Follow the Leaders: Learning from ETFs, BCA and the New PM

Yesterday I had the pleasure of attending an intensive daylong ETF conference in Austin, just up the road from our office in San Antonio. Hosted by Cantor Fitzgerald, the conference was designed for institutional investors.

Welcoming the group was Reginald “Reggie” Browne, the “Godfather of ETFs,” who now serves as the senior managing director at Cantor Fitzgerald. His celebrity and prominence are nearly as big as his six-foot-five frame—and with good reason. Reggie has been instrumental in building the ETF landscape over the last decade and convincing investors of the power of the exchange-traded fund.

One of the panels featured chief investment officers from the Texas Teacher Retirement System (TRS). Jase Auby, Lee Partridge and Tom Tull discussed potential shifts in asset allocation under a rising interest rate environment, among other topics.

The TRS, one of the largest pension funds in the U.S., makes significant use of gold in its investment strategy, holding the yellow metal in many forms over the years. The same is true for the $20 billion University of Texas endowment fund.

Bruce Zimmerman, chief investment officer for UTIMCO, told CNBC in 2011 that the $20 billion endowment holds gold as a diversifier and hedge against currencies. This is precisely what we tell investors, and it’s validating to see such huge funds put it in practice.

During the ETF panel, I asked Jase, Lee, Tom and moderator Ronnie Jung about their thoughts on real interest rates and their relationship with gold. Everyone’s speculating on when the Federal Reserve will hike interest rates, but real interest rates, as I shared with you this week, appear to have already risen. (As a reminder, real interest rates are what you get when you deduct the monthly rate of inflation from the 10-year Treasury yield.) A 10 percent upswing in the U.S. dollar is equivalent to the federal funds rate being hikes 100 basis points.

This has had a huge effect on the yellow metal. When real rates are negative, gold has tended to do well. Conversely, when they’re positive—and rising, as they are now—it’s been a headwind for gold. This relationship was confirmed by the research of Barry Bannister, chief equity strategist for Stifel, who visited our office last week.

I also appreciated the TRS group’s bullishness on China. Their position is that, because everyone is negative on China right now, all sorts of investment opportunities open up from a contrarian point of view.

The World’s Second-Largest Economy in Flux

I’ve commented before that China has been moving away from a manufacturing-based economy and instead focusing more on services—financials, real estate, insurance, ecommerce and the like.

While the country’s purchasing managers’ index (PMI) reading has been in contraction mode since March of this year, these service industries are ever-expanding. The problem is that the transformation has not been fast enough to offset the massive size of the manufacturing sector.

But investment opportunities in this sector still exist. Anyone who’s traveled more than 100 miles inland knows that China is under-urbanized. Ever since Deng Xiaoping created special tax-free zones along the eastern Chinese coastline in 1978, most of the country’s growth has been concentrated in these few regions and municipalities. The interior provinces, on the other hand, have remained largely rural.

You can see this for yourself in the chart below, provided by Marko Papic, chief geopolitical strategist for BCA Research, who briefed our investments team this week. BCA is an influential, independent investment strategy firm with more than 65 years of experience conducting excellent macroeconomic research.

We just learned that the People’s Bank of China cut both lending and saving rates 0.25 percent, to 4.35 percent and 1.50 percent respectively. This will cause negative real rates in China to fall even lower, which is good for gold demand.

It will also likely add to the Fed’s list of doubts about raising its own rates. In a world where every other major country is stimulating its economy by cutting rates and devaluing its currency, it makes less and less sense for the U.S. to hike rates.

BCA’s Marko Papic stressed the need to see further stimulus in China. Without it, commodities and global growth in general are at risk. Some economists believe we might be headed for a global recession.

Difference of Opinion When It Comes to Defining Global Recession

Depending on who you ask, there are different ideas of what global recession looks like. The generally accepted one in the U.S. is two consecutive quarterly declines in real GDP. The International Monetary Fund (IMF), however, uses a different measure. Among other economic conditions, annual GDP must fall below 3 percent, a high benchmark and one that requires much stimulus.

Global growth for 2015 is at 3.3 percent, the IMF calculates, precariously close to the 3 percent threshold.

