Shake Portfolios up after a Market Shakedown

“That which does not kill us makes us stronger.” —Friedrich Nietzsche

Portfolio management is a lot like managing your health: There’s little incentive to change things when things are chugging along. It’s only when something breaks down that you tend to revisit your assumptions and take action. Market breakdowns change valuations and shake nerves, but it’s a good time to see what may rebound.

Is this a rebound, or is worse to come?

The first question to ask—before getting to the question of “What’s attractive in a rebound?”—is “Will there be a rebound?” We think so. In the run-up to the corrections of the 1990s and 2000s, The Conference Board’s Index of Leading Economic Indicators (LEI) was flat to down in the 6 to 12 months before a correction. In the most recent correction, the LEI dipped down briefly, but it was only because of 1 of the 10 components that make up the LEI. That one component—building permits—was distorted by the expiration of tax incentives for building in New York. The other nine components of the LEI looked pretty decent.

That’s one reason this correction seemed backward, being driven by fears of the future rather than the realization that things weren’t as good as they seemed. We think the future isn’t bleak. China may have its challenges, but the American consumer is being encouraged by substantial improvements in the labor market, a buoyant housing market, and a pickup in consumer credit.

What has worked in previous rebounds?

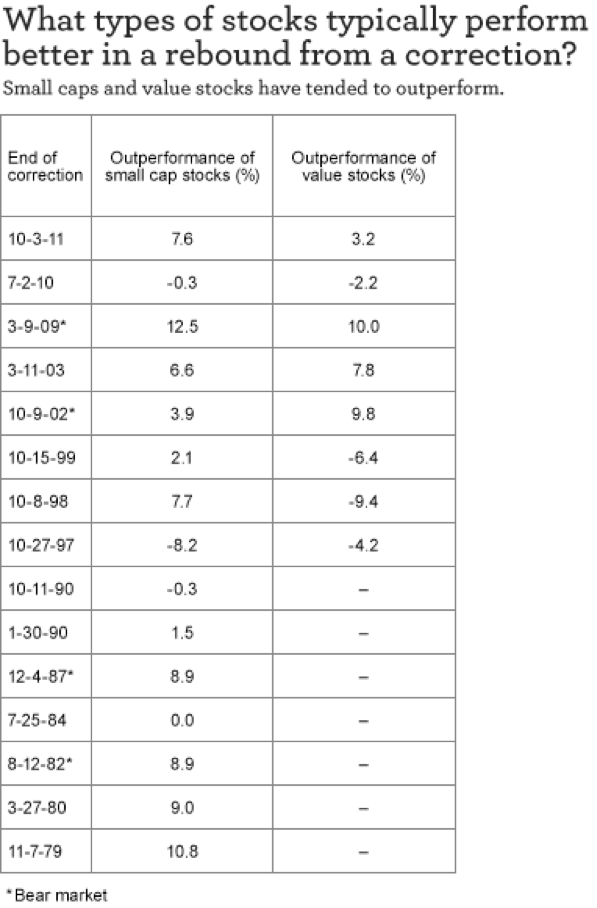

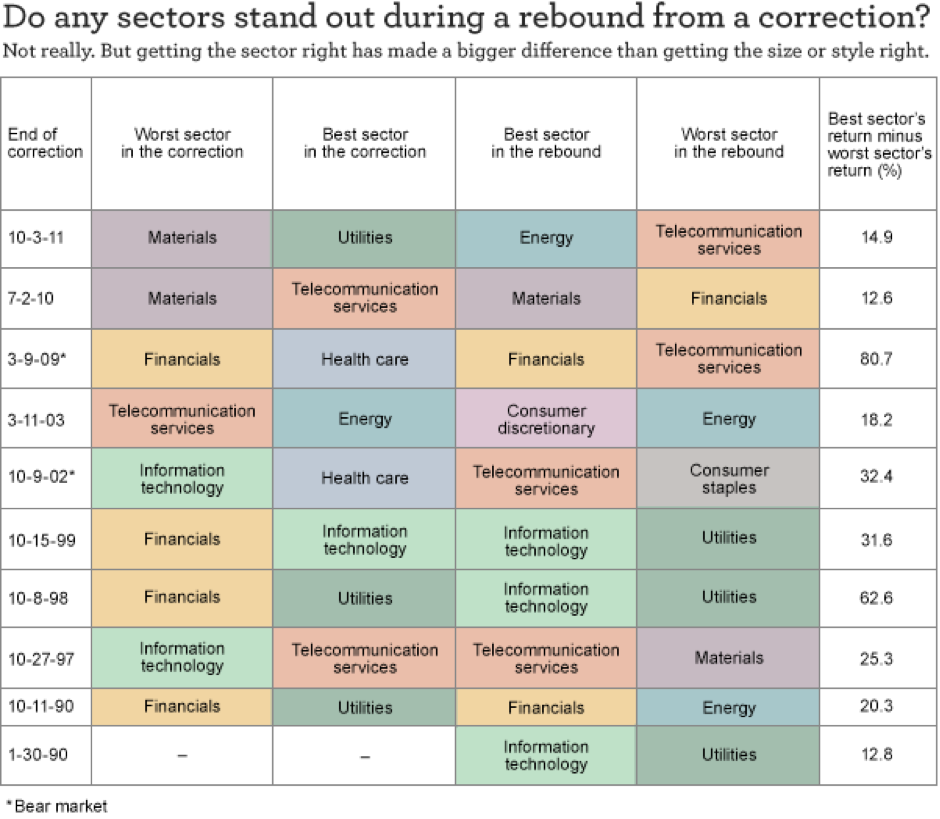

Here are two tables showing the trough dates of corrections (and bears) and the returns based on subsequent (and previous) 60-day moves:

Past performance is no guarantee of future results.

Sources: FactSet and authors’ calculations, based on S&P 500 Index (large stocks), Russell 2000® Index (small stocks), S&P 500 Value Index (value stocks), S&P 500 Growth Index (growth stocks), and the 10 sector indexes of the S&P 500 Index’s subsequent 60-day returns.

Past performance is no guarantee of future results.

Sources: FactSet and authors’ calculations, based on S&P 500 Index (large stocks), Russell 2000® Index (small stocks), S&P 500 Value Index (value stocks), S&P 500 Growth Index (growth stocks), and the 10 sector indexes of the S&P 500 Index’s subsequent 60-day returns.

