Macroeconomics students spend a good bit of class time learning about the Phillips curve, and it is probably etched permanently in their minds. The Phillips curve suggests that there is an inverse relationship between inflation and unemployment in the short run. In practice, the Phillips curve is a conceptual framework that central bankers use to analyze the potential impact of monetary policy actions. In this context, we have been asked on several occasions if the trade-off between inflation and unemployment still exists.

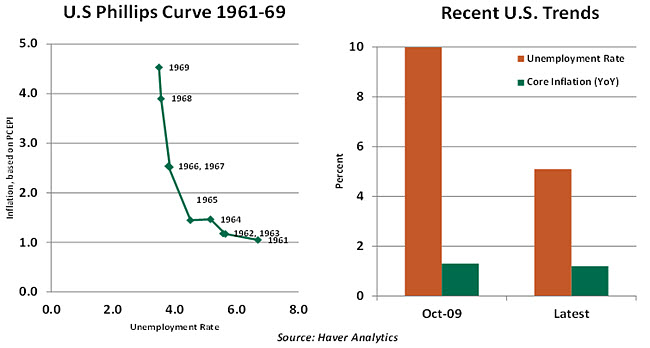

Some history of the Phillips curve is appropriate before examining its relevance today. In 1958, A.W. Phillips showed (based on British data) that years of high unemployment rates tended to coincide with steady or falling wages and vice versa. As wage and price inflation move together, Phillips’ results can be extended to the relationship between inflation and the unemployment rate. Annual U.S. inflation data [based on the personal consumption expenditure price index (PCEPI)] and the unemployment rate for the 1960s illustrate this relationship clearly.

In the 1960s, it was widely believed that policymakers had a menu of different unemployment rates and inflation to choose from when designing policy. It was held that low unemployment could be attained at the cost of some inflation.

But the supposedly stable relationship between unemployment and inflation broke down in the 1970s, when high inflation and high unemployment co-existed. Subsequent research pointed out that inflation expectations play an important role in the process and that monetary policy cannot permanently affect unemployment.

Expansionary monetary policy stimulates aggregate demand in the economy. Firms increase employment to meet rising demand. The short-run trade-off implied by the Phillips curve prevails. But increasing demand will eventually translate into higher prices. It takes time for workers to adjust inflation expectations and demand higher nominal wages to compensate for higher inflation.

As nominal wages increase, production costs escalate, profit margins shrink and firms will cut back on employment. The attempt to increase employment has led to higher prices and no change in employment in the long run. The trade-off between inflation and employment is thus a short-run phenomenon.

Unemployment eventually converges to its natural level (full employment level) determined by structural factors of the economy. In other words, the long-run Phillips curve is a vertical line, representing the absence of a trade-off between inflation and unemployment.

Fast forwarding to the present, it is now broadly recognized that there is a short-run trade-off between inflation and unemployment. The sensitivity of inflation to changes in labor market slack is not fixed over time. The expansionary monetary policy tools of central banks have a limited potential to increase employment. Therefore, they choose to target inflation.

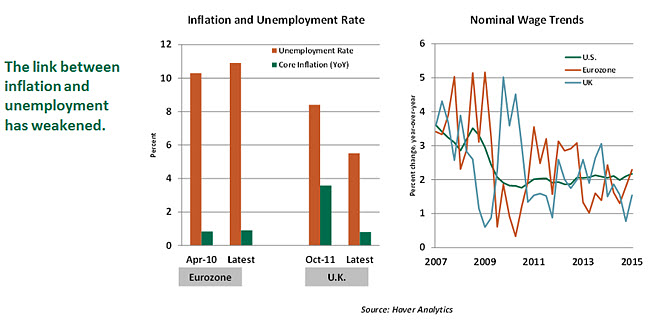

Following the Great Recession, unemployment reached elevated levels in the United States, United Kingdom and the eurozone. The U.S. unemployment rate stands at 5.1% now, down from a high of 10% in October 2009. But core inflation (as measured by the PCEPI excluding food and energy) is 1.2% over the past 12 months, compared with a 1.7% reading in October 2009. A similar situation prevails in the United Kingdom; but the eurozone is at a different place in the business cycle. Also, nominal wages have failed to accelerate despite low jobless rates in both the United States and United Kingdom.

Several reasons are cited for the weak link between slack in the labor market and inflation. First, inflation expectations have changed. Following the inflationary experience of the 1970s and 1980s, studies showed that the Phillips curve was steep largely because inflationary expectations were tied to this experience. The contained inflation experience of the 1990s lowered inflation expectations in most major economies.

