Today is an emotional day for Americans. In an instant, on a beautiful blue sky morning 14 years ago, all of our lives changed forever.

September 11 is a day when we pause and reflect on where we were when—when the towers came crumbling down, when our nation’s capital came under attack, when so many lives were cut short, when so many heroes rushed in.

I was in Manhattan with colleagues that day, attending a financial industry conference uptown. At the time, we didn’t know how fortunate we were that our meeting had been changed from 9:00 a.m. to 11:00 a.m. I was en route when everything stopped, and soon after, I saw all the people covered in dust and walking home across the bridge. The cell phones in the city stopped working, but because mine had a San Antonio area code, I was able to get through to the office to let everyone know we were safe.

|

I was there with two of my company executives and the magnificent Nancy Holmes (no relation, though she often joked that I was her adopted son), who was working with me as a marketing strategist, at the age of 82. Nancy led one of the most interesting and full lives I have ever known. A code clerk for the U.S. Army, a model in Paris for Balmain, a photojournalist for Columbia Pictures, a bestselling author and magazine editor, including editor-at-large for Worth magazine, which she retired from to move to San Antonio and spend time with her granddaughters and be a consultant to U.S. Global. In fact, she was larger than life and filled with enthusiasm for life. She was a fellow traveler of the world, but like the rest of us, in that dark hour we all just wanted to go home, to Texas.

The city was shut down that night. The cabs disappeared and the subways weren’t running. The airports would remain closed for many days.

But the next morning I found a driver to take us to New Jersey where I had reserved one of the last rental cars left in the area. The four of us loaded into a Ford Expedition and began the long ride home and an unforgettable bonding experience. My adrenaline rush enabled me to drive us straight through for 30 hours. Early on we turned off the car radio because the nonstop coverage of the tragedy was too much to take. Instead, Nancy entertained us with stories of her incredible trail blazing life including her close friendships with the rich and famous, from Joan Collins and Elizabeth Taylor to Sean Connery and former hedge fund manager Julian Robertson. Nancy was a bright light on that dark day.

For the last 14 years on this day, I remember all the people who didn’t get to return home that fateful day, and I give thanks that I did, along with these special colleagues and friends.

I find myself back in New York, an unplanned diversion when my flight out of Portland, Maine was cancelled. And once again, I’m trying to get home. Rain has grounded the midsize regional plane I was scheduled to take, an effective reminder that no matter how well you think you’re in control, uncertainty has a habit of stepping in the way.

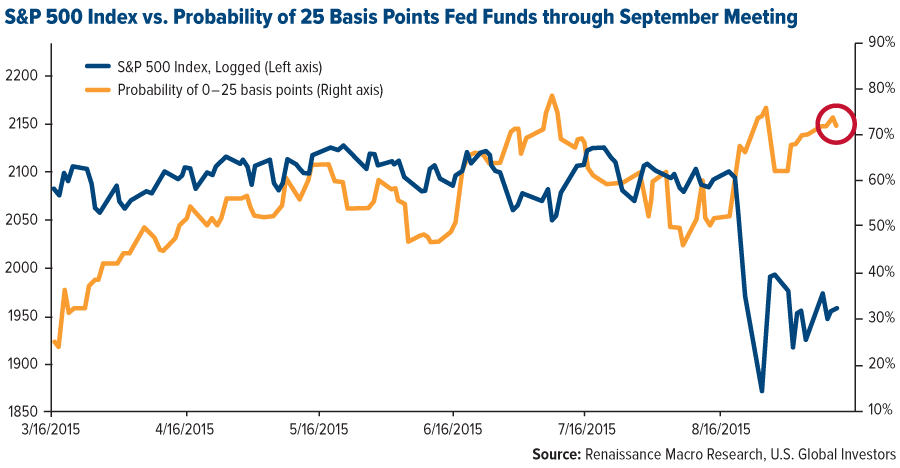

Will They or Won't They?

Right now, a lot of investors are wondering about the uncertainty of rising interest rates—the causes, effects and possible ramifications. Many people have been saying for weeks and months now that a rate hike is imminent and that September is the anticipated takeoff.

I’ve been skeptical of this, and now a chart from highly-respected market analyst Jeff deGraaf confirms my skepticism. In his words, “the market anticipates >70 percent probability of the Fed NOT raising rates.”

