Here Are Two Ways Investors Can Take Advantage of the Fed's Uncertainty

Federal Reserve Chair Janet Yellen this week blinked in the face of—as she described it—global uncertainty, low inflation, and a still-low U.S. labor force participation rate. I’ve written on the emerging markets slowdown numerous times in recent months, so her reasoning is not at all surprising.

Although interest rates could still be hiked in one of the two remaining times the Federal Open Market Committee (FOMC) meets this year, I’m inclined to think they’ll stay near zero until at least 2016.

|

The decision is a welcome one for both gold demand and new home purchases. When rates rise, gold becomes less attractive for some investors, who are encouraged to exchange their no-yielding gold for income-producing assets.

As for loans on new or existing homes, they don’t necessarily rise and fall in perfect correlation with interest rates—they’re more directly related to the 10-year Treasury bond yield—but there’s a strong psychological connection in many potential homebuyers’ minds.

An interest rate reprieve, then, might encourage borrowers to act before it’s “too late,” helping home sales. This could speed up the multiplier effect, or what occurs when there’s an increase in spending that increases income and consumption greater than the initial amount spent. When people buy a home, they also put carpenters to work, purchase new furniture, hire landscaping companies and more.

The same is true when taxes are lower. It creates less friction in the flow of money.

A Record-Setting Year for Chinese and Indian Gold Demand?

Following Yellen’s announcement, I told JT Long of the Gold Report that the Fed’s decision is a wash for precious metals, oil and gas prices. A rate hike would have likely caused the U.S. dollar to strengthen even further, which in turn would have put additional pressure on commodities.

I’ll be watching China’s purchasing managers’ index (PMI) numbers very closely in October and November to see if manufacturing activity will start to turn up. Since China is such an important consumer of metals and other raw materials, it’s crucial that its manufacturing sector break out of the recent slowdown.

An article this week by Oxford Club Resource Strategist Sean Brodrick points out that China’s gold demand, as tracked by deliveries out of the Shanghai Gold Exchange (SGE), is much healthier than many people believe. So far this year, demand has been 36 percent higher than around the same time in 2014, and 13.5 percent higher than in 2013—which was a record year.

Chinese gold demand also tends to increase near the end of the year as the Chinese New Year approaches, so it’s possible 2015 could hit a new record.

Demand out of India is likewise surging, reaching 120 tonnes in August, compared to 50 tonnes this time last year. With important Indian fall festivals quickly approaching such as Diwali, the gold Love Trade is in full swing.

Homebuilders Feeling Good About the Future

Speaking of love, U.S. homebuilders generally seem to have a rosy feeling about the housing market. According to a new survey by the National Association of Home Builders (NAHB), builder confidence in the market for new single-family homes rose to 62 in September, its highest level since November 2005. A reading over 50 means that builders have a positive attitude about economic conditions.

Driving this sentiment are historically low interest rates, low unemployment and steadily rising rents, which makes purchasing a home more appealing.

Housing starts in August fell for a second straight month, but they remain above the one million-unit mark—1.13 million, to be exact—so demand is still on solid footing. This week, Evercore ISI wrote:

Housing starts have already more than doubled and are clearly improving here in 2015. But they still have lots of room to increase.

What this means is there’s a lot of upside opportunity.

A better indicator of the market might be the number of permits filed for new homes, which ticked up 3.5 percent in August.

We own Masco Corporation, which manufactures products for home improvement and new home construction markets. It’s up more than 23 percent year-to-date, while the S&P Homebuilders Select Industry Index is up nearly 30 percent during the same period.

Big Data: October Is the Best Time to Close on a New Home

The reason for a rise in permits is likely because the fall and winter months have traditionally been perceived as the best time of year to buy a new home, due to less competition from other buyers because of the colder weather.

Real estate information company RealtyTrac wanted to check the validity of this longstanding theory and found it be to mostly accurate. After analyzing 32 million home and condo sales since 2000, the group found that buyers tend to get the best deals during October—just next month—when sales prices were 2.6 percent below market value. And if you want to get really precise, October 8 was the absolute best day to close on a home, “when on average buyers have purchased 10.8 percent below estimated market value at the time of the sale,” according to RealtyTrac.

The worst month to buy a home in was April, when prices were at a 1.2 percent premium.

So the takeaway here is that homebuyers who have been sitting on the fence now have a double-incentive to act: historically low mortgage rates and a possible chance at killer bargains.

Government Policy Is a Precursor to Change

Earlier this week, I discussed how homebuilding is important to money velocity, or the rate at which money is exchanged from one transaction to another. The multiplier effect of the housing market, according to the National Association of Realtors (NAR), is between 1.34 and 1.62 in the first year or two of the initial home purchase. What this means is that for every dollar spent on housing, the overall GDP increases by $1.34 and $1.62.

