? Maybe, maybe not. It’s worth remembering, though, that high margin lending in China greatly contributed to the Shanghai Stock Exchange’s 30-percent correction just a month ago.

In its Friday newsletter, Kitco made note of many of these market-moving events and said that “optimism in gold should spill over next week. A strong majority among retail investors and market professionals expect to see higher prices the last full week of August.”

The Contrarian Case for Gold Is Scorching Hot

Earlier this month I shared with you that hedge funds are net short gold for the first time since U.S. Commodity Futures Trading Commission data began in 2006. Being short has become a very crowded trade, and many contrarian investors have seized upon this bearishness to add to their gold exposure. American Eagle gold coin sales rose an impressive 124 percent in July month-over-month.

This week, famed hedge fund manager Stanley Druckenmiller plunked down more than $323 million of his own money into a gold ETF, according to second-quarter regulatory filings.

Druckenmiller is the guy who consistently delivered 30 percent on an average annual basis between 1986 and 2010, the year he closed his fund to investors. He’s also responsible for making the call to short the British pound in 1992, which “broke the bank of England” because it forced the British government to devalue and withdraw the currency from the European Exchange Rate Mechanism (ERM).

And now he’s made a huge bet on gold. The $323-million investment, in fact, is the largest position in his family fund.

Demand among global central banks and retail buyers has also heated up. As I told Daniela Cambone in this week’s Gold Game Film, the Chinese government is now reporting monthly on its gold consumption to offer greater transparency and convince the International Monetary Fund (IMF) that the renminbi should be included as part of the special drawing rights. Last month, the Asian country purchased 54 million ounces. And in the first half of the year, demand in Germany, the third-largest gold market behind China and India, increased 50 percent over the same period in 2014.

Gold in Russian Ruble Terms Shows The Value of Hard Assets

The Russian ruble, meanwhile, has lost nearly 50 percent of its purchasing power from 12 months ago, following its invasion of Ukraine and the drop in oil prices. Over the same period, gold has risen about 54 percent.

It shows that when a currency loses value and falls out of favor, gold has tended to benefit as investors seek real assets. Gold prices have then been able to soar, just as we saw in the months following the financial crisis, eventually reaching an all-time high of $1,921 per ounce in September 2011.

Remember, Druckenmiller just invested heavily into gold. Prudent investors such as him understand the dynamic between fiat currencies and gold, and they adjust their funds accordingly. Does he predict something happening to the U.S. dollar that might benefit gold?

Druckenmiller might have 20 percent allocated to gold, but it’s advisable to have closer to 10 percent—5 percent in gold stocks, 5 percent in bullion, then rebalance every year. This should be strongly considered whether the economy is soaring or struggling.

I invite you to head over to Kitco and compare for yourself the price of gold in U.S. dollars to other world currencies.

Looking for Other “Safe Haven” Options in the Volatile Market?

Gold is indeed glimmering with safe haven appeal, but I encourage investors seeking an investment that has a history of less drama to check out municipal bonds.

Having provided investors with over 20 straight years of positive returns, NEARX holds five stars overall from Morningstar, among 185 Municipal National Short-Term funds as of 6/30/2015, based on risk-adjusted return.

Air Traffic Demand Continues Its Upward Ascent

On a final note, Jeffries released its latest air traffic demand growth numbers yesterday, and the results were very positive. According to the group:

The July Jefferies Air Traffic survey registered a 6.4-percent year-over-year growth rate for our sample. The IATA (International Aviation Transport Association) report for July could show traffic growth of about 8.5 percent, strong vs. 5.9 percent year-to-date. Financial market turmoil and weak commodity prices don’t appear to be hurting demand.

July demand is up from 4.8 percent in June, Jefferies also notes. The strong traffic results serve as further justification for the group’s year-end demand growth of 6 percent.

Index Summary

- The major market indices were hammered this week. The Dow Jones Industrial Average fell 5.82 percent. The S&P 500 Stock Index dropped 5.77 percent, while the Nasdaq Composite declined 6.78 percent. The Russell 2000 small capitalization index slid 4.61percent this week.

- The Hang Seng Composite tumbled 7.29 percent this week; while Taiwan fell 6.25 percent and the KOSPI dropped 5.41 percent.

