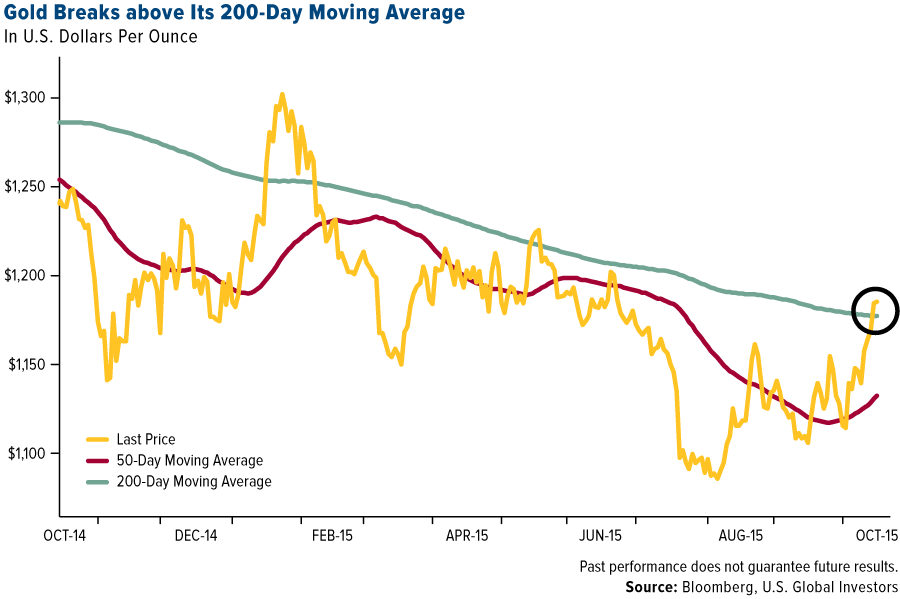

After its stellar performance this week, gold might do something it hasn’t done since 2012—that is, end the year in positive territory. You can see past returns for yourself in our perennially popular Periodic Table of Commodities Return.

Responding to a weaker U.S. dollar, continued contraction in global growth and wide speculation that interest rates will stay near-zero for the remainder of the year, the yellow metal broke above its 200-day moving average and is close to erasing its 2015 losses.

This could be the price reversal many gold bulls have been expecting.

Back in August I shared with you that legendary hedge fund manager Stanley Druckenmiller, who’s made some mythic calls over his long career, invested $323 million of his own money in gold, now the largest position in his family funds. Although such a large weighting isn’t appropriate for all investors—I’ve always recommended 10 percent in gold: 5 percent in gold stocks, 5 percent in bullion—it looks as if Druckenmiller made another good call.

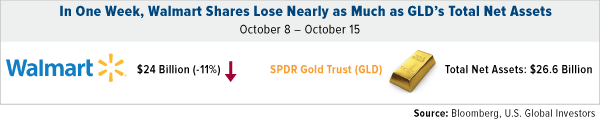

The big news this week is that Walmart took a massive hit after the retail giant said it expected a profit slump in 2016. Walmart investors lost a whopping $24 billion—$21 billion on Wednesday alone. While this news dominated the headlines, it’s important to recognize that the total amount of net assets in the SPDR Gold Trust, the world’s largest gold-backed ETF, is just slightly more than Walmart’s one-week loss.

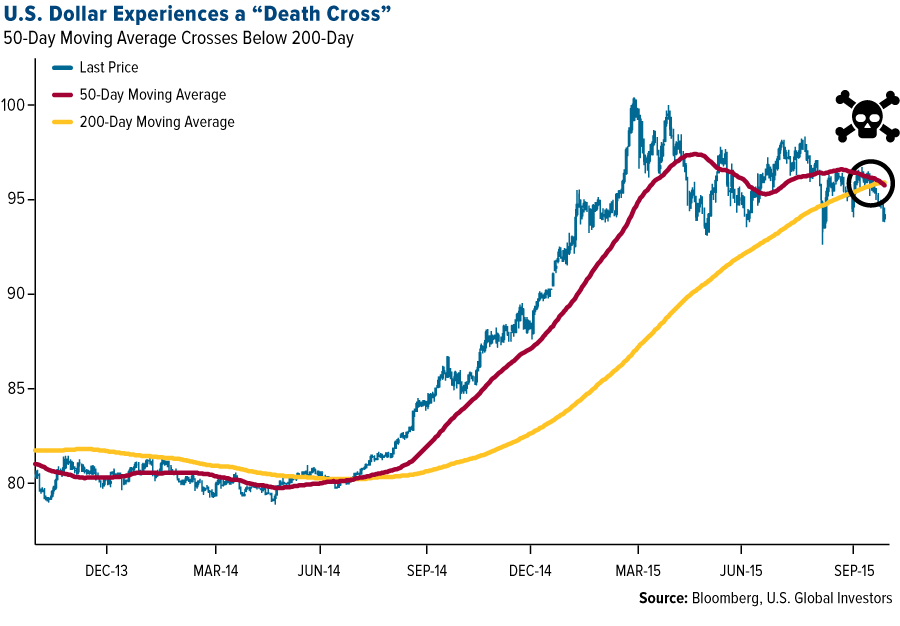

“Death” of the Dollar?

It’s no mere coincidence that gold’s breakout coincides with the weakening of the U.S. dollar this week. The greenback signaled what’s known as a “death cross,” just in time for Halloween. Widely recognized as the start of a bearish trend, a death cross occurs when the 50-day moving average crosses below the 200-day.

This hasn’t happened since September 2013.

As ominous as this sounds, it’s good news for gold and other metals and commodities, not to mention emerging markets and American exports. For the past year, the strong dollar has crushed these assets, something I write and speak about frequently. If the death cross does indeed indicate the start of a downward trend, gold might have the breathing room it needs to reach the important $1,200 resistance level.

Our China Region Fund (USCOX) and Emerging Europe Fund (EUROX) have responded well to the dollar’s drop, both of them crossing above their 50-day moving averages.

When we factor in the Love Trade, gold has even further upside potential. In India, the world’s largest consumer of the precious metal, the annual wedding and fall festival season has officially begun, which has historically triggered a spike in demand. This period is followed by Christmas and the Chinese New Year in February, when gold prices have surged, based on the shorter-term, five-year pattern.

Russian Air Strikes Ignite the Fear Trade

In a recent piece titled “The New Cold War Battlefield… and How It Will Affect Oil Prices,” Dr. Kent Moors, global energy strategist for “Oil & Energy Investor,” writes that what happens in the Middle East has “always had a rather direct impact on energy prices and the prospects for investing in the sector.”

|

The difference today, Moors says, is that Syria “is a rising power vacuum right smack in the middle of the largest concentration of global crude production.”