That’s huge. Not just for GDP growth but also job growth.

Global Construction magazine estimates that an average of 22 subcontractors are involved in the building of a single American home, from carpeting specialists to electricians to plumbers. These are just the subcontractors. The count doesn’t include full-time employees of the homebuilder.

All told, then, many more than 22 people are employed in the construction of each home in the U.S., on average. These professionals create wealth not just for themselves but for others as well.

According to Reuters, construction spending by the U.S. government increased 0.7 percent to a huge $1.08 trillion, the highest level since May 2008. Construction spending has increased for eight straight months, in fact.

This is why we always study government policies, because they’re precursors to change.

It’s why government bond yields spiked in anticipation of the Fed decision. The spike lowered the prices of bonds substantially. Based on our models, the drop in bond prices gave our portfolio managers a buy signal in our Near-Term Tax Free Fund (NEARX), allowing us to pick up some nice bargains in short-term municipal bonds attractive at that level.

While Americans are in the early stages of the presidential election cycle, and the debate stage is still crowded, Canadians will head to the polls in a month to decide the direction of their federal leadership.

I’ve been in Toronto this week where the mood is tense as the effect of falling commodity prices has hit the resource-based Canadian economy especially hard and the Canadian dollar is at its lowest level against the almighty American dollar since 2004.

If the Conservative Party remains in power, Prime Minister Stephen Harper will be the first person in more than a century to win four consecutive elections in Canada. It’s also the first three-way toss up in the nation’s history of Parliamentary elections.

Harper has been a reliable champion of commodity investments, small government and lower taxes—policies that I believe contribute to global growth and prosperity over the long term.

Index Summary

- The major market indices finished mixed this week. The Dow Jones Industrial Average lost 0.29 percent. The S&P 500 Stock Index lost 0.15 percent, while the Nasdaq Composite climbed 0.10 percent. The Russell 2000 small capitalization index gained 0.48 percent this week.

- The Hang Seng Composite gained 2.12 percent this week; while Taiwan was up 1.88 percent and the KOSPI rose 2.81 percent.

- The 10-year Treasury bond yield fell 5 basis points to 2.13 percent.

Domestic Equity Market

Strengths

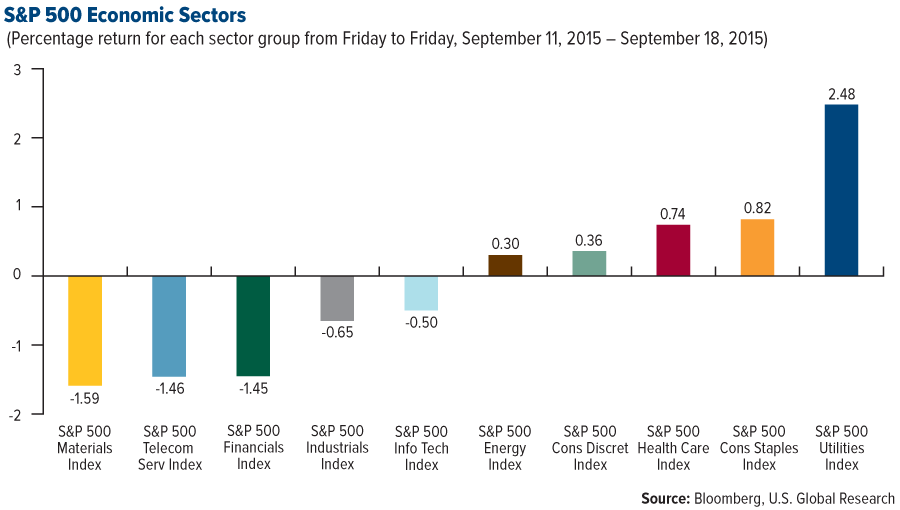

- As a result of the delay of the Federal Reserve’s rate hike, utilities was the best performing sector on a relative basis, up 2.47 percent for the week. In contrast, the S&P 500 Index was down 0.22 percent for the week.

- Molson Coors Brewing was the best performing stock in the S&P 500, up 21.67 percent on the back of Anheuser-Busch’s proposed merger with SABMiller. The merger could have a major impact on Molson Coors with the company operating the Miller Coors joint venture in tandem with SABMiller.

- Initial jobless claims improved to 264,000 from 275,000, and below the expected 275,000. The four-week moving average declined to 272,500 from 275,750. The Labor Department reported that no states or territories estimated claims last week and there were no special factors affecting claims, making this a clean report. The report is consistent with a lower level of firings and continued improvement in the labor market.

Weaknesses

- The materials sector had a tough week, ending as the worst performer with a return of -1.59 percent.