- The 10-year Treasury bond yield fell 2 basis points to 2.04 percent.

Domestic Equity Market

Strengths

- Utilities was the best performing sector in the S&P 500 Index this week as escalating concerns of a global growth slowdown dragged down equities and government yields. The S&P Utilities Sector Index fell 1.19 percent this week.

- Housing starts and existing home sales for the month of July came in much stronger than expected. These two data points highlight that housing is still an area of relative strength in the U.S.

- Despite a selloff in many currencies this week, the dollar actually fell. The decline in the greenback is usually seen as a positive sign for global growth. The Trade Weighted Dollar Index fell 1.67 percent this week.

Weaknesses

- Energy was the worst performing sector in the S&P 500 Index this week as oil prices continue to collapse and global growth concerns take hold. The S&P 500 Energy Sector Index fell 8.64 percent this week.

- The global selloff in equities witnessed this week is particularly concerning for the more cyclical areas such as materials and industrials. The slowdown in the Chinese economy is the largest headwind in the global economy currently.

- The United States Empire Manufacturing Index contracted sharply for the month of August. The index came in at -14.92 compared to an expected gain of 4.5, signaling serious weakness and concern in the manufacturing sector.

Opportunities

- The Federal Open Market Committee (FOMC) minutes were more dovish than expected, which could mean rates will not rise until December, which would be positive for equities in the short term.

- The next preliminary second quarter GDP growth reading for the United States will be released next week and is expected to be much more positive than the first preliminary reading.

- The Conference Board Consumer Confidence Index is expected to rise to 93.4 for the month of August. A further increase in consumer confidence would be a tailwind for discretion and other consumer based industries.

Threats

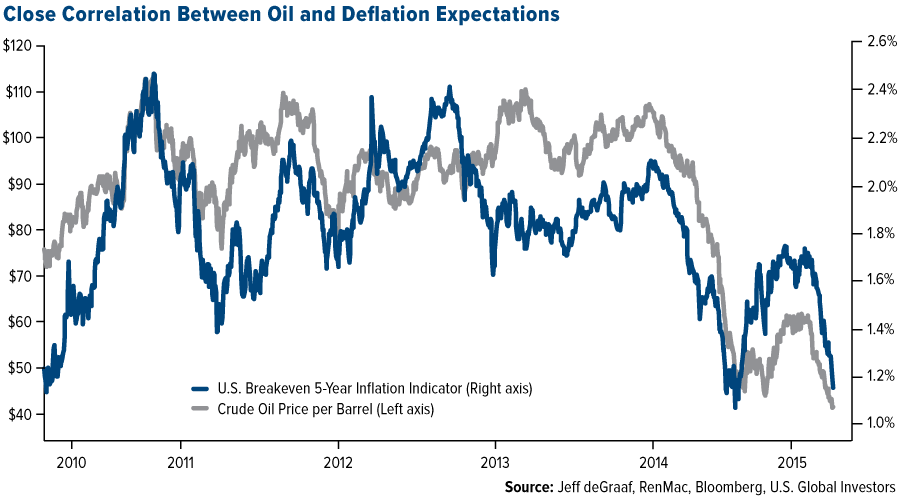

- Any rate hike this year may be too early given the recent changes in global economic sentiment. Inflation expectations are particularly weak, with the 5-year forward 5-year inflation breakeven rate in the United States falling below 2 percent for the first time in months. If the Fed jumps the gun, markets could unwind fast.

- The Markit U.S. Manufacturing Purchasing Managers’ Index (PMI) for month of August came in at 52.9 percent, declining from 53.8 percent in the prior month. This negative reading signals a potential slowdown in the manufacturing sector.

- The Conference Board’s Leading Index contracted by 0.2 percent for the month of July. A composite of various leading indicators, the Leading Index aims to anticipate changes in the real economy that have yet to come.

The Economy and Bond Market

Global markets were rattled by more bad news from China. Still reeling from last week's surprise action to devalue the renminbi, investors sold off stocks and bought “safe-haven” bonds and gold. The bearish mood was exacerbated Friday by the weakest reading from China's factory sector in six years. The VIX volatility index hit 24 intraday, a high not seen in 2015, and the S&P 500 Index fell into negative territory for the year to date. The yield on the 10-year U.S. Treasury note dropped to 2.04 percent, the lowest rate since April.