This is a theme that’s explored in even further detail in my friend Marin Katusa’s bestselling book, “The Colder War: How the Global Energy Trade Slipped from America’s Gasp.”

Speaking of Marin, his Katusa Research and Cambridge House International will be co-producing the Silver Summit and Resource Expo in San Francisco November 23 and 24. I’ll be giving the opening keynote address. If you’d like to attend the conference as my guest, send me an email for a complimentary registration.

Real Interest Rates, Real Impact on Gold

The Fear Trade also includes monetary and fiscal policies such as money supply and real interest rates. As opposed to geopolitical events, which might have an immediate effect on gold, these drivers can have a long-term influence.

As a reminder, real interest rates are what you get when you deduct the rate of inflation from the 10-year Treasury yield. For example, if Treasury yields were at 2 percent and inflation was at 2 percent, you wouldn’t really be earning anything. But if inflation was at 3 percent, you’d be experiencing a negative real rate.

When gold hit its all-time high of $1,900 per ounce in August 2011, real interest rates were sitting at -3 percent. In other words, if you bought the 10-year, you essentially lost 3 percent a year on your “safe” Treasury investment. Since gold doesn’t cost anything to hold, it became more attractive and the metal’s price soared.

Today, the U.S. has virtually no inflation, so real interest rates are at 2 percent, a swing of 500 basis points since August 2011. This has lately had a negative effect on gold, which means it’s even more remarkable that the precious metal has broken above its 200-day moving average.

Our office was visited this week by Barry Bannister, CFA, the chief equity strategist for investment firm Stifel, who gave us buckets of useful macroeconomic research, much of which validated what we’ve been saying for a long time regarding the relationship between the price of gold and real interest rates.

Barry made the case that real interest rates are even higher than we realize. He argued that the reason the Federal Reserve hasn’t allowed rates to lift off yet is because—you might want to sit down for this—it already has, in an “invisible” interest rate hike of 4 percent. Quantitative easing (QE), Barry said, was “negative” interest rates, and that “economic recovery and time ‘raised’ rates to 0 percent, a de factorate hike.”

Gold’s rally this week occurred in spite of this “invisible” rate hike.

Active Management on Top

Even with gold prices off around 38 percent since the August 2011 high, our Gold and Precious Metals Fund (USERX) has done well, outperforming the Market Vectors Gold Miners ETF (GDX) and PowerShares Global Gold & Precious Metals ETF (PSAU).

Speaking to Investor’s Business Daily, portfolio manager Ralph Aldis pointed out that one of the reasons why our fund has outperformed is because we’re able to apply our tacit knowledge of company executives and management teams, as well as anticipate and act on political risks in countries we invest in. This is a skill (and benefit) that only active management can provide.

Both the GDX and the PSAU are strictly market capitalization-weighted, so they might miss out on unexpected “success stories.”

“They end up owning the biggest companies, which because of their size have difficulty growing,” Ralph told IBD.

Klondex Mines is one such success story. It’s the fund’s top weighting, at 17 percent—and yet because of its market-cap, it isn’t included at all in the two ETFs.

As Ralph told The Gold Report this week, “I want to own companies where management can increase the value proposition,” regardless of gold prices.

To end, I’d like to congratulate the U.S. Global communications team for receiving five STAR awards from the Mutual Fund Education Alliance last night for excellence in investor education. Please help me applaud the team’s efforts and your commitment to being a curious and informed investor by sharing our award-winning communications with your friends, family and colleagues.

Thanks you for being a subscriber to our award-winning communications!

P.S. It’s with sadness to say that I just learned of the passing of Raymond Edward “Ed” Flood. Ed spent his whole life and career in the mining industry, serving most recently as the CEO of Concordia Resource Corp. Our paths crossed many times over the years, and I came to know him as not only a talented money manager but also a great human being. I join everyone else who knew him, both personally and professionally, when I say that he’ll be sorely missed.

Index Summary

- The major market indices finished positive this week. The Dow Jones Industrial Average gained 0.77 percent. The S&P 500 Stock Index rose 0.90 percent, while the Nasdaq Composite climbed 1.16 percent. The Russell 2000 small capitalization index lost 0.26 percent this week.

- The Hang Seng Composite gained 2.56 percent this week; while Taiwan was up 1.88 percent and the KOSPI rose 0.53 percent.

- The 10-year Treasury bond yield fell 6 basis points to 2.03 percent.

Domestic Equity Market

Strengths

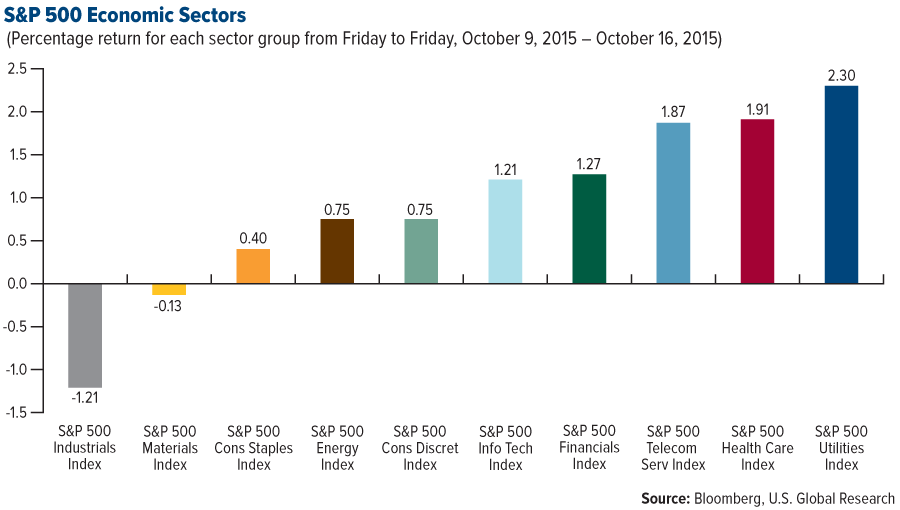

- Utilities was the best performing sector on a relative basis, up 2.30 percent for the week versus a 0.90 percent gain for the S&P 500.

- The health care, telecommunications, financials and information technology sectors all beat the S&P 500 Index, returning 1.91 percent, 1.87 percent, 1.27 percent, and 1.21 percent, respectively.

- TripAdvisor was the best performing stock in the S&P 500, up 22.39 percent after announcing a deal with Priceline, which would merge the online travel company’s catalog of hotels with TripAdvisor’s popular booking system.

Weaknesses

- The industrials sector had a tough week, ending as the worst performer with a return of -1.21 percent, due in part to the profit-taking seen after the substantial gain that occurred during recent weeks.

- Consumer discretionary, energy, consumer staples and materials also lagged the S&P 500, all returning below the S&P 500’s performance of 0.90 percent.