- FMC Corp was the worst performing stock in the S&P 500, down 9.23 percent amid a selloff in fertilizer stocks.

- Empire manufacturing inched up to -14.67 in September from -14.92 in August. This is well below the expected -0.50 and still represents an extremely low value for the index. In fact, excluding last month’s reading, this low level has not been seen since early 2009. The ISM-adjusted index fell to 44.8 in September from 45.0 in August, showing that the components on net deteriorated. This falls notably below the 50 breakeven level.

Opportunities

- Banks continue to do more with less, as evidenced by the surge in loans and the relentless reduction in headcount. They are increasingly willing and able to lend, with the loan-to-deposit ratio making a decisive upshift after a long slump. This is consistent with a more expansionist mindset. Importantly, banks are still enjoying robust credit quality. Loan loss reserves are climbing steadily compared with non-performing loans, as the latter are falling to new cyclical lows. This should provide increased protection against any uptick in bad loans. With housing activity reaccelerating, based on the surge in mortgage purchase applications and the 10-year high in homebuilder sentiment, there is likely an earnings and valuation re-rating ahead in the S&P Banks Index.

- There is lingering concern about how the S&P REIT Index will perform during a Fed tightening cycle, despite the ongoing bullish forces of rising rental inflation and climbing commercial property prices. History suggests that REITs can thrive during a mild and gentle rise in interest rates. With the weak final demand we are seeing around the world, the steady cash flow and yield appeal of the S&P REIT Index should return to favor, given that the path of rate increases will be very gradual when the Fed decides to start the process.

- The latest retail sales reports confirm that grocery stores continue to shine in an otherwise sluggish overall consumption backdrop. Grocery store sales growth is outpacing overall retail sales by an increasing margin. That should drive ongoing store productivity gains, especially in light of the downturn in industry wage inflation. Furthermore, technical conditions are oversold, as the 26-week rate of change is at levels that indicate meaningful upside potential, especially if profit margins positively surprise. All of this is very bullish for retail food stores.

Threats

- The transportation sector is in trouble. Excess capacity and flagging demand have eroded profits. Trade has plummeted as a share of GDP, due to the commodities meltdown, the tightening in global financial conditions courtesy of U.S. dollar strength and deleveraging in China. Consistent with the decline in global export growth, transportation market capitalization has shrunk. When final demand is weak, companies need to respond quickly. However, sector deflation has not yet triggered a broad-based retreat into profit margin preservation mode. Instead, transport capital spending is still accelerating. The implication is that profit margin pressures will remain acute, and as such, a bearish bias should be maintained.

- Energy service stocks are trading at very cheap relative price/book value multiples, which can often be a profitable time to trade this high beta group from the long side. However, from a cyclical standpoint, there is no reason to do so yet. In past cycles, a durable trough required a peak in total OECD oil inventories, a peak in global crude oil production and a rising global oil rig count. At the moment, none of these conditions exist.

- According to BCA’s U.S. equity indicators, investors shouldn’t chase any relief rally that emerges in the wake of extreme volatility. Their Intermediate Equity Indicator, designed to catch three- to six-month equity moves, has fallen below the zero line for the first time since the October 2014 correction. It snapped back quickly in 2014, but has yet to do so this time around.

The Economy and Bond Market

Global stocks generally gave back the week's gains on Friday. U.S. indices climbed steadily on strengthening U.S. economic data, but the U.S. Federal Reserve's decision on Thursday to leave interest rates unchanged was attributed to concern about global weakness. That led to a wide-scale selloff in stocks and a rally in U.S. Treasuries, German bunds and gold.

The yield on the 10-year U.S. Treasury note fell to 2.13 percent Friday from 2.29 percent before the Fed's policy announcement. After falling sharply to 18, right after the Fed's decision, the VIX Index moved back above 22 on Friday. U.S. WTI crude oil futures traded around $45 per barrel Friday, while Brent crude oil was priced near $48.

Strengths

- Retail sales increased 0.2 percent month-over-month (MoM) in August, down from an upwardly-revised 0.7 percent MoM in July. This was slightly below the expected 0.3 percent MoM gain.

- Building permits were reported at 1,170,000 in August, up 3.5 percent MoM from 1,130,000 in the prior month. This was above the expected 1,159,000. This suggests that the trend for homebuilding is still higher, consistent with the positive signal from the NAHB survey in early September.

- The current account balance eased slightly in the second quarter to a deficit of $109.7 billion from an upwardly revised $118.3 billion. The market expected a $111.5 billion deficit. As a percentage of GDP, the current account deficit stands at 2.45 percent in the second quarter, a slight improvement from 2.68 percent in the first quarter.

