Global Economic Outlook - October 2015

It has been a challenging interval for the world economy. The summer saw challenges in Greece, heightened uncertainty over China and renewed concern over emerging markets. At its recent meetings, the International Monetary Fund (IMF) further downgraded its outlook for global growth.

We would certainly concur with the characterization of the Federal Reserve that international risks tend toward the downside. But our most-likely case calls for continued expansion, at a moderate pace.

UNITED STATES

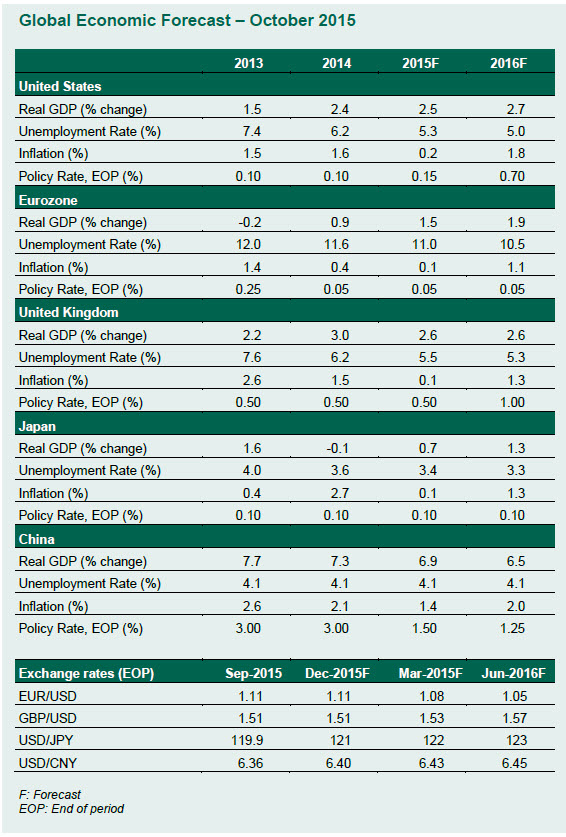

Economic growth in the United States likely slowed in the third quarter, mainly due to a reduction of inventories and decline in exports. Consumer fundamentals remain positive, though, and support expectations of continued progress in the quarters ahead. Real gross domestic product (GDP) is projected to advance 2.7% during 2016, while the unemployment rate should stabilize around 5.0%.

Labor market data suggest the Fed is moving close to its employment mandate, but inflation numbers are far below the 2.0% target. Inflation is predicted to inch forward only gradually in the quarters ahead. Further improvements in the labor market and better readings on wage growth will help to seal the case for reducing monetary policy accommodation.

The lackluster performance of China, the strong dollar and the contraction of the U.S. energy industry will remain headwinds in the near future.

EUROZONE

The eurozone recovery continues to broaden, but risks to the downside remain, including the impact of China’s ongoing slowdown. Europe exports considerable amounts to China, and is therefore more vulnerable than the United States to China’s economic moderation.  Assume that China does not spiral into a hard landing and that Greece’s political establishment continues to muddle through its reform process enough to keep its creditors happy. Then eurozone real GDP growth should edge up to 1.5% this year and 1.9% in 2016.

Assume that China does not spiral into a hard landing and that Greece’s political establishment continues to muddle through its reform process enough to keep its creditors happy. Then eurozone real GDP growth should edge up to 1.5% this year and 1.9% in 2016.

As ever, the pace of recovery remains uneven across the 19 eurozone members. Germany is still the growth engine, although the likely slide in external demand will somewhat dampen its export growth through 2016. Spain and Ireland continue to post firm recoveries that are starting to have a positive impact on their labor markets.

Italy continues to struggle to build economic momentum while its government grapples with long-term structural and constitutional reforms. France remains the laggard on the reform front, and its growth rate will continue to fall short of the eurozone average. The overall unemployment rate will continue to vary widely among members; the eurozone average jobless rate should come in at 11.0% this year and improve to 10.5% in 2016.

Eurozone inflation will remain muted for the remainder of 2015, driven down by low oil prices. The annual rate of increase in the price level should average 0.1% this year before picking up to 1.1% next year – still well below the European Central Bank (ECB) target of “near 2.0%.” The ECB will continue with its asset purchase program and may even extend or expand it. Either way, the main policy rate will likely stay at 0.05% until the end of 2016.