In the rebound from a correction, small typically wins. Value typically wins. Which sector does best depends on why the correction happened and what the outlook is. In the rebound, though, the sector difference matters a lot. In fact, it’s interesting that getting the sector right has made a bigger difference than getting the size or style right.

Looking 250 days out instead of 60, you get a slightly different picture. Small and value still win, but there’s more variability around the value premium. In terms of sectors, only 40% of the time does the top sector over 60 days become the top sector over 250 days. That suggests that what works in the early stages of a rebound might not work as well in the later stages, calling for a more active approach to portfolio management.

Where we see opportunities

In the near term, we think investors should consider “getting their beta on.” Beta is just a way of referring to those parts of the market that typically swing the most relative to the broad market. Over the intermediate and long term, we see good opportunities in health care, energy, and information technology (IT).

If a bubble forms before the bull market blows its top, it will probably be in health care. Demographic and regulatory changes may make health care the tech of 1999. It could have a lot of resiliency even if valuations stretch even farther. It seems like the perfect industry for those concerned about an aging demographic. We spend more to live longer. We then need to keep spending more to live better, not just longer. That seems like a cash cow.

Energy kicks off income and now shows great possibilities for growth. Even if energy companies don’t grow revenues very fast, price/earnings can grow fast when earnings prove to be resilient. It takes months and sometimes years for supply to fully respond to price signals. Existing high-cost wells were more high-cost due to the costs of finding them and initially drilling them. Once they are in place, they deplete quickly, but the variable costs of operating them are relatively low compared with the all-in cost of finding them and operating them. As a result, less exploration and rapid well depletion should push prices higher to a level to encourage more exploration. It’s a process, but there are some very good cash-flow-rich companies in the energy sector.

With IT, we can’t help but think companies will keep enhancing efficiencies as they fight tooth and nail to grow market share and protect margins. Not all things called IT are really about enhancing efficiency, though that’s the part of the sector we like.

Don’t narrowly focus on the U.S.