Weaknesses

- At Thursday’s meeting, the Fed not only failed to hike, but also delivered a relatively dovish statement. There were two key messages. First, there is concern about global economic and financial developments. Fed Chair Yellen cited the drop in equity prices, further appreciation of the dollar, and a widening of risk spreads. Second, the Fed gave some concession on inflation expectations citing they have moved lower.

- Industrial production declined 0.4 percent MoM in August, down from a 0.9 percent MoM increase in the prior month. This is below the expected 0.2 percent MoM decline. Much of the weakness came from manufacturing and mining.

- The Philadelphia Fed Business Outlook Index declined to -6.0 in September from 8.3 in August, notably below the expected 5.9. The ISM-Adjusted Index only softened to 51.0 from 52.6, still above the 50 breakeven level, suggesting that the components of the report were still fairly solid. This likely means manufacturers are concerned about downside risks to the sector but are not actually seeing the deterioration yet.

Opportunities

- The post-FOMC meeting communication was very vague about what needs to occur for policymakers to become more optimistic about “global developments.” A number of FOMC members are scheduled to speak over the weekend and next week, and any color on their views of the global outlook will be important.

- Chinese President Xi Jinping will visit Washington, DC for a meeting with U.S. president Barack Obama on Friday. The visit between the two presidents has taken on greater importance as of late, in light of the People’s Bank of China’s decision to move toward a managed peg.

- U.S. Existing Home Sales for August will be released on Monday. With the one-month trend above the three-month, August should continue to show a robust housing market.

Threats

- The U.S. Treasury market is not priced for a gradual Fed rate cycle. Interest rate expectations are likely to move higher once the Fed starts the process and investors realize the economy can cope. This will put upward pressure on yields across the curve. The 10-year U.S. Treasury appears vulnerable, with yields trading in a pattern of higher highs and higher lows, much like the way it traded in late 2012 and early 2013 before yields spiked to 3 percent. The Fed’s decision this week only delays the inevitable rate hikes down the line.

- U.S. Durable Goods Orders for August will be released on Thursday. The consensus expects a decline of 2.1 percentage points towards further deterioration in demand for manufactured goods.

- U.S. second quarter GDP will be released next Friday. Given pressures from a strong dollar and weak global demand, the expected growth of 3.7 percent may be too optimistic.

Gold Market

For the week, spot gold closed at $1,139.27 up $31.49 per ounce, or 2.84 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, gained 9.83 percent. The U.S. Trade-Weighted Dollar Index gained 0.05 percent for the week. Senior miners outperformed juniors for the week as the GDM Index gained 9.83 percent, more than the S&P/TSX Venture Index’s gain of 7.60 percent.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Sep -15 | GE ZEW Survey Current Situation | 64 | 67.5 | 65.7 |

| Sep -15 | GE ZEW Survey Expectations | 18.3 | 12.1 | 25 |

| Sep -16 | EC CPI Core YoY | 1.00% | 0.90% | 1.00% |

| Sep -16 | US CPI YoY | 0.20% | 0.20% | 0.20% |

| Sep -17 | US Housing Starts | 1160K | 1126K | 1206K |

| Sep -17 | US Initial Jobless Claims | 275K | 264K | 275K |

| Sep -17 | US FOMC Rate Decision (Upper Bound) | 0.25% | 0.25% | 0.25% |

| Sep -22 | CH Caixin China PMI Mfg | 47.6 | -- | 47.3 |

| Sep -24 | HK Exports YoY | -1.50% | -- | -1.60% |

| Sep -24 | US Initial Jobless Claims | 275K | -- | 264K |

| Sep -24 | US Durable Goods Orders | -2.20% | -- | -2.00% |

| Sep -24 | US New Home Sales | 515K | -- | 507K |

| Sep -25 | US GDP Annualized QoQ | 3.70% | -- | 3.70% |

Strengths

- Silver was the best performing precious metal for the week, up 3.9 percent. It outperformed gold for the week on the back of increased offtake by industrial users and coin makers. Confidence in gold as a safe-haven asset returned following dollar weakness after the Federal Reserve left U.S. interest rates unchanged. The metal saw its first weekly gain in four weeks as a result. China’s economic slowdown, rising emerging-market currency volatility and the Fed highlighting “heightened uncertainties,” may persuade more investors to seek refuge in gold. This could be a bullish signal for gold, at least in the short-term, particularly as investors in China have been acquiring gold in anticipation of a rally.