- The worst performing stock in the S&P 500 was Quanta Services, which fell 29.31 percent after the company warned that third-quarter results wouldn't be as strong as expected.

Opportunities

- The consumer staples sector is in a stealth relative performance uptrend which is likely to continue. The latest retail sales report was a disappointment. Sales at non-cyclical stores are growing faster than overall retail sales, consistent with a slowing economy, which boosts the relative profit allure of the defensive consumer staples sector. Nonetheless selectivity is necessary as the grocery and beverage industries have been able to raise selling prices, while the retail drug store and packaged food industries are cutting prices. Profits are likely to follow pricing power trends.

- Household product stocks are playing catch up to other consumer products groups, and the dip in the U.S. dollar provides a catalyst for gains. The household products group has relied on developing countries as a key source of growth. As a result, sales have taken a hit. However, U.S. exports of cosmetics and toiletries have reaccelerated in recent months, which may be an early indication of a turnaround. Asian retail sales have held up well. Importantly, disposable income has been freed up by the dramatic plunge in energy costs. Given that household products are a small ticket purchase, the odds of consumers trading up into higher margin brand names increase as discretionary spending firms. Against a backdrop of lower commodity prices, depressed profit margins have room to expand, as they have in the past.

- Share price stabilization for the energy services sub-sector is possible on evidence of a credible decline in oil output, which is necessary to rebalance the market. Share prices have rallied hard since the market began re-pricing a more benign Fed rate hike cycle, which took the U.S. dollar off its highs. If this trend persists, particularly against emerging markets, then the odds of a durable trough in energy services relative performance have increased.

Threats

- According to BCA, managed care stocks are poised to roll over. This is because medical services are at a disadvantage when overall consumer spending on health care accelerates. Further, the risk of profit margin pressure is likely to intensify. Leading employment indicators have softened, suggesting that membership growth may have passed its peak. Lastly, the relentless surge in key costs such as pharmaceuticals suggest further profit risks.

- The latest NFIB survey of the small business sector suggests that small businesses may come under intense margin pressure. Companies are facing an unfavorable combination of soaring labor quality concerns and rising compensation expectations along with a sagging sales outlook amidst intensification in deflation pressures. Further, planned price hikes are heading towards their lowest level in years. Historically, small caps underperform large caps when overall profit margins narrow. Thus, a large cap bias may be warranted.

- Chemical stocks have been crushed this year and are overdue for relief. However, that would likely be a chance to sell rather than an opportunity to bottom fish. One of the main issues for the industry has been an inability to adjust to slumping global manufacturing activity. Chemicals industrial production has been growing robustly for more than a year even though shipments of chemicals have contracted during this time. The resulting growth in inventories has pushed pricing power into the deflation zone. Further, chemical companies continue to add employees, representing another pressure point for profit margins. Unless these imbalances are corrected, chemical stocks are likely to remain under pressure.

The Economy and Bond Market

Lackluster economic data led to a rebound in global stocks, as investors expect central banks to extend their accommodative policies. Early U.S. corporate profit reports were mixed, though large banks performed well overall. Crude oil prices eased, trading around $46 and $50 per barrel on Friday for U.S. West Texas Intermediate and Brent, respectively. The yield on the 10-year U.S. Treasury note hovered near 2.0 percent.

Strengths

- Consumer sentiment rebounded to 92.1 in the preliminary October release from 87.2 in September, suggesting an upbeat consumer and perhaps dispelling some of the pessimism in markets around the U.S. outlook. This beat expectations of a smaller improvement to 89.0. Both the current conditions and expectations indices saw nice gains, with the former jumping to 106.7 from 101.2 and the latter rising to 82.7 from 78.2.

- After a recent run of disappointing data, core CPI came in a tenth above forecasts, rising 0.2 percent in September. Meanwhile, headline CPI fell 0.2 percent month-over-month, which was as expected. These changes resulted in unchanged annual growth for headline, down from 0.2 percent year-over-year in August, while core inflation inched up a tenth to 1.9 percent from 1.8 percent, the highest reading since July 2014. While these developments are encouraging, inflation still remains muted overall, and the continued disinflationary pressures from the stronger dollar and a slowing global backdrop are notable downside risks.

- Initial jobless claims were reported at 255,000 for the week ending October 10, down from 262,000 in the prior week. This is below the expected 270,000. This report moves the four-week moving average down to 265,000 from 267,250, representing the lowest level since late 1973.

Weaknesses

- Producer price index (PPI) final demand declined 0.5 percent month-over-month in September, down from 0.0 percent month-over-month in August and below the expected 0.2 percent month-over-month decline. This translates to a 1.1 percent year-over-year decline, down from a 0.8 percent year-over-year decline in the prior month and below the expected 0.8 percent year-over-year decline. Core PPI, PPI excluding food and energy, declined 0.3 percent month-over-month, down from a 0.3 percent month-over-month increase in August and well below the expected 0.1 percent month-over-month gain. This translates to a 0.8 percent year-over-year gain, down from 0.9 percent year-over-year in the prior month and below the expected 1.2 percent year-over-year gain.

- Industrial production contracted 0.2 percent month-over-month in September, which was the eighth monthly decline in nine months this year. The Empire Manufacturing Index increased to -11.36 in October from -14.67 in September. This is still below the expected -8.00. The ISM Adjusted Index declined to 44.8, still below the 50-breakeven level, showing a modest deterioration in the components. The Philadelphia Fed Business Outlook Index improved to -4.5 in October from -6.0 in September. This is below the expected -2.0. On an ISM-Adjusted basis, the index declined to 44.7 from 51.0, falling below the 50-breakeven level.

- Retail sales data were disappointing for September. Retail sales added only 0.1 percent month-over-month in September, up slightly from a downwardly revised 0.0 percent in August (revised down from 0.2 percent month-over-month). This was below the expected 0.2 percent.

Opportunities

- The housing market has been one area of the U.S. economy that has been relatively resilient. The homebuilder's sentiment survey on Monday and housing starts on Tuesday should help determine if the housing market can stay robust.

- The European Central Bank announces its monetary policy next Thursday. There is wide anticipation for an extension or increase of monetary stimulus.

- Municipal bond yields held steady this week as both the supply and demand side decreased in the Columbus Day holiday-shortened trading week. Net issuance is expected to remain negative for the rest of the year, which should be supportive of market technicals.

Threats

- Treasury yields are not cheap at current levels, but they are unlikely to rise above current forward rates given the current depressed global economic backdrop and persistent strength of the U.S. dollar. According to BCA, a much lower projected path of the funds rate is very much a product of the strong U.S. dollar, which is acting as a drag on growth via net exports and on corporate profits via a massive reduction in pricing power. The other piece of the valuation puzzle, the term premium, is likely to stay depressed given the surge in global excess savings that is finding its way into U.S. Treasuries. That, combined with the steady downward pressure on global bond risk premiums due to the QE programs in Europe and Japan, is likely to keep U.S. Treasuries expensive.

