Shifting expectations of whether the Federal Reserve (Fed) will or won’t hike interest rates may not be the only factor causing global volatility—just look at how China’s slow growth is roiling markets—but the rate debate is weighing on investors’ minds. However, we should ask ourselves, why the concern when it’s pretty clear the Fed won’t hike rates beyond a modest 0.25 percentage points? Why the concern when the Fed is only targeting the federal funds rate and not something more important, like the 30-year mortgage rate or the 10-year Treasury rate?

What’s causing concerns?

One key factor that’s sparking concerns is the notion that, in 2015, the Fed’s impending rate hike marks a policy shift that we haven’t seen since 2006. It used to be that increasing the federal funds rate required the Fed to drain bank reserves from the financial system, which limited credit. In today’s economy, with oodles of excess reserves, a rate hike’s potential effect on credit availability may be less damaging than in the past. This time, a higher federal funds rate will likely be accompanied by increases for other rates, such as interest on excess reserves and the Fed’s reverse repo rate.

These adjustments, in turn, could increase short-term interest rates, which is important for businesses and governments that raise money in short-term markets. Higher rates might be good for investors, but for issuers of those instruments, the higher rates come at a higher price.

How can we gauge the unknowns?

If the Fed raises rates—or if it doesn’t—investors want to know: How will other interest rates move? How will the dollar respond? How will the stock market react?

While most of these unknowns can only be answered after the fact, we may gain a glimpse of the Fed’s strategy, depending on how well it telegraphs its moves. Events that are widely anticipated by investors rarely move markets; unanticipated events and evolving anticipations, however, do move markets.

- Longer-term securities, such as stocks and bonds, will probably move based on the outlook for growth and inflation.

- If a Fed rate hike proves disruptive to the economy, then a hike should be expected to drive stock and bond prices lower.

- If a hike is perceived to make the economic expansion more sustainable while staving off a buildup in inflation, then a hike could be cheered by the markets.

I don’t think the market is pricing in the bulk of inflationary worries. The bigger concern is the U.S. growth outlook, which could push the majority of the Federal Open Market Committee’s voting members to wait on hiking rates. Ultimately, the only vote that really matters is Chair Yellen’s; since 1938, the chair has always been in the majority. Even if the September 17 meeting includes a dissenter or two, they won’t change the outcome of the meeting.

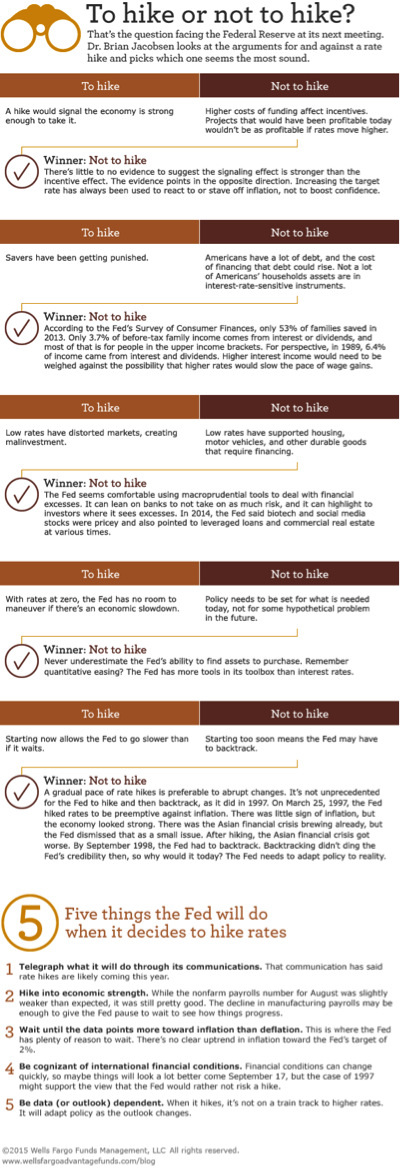

Should the Fed hike rates? Two sides to the story.

There are two sides to most arguments, so I created an infographic to compare the arguments for and against hiking rates and then highlighting the case I think is most sound.

We’ve heard most of these arguments before, when the Fed hiked rates in the past. I think the strongest argument for hiking is that starting sooner allows the Fed to go slower. However, in the grand scheme of things, monetary policy operates on the economy through long and variable lags. So there’s probably little reason to worry about whether the Fed hikes in September or October—and certainly not over 25 basis points.

Please visit our blog, AdvantageVoice, for additional viewpoints from Wells Fargo Asset Management’s investment strategists, portfolio managers, and practice management experts. You can also follow us on Twitter at @WFAssetMgmt for real-time updates. Are you an advisor or institutional investor? Check out our website for investment professionals.

The views expressed are as of 9-9-15 and are those of Dr. Brian Jacobsen, CFA, CFP®, and Wells Fargo Funds Management, LLC. The information and statistics in this report have been obtained from sources we believe to be reliable but are not guaranteed by us to be accurate or complete. Any and all earnings, projections, and estimates assume certain conditions and industry developments, which are subject to change. The opinions stated are those of the authors and are not intended to be used as investment advice. The views and any forward-looking statements are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally, or any mutual fund. Wells Fargo Funds Management, LLC, disclaims any obligation to publicly update or revise any views expressed or forward-looking statements.

Wells Fargo Funds Management, LLC, a wholly owned subsidiary of Wells Fargo & Company, provides investment advisory and administrative services for Wells Fargo Advantage Funds®. Other affiliates of Wells Fargo & Company provide subadvisory and other services for the funds. The funds are distributed by Wells Fargo Funds Distributor, LLC, Member FINRA, an affiliate of Wells Fargo & Company.

Not FDIC Insured • No Bank Guarantee • May Lose Value

© Wells Fargo Asset Management