Second, the tough inflation experience prodded central bankers to adopt a new monetary policy approach. Central banks have cultivated an image as inflation fighters in the past 25 years. Several adopted formal inflation targets and promoted transparency of monetary policy. Research at the International Monetary Fund (IMF) indicates that the new approach of central bankers has played an important role in changing inflation dynamics across several economies. The increased anchoring of inflation expectations to central bank targets renders inflation less sensitive to economic activity.

Third, Fed Chair Janet Yellen has noted that there is resistance to nominal wage reductions, which is consistent with a weakened relationship between inflation and the unemployment rate. During the Great Recession, wages did not fall in line with the sharp declines in the unemployment rate. The “pent-up wage deflation” has resulted in subdued gains as the labor market has tightened, which in turn has helped to hold down inflation.  Fourth, cross-country evidence shows that firms change prices less frequently when inflation is low, as there are costs associated with adjusting nominal prices. Firms adjust prices more frequently when the average rate of inflation increases in order to keep up with it. As a result, in a low-inflation environment, the inflation and unemployment link will be different.

Fourth, cross-country evidence shows that firms change prices less frequently when inflation is low, as there are costs associated with adjusting nominal prices. Firms adjust prices more frequently when the average rate of inflation increases in order to keep up with it. As a result, in a low-inflation environment, the inflation and unemployment link will be different.

Fifth, the size and duration of economic slack has an important bearing on how sensitive inflation is to the labor market situation. During the upswing of a business cycle, additional demand translates into price more rapidly than during early stages of a business expansion, when there is more unused capacity.

Central bankers will need to consider these factors when calibrating monetary policy. Monetary policy is perhaps more effective in increasing employment. The Phillips curve has flaws, but until a better paradigm is invented to analyze the dynamics of inflation and monetary policy, it will remain an important part of the central banker’s tool kit.

Will Japan Go Back to the Well?

Everything seemed to be going according to plan in Japan just a quarter ago. Domestic demand appeared to be on the road to recovery, export growth was solid, the Trans-Pacific Partnership seemed within reach and Prime Minister Shinzo Abe seemed invincible.

Fast forward a few months, and Japan’s latest economic experiment seems to have gone off the rails, hindered heavily by the slowdown in China. The economy is contracting, and the promise of 2% inflation seems hollow. It is becoming harder to envision the project succeeding without consumer demand returning to levels last seen after last year’s consumption tax increase. But corporations are hesitant to use some of their accumulated cash for significant capital expenditure and wage increases.

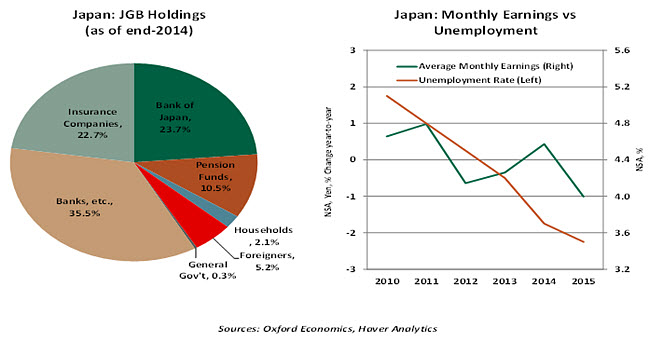

As it has been from the beginning, the responsibility for maintaining Abe’s economic experiment will fall to the Bank of Japan (BOJ). The central bank’s massive qualitative and quantitative easing (QQE) program currently sets asset buying at an annual target rate of ¥80 trillion per year. As expected, this has led to a massive expansion of the banks sovereign bond holdings: as of end-2014, the bank held 23.7% of all Japanese government bonds, up from 12% two years earlier. With the economy back in the doldrums, there is speculation that the program will be expanded at some point this year.  Ever the optimist, Governor Haruhiko Kuroda publicly claims that there is no imperative to add to QQE. Yet his conviction that the tight labor market will eventually force wage increases, which will in turn break the deflationary cycle, is becoming harder to believe. The economy is at or near full employment by any standard, yet wage growth and summer bonuses have been disappointing. Without his virtuous cycle and with oil prices nowhere near the $70-$75 per barrel that BOJ forecasts are based upon, hopes of achieving 2% inflation by 2017 are starting to appear like a fantasy.

Ever the optimist, Governor Haruhiko Kuroda publicly claims that there is no imperative to add to QQE. Yet his conviction that the tight labor market will eventually force wage increases, which will in turn break the deflationary cycle, is becoming harder to believe. The economy is at or near full employment by any standard, yet wage growth and summer bonuses have been disappointing. Without his virtuous cycle and with oil prices nowhere near the $70-$75 per barrel that BOJ forecasts are based upon, hopes of achieving 2% inflation by 2017 are starting to appear like a fantasy.

