With the benefit of some additional time to reflect, here are some deeper thoughts on yesterday’s Federal Open Market Committee (FOMC) meeting.

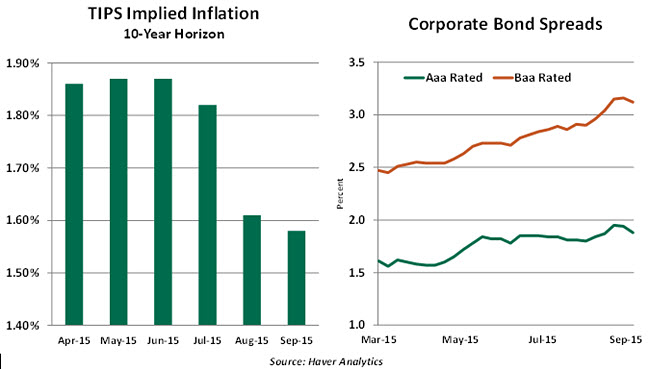

- The Federal Reserve has typically downplayed market expectations of inflation. These indicators emerge from trading in Treasury Inflation-Protected Securities (TIPS), which can be influenced by many things. A flight to safety, for instance, will raise TIPS prices, lowering their yields. This may reflect an asset allocation choice rather than expectations of disinflation.

Nonetheless, market-based expectations of long-term inflation have dropped from 1.9% to less than 1.6% since July. And this merited mention in both the FOMC statement and in Janet Yellen’s press conference. The decline could prove to be another of the many false alarms the TIPS market has signaled over the years. But because survey-based measures of inflation don’t typically change much over time, market indicators can provide an early warning.

The FOMC was not comfortable enough with the inflation outlook to change policy this month. The TIPS market may be one reason why, and it bears watching in the weeks ahead.

- Chair Yellen also noted that financial conditions had tightened somewhat over the past several months. Bond spreads have widened, and measures of financial stress have risen. Both are likely due to the market uncertainty kindled first by Greece and then by China. This acts as a tightening in credit conditions, which may have reduced the urgency within the FOMC to tighten credit conditions.

-

It is hard, at times, to interpret the Fed’s dot chart. But if my eyes don’t deceive me, there were still six participants who called for more than one move this year. One might reasonably assume that those six had thought that hikes in September and December were appropriate, given their outlook on the economy.

One of the six is clearly Jeffrey Lacker, who dissented from yesterday’s decision. It is not clear who the other five are, and whether they are current FOMC voters. But the dots do reveal that sentiment going into the meeting was not as dovish as the post-meeting messaging.

If the economic news, especially on the employment front, continues to be positive, there will be a core of Fed officials who will urge action in December. In that instance, it may be hard for Janet Yellen to disagree with them.

It is hard, at times, to interpret the Fed’s dot chart. But if my eyes don’t deceive me, there were still six participants who called for more than one move this year. One might reasonably assume that those six had thought that hikes in September and December were appropriate, given their outlook on the economy.

It is hard, at times, to interpret the Fed’s dot chart. But if my eyes don’t deceive me, there were still six participants who called for more than one move this year. One might reasonably assume that those six had thought that hikes in September and December were appropriate, given their outlook on the economy. Money for Nothing?

My brother and I grew up in a very small apartment. When the weather was warm, we’d play outside as long as we could. But during the winters, we played soccer, hockey, football and basketball inside our tiny living room. The furniture took a horrible beating.

My mother was constantly admonishing us to settle down, threatening us with all manner of consequences. I proposed a different kind of incentive: raise our allowance, I said, and we’ll knock off the rough stuff. That got me a week of doing the dishes.

The notion of paying someone to prevent undesirable outcomes is not easily embraced. As the Federal Reserve contemplates its interest rate strategy, it is facing criticism in some corners for essentially paying banks to slow down their lending. While this is an oversimplification, it is among the complications of moving away from near-zero interest rates.

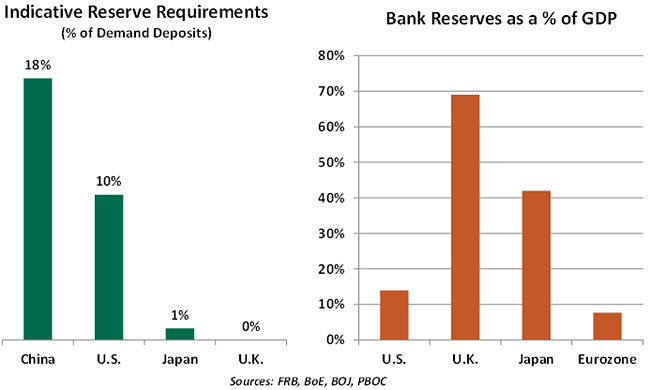

Reserve requirements are still used in some nations as an instrument of monetary policy; raising reserve requirements tightens credit, while lowering them does the opposite. Different countries use this lever to varying degrees.