The Fed will convene next Thursday, and according to deGraaf, the most bullish outcome would be if Chair Janet Yellen held off raising rates and also took a more dovish tone. A more bearish outcome would be if she announced a rate hike and assumed a hawkish tone. I could see a rate hike fast-tracking QE4.

Low Energy Prices Offer Companies Delayed Gratification

Speaking of the S&P 500, many investors might worry that falling energy stocks are creating havoc for the index. In reality, the S&P isn’t affected by a drop in energy as much as some believe. Currently, energy is only 7 percent of the index, and its position is dropping. As recently as December 2014, it was 9 percent.

Part of the reason it’s falling is because the market cap for energy stocks has collectively declined 32 percent for the 12-month period. Do the math. The point is that, as the fourth-smallest sector in the S&P following telecommunications services (2.4 percent), materials (2.9 percent) and utilities (3 percent), energy has a minimal impact on the overall index.

Everyone knows that when energy prices drop, oil specifically, companies within the sector are hurt, including producers, refiners and the like. The winners are consumers, who save at the pump and benefit when companies pass along energy savings.

What many people might not know, however, is that it often takes a few quarters before these benefits are realized. Take the airline industry. Domestic carriers reported their first-ever $5-billion quarter in July, which is exactly a year after oil prices started to plummet from more than $90 per barrel.

The longer fuel prices stay low, the more likely it is that airlines will continue to perform beyond expectations. Irish low-cost carrier Ryanair, for instance, recently hit a 52-week high. If prices were to plunge to $20 per barrel, as Goldman Sachs claim is a possibility, the savings would be even larger.

However, with a growing global population over seven billion people, it will not be longer before the oil supply at these prices eases and prices rise to the $60-per-barrel level. This will have many benefits for both consumers as well as the energy space.

As always, investors should consider their tolerance level based on risk and age to help balance their investments between short-term bonds and equities.

Manufacturing and the Velocity of Money

Here’s a final thought I want to leave you with. According to new data released by the Bureau of Labor Statistics, government employees outnumber workers in the manufacturing sector 1.8 to 1—nearly double. What if it were the other way around? The economy would likely be stronger and more vibrant, as I see it.

Think of home construction. When a house is built, money touches so many people, from surveyors to architects, from plumbers to landscapers, from lawyers to accountants. All of these people are creating wealth for themselves and for others. For every dollar invested, housing returns between $12 and $14.

That’s not the case with government workers, for whom taxes must be raised to pay for their wellbeing. Don’t get me wrong. We need such people to run the government. But the ratio between the two types of workers is out-of-balance for a vibrant economy.

It’s classic macroeconomics on money supply growth and velocity. Different industries and sectors have different values for each dollar spent. The private sector is higher than the public sector, and housing is highest.

I wish all of my readers, shareholders and investors a safe and happy weekend! To my Jewish friends, L'shanah tovah! For a good year!

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 2.05 percent. The S&P 500 Stock Index rose 2.07 percent, while the Nasdaq Composite climbed 2.96 percent. The Russell 2000 small capitalization index gained 1.90 percent this week.

- The Hang Seng Composite gained 3.91 percent this week; while Taiwan was up 3.81 percent and the KOSPI rose 2.93 percent.

- The 10-year Treasury bond yield rose 6 basis points to 2.19 percent.