- Roxgold provided a positive update on construction at its ultra-high grade Yaramoko project in Burkina Faso. The company announced that the Yaramoko water storage facility and tailings storage facility embankments were completed ahead of schedule, while the bulk earthworks at the mine camp are now 95 percent done. The underground mine is expected to produce 99,500 ounces per year for seven years, beginning mid-2016. Yaramoko is one of the highest grade, undeveloped deposits in the world, with an average grade of 11.83 grams per ton. It also contains some of the lowest costs in the industry, with all-in sustaining costs estimated at $590 an ounce. Sunridge Gold Corp. announced the signing of a mining agreement with the Eritrean Ministry of Energy and Mines. The ministry will issue three mining licenses, providing the key permits required for development of the four advanced projects – Emba Derho, Adi Nefas, Gupo Gold and Debarwa – that constitute Sunridge’s copper-zinc-gold project in Eritrea. Pretium Resources announced a $540 million construction financing package with the Orion Mine Finance Group and Blackstone Tactical Opportunities for its Brucejack Project. In doing so, Pretium largely funds a major, undeveloped gold project in Canada centered on a uniquely high-grade gold deposit.

- JPMorgan is calling a bottom on the mining sector, suggesting now is the time to pounce. The bank slapped an overweight on the sector this week, ending its bearish view. JPMorgan’s argument for miners was that in price-relative terms, mining is back to its levels from 10 years ago, when the Chinese commodity super-cycle was just starting. They see prices stabilizing in the coming year and note that miners have lowered capital spending in the past few years. They also believe that the bulk of EPS downgrades are behind us given the latest consensus projections of -44 percent year-on-year EPS growth for miners in 2015.

Weaknesses

- Platinum was the weakest precious metal for the week, rising 1.22 percent. Consumers in China purchased fewer autos in August, the third straight month of declines. This weighed on both platinum and palladium, which are used in gasoline engines to control emissions.

- According to a new Division of Minerals report put out by the state, just 4.94 million ounces were extracted from Nevada’s mines in 2014, compared to 5.5 million ounces in the previous year. 2014 was the first time since 1988 that production of the precious metals dropped so low. Various mines have been forced to close in recent years as they have not been able to stay profitable amid the plunge in the price of gold.

- Even stockpiles at a two-year low aren’t enough to cheer gold investors. Inventories of the metal on the Comex in New York have fallen for seven straight sessions to 6.89 million ounces, the smallest since October 2013. According to Jeffrey Christian, managing director at CPM Group, the Comex running low on stockpiles is a non-issue because most Comex futures contracts are cash settled and traders don’t take delivery of the metal. Additionally, while the percentage of Comex gold open interest covered by total Comex reported stocks has fallen over the past year and a half, it remains very high by historical standards. Furthermore, he added that gold futures, which have dropped more than 5 percent this year and are headed for a third straight annual decline, aren’t likely to rebound soon as the economic and political outlook probably won’t be threatening enough to generate a jump in investment demand until 2017. Nonetheless, the group said it considers bullion an excellent investment at current prices, on a long-term basis.

Opportunities

- According to Balvinder Kumar, of the Indian Mines Ministry, studies by state governments have uncovered some very deep and old mines with gold worth more than $3.9 billion existing in the Kolar region in the southern state of Karnataka alone. Allegedly, the ministry will put about 80 mines to auction within two or three months. That could allow miners to acquire rich assets at a time when valuations are low and sentiment toward the sector is still predominantly negative. Separately, Randgold Resources announced it has concluded a joint venture agreement to redevelop AngloGold Ashanti’s Obuasi gold mine in Ghana. Randgold said it would lead and fund the development plan to rebuild the mine, which is a large, high-grade deposit with proven and probable ore reserves of 24.53 metric tons at 6.70 grams per ton, making for 5.29 million ounces of gold.