As the inflation target moves further away from realization, there is a chance that the BOJ will add to QQE, possibly when it releases a new economic forecast at the end of October. Kuroda’s optimism about the virtuous cycle may not prove to be an obstacle, since he was also publicly bubbly about economic prospects before last year’s surprise QQE increase.

However, the constraining factor that did not exist last year is the already-weak yen. The BOJ currently believes the yen should settle into equilibrium in the ¥120-125/$US level. An additional injection of monetary stimulus will almost certainly weaken the currency well past this range at a time when the benefits from rapid depreciation have largely been realized.

The BOJ should not expect much help on the fiscal front. A small supplementary budget may be on offer, but large-scale stimulus is not likely. The most the government is offering is a possible delay of the second phase of the consumption tax increase, currently scheduled to take effect in April 2017, and a highly unpopular 2% rebate on essential purchases.

At least the Prime Minister can rightfully claim some successes on the third arrow. However, the government has been frustratingly slow on the measures that are most important to ensuring the country’s economic future – immigration and labor market reform.

The Japanese economy could well enter into technical recession (again) this year, but this does not mean the Abenomics project is doomed. The headwinds are undeniable, but one would be hard-pressed to find an economy, especially within APAC, that has not struggled with growth and weak inflation in the wake of China’s woes and low oil prices. The BOJ’s policy path is uncertain as the benefits of additional QQE appear limited, but this does not mean that the bank will not continue to press ahead with the effort.

Greece Enjoys Calm Before Reform

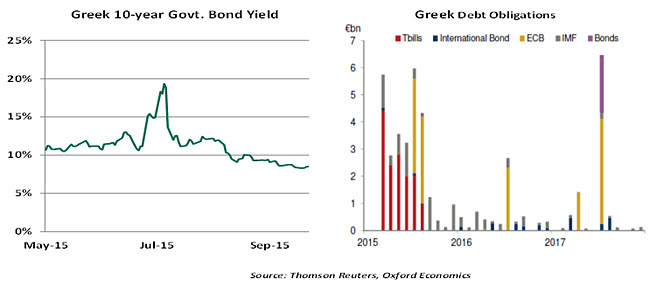

Last weekend’s snap parliamentary election in Greece confirmed Prime Minister Alex Tsipras as the dominant player in the country’s political system. His Syriza party was re-elected with about the same share of the vote as in the January election. The radical left group that split from his party did not do well enough to claim any parliamentary seats, and the various opposition parties performed relatively poorly. Tsipras has reformed the previous coalition with a smaller right-wing party and installed a mostly unchanged Cabinet. Markets treated the news with relief. While the vote may seem to have marked the end of the summer of crisis, it was really just one step in an ongoing process of negotiation with Athens’ European partners – a process in which periodic clashes are still likely.  The government must now get back to the task of tackling the country’s myriad economic and policy challenges. Tsipras should find this somewhat easier, with the radical left opponents of austerity mostly out of parliament. But the tight deadlines in the ongoing reform program remain daunting. Near-term challenges include recapitalizing the banks and implementing further pension and labor market reforms. Longer-term issues such as the fight against corruption and vested interests will take years to tackle.

The government must now get back to the task of tackling the country’s myriad economic and policy challenges. Tsipras should find this somewhat easier, with the radical left opponents of austerity mostly out of parliament. But the tight deadlines in the ongoing reform program remain daunting. Near-term challenges include recapitalizing the banks and implementing further pension and labor market reforms. Longer-term issues such as the fight against corruption and vested interests will take years to tackle.

Next month will see the first review of progress on the measures demanded as part of the €86 billion bailout package agreed with creditors in July. If the review goes smoothly, then the creditors will start to discuss some form of debt relief – likely an easing of debt-service terms. If the IMF feels this is enough to make the country’s debt burden sustainable, then the fund will be willing to contribute to financing the package. However, it is not at all clear that spreading out the repayment terms still further will make a meaningful difference to the debt-service burden. And without IMF involvement, Germany and others may start to balk at the long-term cost of support for Greece.

With Greece’s membership in the eurozone apparently settled for now, and with the ongoing European refugee crisis grabbing all the headlines, the markets probably will not pay as much attention to the talks on debt relief. But there remains a risk that yet another round of Grexit woes will return sometime in the coming year.

(c) Northern Trust