UNITED KINGDOM

Growth in the United Kingdom is still heavily determined by the service sector. Manufacturing and construction contracted over the summer, and trade will remain a drag. The relatively strong pound continues to depress import prices and hold down inflation. Nevertheless, firm consumer spending will continue to underpin real GDP growth, which should come in around 2.6% this year and next.  A referendum sometime in 2016 on membership in the European Union presents downside risks, as it may cause companies to delay hiring decisions, or threaten London’s standing as a financial center.

A referendum sometime in 2016 on membership in the European Union presents downside risks, as it may cause companies to delay hiring decisions, or threaten London’s standing as a financial center.

Inflation briefly turned negative again in September and will likely average just 0.1% this year. The Bank of England (BoE) continues to point to temporary factors, principally the low oil price, which will eventually work their way out of the system; we expect inflation to average a still-subdued 1.3% in 2016. Unemployment is forecast to fall to 5.5% this year and 5.3% next as labor-market normalization continues.

The BoE’s first policy rate hike will likely come sometime in the second quarter, when inflation is forecast to reach 1.0%. A second hike later in the year will leave the policy rate at 1.0% by the end of 2016.

JAPAN

In a halting and painfully slow way, it is possible that Abenomics is actually working. Agricultural reform, improved corporate governance and rising female workforce participation were once almost unthinkable goals that have come to fruition.  Although second-quarter growth was disappointing, it does not spell doom for the Japanese economy. Investment intentions among corporations are solid, and the increase to the minimum wage later in the year should boost consumer spending. However, net exports could continue to be a drag as the slowdown in China counterbalances the benefits gained from the weak yen.

Although second-quarter growth was disappointing, it does not spell doom for the Japanese economy. Investment intentions among corporations are solid, and the increase to the minimum wage later in the year should boost consumer spending. However, net exports could continue to be a drag as the slowdown in China counterbalances the benefits gained from the weak yen.

Unlike in previous slowdowns, substantial fiscal stimulus has been noticeably absent; however, this could change after third-quarter GDP is announced in November. If the economy falls into technical recession, it will be hard for Prime Minister Shinzo Abe to avoid introducing a supplementary budget.

The Bank of Japan (BOJ) will continue to be the primary engine for stimulus in the economy, and the larger policy question is whether or not it adds to its quantitative easing program. Odds are that the BOJ will not take that step this year – largely due to desire to maintain yen stability – but headwinds might push the central bank to react.

CHINA

We have inched our forecast for 2015 Chinese GDP growth down to 6.9%. Third-quarter expansion registered 6.9%, down from 7% the previous quarter. Growth in the fourth quarter is likely to post similar numbers, as weak export readings, declining industrial activity and a real estate slump continue to weigh on the economy. The Chinese are reporting greater gains in spending and services, which offset these disappointments to a degree; analysts are taking these readings cautiously.  Chinese fiscal policy is set to remain accommodative as officials attempt to spend their way to growth stability. At 1.78 trillion yuan, government spending increased 27% year-over-year in September. Beijing appears, at present, to be focusing on the fast tracking of infrastructure spending rather than direct fiscal stimulus. To this end, there is evidence that local governments are being pressured to accelerate infrastructure spending and exhaust their budgets.

Chinese fiscal policy is set to remain accommodative as officials attempt to spend their way to growth stability. At 1.78 trillion yuan, government spending increased 27% year-over-year in September. Beijing appears, at present, to be focusing on the fast tracking of infrastructure spending rather than direct fiscal stimulus. To this end, there is evidence that local governments are being pressured to accelerate infrastructure spending and exhaust their budgets.

Meanwhile, another interest-rate cut from the People’s Bank of China (PBoC) is possible before the end of the year. Any rate change is also likely to include a cut in banks’ reserve requirement ratio. The central bank has already eased on five separate occasions since November 2014. Our baseline forecast includes at least two more interest-rate cuts before the end of 2016.

The PBoC’s unexpected, and poorly explained, devaluation of the yuan in August unsettled markets and took emerging markets on a bumpy ride. However, fears of rapid depreciation of the currency have been unfounded. In fact, officials have burned through at least $200 billion in international reserves to keep the yuan steady. The continued push to be included in the IMF’s Special Drawing Rights basket should be enough to ensure that policymakers pursue an orderly descent of the currency.