Accompanying the broad and steep selloff in equities were further drops in prices for commodities, including oil and copper. Asian emerging markets were among the hardest hit, feeling the fallout from China's currency weakness and declining demand for their exports. U.S. West Texas Intermediate crude oil fell to $40 per barrel, while Brent futures traded close to $45.

Strengths

- Housing starts picked up to 1.206 million seasonally adjusted annual rate (SAAR) in July, surpassing expectations of 1.18 million and reaching the fastest pace of building since October 2007. June was also revised up notably to 1.204 million from 1.174 million. Coupling this with increasing optimism among homebuilders, as evidenced by the NAHB housing index reaching a cyclical high of 61 in August, the uptrend for housing starts should continue.

- Existing home sales ramped up for a third consecutive month in July, rising 2.0 percent to 5.59 million SAAR. This was well above expectations for a pullback to 5.43 million, and is the strongest pace of sales since February 2007.

- Britain’s inflation rate unexpectedly rose in July and a core measure of price growth jumped to the highest in five months. The increase in the headline reading to 0.1 percent from zero was due to clothing prices, with smaller discounts in the summer sales this year compared with a year earlier. Economists in a Bloomberg survey had forecast the rate would stay at zero. The core measure increased to 1.2 percent from 0.8 percent, higher than the 0.9 percent reading predicted by economists.

Weaknesses

- Headline and core Consumer Price Index (CPI) both increased 0.1 percent month-over-month in July, coming in a touch below expectations of 0.2 percent. Should the recent fall in crude prices persist, it would suggest additional downside to headline inflation.

- The Empire manufacturing index collapsed to -14.9 in August from 3.9 in July, suggesting a notable contraction in manufacturing conditions during the month. This was a hugely disappointing print, as the market anticipated a slight improvement to 4.5. Additionally, this is the lowest reading for the index since April 2009.

- Japan's economy contracted at a 1.6 percent annualized rate in the second quarter, dragged down by weaker consumer spending and exports.

Opportunities

- U.S. second quarter GDP is released next Thursday. A confirmation of the expected 2 percent growth would likely add some stability to recent volatility.

- According to PIMCO, securities near the middle of the quality scale will probably be in a sweet spot when the Federal Reserve raises rates. The so-called “crossover bonds” perform better and are less correlated to U.S. Treasuries than are their investment-grade counterparts. This would provide an opportunity for bond investors that have the flexibility to cross the line between high-quality and junk-rated debt.

- Thanks to stronger sales growth and improving margins, European firms should continue to enjoy robust earnings growth.

Threats

- Goods-producing and globally-exposed firms will remain under pressure as their pricing power deflates. Leading indicators such as the ISM services vs. ISM manufacturing indexes have been favoring services producers, and additional U.S. dollar strength will reinforce these trends. Defensives and services companies have a substantial positive pricing power advantage over their cyclical and goods-producing counterparts and the meltdown in emerging market currencies will likely exacerbate that gap further.

- With the one-month in Durable Goods Orders trending below the three-months, a data disappointment in next Thursday’s reading could negatively affect equity sentiment.

- Given the focus on the trajectory of economic growth in the second half of the year, the Conference Board's index of leading economic indicators (LEI) series should receive heightened attention. This index is highly correlated with GDP growth over broad periods of time. If the LEI is entering a sustained deceleration, it would be a troubling omen for GDP. The LEI is now up 5.4 percent over year-ago levels, modestly below the pace in the first quarter (5.8 percent) and fourth quarter of 2014 (6.2 percent), though this is not sufficient in magnitude to imply a GDP slowdown. Nonetheless, the cooling trend in the LEI is hinting that the economy is only gradually improving relative to the first half.