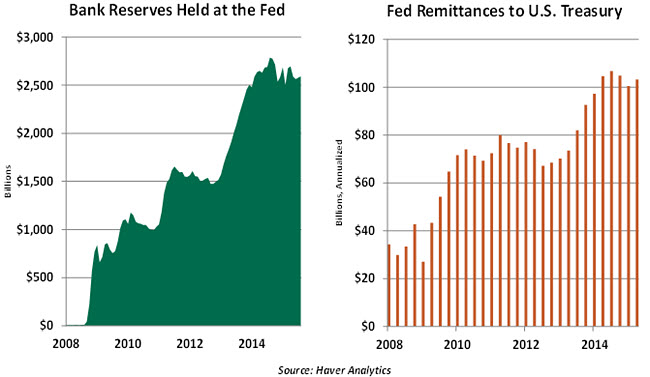

Reserves held with the Federal Reserve paid no interest prior to 2008, so lenders went to great lengths to minimize them. Sweep products, which automatically transfer balances nightly from accounts which require reserves to investment vehicles, are just one of many strategies financial companies use for this purpose. As a result, reserve requirements have diminished as a policy instrument in the United States.

On those occasions where U.S. institutions had excess reserves, they lent them to banks that needed them via the Federal funds market. The rate on these transactions, the Federal funds rate, is the subject of the Federal Reserve’s short-term rate targeting. The Fed’s current target range for the Fed funds rate is 0 to 25 basis points, and policy has endeavored to keep actual trading in the middle of that band.

Once quantitative easing began in late 2008, the U.S. financial system was awash with liquidity, and banks had far more deposits than they could possibly deploy. To prevent the excess supply of reserves from driving the Fed funds rate to infinitesimal levels, the Fed began paying interest on excess reserves (IOER) to banks. The IOER rate stands at 25 basis points, the top of the interest rate range cited in the Fed’s statements.

The IOER rate essentially restricts supply in the Fed funds market by offering banks an alternative to selling excess reserves in the marketplace. That helps to keep the Fed funds rate at the desired level. The IOER rate aids monetary policy in a second way: by offering a modest return on accounts held with a riskless counterparty, holding reserves at the Fed becomes an alternative to new lending, which carries higher returns but also higher risks.  While undeniably effective as an instrument of monetary policy, the interest payments to the banks have drawn some political fire. On the surface, the Fed appears to be giving $6 billion annually to the very organizations that led the world financial system to the brink of disaster seven years ago. The fact that foreign banks with U.S. operations are among the recipients only adds to the anxiety.

While undeniably effective as an instrument of monetary policy, the interest payments to the banks have drawn some political fire. On the surface, the Fed appears to be giving $6 billion annually to the very organizations that led the world financial system to the brink of disaster seven years ago. The fact that foreign banks with U.S. operations are among the recipients only adds to the anxiety.

Some have suggested that the Fed is channeling American tax dollars to those whose rescue cost taxpayers dearly. This is not strictly true: the Federal Reserve earns substantial amounts on the investments it holds, which are more than enough to offset payments to its depositors. No tax money is involved. The income earned by the Fed, net of its operating expenses, is remanded to the U.S. Treasury; this amounted to nearly $100 billion in 2014.

When the Fed ultimately raises interest rates, it has signaled that the IOER rate will be increased to set the top of a new range for the Federal funds rate. As the IOER rate goes up, interest payments to banks will rise and annual rebates to the Treasury will drop. That is part and parcel of monetary policy, but it will certainly catch the attention of the Fed’s Congressional critics.  Some have suggested that the Fed could achieve a similar end by returning to the use of reserve requirements as a policy tool. Should they wish to restrain credit, thereby moderating the pace of economic growth, they could simply lock some of the excess reserves in place by fiat. From a populist perspective, this would have the favorable appearance of reducing payments from the Fed to financial institutions.

Some have suggested that the Fed could achieve a similar end by returning to the use of reserve requirements as a policy tool. Should they wish to restrain credit, thereby moderating the pace of economic growth, they could simply lock some of the excess reserves in place by fiat. From a populist perspective, this would have the favorable appearance of reducing payments from the Fed to financial institutions.