- China is at the center of the emerging markets slowdown and recent data, while not uniformly negative, has failed to assuage fears that the economic momentum will continue to deteriorate. China will release GDP figures for the third quarter on Monday.

- S&P operating margins excluding the energy and financial sectors are indeed still edging higher, but this is unlikely to persist. Even outside of energy and materials, earnings-per-share growth is negative or low single digits in six out of eight sectors (despite share buybacks). It is the same story for sales per share. A key problem is that pricing power is eroding across most sectors. The bottom line is that weak U.S. top- and bottom-line growth are not just an energy and materials story. As a result, profit margins are likely to see a broad-based downtrend in the coming months.

For the week, spot gold closed at $1,175.48, up $18.20 per ounce, or 1.57 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, rose 1.72 percent. Junior miners underperformed the seniors for the week as the S&P/TSX Venture Index gained just 0.73 percent. The U.S. Trade-Weighted Dollar Index slid 0.08 percent for the week.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Oct -13 | GE CPI YoY | 0.00% | 0.00% | 0.00% |

| Oct -13 | GE ZEW Survey Current Situation | 64 | 55.2 | 67.5 |

| Oct -13 | GE ZEW Survey Expectations | 6.5 | 1.9 | 12.1 |

| Oct -14 | US PPI Final Demand YoY | -0.80% | -1.10% | -0.80% |

| Oct -15 | US Initial Jobless Claims | 270K | 255K | 263K |

| Oct -15 | US CPI YoY | -0.10% | 0.00% | 0.20% |

| Oct -16 | EC CPI Core YoY | 0.90% | 0.90% | 0.90% |

| Oct -18 | CH Retail Sales YoY | 10.80% | -- | 10.80% |

| Oct -20 | US Housing Starts | 1147K | -- | 1126K |

| Oct -22 | EC ECB Main Refinancing Rate | 0.05% | -- | 0.05% |

| Oct -22 | US Initial Jobless Claims | 265K | -- | 255K |

Strengths

- Platinum was again the best performing precious metal, rising 3.31 percent for the week. Platinum historically has traded at a premium to gold, so perhaps there is still further room to go.

- Gold is beginning to shed its reputation as a dead asset thanks to the string of lukewarm economic reports in recent weeks. As a result, there is speculation that the Federal Reserve probably missed its window to hike in 2015. Gold has now managed to rise above the technically important 200-day moving average for the first time in five months. Furthermore, the world’s largest gold ETF recorded its highest daily inflow since early February with an addition of 7.7 tonnes. The gold price, which typically trades inverse to the U.S. dollar, may have some real room to run as the recent dollar weakness has put in a “death cross,” with its 50-day moving average price plunging beneath its 200-day average price.

- Australia and New Zealand Banking Group said it expects gold to reach the bottom of the recent range in the next couple of months. It said its physical demand barometer for China rose to a 2-year high in September, suggesting demand before Golden Week is very strong. The group expects sharp increases in China’s gold imports in September. Lastly, its forecast for the fourth quarter is $1,110 per ounce.

Weaknesses

- Palladium was the worst-performing precious metal, falling 2.06 percent on the unwinding of speculative trades that had shorted platinum to go long palladium. Silver only gained 1.41 percent this past week, slightly underperforming gold.

- Mitsui and Co., Japan’s second-biggest trading house with involvement in the precious metals dating back to the 1970s, said it will pull out of overseas precious metals trading after evaluating the profitability of the business. The company will keep its business in Japan. According to the company, this decision had nothing to do with the naming of the company by Swiss authorities as one of six involved in the manipulation of gold price fixing in London.

- Third-quarter revenues for the S&P 500 Index are projected to fall 3.3 percent from the third quarter of last year, following a 3.3 percent decline in the second quarter and a 2.8 percent drop in the first quarter, according to FactSet. Fourth-quarter revenues are projected to decline 1.6 percent. The last time revenues ran four negative quarters in a row was during the 2008-2009 Great Recession.

Opportunities

- According to Elliott Management’s Paul Singer, gold is under-owned and should be part of every investment portfolio to the tune of 5 to 10 percent. At the SOHN Investment Conference in Tel Aviv, Singer criticized monetary policymakers, calling them the “cult of central banking” in which investors turn to regulators such as Janet Yellen to solve the ills of the global financial system. He also said the supply of gold cannot be radically expanded in a short period of time, which paints a good demand/supply imbalance. Furthermore, bullion looks extended as it has posted five consecutive quarterly losses, the longest run of declines since 1997.

- According to DBS Group Holdings, the Fed will raise U.S. rates only gradually, and the cycle will peak at a lower level than earlier rounds. They interpret this change to allow gold some room to run when the market comes to realize the new paradigm.

- Haywood Securities has initiated coverage on Fortuna Silver Mines with an outperform rating and a $4.50 target price. They highlight the company’s stable operating platform with fully-funded organic growth potential, industry leading margins that are set to improve as expansion plans unfold, balance sheet strength and a valuation that provides a compelling entry point.

Threats

- Natixis sees gold prices averaging $990 an ounce in 2016 on expectations of higher U.S. interest rates and strength in the U.S. dollar.

- According to a report by Goldman Sachs, BHP Billiton’s and Rio Tinto’s net asset bases are three times higher than they were a decade ago, yet they are not as productive. Much of the capex invested in the super-cycle was subject to major inflationary pressures. Thus, the bank contends that book values are overstated relative to production levels.

- According to Cornerstone Macro, there is no consensus on what to do inside the Federal Open Market Committee. While Chair Yellen has touted the Phillips curve on various occasions, both Daniel Tarullo and Lael Brainard have dismissed it, sending mixed signals. This internal disconnect in a coherent message could cause market participants to lose faith in the Fed. Such a loss of confidence would disrupt market prices.Global Resources Fund - PSPFX

Energy and Natural Resources Market

Strengths

- Gold stocks continued to build on last week’s gains due in part to both a lower U.S. dollar and stronger emerging market currencies. The NYSE Arca Gold Miners Index jumped an amazing 4.9 percent during the week.

- Utility stocks pushed higher on the combination of a delayed rate hike by the Federal Reserve and the outperformance of bond proxies. The S&P 500 Utilities Index increased 2.5 percent during the week.

- Iron and steel equities improved as investor sentiment across the entire alloy metals complex rose. The Bloomberg World Iron/Steel index gained 1.5 percent over five days.

Weaknesses

- Base metals stocks trailed due in part to the profit taking seen after the substantial gain that occurred during recent weeks. The S&P/TSX Capped Metals & Mining Index weakened by 8.1 percent this week.