![[thumb]](/images/content_image/data/ec/eca6a0525e2dfb8eaae4f9de56aad03d.jpg)

August 20, 2015Will the Fed Spark a Currency War? |

![[thumb]](/images/content_image/data/5b/5b13fa7c428334d4ab251da0c56a463c.jpg)

August 19, 2015Record Consumption of Gold Continues |

![[thumb]](/images/content_image/data/b4/b44915b1bf9180453ad2b6e81dae2cc8.jpg)

August 3, 2015Is Gold Still a Safe-Haven Asset? |

Gold Market

For the week, spot gold closed at $1,160.95 up $45.86 per ounce, or 4.11 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, gained 6.42 percent. The U.S. Trade-Weighted Dollar Index slid 1.57 percent for the week.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Aug -18 | U.S. Housing Starts | 1180K | 1206K | 1174K |

| Aug -19 | U.S. CPI YoY | 0.20% | 0.20% | 0.20% |

| Aug -20 | U.S. Initial Jobless Claims | 271K | 277K | 274K |

| Aug -20 | CH Caixin China PMI Mfg | 48.2 | 47.1 | 47.8 |

| Aug -25 | HK Exports YoY | -- | -- | -3.10% |

| Aug -25 | US New Home Sales | 510K | -- | 482K |

| Aug -25 | US Consumer Confidence Index | 93.4 | -- | 90.9 |

| Aug -26 | US Durable Goods Orders | -0.40% | -- | 3.40% |

| Aug -27 | US GDP Annualized QoQ | 3.20% | -- | 2.30% |

| Aug -27 | U.S. Initial Jobless Claims | 275K | -- | 277K |

| Aug -28 | GE CPI YoY | 0.10% | -- | 0.20% |

Strengths

- Gold Fields was the best-performing senior mining stock for the week, up 33.96 percent. CEO Nick Holland said investors are missing the quality of its foreign operations by focusing on delays and higher costs at its domestic projects. The company’s mines in Peru, Australia and Ghana helped raise headline earnings to $19 million in the second quarter, mending losses from the previous two quarters.

- Alamos Gold was the best-performing junior mining stock for the week, up 20.57 percent. The company recently reported positive second-quarter financial results and was upgraded by the Canadian Imperial Bank of Commerce (CIBC). We see the stock trading 5 percent above the fair value of its resource base.

- According to the latest SEC filings, Stanley Druckenmiller bought shares in a gold ETF worth $323.6 million at the end of June, making it the largest position in his family office fund.

- South African unions accepted the Chamber of Mines’ final gold pay offer, ending what has been a contentious rout of negotiations.

Weaknesses

- Eldorado Gold was the worst-performing senior mining stock for the week, down 12.67 percent. The company is battling to develop its Greek mines in the face of government opposition. Citing an “openly hostile” Greek Energy Ministry, the company said it would suspend most mining and development activities at its operations in northern Greece. It also said it would take legal action against the government’s decision to revoke its technical studies at the development projects.

- Rubicon Minerals Group was the worst-performing junior mining stock for the week, down 22.57 percent. The company’s update on its projects revealed some delays in the extraction of its first trial slope. This will likely cause a cash burn that could force the company to come back to the markets to raise money.

- In the past few months, a handful of mines have dropped under $1 per share, prompting notices from the New York Stock Exchange that they have six months to resume trading over $1 for at least a month or else they will be forced to delist. Companies affected have been McEwen Mining, Thompson Creek Metals and Silvercorp.

- Huaan Yifu Gold ETF, the bullion ETF with the biggest volume in China over the past month, posted a third straight weekly outflow. Outflows could be driving liquidity needs.

Opportunities

- According to Strategas, 30 percent of S&P 500 Index stocks have fallen to a 20-day low. Readings in excess of 50 percent would be more consistent with a washout. That means gold’s oversold rebound can continue. According to the King Report, if there is no stock market appreciation from the recent rout, the entire rationalization for financial repression will be destroyed. If a bear market for stocks develops during financial repression, the economic consequences should be dire. At that point, it would then be time to get long pitchforks and torches. Government leaders and Fed officials would be a short.

- China increased its gold reserves 1.1 percent in July as gold prices dropped 4 percent in July, according to data release from the central bank this week. This may suggest that China is selling some of its dollar reserves and rolling it into gold. If these monthly updates become a mainstay, it could provide momentum for the gold market.

- The release of the U.S. Consumer Confidence Index is expected to show an improvement from 90.9 to 93.4. Given the recently mixed economic data, a disappointment could lift gold prices.