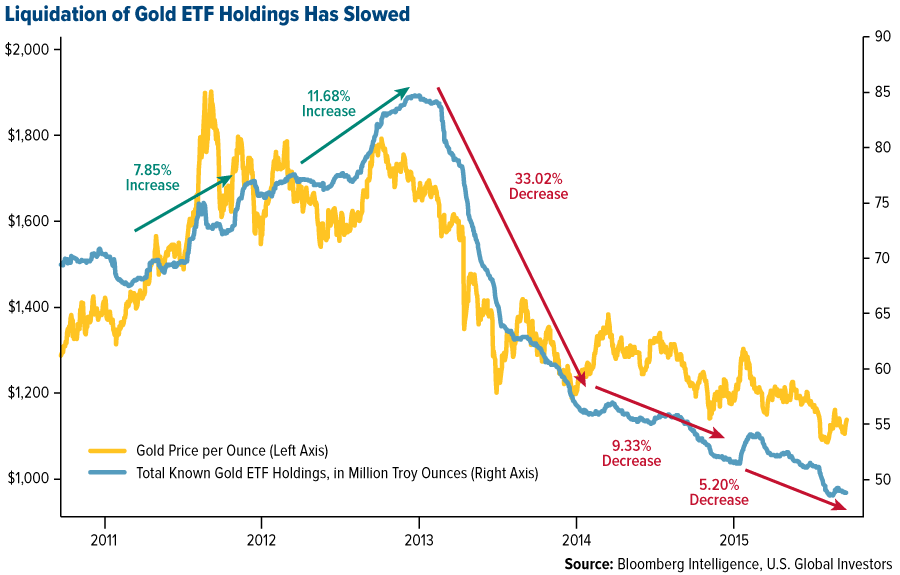

- ETF gold holdings have declined by 5.2 percent this year, while gold has fallen by 6.3 percent. The pace of withdrawals has slowed, possibly indicating that sales may be coming to an end. Based on past rallies, ETF buying may pick up if gold prices start to climb. This could be prompted by the Chinese. The decline of the Chinese real estate market moved billions of dollars into the country’s stock market, which saw a dramatic rise and then equally sharp decline. If Chinese investors fleeing from stocks decide that the historic value in gold is tempting, that could mean the next boom could come in gold. The metal has historically been a safe-haven in countries that suffer from bouts of inflation as well as political upheaval.

- China continues to be one of the world’s largest buyers of gold as gold deliveries from the Shanghai Gold Exchange continue to set record highs. SGE volumes were up 14.2 percent through August versus the same month in 2014, and are on pace to reach almost 2,600 metric tons of gold this year. The planned establishment of a yuan-based gold fix by the SGE by the end of 2015 also shows that China wants to have its say in the global pricing of the metal.

Threats

- Researchers say they found scattered accumulations of heavy metals along 60 miles of riverbank in Colorado and New Mexico after the Gold King Mine spill. About 3 million gallons of wastewater rushed out of the mine August 5 after a cleanup crew supervised by the Environmental Protection Agency inadvertently breached a debris dam. Congressional investigators are looking into why the EPA didn't do more to find out how much toxic water was inside Gold King before using heavy machinery to open it. The agency needs to answer that question publicly and tighten its procedures accordingly. Unlike the oil and gas sector, companies that extract gold, silver, uranium and other heavy metals from federal lands pay no royalties to the government. Legislation in the House of Representatives threatens this by the potential of amending the 1872 law that still governs mining. The intention would be to force the mining industry to help foot the bill for disasters like this.

- An Argentine court has ordered a five-day suspension of the gold leaching process at Barrick Gold Corp's Veladero mine to determine whether there was any environmental damage from a cyanide leak triggered by a faulty valve. A lengthier prolongation of the mine closure could have materially adverse economic impacts on the company.

- Palladium-backed ETFs in August had their biggest monthly outflow in six months as prices slid to a five-year low of $533 an ounce. Demand for the metal, mainly used in emission control systems of gasoline-fueled vehicles, has been hurt by a three-month decline in Chinese auto sales. Given stock market volatility and worsening economic data out of China, this rout could have more room on the downside as consumers feel the pinch.

Energy and Natural Resources Market

Strengths

- Gold and precious metals stocks rebounded this week after the Federal Reserve decided not to raise the benchmark interest rate. The announcement weakened the U.S. dollar while strengthening gold. The Philadelphia Gold & Silver Index gained 9 percent this week.

- Expectations for higher OPEC crude oil production were supportive for tanker stocks with VLCC (Very Large Crude Carrier) exposure. The Bloomberg Tanker Index jumped 5.4 percent.

- Higher weekly WTI crude oil prices, along with the Fed’s decision not to raise interest rates, helped oil & gas royalty stocks this week. The Yorkville Oil & Gas Royalty Index gained 4.6 percent during the week.

Weaknesses

- Base metals stocks declined this week on renewed fears over China’s economic growth outlook. The S&P/TSX Capped Diversified Metals and Mining Index fell 4.6 percent this week.

- Falling margins and the start of seasonal maintenance weighed on refining stocks this week. The S&P Oil Refining Index fell 3.4 percent.

- Oversupply, along with soft pricing for potash and other fertilizers, pressured agricultural chemical companies this week. The Bloomberg Fertilizer Index dropped 2.2 percent.

Opportunities

- New home sales will be released next week and expectations are for 514,700 new starts, versus 507,000 in the prior month.

- The U.S. manufacturing purchasing managers’ index (PMI) is set to be released next week. The forecast reading is 53.1, a slight increase from the prior month.

- Bloomberg reports that executives at Exxon, the world’s largest publically-listed oil company, are in talks with producers in the Permian Basin to negotiate possible purchases and joint ventures.

Threats

- According to Goldman Sachs, there is a high probability that crude oil prices will stay low through the end of the next decade as the world shifts from the “investment phase” of global exploration and development to the “exploitation phase,” with shale as a main source of output.

- Despite the recent rally, copper prices have not broken out of a multi-year bear market yet. According to Bank of America, production cuts are not yet sufficient to rebalance the global market.