Domestic Equity Market

Strengths

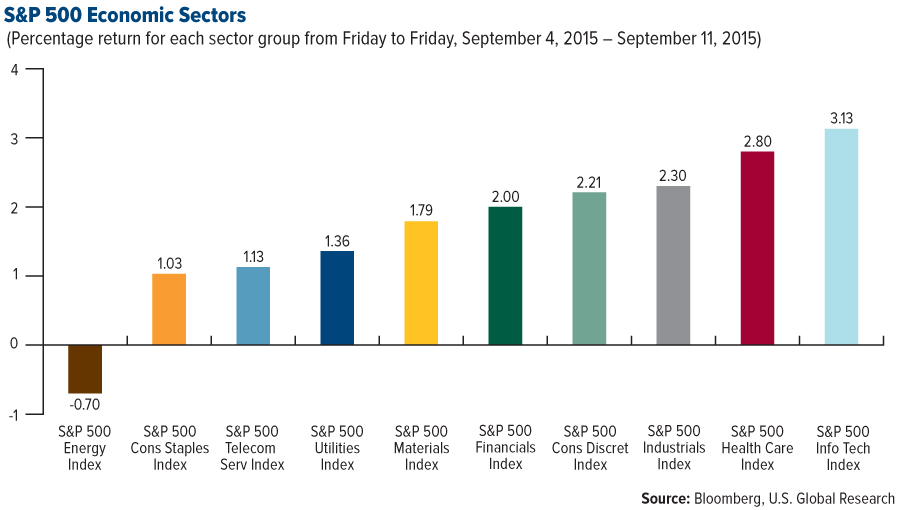

- Information technology was the best performing sector in the S&P 500 this week following its sharp sell off the week prior. The S&P Information Technology Sector Index rose 3.13 percent this week.

- The preliminary reading for eurozone productivity growth during the second quarter surprised to the upside this week. Gross domestic product for the eurozone grew 1.5 percent in the second quarter from the same period one year ago. Analysts estimated a slightly lower growth rate of 1.2 percent.

- Small business sentiment improved for the month of August. The NFIB Small Business Optimism Index rose to 95.9 from 95.4 in July.

Weaknesses

- Energy was the worst performing sector in the S&P 500 this week as WTI crude prices remain severely depressed. The S&P 500 Energy Sector Index fell 0.70 percent this week.

- Inflation expectations remain considerably depressed, hovering at levels not seen since late last year. Investor confidence in the underlying economy is shaky.

- Yields on 10-year U.S. Government notes rose roughly 6 basis points this week, placing more competitive pressure on other income plays.

Opportunities

- Consumer credit grew by $19.1 billion in July, surpassing analysts’ estimates. Further borrowing should benefit consumer oriented stocks.

- The Conference Board’s Leading Index, a composite of various leading economic indicators, is forecasted to rise 0.2 percent for the month of August, implying improvement in the economy in the near future.

- Certain big name investors are commenting on the attractive valuations within various industries, particularly energy.

Threats

- The Federal Open Market Committee (FOMC) will release its updated target for the federal funds rate next Thursday. The long awaited announcement is sure to have a meaningful impact on markets. Given that economists are forecasting an incremental increase of 25 basis points, markets could be caught off guard as futures contracts still imply a low probability of a rate hike.

- Consumer sentiment contracted sharply for the month of September according to a preliminary reading released this week. The University of Michigan Consumer Sentiment Index fell to 85.7 from 91.9, the lowest level in a year.

- Housing starts during the month of August are forecasted to fall, which could put pressure on the housing and construction industries.

The Economy and Bond Market

Major global equity market indices were volatile, but gained for the week even as investors remained nervous about China's slowing economy ahead of a much-anticipated U.S. Federal Reserve policy meeting next week. The VIX index traded in a fairly tight band of 23–27, indicating slightly less U.S. stock market turbulence than in prior weeks. The yield on the 10-year U.S. Treasury note varied between 2.13 percent and 2.24 percent, ending the week in the middle of that range. U.S. West Texas Intermediate crude oil futures hovered under $46 per barrel this week, while Brent crude oil fell below $48 per barrel and gold dipped below $1,100 an ounce Friday, near its low for the year.

Strengths

- Consumer credit expanded by $19.1 billion in July, though this was a slowdown from the $27 billion increase in June. This was a touch higher than expectations of $18.8 billion. The gain this month was once again driven by nonrevolving debt, which grew by $14.8 billion to $2.54 trillion. Revolving debt went up by a smaller $4.3 billion, increasing total outstanding to $0.91trillion. Consumer credit should continue to expand amid a strong labor market and U.S. economy.

- The Census Bureau released the Q2 Quarterly Services Survey this week, revealing a stronger trend for healthcare services spending.

- The NFIB small business sentiment index inched up to 95.9 in August from 95.4. This was right in line with expectations of 96.0, which is also the 6-month average.

Weaknesses

- The University of Michigan Sentiment index fell to 85.7 in the preliminary report for September from 91.9 in the final report for August. This is below the expected weakening to 91.1 and represents the lowest reading since last September. The current conditions index slipped to 100.3 from 105.1 in the prior month, and the expectations index fell to 76.4 from 83.4. The drop in sentiment likely reflects the turmoil in the financial market, which is offsetting the boost from lower gasoline prices and job growth.