Threats

- Barnabas Gan, the top-ranked precious metals forecaster, said the Fed will still raise interest rates this year, which will hurt gold.

- According to Citigroup, Venezuela appears poised for a near-term crisis amid protests and basic goods shortages as the country heads for parliamentary elections in December. As such, the central bank could be tempted to sell part of their gold reserves to raise funds.

- If next week’s release of second-quarter GDP comes in stronger than the expected 3.2 percent, it could raise the prospect of a September rate hike by the Federal Reserve and potentially depress the gold price.

Energy and Natural Resources Market

Strengths

- Gold equities led natural resources this week as Kazakhstan’s currency, the tenge, plunged by about a quarter on Thursday after the central bank stopped managing the exchange rate, prompting fears that a wider emerging market currency rout could be coming. The Philadelphia Gold & Silver Index gained 4.95 percent this week.

- The S&P 500 Utilities Index outperformed the S&P 500 Index by 4.57 percent this week on renewed fears over global deflation and falling government bond yields.

- On a relative basis, global coal stocks weathered the broader market downturn better than most natural resources industry groups, as selling pressure decelerated from an oversold condition.

Weaknesses

- Oil and gas royalty companies underperformed as dividends continue to be cut or suspended due to falling crude oil prices. The Yorkville Oil & Gas Royalty Index fell 10.88 percent this week.

- TSX listed energy stocks underperformed this week on a combination of a weakening Canadian dollar, declining market liquidity and a weaker commodity price. The TSX Capped Energy Index fell 10.00 percent during the week.

- Copper and other base metals stocks pulled back as investors continue to fear a slowdown in China’s growth. The S&P/TSX Capped Diversified Metals and Mining Index fell 10.41 percent this week.

Opportunities

- U.S. New Homes sales will be released next week and is expected to show further momentum building in housing market, which could be positive for timber and related wood product producers.

- China’s Conference Board of Leading Economic Indicators will be released next week which could provide more visibility regarding the country’s economic growth.

- U.S. President Barack Obama will speak at the eighth annual National Clean Energy Summit next week, kicking off a campaign to promote his climate agenda ahead of United Nations-sponsored negotiations in December.

Threats

- Concerns over China’s slowing growth rate remain high. Commodities and related stocks could remain volatile over the short-term.

- Crude oil fell below $40 a barrel in intraday trading on Friday, and could fall further given high inventories and resilient U.S. production that remains elevated despite a lower rig count and softer prices.

- The Fed has all but said for certain that it will raise rates this year, which threatens to boost the U.S. dollar higher and pressure commodity prices.

![[thumb]](/images/content_image/data/ac/ac3cca304ecf867576cbb9a256970ec1.jpg)

![[thumb]](/images/content_image/data/28/284ce58d96c517bc0f79e18df2c86b35.jpg)

![[thumb]](/images/content_image/data/64/64f75a83d3ceaf0b549ba10d2394f26a.jpg)

China Region

Strengths

- This week saw a global sell off in equities. With very few places to hide, gold and other “safe haven” assets were the relative outperformers as far as asset classes go. Regionally, every East Asian market closed down for the week.

- Telecommunication was the best performing sector in the region as investors flocked to lower beta and more defensive areas of the market.

- Singapore retail sales for the month of June came out last week and were particularly strong. Analysts expected year-over-year growth in retail sales to be 3.5 percent, but the actual growth was 6.9 percent.

Weaknesses

- Chinese equities fell sharply amid a global sell off in equities. The government’s unexpected devaluation of the yuan and consistently disappointing PMI readings are greatly weakening investor sentiment. The Shanghai Stock Exchange Composite Index fell 11.54 percent this week.

- Indonesian equities fell with the rest of global markets this week as the country’s exports contracted sharply in July from a year earlier. The Jakarta Stock Exchange Composite Index fell 5.44 percent this week.

- South Korean stocks underperformed this week alongside its regional peers. The Korea Stock Exchange KOSPI index fell 5.41 percent this week.