- Persistent U.S. natural gas output will continue to boost inventories, which are forecast to reach a record level when the traditional heating season begins. If temperatures are warmer than normal this winter, natural gas prices could be negatively impacted.

China Region

Strengths

- Malaysia was the best performing country in Asia this week, as both crude oil and the Malaysian ringgit rebounded, thanks to the absence of any interest rate hike by the Federal Reserve. The FTSE Bursa Malaysia KLCI Index advanced 6.25 percent this week.

- Information technology was the best performing sector in Asia this week, driven by rising semiconductor and electronics companies from Taiwan and South Korea, ahead of the new iPhone sale. The MSCI Asia Pacific ex Japan Information Technology Index rose 3.58 percent this week.

- The Malaysian ringgit was the best performing currency in Asia this week, strengthening by 2.06 percent, in response to the U.S. dollar’s retreat as the Fed delayed its interest rate hike.

Weaknesses

- Chinese A-Shares performed poorly this week, as investors shrugged off the weekend’s release of China’s State-Owned Enterprise Reform Plan. The plan seemed thin on detail, and remained nervous in tone about continued capital flight and the prospect of currency stability. The Shanghai Composite Index declined 3.05 percent this week.

- Telecommunication services was the worst performing sector in Asia this week, as investors stayed away from defensive sectors during a week of regional market recovery. The MSCI Asia Pacific ex Japan Telecommunication Services Index gained 0.75 percent.

- The Indonesian rupiah was the worst performing currency in Asia this week, weakening by another 0.23 percent. The weak rupiah was driven by the country’s lower-than-expected trade surplus in August, at $0.4 billion, narrowing from July. Overseas funds have sold a net $991 million of Indonesian shares this quarter, the biggest net outflow in more than two years.

Opportunities

- Maintaining higher-than-normal cash levels should continue to help our China Region Fund, as Chinese equities could remain unsettled in the near term given: (1) accelerating capital outflow from China in August; (2) decelerating tax revenue growth in the first eight months of this year at only 4.4 percent; and (3) the probable continuation of slowing manufacturing activity to be revealed in next week’s purchasing managers’ index (PMI) release.

- Taiwanese semiconductor and electronics companies on Apple’s supply chain could continue to benefit from any upside surprise from initial sales of the iPhone 6S/6S Plus in China, starting September 25.

- Standard and Poor’s surprise upgrade of South Korea’s sovereign debt rating, along with the first net foreign purchase of South Korean stocks in nine weeks, might be an early sign that investor sentiment towards South Korea is on the mend. Its market could see continued positive momentum in the short term.

Threats

- Lingering political noise fueled by anti-ethnic Chinese riots in Kuala Lumpur this week, coupled with little convincing evidence of recovery in the crude oil market might result in another round of volatility in Malaysian stocks and the Malaysian ringgit.

- Deteriorating working capital and operating cash flows at certain Macau casino operators could worsen investor fears of dividend cuts and reduce the appeal of casino stocks to long-term income investors. Should there be no concrete signs of a pickup in Macau visitor arrivals in August, due to be released next week, investor sentiment might remain subdued towards this sector.

- Further draconian restrictions on index futures trading in the Chinese A-Share market, and alleged government plans to close over 150 factories near the future location of the Shanghai Disney Park around its launch date, signify little change in the mindset of Chinese policymakers. These policymakers rely on command and order measures, which do little to lift global investor confidence in China.

Emerging Europe

Strengths

- The Borsa Istanbul 100 Index was a strong performer this week, gaining 5.25 percent. The Turkish lira rebounded from oversold levels, gaining 1.17 percent. The Federal Reserve decision not to hike interest rates helped Turkish equities and the lira to regain some strength in a country that relies heavily on foreign capital inflows to finance its trade deficit.

- The Russian ruble was the strongest currency this week, gaining 1.86 percent. The Fed’s decision to hold borrowing costs near zero gave Elvira Nabiullina, Governor of the Central Bank of Russia, the chance to extend a series of interest rate cuts.

- The industrial sector was the strongest this week, led by Turkish industrial holdings.

Weaknesses

- The Czech Republic was the weakest market this week, with the Prague Stock Exchange Index losing 1.77 percent. The Czech Republic’s PPI declined by 3.7 percent compared to the prior year. Low interest rates and central bank interventions to prevent the appreciation of the Czech koruna have had little effect on inflation. August inflation was reported at 0.3 percent, lower than expected.

- The Polish zloty was the weakest currency, losing 39 basis points in a week. Political risk looms over Poland as the conservative Law & Justice party gains support before the parliamentary election scheduled for later this year.

- The utility sector was the weakest sector for the week, led by weakness in Polish utilities.