BCA Research: The Trans-Pacific Partnership Is Needed to Fast-Track Global Growth

This is where the Trans-Pacific Partnership (TPP) comes into play, which is the stance BCA also takes. The landmark trade agreement, involving 12 nations, was signed earlier this month. Although it still requires ratification, the TPP could boost the world economy by an incredible $223 billion by 2025, according to the Peterson Institute for International Economics.

Like Father, Like Son: Canada Elects a New Leader

|

One of the TPP’s biggest supporters was outgoing Canadian Prime Minister Stephen Harper. But the newly elected Justin Trudeau, member of the Liberal party, has also come out in support of free trade agreements. The hope is that he will continue to take this position where the TPP is concerned.

Although Trudeau earned his degree in education from the University of British Columbia and taught as a school teacher for many years, he is by no means a stranger to politics. He’s served as a Member of Parliament since 2008, and his father, Pierre Trudeau, served as Canada’s prime minister for 15 years.

Back in the 1970s, in fact, I campaigned for Pierre Trudeau alongside Dr. John Evans, a Rhodes Scholar. This was during Trudeau’s first stint in office, before being voted out in 1979 and then returning to serve again in 1984.

His son, only 43, ran on a campaign of hope and change—sound familiar?—and promised that, if elected, he would help the economy by increasing infrastructure spending. Unlike some other world leaders, he wants to put people to work instead of establishing a welfare state. Trudeau plans to raise revenue by taxing recreational marijuana—if he succeeds at legalizing it, that is.

|

One of the main criticisms of Trudeau the Younger is that he’s inexperienced politically. But here in the U.S., take a look at who’s currently topping the polls in the Republican field: business magnate Donald Trump, neurosurgeon Dr. Ben Carson and former Hewlett-Packard CEO Carly Fiorina. Accomplished though they are, none of them has been elected to office. This goes to show that voters have grown fed up with career politicians who lack accountability.

One of the main criticisms of Trudeau the Younger is that he’s inexperienced politically. But here in the U.S., take a look at who’s currently topping the polls in the Republican field: business magnate Donald Trump, neurosurgeon Dr. Ben Carson and former Hewlett-Packard CEO Carly Fiorina. Accomplished though they are, none of them has been elected to office. This goes to show that voters have grown fed up with career politicians who lack accountability.

Next stop, the Big Easy

|

Next week will kick off my short conference road trip, beginning with the 2015 New Orleans Investment Conference, happening October 28 – 31. For 41 years, this event has attracted some of the world’s most distinguished speakers—from Margaret Thatcher to Steve Forbes to Norman Schwarzkopf—and this year’s no exception. I look forward to speaking again this year alongside some of the brightest minds in the industry at what some call the “World’s Greatest Investment Event.”

After that, I’ll head to Peru for the Mining & Investment Latin America Summit, November 4 – 5, and wrap things up in Melbourne, Australia, at the International Mining and Resources Conference.

I look forward to sharing my insights gained from my travels and hope you’ll join me in New Orleans!

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 2.50 percent. The S&P 500 Stock Index rose 2.07 percent, while the Nasdaq Composite climbed 2.97 percent. The Russell 2000 small capitalization index gained 0.32 percent this week.

- The Hang Seng Composite gained 0.31 percent this week; while Taiwan was up 0.80 percent and the KOSPI rose 0.50 percent.

- The 10-year Treasury bond yield rose 5 basis points to 2.09 percent.