- Import prices were weaker than expected in August, falling 1.8 percent month-over-month versus expectations of -1.6 percent. Even controlling for petroleum, import prices ex-petroleum declined 0.4 percent. Consumer import prices declined 0.1 percent month-over-month, remaining weak and pushing the year-over-year rate down a tenth to -1.3 percent. These data suggest continued disinflationary pressure feeding into measures of underlying consumer price index (CPI) and personal consumption expenditures (PCE) inflation.

- Job openings surged to 5.75 million in July from 5.32 million in June, coming in well above expectations of 5.3 million. As a result, the job openings rate jumped to 3.9 percent from 3.6 percent. Businesses are increasingly in need of labor, and there is evidence of skill mismatch in the Job Openings and Labor Turnover Survey (JOLTS) data. Indeed, the increase in the job openings rate now puts it above the hire rate (which fell to 3.5 percent from 3.7 percent) for the first time since the data goes back to December 2000. Firms want to hire workers, but they are having trouble finding suitable employees.

Opportunities

- Retail sales, released Tuesday, have been volatile in the last couple of months but have remained in positive territory. Next week’s print is likely to show a continuation in the tepid growth pace.

- The National Association of Home Builders (NAHB) survey will be released Wednesday. With the 1-month trend above the 3-month, results are likely to show continued progress in the housing recovery.

- Capacity utilization, released on Tuesday, is likely to continue its upward trend and carries positive momentum given the 1-month is above the 3-month trend.

Threats

- While direct links with China and many developing countries may be small, these countries represent the marginal price setters for tradeable goods. As such, plunging emerging market currencies are importing deflation into the U.S. Nearly half of U.S. industry groups are suffering a contraction in selling prices, with two thirds unable to raise selling prices by more than 1 percent. Half of the ten broad sectors are in deflation. This is highly relevant for equity investors, because it warns that falling sales growth is likely to persist. Without sales growth, profits can only grow if margins expand through cost cutting. That is unlikely given that labor costs are now rising, however modestly. Thus, expectations for resumption in profit growth starting in the fourth quarter of this year and continuing throughout 2016 at a double-digit pace are far too optimistic. If this persists, the likely outcome is that equities will continue to adjust downward toward a valuation level that better reflects meager profit growth prospects.

- The odds of a Fed liftoff have fallen, but a rate hike is not completely off the table. The new set of dots and economic forecast, as well as Yellen's press conference will show how much the market turbulence has affected the Fed's plans.

- CPI will be released Wednesday. The 1-month trend remains below the 3-month, pointing to a likely disappointing print that reflects an economy continuing to struggle with increasing the inflation rate.

Gold Market

For the week, spot gold closed at $1,107.78 down $15.67 per ounce, or 1.39 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, lost 1.49 percent. The U.S. Trade-Weighted Dollar Index backed off 1.09 percent for the week. Junior tiered stocks outperformed seniors for the week as the S&P/TSX Venture Index was off just 0.98 percent outpacing the GDM Index. Most people expect the Fed to not raise interest rates at next week’s FOMC meeting; however there will still likely be plenty of vocal gold bears eager to encourage you to sell your gold to them to cover their shorts.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Sep -10 | US Initial Jobless Claims | 275K | 275K | 282K |