- Construction and engineering lagged most resource sectors following disappointing earnings and negative market commentary by Schlumberger, the world’s leading oil services provider. The S&P 500 Supercomposite Construction & Engineering Index fell 7.8 percent this week.

- Construction materials suffered as capital was redirected to emerging market resource equities. The S&P 500 Supercomposite Construction Materials Index fell 6.5 percent over the prior five days.

Opportunities

- We are seeing a supportive forecast for crude oil pricing next year, as OPEC stated in its monthly report that U.S. oil production is projected to decrease in 2016 for the first time in eight years. Total output of crude and natural gas liquids is estimated to fall 0.5 percent to 12.47 million barrels a day.

- China is expected to release its crude oil import estimate for September next week. If recent trends hold, this could be supportive for pricing, which would offset already high global inventories.

- According to Bloomberg surveys, next week’s housing starts number is expected to increase by 1.6 percent, which could be constructive for lumber prices.

Threats

- Schlumberger, the world’s largest oilfield services provider, reported earnings for the third quarter that fell 49 percent from a year ago, amid declining oil prices and lower spending within the oil patch. The company also warned that a recovery may not materialize until next year.

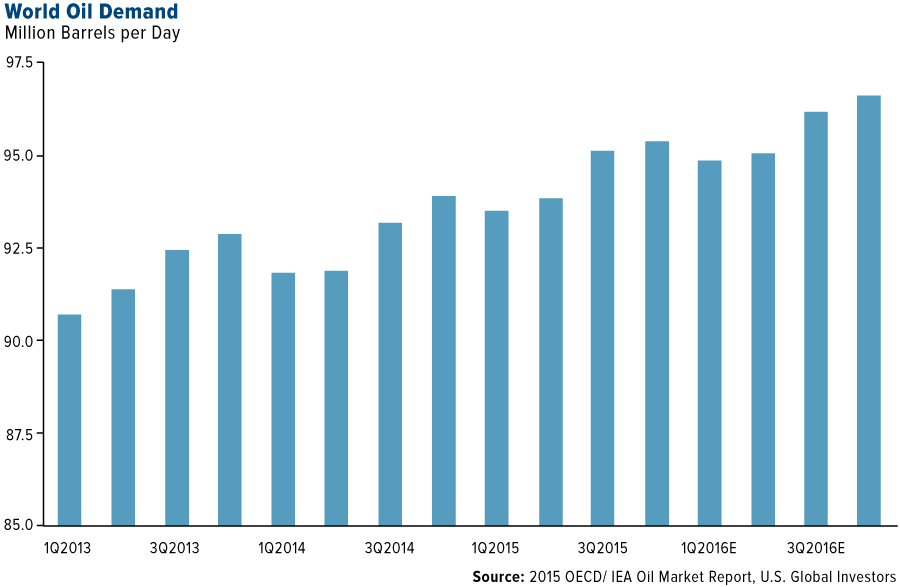

- According to the International Energy Agency (IEA) global oil demand growth is expected to slow from its five-year high of 1.8 million barrels per day (bpd) in 2015 to 1.2 million bpd in 2016, closer toward its long-term trend.

- Iron ore prices may remain depressed for some time as Rio Tinto, one of the world’s lowest cost producers, reported shipped iron ore volumes for the third quarter that increased by 11 percent to 85.6 metric tons, further saturating global supply.

China Region

Strengths

- The China A-Share market was the best performing market in the region this week, driven by better than expected September exports and new bank loans. Investors remained hopeful ahead of the October 26-29 Fifth Party Plenum, anticipating progress on state owned enterprise reform and the next Five Year Plan. The Shanghai Composite Index was up 6.34 percent for the week.

- Industrials was the best performing sector in the region this week, reflecting the ongoing global sector rotation from leaders to laggards. The MSCI Asia Pacific ex Japan Industrials Index rose 2.32 percent for the week.

- The South Korean won was the best performing currency this week, realizing a 1.37 percent gain, due in part to the Bank of Korea’s decision to maintain interest rates at a record-low 1.5 percent rather than implementing further easing.

Weaknesses

- Indonesia was the worst performing market in the region this week, as both the Indonesian rupiah and crude oil prices pulled back from their recent surges. The Jakarta Composite Index was down 1.99 percent for the week.

- Health care was the worst performing sector in the region this week, as defensive sectors underperformed relative to cyclical sectors in the ongoing countertrend rally. The MSCI Asia Pacific ex Japan Healthcare index fell 0.78 percent for the week.

- The Malaysian Ringgit was the worst performing currency in the region this week, losing 0.95 percent, due in part to both political uncertainties and renewed downward pressure on crude oil prices.

Opportunities

- The recent pauses in Chinese sportswear makers should be viewed by long term investors as buying opportunities, as rising health consciousness and sports participation among the country’s middle class frustrated by environmental pollution and food safety remain a robust, visible, and sustainable trend. According to Morgan Stanley research, the share of Chinese population aged 6 to 69 who exercise at least three times a week has increased to 31.2 percent in 2014 from 28.2 percent in 2007, but still below global average and trailing the vast majority of developed economies.

- Indonesia’s government may announce a fourth round of stimulus as early as next week and policymakers are expected to keep borrowing costs at 7.50 percent, according to 25 economists in a Bloomberg survey. With market expectations for the Fed rate hike in 2015 diminishing, Indonesia now has more flexibility in regards to the implementation of economic policy packages.

- Korean regulators’ recent announcement to increase premium rates for foreign and domestic luxury autos effective January 2016 is expected to bring a meaningful earnings increase for the country’s property & casualty insurance industry and extend the underwriting cycle recovery further into the future.

Threats

- While moderating from August’s $154.2 billion, capital outflow from China remained significant at 103.6 billion in September, approximated by detracting trade balance from the change in foreign exchange reserve. Next week’s data release might show China's GDP growth falling below 7 percent year-over-year in the third quarter for the first time since the global financial crisis, a humbling reality check for overly bullish macro investors who expect a swift turnaround of Chinese economic activity.

- The sharp rally of Macau casino stocks might be unjustified, given the significant deceleration of mainland Chinese tourist arrivals in Macau to 7 percent year-over-year during this past National Day holiday week, from 17 percent for the same period last year. While mass market gaming revenue might have stabilized and cost cutting might help increase profit margins, revenue from VIP customers still faces challenges in an industry whose valuation is not yet attractive.

Emerging Europe

Strengths

- Greece was the best performing market this week, gaining 1.3 percent. The biggest profits were noted in banks, on average banks gained 12.4 percent. Prime Minister Alexis Tsipras is pushing for the completion of the bank recapitalization process by the end of this year.

