Next week’s meeting of the Federal Open Market Committee (FOMC) is one of the more highly anticipated central bank sessions in years. A couple of months ago, the policy decision that will emerge next Thursday afternoon seemed clear. But international events through the summer have clouded the picture considerably.

At the outset, we would stress that the emphasis observers are placing on this particular meeting seems a little excessive. Whether or not the Fed raises rates this month, it is likely to proceed upward very slowly and cautiously. That matters more to long-term investors than the date of “liftoff.”

Nonetheless, a decision to move interest rates upward after nearly seven years at the zero lower bound is not one to be taken lightly. Here is our take on the pros and cons that might arise in Washington next week.

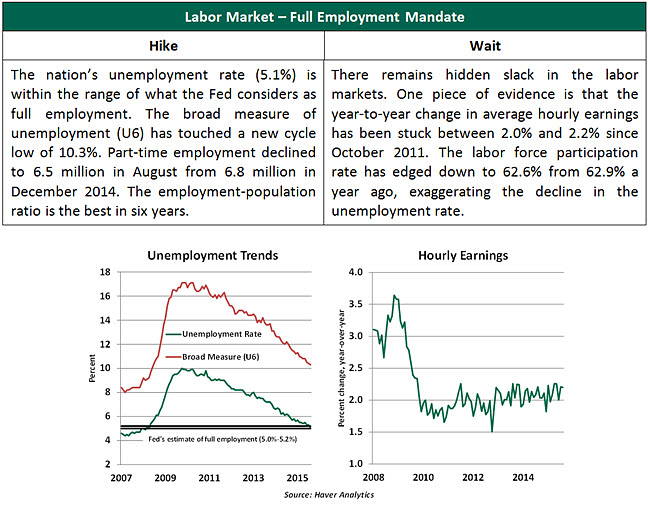

If the United States isn’t at full employment, it isn’t far away. Beyond the unemployment rate, the job-opening rate reached a new record high last month, reflecting strong hiring plans. The ranks of the long-term unemployed are a third of what they were at the peak of the crisis. While there is probably still room for improvement, labor market conditions clearly suggest a move away from zero interest rates.

An interesting note: the unemployment rate has dropped almost 5% from its peak. In the post-war era, we have never seen that kind of decline without a tightening of monetary policy.

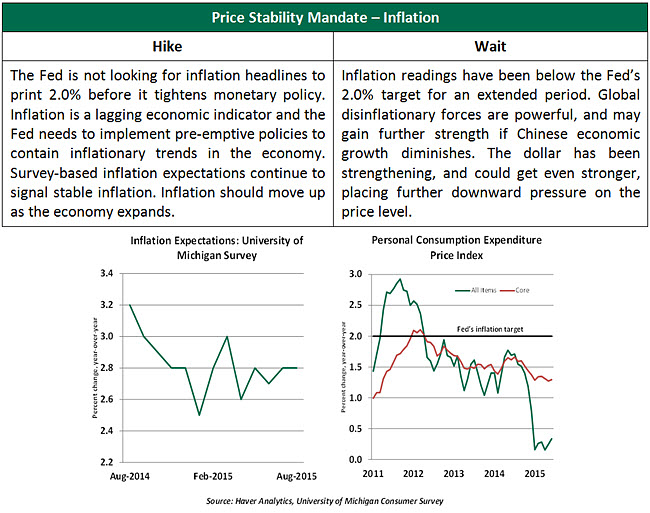

The FOMC has predicated its decisions on the outlook for inflation, not necessarily on where inflation is at present. This forward-looking frame of reference minimizes the influence of volatile components like energy prices, and accounts for diminishing resource slack as the economy grows.

The challenge is that a forward-looking assessment is terribly difficult to assemble at the moment. The potential ripple effects from China could range from benign and fleeting to severe and contagious. That leaves a wide range of paths for the dollar, commodities prices and financial markets.

Even the best of models won’t be able to see clearly through the clouds hanging over the outlook. We’d expect quite a range of expectations to be reflected in the Fed’s updated forecast summary, which will be released after the FOMC meeting. But given the uncertainty, it will be difficult for participants to have confidence that inflation will trend toward the 2% target anytime soon.

Earlier this summer, Fed Chair Janet Yellen testified in front of Congress that, “If the economy evolves as we expect, economic conditions would likely make it appropriate at some point this year to raise the federal funds rate target, thereby beginning to normalize the stance of monetary policy.” Her sentiments were echoed by a series of other FOMC participants, who began to prepare markets for an interest rate increase.

In the weeks following the upheaval in China, many of those same policy makers have been retreating from their positions. New York Federal Reserve President William Dudley said that the case for a September hike of the policy rate is less compelling, and San Francisco Fed President John Williams has become more equivocal in his evaluation of conditions. Fed Vice Chairman Stanley Fischer indicated that a September move was still a possibility, but hardly sounded hawkish.

Yellen has been largely silent over the past two months, making it even more difficult to ascertain what might occur. Given the extreme views on the Fed’s flanks, forging a consensus next week will certainly be challenging.

We have been calling for a September rate hike for more than a year. It is therefore hard to move away from that prediction, given that it is such a close call. But the cost of waiting seems low, and the cost of moving too early seems more substantial. So the odds are that the Fed will temporize, and explain afterwards that they will watch international developments closely during the intermeeting period.

We’ll provide analysis of the outcome in this space next week.