| Sep -11 | GE CPI YoY | 0.20% | 0.20% | 0.20% |

| Sep -11 | US PPI Final Demand YoY | -0.90% | -0.80% | -0.80% |

| Sep -13 | CH Retail Sales YoY | 10.60% | -- | 10.50% |

| Sep -15 | GE ZEW Survey Current Situation | 64 | -- | 65.7 |

| Sep -15 | GE ZEW Survey Expectations | 18.3 | -- | 25 |

| Sep -16 | EC CPI Core YoY | 1.00% | -- | 1.00% |

| Sep -16 | US CPI YoY | 0.20% | -- | 0.20% |

| Sep -17 | US Housing Starts | 1170K | -- | 1206K |

| Sep -17 | US Initial Jobless Claims | 276K | -- | 275K |

| Sep -17 | US FOMC Rate Decision (Upper Bound) | 0.50% | -- | 0.25% |

Strengths

- Palladium was the best performing precious metal for the week, up 4.08 percent. According to Goldman Sachs, 70 percent of global palladium demand originates from catalytic convertors found in gasoline dependent motor vehicles. Auto demand has been more than robust, averaging growth of over 5 percent year-over-year y in the last 12 months. Further, 79 percent of global palladium mine supply comes from Russia and South Africa. The strength of the U.S. dollar versus both the Russian ruble and the South African rand over the past 12 months has acted as an effective tailwind for producers in both countries as operating costs have shifted down. Silver outperformed gold for the week. Sales of silver coins at the U.K. Royal Mint have tripled from April to August, compared with a year ago.

- Foreign exchange figures released Monday suggest China added around 16 million tons of gold in August, according to UBS. Gold watchers will be paying attention to see if China continues its recent trend of publishing its gold accumulation on a monthly basis.

- The demand for imported gold in China seems to be improving, based on higher premiums paid for the metal.

Weaknesses

- Platinum was the weakest precious metal for the week, down 2.12 percent. Platinum group metals (PGM) production data released by South Africa, showed a 72 percent output rise year-over-year, perhaps explaining why the PGMs have underperformed gold over the past year.

- Consumer sentiment declined in September to the lowest level in a year as Americans anticipated a weaker economy in the face of a global slowdown and turbulent financial markets. HSBC expects the FOMC to forego a rate hike next week. If that is the case, gold will remain subdued, in expectation of the eventual hike.

- Two straight years of drought in India have hit gold demand and could cut imports by up to 10 percent in 2015, according to the head of the All India Gems and Jewellery Trade Federation. Further, Indian gold premiums are negative which shows little demand for imported gold.

Opportunities

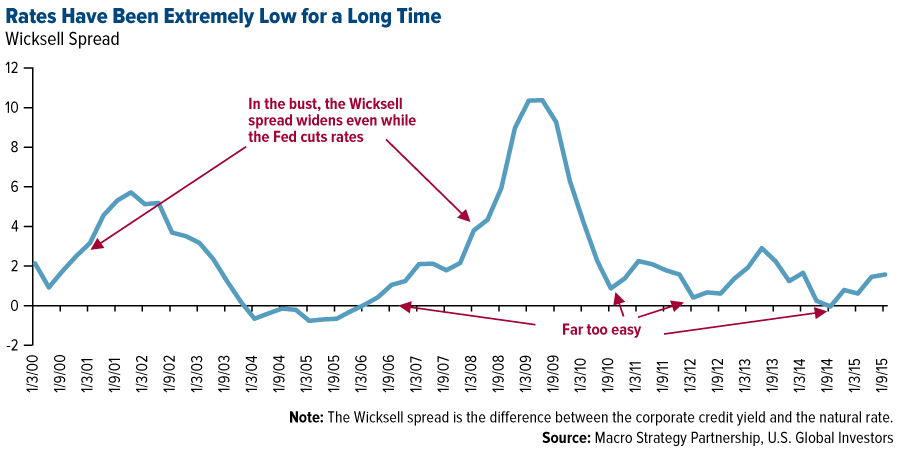

- The Wicksell spread, which shows the difference between the corporate credit yield and the “natural interest rate,” shows that rates have been too low for a very long time. It focuses on the key drivers of the business cycle; what is happening to the cost of capital versus what is happening to the return on capital. As such, if returns fall below the market rate for credit, boom turns to bust. That is exactly where we seem to find ourselves currently according to research by Julien Garran of Macro Strategy Partnership. Furthermore, billionaire investor David Tepper said this week that he sees problems with earnings growth, valuations, and people having too high expectations for earnings in 2016. Thus, he said he would be a buyer of equities if the market fell 20 percent. Mr. Garran suggests today investors should be long gold and short U.S. stocks.

- Copper had its longest rally since June on speculation that output cuts by miners will tighten supplies just as demand rebounds. Technically, the move in copper has broken through its overhead resistance and copper producers have started to rally.

- Macquarie initiated coverage of St. Barbara Limited with an outperform rating and a target price of $1.00/share. According to them, the company has found a new direction after a change of senior management and strong performance from its key asset at Gwalia. This has been complemented by a strong turnaround at Simberi and the divestment of Gold Ridge is putting the company in a position where it can deleverage and re-examine expansion options.