But raising reserve requirements would carry significant risks. The United States has no recent experience to guide the decision of how the economy would react to a reserve increase, so sizing such a step properly would be very challenging. As mentioned earlier, banks have proven pretty resourceful when it comes to working around reserve requirements, so increasing them ultimately may not be that limiting. And the Federal Reserve has been criticized for its 1937 decision to double reserve requirements, which added to the Great Depression.

So expect the Fed to continue using positive incentives rather than punitive ones. I wish my mother had followed that advice when we broke the sofa. I think I am still paying for that one.

Full Unemployment – A Moving Target

The definition of full employment is an important input to monetary policy. The Fed tends to maintain an accommodative stance before reaching full employment, and a restrictive one afterwards. What makes the process more challenging is the range of opinions about what full employment looks like.

Full employment does not mean there is zero unemployment, because at any point in time people are in between jobs and there are also people with obsolete skills who need retraining. It is not a fixed rate, and it changes over time. A lengthening of unemployment benefits during recessions can raise the level of unemployment that is consistent with full employment. Licensing changes and other certification requirements for jobs also play a role.

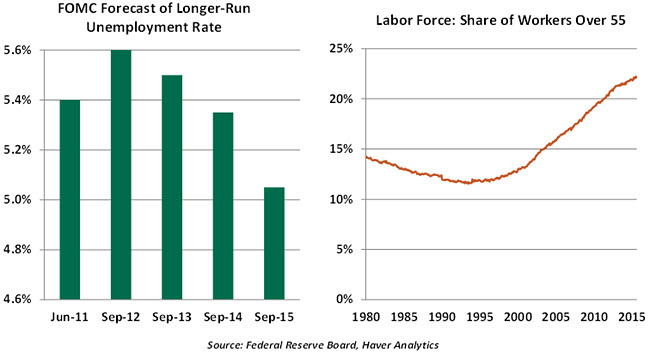

The longer-run jobless rate that is associated with full unemployment is the rate of unemployment at which there is no tendency for inflation to increase. It is an estimated – not an observed – rate of unemployment. The Congressional Budget Office estimated that a 5.1% jobless rate represented full employment for 2015.

The Fed’s latest Summary of Economic Projections showed a slightly lower estimate of the long-term unemployment rate as compared with the June projections. (Many analysts associate this with a state of full employment.) Now at a range of 4.9% and 5.2%, the Fed’s long-run window is down several notches from 2011 (5.0%-6.0%). The adjustment mostly reflects cyclical influences on the unemployment rate.

Studies suggest that other factors influence the full employment mark. Research at the Federal Reserve Bank of Chicago indicates that the change in composition of the labor force is one such determinant. According to this research, the longer-run unemployment rate would be 4.6% by 2020. It is well known that the labor force participation (LFP) of the United States has declined in the last 15 years. But shifts in the country’s age ranges may play an important role in defining full employment.

Studies suggest that other factors influence the full employment mark. Research at the Federal Reserve Bank of Chicago indicates that the change in composition of the labor force is one such determinant. According to this research, the longer-run unemployment rate would be 4.6% by 2020. It is well known that the labor force participation (LFP) of the United States has declined in the last 15 years. But shifts in the country’s age ranges may play an important role in defining full employment.

Teenagers accounted for 8% of the labor force in the early 1980s, but they made up only about 4% in August 2015. Although baby boomers are retiring in large numbers, the share of workers 55 years and older is about 22% of the labor force now compared with 12.5% in the 1990s. Typically, the unemployment rate of this older group is significantly lower than the teenage cohort. Therefore, the new composition of the labor force has probably resulted in a lower rate of unemployment consistent with full employment compared with levels seen in prior periods.

Another related issue that bears on the full employment gauge is employment flows and business dynamics. Reduced business volatility and job destruction means fewer people will be in between jobs. The technical term for job-to-job movement of workers is labor market churn. Studies have shown that labor market churn in recent years has declined. This phenomenon puts downward pressure on the unemployment rate associated with full employment.

If such factors are working in the background, the U.S. unemployment rate has room to fall further. This would suggest the presence of more labor market slack than estimated, and reduced wage pressures.

Like today, the Fed had a hard time defining full employment during the business expansion prior to the Great Recession. The full employment concept is a simple and useful benchmark in theory but complex in practice.

(c) Northern Trust