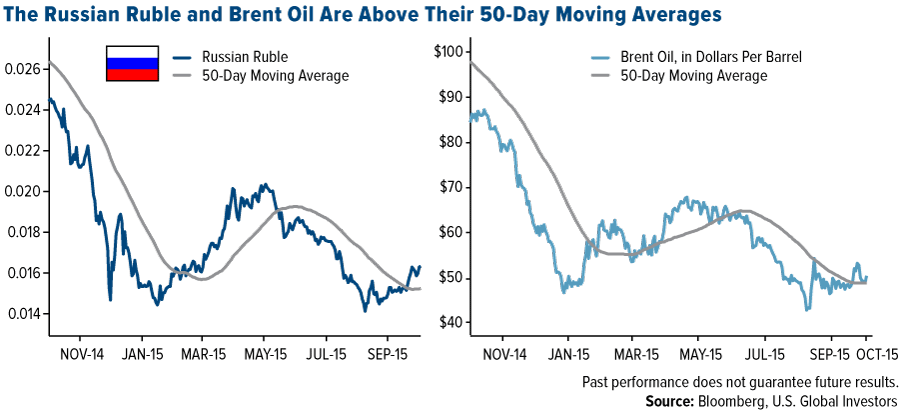

- The Russian ruble was the strongest currency this week, closing at 61.19 vs. the dollar and gaining 94 basis points in a week. The currency is up 7 percent in October, the third best-best performing currency among 24 emerging market peers.

- Health care was the strongest sector within the emerging European countries this week.

Weaknesses

- Czech Republic was the weakest market this week, losing 1.06 percent. The Producer Price Index, which measures the average change in selling prices received by domestic producers, declined by 4.2 percent compared to the prior year. This week’s import and export data showed a slowdown in economic activity as well.

- The Polish Zloty was the weakest currency this week, losing 25 basis points. According to preliminary September data on money supply released by the central bank of Poland, the M3 aggregate amount increased significantly year over year caused by an increase in the level of corporate deposits. The latest CPI reading was reported as still negative at 0.8 percent.

- Energy was the weakest sector this week within the emerging European countries this week.

Opportunities

- The Bank of Russia has kept rates unchanged in September for the first time this year at 11 percent. With the ruble recently strengthening, the central bank of Russia may have more room to cut its rate at the next meeting on October 30.

- The Foundation of Economic and Industrial Research (IOBE) states in its quarterly review for the Greek economy that it is expecting 2015 gross domestic product to contract between 1.5 to 2 percent. IOBE predicts that the economy could return to growth in the second half of next year, provided the government takes the necessary steps.

- Yields on Polish bonds are declining despite an expected win in parliamentary elections later this month by the opposition party which promised to boost social spending, reduce the retirement age and impose tax on banks. A potential deterioration in Poland’s budget may be diminished by the European Central Bank’s bond-buying program and the delay in lifting U.S. interest rates.

Threats

- The Central Bank of Turkey has kept the one-week repurchase rate at 7.5 percent for more than six months, weakening the lira. The next rate decision will be announced on Tuesday, and most analysts predict the rate to remain unchanged at 7.5 percent.

- The European Union’s statistics office has confirmed that annual eurozone inflation turned negative in September due to lower energy prices. The European Central Bank may be under pressure to increase its asset purchase plan to boost the economy.

- Russian central bank governor Elvira Nabiullina does not worry about oil at $50 a barrel, but she is concerned “with the pace of reforms in the economy that could stimulate private investment.” Russia has adjusted to the collapse of oil prices but its economy is under pressure due to corruption and inefficiencies. In Transparency International’s 2014 rankings of perceived level of corruption, Russia is rank at 136, out of 174 countries, alongside Nigeria and Kyrgyzstan. The chart below shows the slowdown in Russian investment, now reaching 20 months of decline, the longest stretch of decline since at least 1995.

Leaders and Laggards

| Index | Close | Weekly Change($) |

Weekly Change(%) |

|---|---|---|---|

| DJIA | 17,215.97 | +131.48 | +0.77% |

| S&P 500 | 2,033.11 | +18.22 | +0.90% |

| S&P Energy | 509.95 | +3.77 | +0.74% |

| S&P Basic Materials | 276.91 | -0.35 | -0.13% |

| Nasdaq | 4,886.69 | +56.22 | +1.16% |

| Russell 2000 | 1,162.31 | -3.05 | -0.26% |

| Hang Seng Composite Index | 3,170.78 | +79.04 | +2.56% |

| Korean KOSPI Index | 2,030.26 | +10.73 | +0.53% |

| S&P/TSX Canadian Gold Index | 142.26 | +2.10 | +1.50% |

| XAU | 56.03 | -0.01 | -0.02% |

| Gold Futures | 1,175.70 | +19.80 | +1.71% |

| Oil Futures | 47.22 | -2.41 | -4.86% |

| Natural Gas Futures | 2.42 | -0.08 | -3.16% |

| 10-Yr Treasury Bond | 2.03 | -0.06 | -2.78% |

| Index | Close | Monthly Change($) |

Monthly Change(%) |

|---|---|---|---|

| DJIA | 17,215.97 | +476.02 | +2.84% |

| S&P 500 | 2,033.11 | +37.80 | +1.89% |

| S&P Energy | 509.95 | +34.92 | +7.35% |

| S&P Basic Materials | 276.91 | +6.61 | +2.45% |

| Nasdaq | 4,886.69 | -2.55 | -0.05% |

| Russell 2000 | 1,162.31 | -12.90 | -1.10% |

| Hang Seng Composite Index | 3,170.78 | +171.75 | +5.73% |

| Korean KOSPI Index | 2,030.26 | +54.81 | +2.77% |

| S&P/TSX Canadian Gold Index | 142.26 | +17.65 | +14.16% |

| XAU | 56.03 | +8.72 | +18.43% |

| Gold Futures | 1,175.70 | +56.70 | +5.07% |

| Oil Futures | 47.22 | +0.07 | +0.15% |

| Natural Gas Futures | 2.42 | -0.24 | -8.91% |

| 10-Yr Treasury Bond | 2.03 | -0.26 | -11.50% |

| Index | Close | Quarterly Change($) |

Quarterly Change(%) |

|---|---|---|---|

| DJIA | 17,215.97 | -870.48 | -4.81% |

| S&P 500 | 2,033.11 | -93.53 | -4.40% |

| S&P Energy | 509.95 | -21.91 | -4.12% |

| S&P Basic Materials | 276.91 | -22.09 | -7.39% |

| Nasdaq | 4,886.69 | -323.46 | -6.21% |

| Russell 2000 | 1,162.31 | -104.79 | -8.27% |

| Hang Seng Composite Index | 3,170.78 | -306.69 | -8.82% |

| Korean KOSPI Index | 2,030.26 | -46.53 | -2.24% |

| S&P/TSX Canadian Gold Index | 142.26 | +5.54 | +4.05% |

| XAU | 56.03 | +1.83 | +3.38% |

| Gold Futures | 1,175.70 | +42.20 | +3.72% |

| Oil Futures | 47.22 | -3.67 | -7.21% |

| Natural Gas Futures | 2.42 | -0.45 | -15.57% |

| 10-Yr Treasury Bond | 2.03 | -0.32 | -13.50% |

Please consider carefully a fund’s investment objectives, risks, charges and expenses. For this and other important information, obtain a fund prospectus by visiting www.usfunds.com or by calling 1-800-US-FUNDS (1-800-873-8637). Read it carefully before investing. Distributed by U.S. Global Brokerage, Inc.