Domestic Equity Market

Strengths

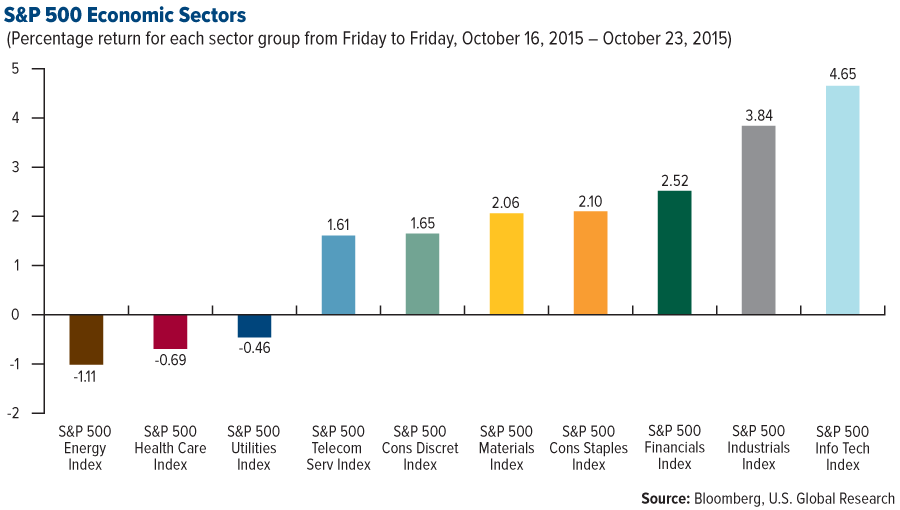

- Information technology was the best performing sector this week, boosted by KLA-Tenor Corp after Lam Research agreed to buy the semiconductor manufacturing firm. The S&P 500 Information Technology Index rose 4.65 percent this week.

- Industrials was the second strongest sector in the S&P 500 this week, driven largely by the airline industry which continues to benefit from cheap fuel costs. The S&P 500 Industrials Index rose 3.84 percent this week.

- Existing home sales in the United States grew to 5.55 million in September from 5.31 million in August, surpassing analyst expectations. The housing market continues to show signs of strength.

Weaknesses

- Energy stocks lagged the broader market this week as WTI crude oil fell to $44.70 per barrel. The S&P 500 Energy Index fell 1.01 percent this week.

- The yield on the 10-year U.S. government note rose this week, putting pressure on other income plays. The 10-year yield is now roughly 2.085 percent.

- The U.S. dollar rallied back up to 97.15 this week, adding further pressure on commodities and other export driven markets.

Opportunities

- U.S. Markit flash manufacturing purchasing managers’ index (PMI) rose to 54.0, according to October’s preliminary reading. A turnaround in the manufacturing PMIs, which have been trending downward, could benefit cyclical sectors.

- President of the European Central Bank (ECB) Mario Draghi further emphasized this week the bank’s willingness to use any monetary tool at its disposal. The expectation of further stimulus has placed downward pressure on the dollar and should benefit more risk heavy areas of the market.

- China cut interest rates again this week, boosting market expectations that the economic juggernaut is not willing to allow growth to slow down too much further.

Threats

- The Conference Board’s Leading Economic Index contracted by a larger amount that expected, according to official data released this week. The index fell 0.2 percent for the month of September, compared to a 0.1 percent expansion the prior month.

- The assault on the health care sector continues this week with Hillary Clinton emphasizing the need for tighter regulation of the industry.

- There is still a sharp divergence between market and economist expectations regarding when the Federal Reserve will raise the Fed Funds rate. If the majority of economists are correct and a hike occurs this year, the market could react negatively to the surprise.

The Economy and Bond Market

Strengths

- Yields on 10-year U.S. Treasury notes rose this week as investors reacted positively to China’s interest rate cuts and the European Central Bank’s (ECB’s) pledge to do anything necessary to support the economy. Although poor for bonds, the rise in yields shows further confidence in the global economy.

- The Markit Eurozone Manufacturing PMI remained at 52.0 percent according to the preliminary October reading released this week. The street was expecting a further decline, making this a positive surprise.

- Eurozone’s Markit services purchasing managers’ index (PMI) showed significant signs of strength this week, as the preliminary October reading rose to 54.2. Given that services make up a large majority of economic activity in the eurozone, this is a welcomed surprise.

Weaknesses

- Germany’s manufacturing sector continues to forecast further weakness as the Markit/BME Germany manufacturing PMI fell to 51.6 in October from 52.3 the prior month.

- Although China’s GDP growth for the third quarter beat analyst expectations, there is speculation that the service sector data may have been propped up. Regardless, manufacturing continues to be the main drag on Chinese growth.

- Another disappointing data point released this week was China’s industrial production for the month of September, which rose by only 5.7 percent compared to an expected 6.0 percent.

Opportunities

- Mario Draghi, president of the ECB, further emphasized the bank’s commitment to using any and all monetary tools at their disposal to stimulate growth. Further easing would push down yields in the eurozone which could drag down Treasury yields.

- China cut its interest rates once again this week, strengthening the view that the slowing economy will see the necessary government intervention.

- The University of Michigan’s Consumer Sentiment Index is forecasted to rise to 92.5 for the month of October. Retail and other discretionary stocks could rally.

Threats

- Consumer confidence in the eurozone fell more than expected this week, according to the European Commission’s Consumer Confidence Indicator. Retail and other discretionary stocks might be at risk.