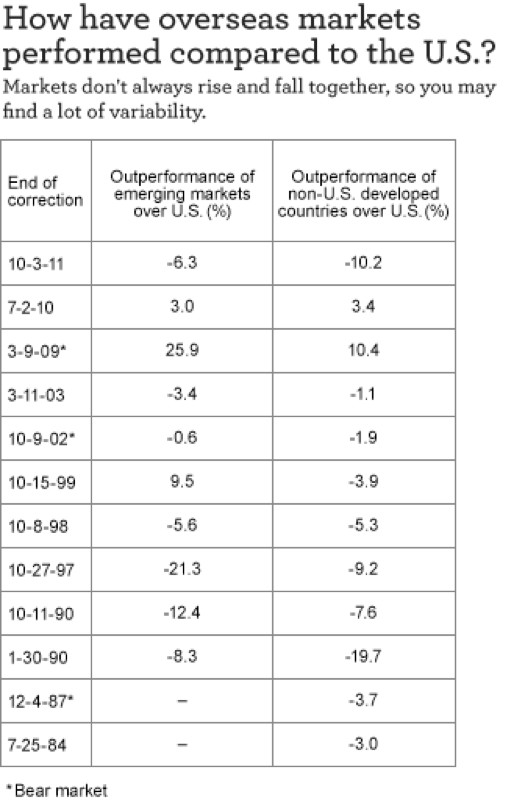

While it’s easy to look at the U.S. markets for opportunities, it’s more important to look globally. There is a lot of variability around whether U.S. markets or non-U.S. markets do better in a rebound. Part of this is because markets don’t always rise and fall together. For example, in 1997, emerging markets got more caught up in the Asian financial crisis than the U.S. did. As another example, the eurozone debt crisis of 2011 more detrimentally affected European markets than U.S. markets. The rebound depends, to a great extent, on the causes of the descent.

Past performance is no guarantee of future results.

Sources: FactSet and authors’ calculations, based on MSCI EM Index (emerging markets), S&P 500 Index (U.S. markets), and MSCI World ex USA Index (non-U.S. developed) subsequent 60 trading days’ returns.

While the U.S. recently experienced a correction (a drop of 10% or more), other parts of the world experienced deeper corrections or have been in a bear market (down 20% or more). Lower prices for stocks, however, aren’t a reason to buy. You need to assess the quality of what you’re buying. You also need to determine whether it is likely that market prices will begin to reflect the quality of what you’re buying in a reasonable time frame. Trying to get the timing exactly correct will leave you twitchy and disappointed. Looking for when things are changing for the better—as they are in Europe—or when they are getting less worse—as in much of the emerging markets—can make this a prime time to diversify your portfolio globally. It might not be the comfortable time, but don’t let a little discomfort dissuade you from taking advantage of opportunities when they present themselves. If you’re waiting for clarity, chances are the market will have moved on well before you get that clarity.

Please visit our blog, AdvantageVoice, for additional viewpoints from Wells Fargo Asset Management’s investment strategists, portfolio managers, and practice management experts. You can also follow us on Twitter at @WFAssetMgmt for real-time updates. Are you an advisor or institutional investor? Check out our website for investment professionals.

The views expressed are as of 9-15-15 and are those of Dr. Brian Jacobsen, CFA, and John Manley, CFA, and Wells Fargo Funds Management, LLC. The information and statistics in this report have been obtained from sources we believe to be reliable but are not guaranteed by us to be accurate or complete. Any and all earnings, projections, and estimates assume certain conditions and industry developments, which are subject to change. The opinions stated are those of the authors and are not intended to be used as investment advice. The views and any forward-looking statements are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally, or any mutual fund. Wells Fargo Funds Management, LLC, disclaims any obligation to publicly update or revise any views expressed or forward-looking statements.

Wells Fargo Funds Management, LLC, a wholly owned subsidiary of Wells Fargo & Company, provides investment advisory and administrative services for Wells Fargo Advantage Funds®. Other affiliates of Wells Fargo & Company provide subadvisory and other services for the funds. The funds are distributed by Wells Fargo Funds Distributor, LLC, Member FINRA, an affiliate of Wells Fargo & Company.

Not FDIC Insured • No Bank Guarantee • May Lose Value

© Wells Fargo Asset Management