All opinions expressed and data provided are subject to change without notice. Some of these opinions may not be appropriate to every investor.

| Fund | Year to Date | One-Year | Five-Year | Ten-Year | Gross Expense Ratio | Expense Cap |

|---|---|---|---|---|---|---|

| Emerging Europe Fund (EUROX) | 17.84% | -26.10% | -10.43% | -4.65% | 2.29% | N/A |

| China Region Fund (USCOX) | -11.46% | -6.68% | -4.78% | 2.53% | 2.97% | 2.55% |

| Gold and Precious Metals Fund (USERX) | -6.98% | -21.82% | -20.11% | -1.79% | 1.97% | 1.90% |

| Market Vectors Gold Miners ETF (GDX) | -25.39% | -35.31% | -23.97% | N/A | 0.53% | N/A |

| SPDR Gold Shares ETF (GLD) | -7.39% | -8.79% | -3.53% | N/A | 0.40% | N/A |

| PowerShares Global Gold & Precious Metals Portfolio ETF (PSAU) | -26.26% | -34.84% | -22.62% | N/A | 0.75% | N/A |

Expense ratios as stated in the most recent prospectus. The expense cap is a voluntary limit on total fund operating expenses (exclusive of any acquired fund fees and expenses, performance fees, extraordinary expenses, taxes, brokerage commissions and interest) that U.S. Global Investors, Inc. can modify or terminate at any time, which may lower a fund’s yield or return. Performance data quoted above is historical. Past performance is no guarantee of future results. Results reflect the reinvestment of dividends and other earnings. For a portion of periods, the fund had expense limitations, without which returns would have been lower. Current performance may be higher or lower than the performance data quoted. The principal value and investment return of an investment will fluctuate so that your shares, when redeemed, may be worth more or less than their original cost. Performance does not include the effect of any direct fees described in the fund’s prospectus (e.g., short-term trading fees of 0.05%) which, if applicable, would lower your total returns. Performance quoted for periods of one year or less is cumulative and not annualized. Obtain performance data current to the most recent month-end at www.usfunds.com or 1-800-US-FUNDS.

For information regarding the investment objectives, strategies, liquidity, risks, expenses and fees of the Market Vectors Gold Miners ETF, SPDR Gold Shares ETF, or the Powershares Global Gold & Precious Metals Portfolio please refer to those funds’ prospectuses.

Investment Objective: The Gold and Precious Metals Fund is an actively managed mutual fund that focuses on gold and precious metals producing companies. The Market Vectors Gold Miners ETF is a passively managed fund that seeks to replicate as closely as possible, before fees and expenses, the price and yield performance of the NYSE Arca Gold Miners Index. The investment objective of the SPDR Gold Trust is for the shares to reflect the performance of the price of gold bullion, less the expenses of the Trust’s operations. The PowerShares Global Gold & Precious Metals ETF is a passively managed fund that seeks to replicate as closely as possible, before fees and expense, the price and yield performance of the NASDAQ OMX Global Gold and Precious Metals Index.

Liquidity: The Gold and Precious Metals Fund can be purchased or sold at a net asset value (NAV) determined at the end of each trading day. The Market Vectors Gold Miners ETF, SPDR Gold Shares ETF and Powershares Global Gold & Precious Metals Portfolio can be purchased or sold intraday. These purchases and redemptions may generate brokerage commissions and other charges not reflected in the ETF’s published expense ratio.

Safety/Fluctuations of principal/return: Loss of money is a risk of investing in the Gold and Precious Metals Fund, the Market Vectors Gold Miners ETF, the SPDR Gold Shares ETF and the Powershares Global Gold & Precious Metals Portfolio. Shares of all of these securities are subject to sudden fluctuations in value.

Tax features: The Gold and Precious Metals Fund may make distributions that may be taxed as ordinary income or capital gains. Mutual funds are pass-through entities, so the shareholder is responsible for taxes due on distributions.

The Market Vectors Gold Miners ETF and the Powershares Global Gold & Precious Metals Portfolio may make distributions that are expected to be taxed as ordinary income or capital gains. However, ETFs are designed to minimize taxable distributions to shareholders. Shareholders of the SPDR Gold Trust will generally be treated as if they directly owned a pro rata share of the underlying assets held in the Trust. Shareholders also will be treated as if they directly received their respective pro rata shares of the Trust’s income and proceeds, and directly incurred their pro rata share of the Trust’s expenses.

The sale of shares of both mutual funds and ETFs may be subject to capital gains taxes by the shareholder.

Information provided here is neither tax nor legal advice and is general in nature. Federal and state laws and regulations are subject to change.

NASDAQ OMX Global Gold and Precious Metals Index is designed to measure the overall performance of the most liquid, globally traded companies involved in gold and other precious metals mining-related activities.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver. The index benchmark value was 500.0 at the close of trading on December 20, 2002.

Stock markets can be volatile and share prices can fluctuate in response to sector-related and other risks as described in the fund prospectus.

Foreign and emerging market investing involves special risks such as currency fluctuation and less public disclosure, as well as economic and political risk. By investing in a specific geographic region, a regional fund’s returns and share price may be more volatile than those of a less concentrated portfolio.

The Emerging Europe Fund invests more than 25 percent of its investments in companies principally engaged in the oil & gas or banking industries. The risk of concentrating investments in this group of industries will make the fund more susceptible to risk in these industries than funds which do not concentrate their investments in an industry and may make the fund’s performance more volatile.

Because the Global Resources Fund concentrates its investments in a specific industry, the fund may be subject to greater risks and fluctuations than a portfolio representing a broader range of industries.

Gold, precious metals, and precious minerals funds may be susceptible to adverse economic, political or regulatory developments due to concentrating in a single theme. The prices of gold, precious metals, and precious minerals are subject to substantial price fluctuations over short periods of time and may be affected by unpredicted international monetary and political policies. We suggest investing no more than 5 percent to 10 percent of your portfolio in these sectors.