Opportunities

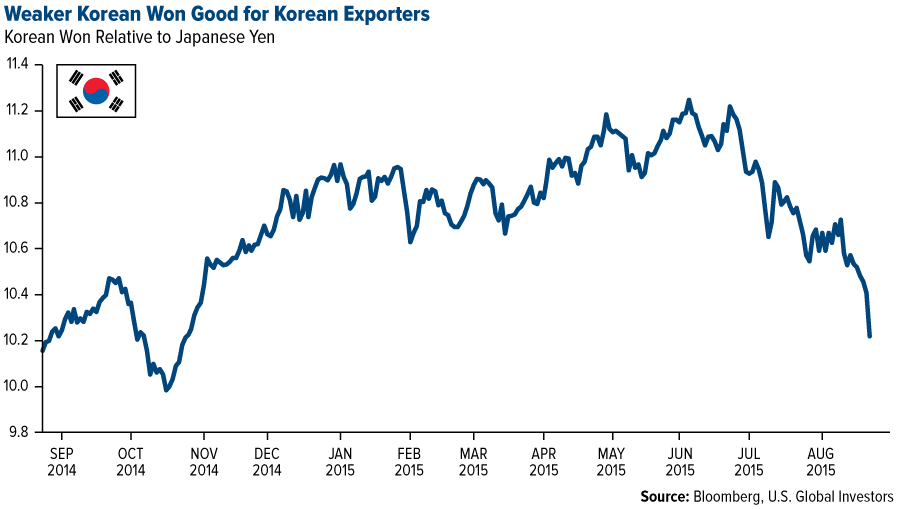

- Korean exporters should see increased competiveness from a weaker won relative to the Japanese Yen. The won has weakened significantly against the yen over the past few weeks after a prolonged period of yen depreciation due to Japan’s QE program.

- The Federal Open Market Committee (FOMC) minutes revealed a more dovish Fed than expected, meaning it may be more likely that rates rise in December rather than next month. Prolonging the inevitable rate rise is positive for emerging markets.

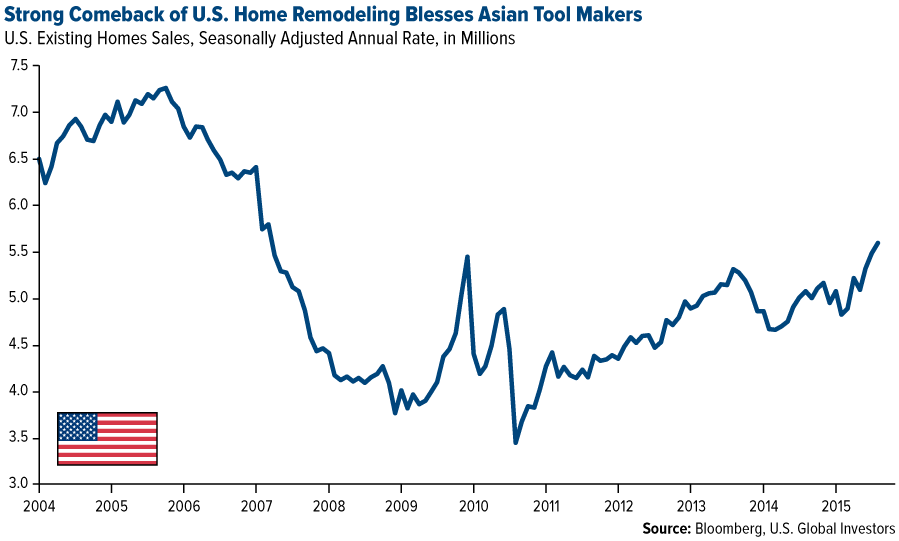

- Ongoing recovery in the U.S. housing market has pushed existing home sales to the highest since February 2007, which has manifested itself in the latest quarterly results of bellwether U.S. home improvement stores. Leading power tool exporters in Asia should continue to benefit from resurgent demand for remodeling homes for sale in the U.S., significantly lower raw material prices compared with a year ago, and favorable effect from recent Chinese devaluation due to U.S. dollar denominated revenue and renminbi denominated costs of production.

Threats

- Malaysia’s foreign exchange reserve fell below US$ 100 billion in July for the first time since August 2010. Slumping local currency, accelerating capital outflow, growing fiscal pressure, and, above all, a real threat of crude oil declining further make the net energy exporting country vulnerable for sustained underperformance within emerging Asia.