Threats

- According to Nomura, India’s sovereign gold bond scheme is more likely to succeed. Their annual investment demand for gold is estimated at 300 MT per annum, which is around 35 percent of India’s gold import bill. Furthermore, the government is likely to offer 2-3 percent interest rates for the two gold schemes it announced on Wednesday according to a senior government official.

- According to past government gold monetization schemes in India, there are reasons to believe the current one will fail. As part of the 1993 scheme, the government managed to mobilize a little over 41 tons because the scheme offered immunity to investors from being asked questions as to how this gold was acquired and the source of funds. The current plan contains no such protections and thus, the potential oversight and investigations could cause investors to be much more wary in taking part.

- ABN Amro, the biggest Dutch bank, cut its forecast for gold prices and now expects them to fall to $1,000 by the end of the year and to $800 by 2016 on expectations the Fed will cut interest rates. Keep in mind this is the same ABN Amro that defaulted on physical delivery of gold to their customers in 2013 because they did not have any physical gold to deliver.

Energy and Natural Resources Market

Strengths

- Base metals stocks rallied again this week as investors became more constructive towards China’s economic growth outlook. The S&P/TSX Capped Diversified Metals and Mining Index gained 10.2 percent this week.

- The Bloomberg Dry Ships Index gained nearly 6 percent on the week as iron ore prices recovered in response to declining inventories following a period of destocking in China.

- Oil refining stocks led the energy complex this week on falling crude prices and strong gasoline demand. The S&P 500 Oil Refining & Marketing Index gained 4.9 percent on the week.

Weaknesses

- The threat of an impending interest rate hike by the Fed next week weighed on income related equities in the oil patch. The Alerian MLP and Yorkville Oil & Gas Royalty indices fell 2.8 and 4.9 percent, respectively.

- Forecasts for lower crude oil prices next year due to resilient production and abundant inventories weighed on oil service and equipment stocks this week. The Philadelphia Oil Service & Equipment index fell 2.3 percent during the week.

- The Bloomberg Oil Tanker Index fell 1.6 percent this week on news of further VLCC new-build orders and deliveries into the market later this year.

Opportunities

- Industrial Production and Fixed Asset Investment in China are scheduled to be released next week, with expected growth forecasts of 6.5 and 11.2 percent, respectively.

- Lower oil prices will force non-OPEC producers including the United States to cut output by the steepest rate in more than two decades next year, rebalancing an oversupplied oil market, the International Energy Agency (IEA) said. The IEA said it now expects U.S. light, tight oil production to shrink by 0.4 million barrels per day (bpd) next year after expanding by a record 1.7 million bpd in 2014.

- The World Nuclear Association Nuclear Fuel reported that global nuclear capacity will grow to 552 gigawatts equivalent (GWe) in 2035 from 379 GWe currently. Still, the IEA states this will fall short of its threshold figure of 900 GWe in capacity (by 2050) needed to avoid the worst effects of climate change. In order to reach its estimate, the IEA believes $81 billion a year in nuclear plant investments would be needed throughout that time frame.

Threats

- According to Goldman Sachs, the world’s oil glut may be bigger than originally thought even as U.S. shale production is expected to decline next year, which could push crude oil to $20 a barrel in order to rebalance global supply.

- Concerns over China’s slowing growth rate remain high. Commodities and related stocks could remain volatile over the short-term.

- A Federal Reserve rate hike next week could prove to be a policy mistake given already unstable global equity markets and tenuous economic growth domestically and abroad.

![[thumb]](/images/content_image/data/60/607c097dbde7af4aa7716e23f3767bd5.jpg)

September 10, 20158 Iconic American Companies that Have Been Hurt by the Strong Dollar |

![[thumb]](/images/content_image/data/7d/7d7b54dd88e8b757c1c91f8efbd136cf.jpg)

September 8, 2015What the Influencers Are Saying about Commodities |

![[thumb]](/images/content_image/data/ac/acd9db58cc70ef9df1d5e1726beaa9c8.jpg)

September 2, 2015The Many Uses of Gold |

China Region

Strengths

- Taiwanese equities rose sharply this week despite the release of disappointing economic data. However, renewed commitment from China to supporting economic growth lifted the region. The Taiwan Stock Exchange Weighted Index rose 3.81 percent this week.