Bond funds are subject to interest-rate risk; their value declines as interest rates rise. Though the Near-Term Tax Free Fund seeks minimal fluctuations in share price, it is subject to the risk that the credit quality of a portfolio holding could decline, as well as risk related to changes in the economic conditions of a state, region or issuer. These risks could cause the fund’s share price to decline. Tax-exempt income is federal income tax free. A portion of this income may be subject to state and local taxes and at times the alternative minimum tax. The Near-Term Tax Free Fund may invest up to 20% of its assets in securities that pay taxable interest. Income or fund distributions attributable to capital gains are usually subject to both state and federal income taxes.

Investing in real estate securities involves risks including the potential loss of principal resulting from changes in property value, interest rates, taxes and changes in regulatory requirements.

Past performance does not guarantee future results.

Some link(s) above may be directed to a third-party website(s). U.S. Global Investors does not endorse all information supplied by this/these website(s) and is not responsible for its/their content.

These market comments were compiled using Bloomberg and Reuters financial news.

Fund portfolios are actively managed, and holdings may change daily. Holdings are reported as of the most recent quarter-end. Holdings as a percentage of net assets as of 9/30/15:

Wal-Mart Stores, Inc.: All American Equity Fund, 0.98%

SPDR Gold Trust: 0.0%

Market Vectors Gold Miners ETF: 0.0%

PowerShares Global Gold & Precious Metals ETF: 0.0%

Klondex Mines Ltd: Global Resources Fund, 3.79%; Gold and Precious Metals Fund, 16.91%; World Precious Minerals Fund, 17.76%

TripAdvisor, Inc.: 0.0%

The Priceline Group, Inc.: 0.0%

Quanta Services, Inc.: 0.0%

Fortuna Silver Mines, Inc.: Gold and Precious Metals Fund, 1.53%; World Precious Minerals Fund, 1.56%

BHP Billiton Ltd: 0.0%

Rio Tinto PLC: Global Resources Fund, 0.33%

Schlumberger Ltd: All American Equity Fund, 1.04%

*The above-mentioned indices are not total returns. These returns reflect simple appreciation only and do not reflect dividend reinvestment.

The Dow Jones Industrial Average is a price-weighted average of 30 blue chip stocks that are generally leaders in their industry.

The S&P 500 Stock Index is a widely recognized capitalization-weighted index of 500 common stock prices in U.S. companies.

The Nasdaq Composite Index is a capitalization-weighted index of all Nasdaq National Market and SmallCap stocks.

The Russell 2000 Index® is a U.S. equity index measuring the performance of the 2,000 smallest companies in the Russell 3000®, a widely recognized small-cap index.

The Hang Seng Composite Index is a market capitalization-weighted index that comprises the top 200 companies listed on Stock Exchange of Hong Kong, based on average market cap for the 12 months.

The Taiwan Stock Exchange Index is a capitalization-weighted index of all listed common shares traded on the Taiwan Stock Exchange.

The Korea Stock Price Index is a capitalization-weighted index of all common shares and preferred shares on the Korean Stock Exchanges.

The Philadelphia Stock Exchange Gold and Silver Index (XAU) is a capitalization-weighted index that includes the leading companies involved in the mining of gold and silver.

The U.S. Trade Weighted Dollar Index provides a general indication of the international value of the U.S. dollar.

The S&P/TSX Canadian Gold Capped Sector Index is a modified capitalization-weighted index, whose equity weights are capped 25 percent and index constituents are derived from a subset stock pool of S&P/TSX Composite Index stocks.

The S&P 500 Energy Index is a capitalization-weighted index that tracks the companies in the energy sector as a subset of the S&P 500.

The S&P 500 Materials Index is a capitalization-weighted index that tracks the companies in the material sector as a subset of the S&P 500.

The S&P 500 Financials Index is a capitalization-weighted index. The index was developed with a base level of 10 for the 1941-43 base period.

The S&P 500 Industrials Index is a Materials Index is a capitalization-weighted index that tracks the companies in the industrial sector as a subset of the S&P 500.

The S&P 500 Consumer Discretionary Index is a capitalization-weighted index that tracks the companies in the consumer discretionary sector as a subset of the S&P 500.

The S&P 500 Information Technology Index is a capitalization-weighted index that tracks the companies in the information technology sector as a subset of the S&P 500.

The S&P 500 Consumer Staples Index is a Materials Index is a capitalization-weighted index that tracks the companies in the consumer staples sector as a subset of the S&P 500.

The S&P 500 Utilities Index is a capitalization-weighted index that tracks the companies in the utilities sector as a subset of the S&P 500.

The S&P 500 Healthcare Index is a capitalization-weighted index that tracks the companies in the healthcare sector as a subset of the S&P 500.

The S&P 500 Telecom Index is a Materials Index is a capitalization-weighted index that tracks the companies in the telecom sector as a subset of the S&P 500.

The NYSE Arca Gold Miners Index is a modified market capitalization weighted index comprised of publicly traded companies involved primarily in the mining for gold and silver.

The Consumer Price Index (CPI) is one of the most widely recognized price measures for tracking the price of a market basket of goods and services purchased by individuals. The weights of components are based on consumer spending patterns.

The Purchasing Manager’s Index is an indicator of the economic health of the manufacturing sector. The PMI index is based on five major indicators: new orders, inventory levels, production, supplier deliveries and the employment environment.

The National Federation of Independent Business’s (NFIB) Index of business optimism is based on responses from 1,221 member firms.

The Producer Price Index (PPI) measures prices received by producers at the first commercial sale. The index measures goods at three stages of production: finished, intermediate and crude.

The New York Empire State Manufacturing Survey is sent out to companies in the manufacturing industry in New York state. The survey provides an early indication of business conditions, such as price levels and employment trends, and it gives an indication of changes in sentiment. The survey is produced by the Federal Reserve Bank of New York and is released around the middle of the month.

The Philadelphia Federal Index is a regional federal-reserve-bank index measuring changes in business growth. The index is constructed from a survey of participants who voluntarily answer questions regarding the direction of change in their overall business activities. The survey is a measure of regional manufacturing growth. When the index is above 0 it indicates factory-sector growth, and when below 0 indicates contraction. Also known as the "Business Outlook Survey.”

The Bloomberg World Iron/Steel Index is a capitalization-weighted index of the leading iron/steel stocks in the world.

The S&P/TSX Capped Metals and Mining Index is a capitalization-weighted index.

The S&P 500 Construction & Engineering Index is a capitalization-weighted index.

The S&P 500 Construction Materials Index is a capitalization-weighted index that tracks the companies in the construction materials industry as a subset of the S&P 500.

The Shanghai Composite Index (SSE) is an index of all stocks that trade on the Shanghai Stock Exchange.

The MSCI Asia Pacific ex Japan Industrials Index is a free-float weighted equity index.

The Jakarta Stock Price Index is a modified capitalization-weighted index of all stocks listed on the regular board of the Indonesia Stock Exchange.

The MSCI Asia Pacific ex Japan Healthcare Index is a free-float weighted equity index.