- Economists cut Japan’s growth forecast for the 12 months ending March 2016 once again. The lower forecast even further diverges from the Bank of Japan’s more optimistic forecast.

- Singapore’s industrial production growth for the month of July is expected to decline by 3.7 percent. While this is an improvement from the prior months reading, the contraction is still concerning.

Emerging Europe

Strengths

- Hungary was the strongest market this week, falling only 80 basis points. On the other hand, GDP growth for the second quarter was reported at 2.7 versus the prior reading of 3.5, and July PMI data was reported at 50 versus the prior reading at 55.4.

- The Czech koruna was the strongest currency this week, gaining 2.3 percent. Economic data coming out for Czech Republic continues to surprise to the upside. Second quarter GDP growth was reported at 4.4 percent versus the prior 4 percent. The PMI data for July was the strongest among emerging European countries at 57.5.

- In a down week, the utilities sector was the best performing sector.

Weaknesses

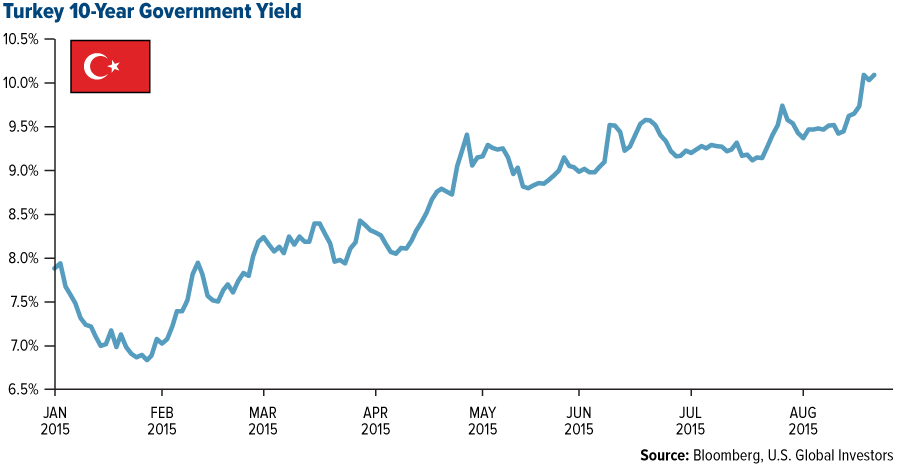

- Borsa Istanbul fell 4.5 percent this week and the Turkish lira weakened by 3 percent. Political crisis and reports of violence in Turkey weighted on equities and sent the lira to a record low. The yield on 10-year Turkish Government notes continues to move higher, highlighting the stress in the country’s markets.

- The Russian ruble lost 6 percent of its value this week, moving towards prior low levels that we saw at the end of January. Economic data coming out of Russia is weak. Real wages and retail sales declined by 9.2 percent, industrial production is down 4.7 percent and July PMI data fell to 48.3. Further weakness in Brent crude oil prices put pressure on Russia’s economy.

- The Industrial sector was the worst performing sector this week.

Opportunities

- Greece’s Prime Minister Alexis Tsipras resigned late Thursday after being in power for seven months. He accepted that he failed to bring the agreement that he wanted but he will continue to try to improve the Memorandum of Understanding (MoU). During his resignation speech, his comments were pro Europe and supporting the MoU. A new round of elections will take place probably on September 20 or 27.

- Eurozone Manufacturing PMI data for July came in strong at 52.4. Polish and Czech Republic PMI numbers remain strong as well. Turkey’s PMI data crossed above 50, signaling growth. Also, Consumer Confidence for the eurozone came in stronger than expected.

- Next week Economic Confidence data will be coming out for the eurozone area.

Threats

- Russia’s manufacturing PMI headed lower this week, signaling further signs of trouble for the struggling economy. Furthermore, Brent crude’s continued decline is creating serious headwinds for the country.

- Despite a more comforting dovish tone from the FOMC minutes released this week, the Fed will still most likely hike rates this year, which will negatively affect emerging markets.

- If there is no pickup in China’s economic growth and a restoration of investor confidence, global equities will continue to remain depressed.

(c) US Global Investors