- Hong Kong stocks rallied this week after suffering sharp sell offs the week prior. The Hong Seng Composite Index rose 3.91 percent this week.

- South Korean stocks participated in the bounce as well as the unemployment rate fell more than expected. The Korea Stock Exchange KOSPI Index rose 2.93 percent this week.

Weaknesses

- Philippine stocks underperformed this week in anticipation of the FOMC decision next week. The Philippines Stock Exchange PSEi Index fell 1.99 percent this week.

- Taiwan export growth year-over-year for the month of August contracted by more than expected.

- Japanese machine orders growth year- over-year for the month of July was much weaker than expected, adding some negative sentiment to the positive GDP release this week.

Opportunities

- Holding higher than normal cash should continue to help weather short-term market volatility ahead of next week’s Federal Reserve interest rate decision. Cautious fund positioning is prudent, given little evidence of a positive reversal from China’s August macro data and lack of convincing government policy stimulus. It is very difficult to foresee a sustainable turnaround in investor sentiment when the Chinese A Share market has yet to see a real capitulation because local retail investors, who dominate daily trading activity, have just turned net sellers in August after ten consecutive months of net accumulation.

- China industrial production growth for the month of July is expected to be revised up to 6.5 percent from 6.0 percent.

- China has committed to providing more government funds in the wake of recent market and economic turmoil. Such support could be the deciding factor in China’s growth trajectory.

Threats

- Negative news headlines regarding thievery of hundreds of millions of dollars from a Macau junket as well as lingering concerns over a complete smoking ban inside the city’s casinos do not alleviate the uncertainty of the gambling industry’s secular appeal. Subdued visibility of industry growth, less than attractive valuation, and dearth of sustainable catalysts may continue to weight on investor sentiment towards Macau casino stocks.

- Singapore export growth for the month of August is expected to contract 3.3 percent, which would weigh on companies with a high degree of foreign sales.

- The FOMC will release its upper limit target for the federal funds rate next week. With economists expecting a slight increase and markets still unconvinced, a sell off could ensue.

Emerging Europe

Strengths

- Greek stocks rallied sharply this week, continuing their oversold bounce. Investor optimism over the political environment in Greece is also improving. The Athens Stock Exchange General Index rose 4.21 percent this week.

- Russian equities rose this week despite the decline in Brent crude prices. The central bank did leave rates unchanged, which dismissed investors’ fears that the bank would need to raise rates to defend the ruble.

- The Czech economy appears to be on fire, especially relative to its peers in the emerging European region, and indeed the broader emerging market universe. Industrial production and GDP growth continue to remain in a steady uptrend. The outperformance of the Czech economy could be partly attributed to the monetary policy of the Czech Central Bank, which continued to cut rates while its peers chose to raise rates.

Weaknesses

- Turkish equities and the currency continue to fall as investor concerns over terrorist activity in the country increase. Furthermore, the Turkish economy is struggling as industrial production growth for the month of July was much weaker than expected. The Borsa Istanbul 100 Index and the Turkish lira declined 2.19 and 1.17 percent, respectively.

- Hungary’s industrial production growth contracted between June and July, highlighting weakness in the underlying economy. The Budapest Stock Exchange Index fell 1.18 percent this week.

- Disinflation is reemerging in the region as both Czech and Hungary reported weaker growth in consumer prices from a year earlier.

Opportunities

- The Russian Central Bank’s decision to leave rates unchanged highlights its comfortability with the Ruble’s depreciation, which could be a sign that the bank thinks the decline is over.

- Polish industrial production growth from a year earlier is expected to rise to 6.3 percent from 3.8 percent.

- European exporters should continue to see benefits from weaker currencies if the dollar rises as a result of the FOMC decision next week.

Threats

- Polish consumer prices are expected to have contracted by 0.7 percent from a year earlier, signaling deflation and weak growth.

- Should the FOMC raise interest rates next week, the most susceptible country is Turkey, which relies heavily on foreign capital inflows to finance its trade deficit.

- China continues to remain a serious concern for all emerging markets. Investors remain pessimistic.

(c) US Global Investors