Opportunities

- Emerging European equites and currencies were trending higher for two days prior to the Fed’s rate announcement. On Thursday, the Fed left interest rates unchanged at 25 basis points, boosting demand for Emerging European assets.

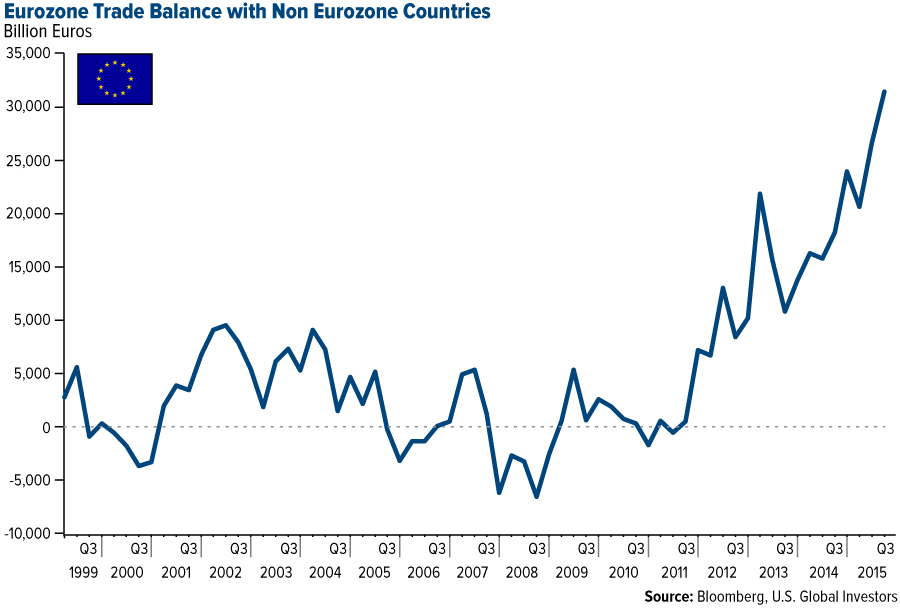

- The latest release of trade surplus data for the eurozone hit a record high not seen since January 1999. Exports of goods exceeded imports by 31.4 billion euros in July, up from 21.2 billion in the same month last year. A weaker euro at the start of the third quarter contributed to the economic recovery.

- After Prime Minister of Greece Alexis Tsipras resigned last month, Greeks will go to the polls for the third time this year. The latest polls show growing support for the conservative New Democracy party, slightly ahead of the left-wing Syriza party.

Threats

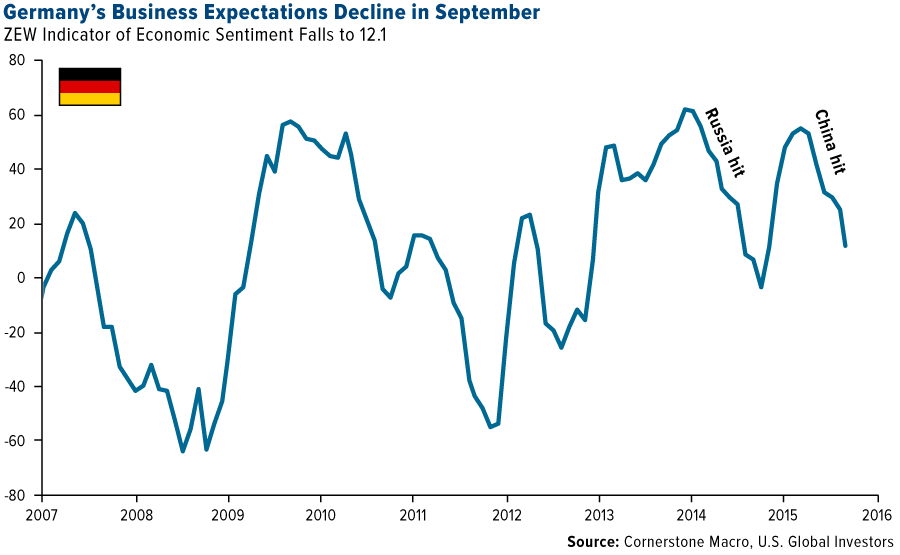

- Germany’s ZEW Indicator of Economic Sentiment declined 13 points in September, suggesting downside risk to German economic activity. The sharp decline in the ZEW last year was due to Russia’s turmoil. This year’s decline is likely due to China’s slowdown.

- The Markit Eurozone Composite purchasing managers’ index (PMI) data is expected to decline from 54.3 to 54 in September. This would suggest expansion but at a slower rate compared to the previous month.

- The latest polls in Turkey show that support for the current ruling party is falling. The AKP party failed to form a collation in recent months and a snap election is scheduled for November 1. Political risk may weigh on equities and the Turkish lira.

(c) US Global