- The Federal Reserve could decide to raise the Fed Funds rate next week, and with the market predicting lower rates for longer, the surprise could shock the market.

- Economic activity is forecasted to have grown only 1.6 percent for the third quarter, according to Bloomberg surveys. This is a steep decline from the 3.9 percent expansion seen in the second quarter.

Gold Market

For the week, spot gold closed at $1,164.572 down $12.60 per ounce, or -1.07 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, held in with a gain of 0.19 percent. Junior miners underperformed seniors for the week as the S&P/TSX Venture Index’s loss of 0.91 percent. The U.S. Trade-Weighted Dollar Index surged 2.71 percent for the week.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Oct -18 | CH Retail Sales YoY | 10.80% | 10.9% | 10.80% |

| Oct -20 | US Housing Starts | 1142K | 1206K | 1126K |

| Oct -22 | EC ECB Main Refinancing Rate | 0.05% | 0.05% | 0.05% |

| Oct -22 | US Initial Jobless Claims | 265K | 259K | 255K |

| Oct -26 | New Home Sales | 550K | -- | 552K |

| Oct -27 | Export YoY | -3.5% | -- | -6.1% |

| Oct -27 | Durable Goods Orders | -1.3% | -- | -2.0% |

| Oct -27 | Consumer Confidence Index | 103.0 | -- | 103.0 |

| Oct -28 | FOMC Rate Decision | 0.25% | -- | 0.25% |

| Oct -29 | US Initial Jobless Claims | 263K | -- | 259K |

| Oct -29 | GDP Annualized QoQ | 1.6% | -- | 3.9% |

| Oct -29 | CPI YoY | 0.2% | -- | 0.0% |

| Oct -30 | CPI Core YoY | 0.9% | -- | 0.9% |

Strengths

- Palladium was the best relative performing precious metal this week, recording a fall of just 0.27 percent. Palladium has been in a gentle decline post the Volkswagen story on emissions fixing, but rallied the last few days of this week.

- Gold traders are maintaining their bullish calls on the precious metal for the third week in a row. Of the 24 traders surveyed by Bloomberg, 13 hold a bullish outlook on gold.

- Gold got a boost this week as China announced further interest rate cuts and the ECB re-emphasized its pledge to use all the monetary tools at its disposal to support global growth. Furthermore, Russia boosted its gold purchases by the largest amount in a year throughout the month of September, adding 34 tonnes.

Weaknesses

- Silver was off 1.47 percent, making it the worst performing precious metal this week. Silver is normally more volatile than gold, so during a week that gold declines we should expect to see silver be pared back more so than gold.

- India has officially announced the implementation of its gold monetization scheme that is set to replace existing deposit structure. The plan seeks to reduce imports as banks will now be allowed to sell or lend gold to retailers, thus boosting supply if owners of the gold trust the system enough to lend their gold to the state.

- Argonaut Gold is facing some operation issues as an illegal blockade has formed at its El Castillo mine in Durango, Mexico.

Opportunities

- Investors are eyeing gold once again as $393 million flowed into U.S. precious metals-backed exchange traded funds this month, through October 20. After a multiyear downturn in the precious metal, more bulls are emerging. Retail investors have depleted coin dealer inventories of silver coins, Russia and China are buying gold, and even Paul Singer of Elliot Management said recently that investors should have up to 10 percent of their portfolio in gold and/or gold stocks.

- The corporate sector could cause trouble for the U.S. economy as profits are contracting on a year-over-year basis. What’s more, every contraction in profits since 1980 has coincided with a rise in the corporate default rate. The default rate also closely correlates with job cut announcements.

- Overall, credit conditions for U.S. companies are already deteriorating as the 10-month span through this year has seen more S&P downgrades than the prior two years combined. Even more concerning is that these downgrades are not solely limited to the energy space. Challenger Gray noted that they are seeing layoffs at major firms at a level they have not witnessed since 2009.

Threats

- The largest hurricane the world has ever recorded could cause trouble for certain Mexican mining operators proximal to the Western coast. The third-quarter rainy season just ended, normally playing havoc with heap leach operations. Companies such as Primero, Alamos and Argonaut could be affected; potentially even Goldcorp or Agnico-Eagle, should the rainfall be intense.

- Goldman Sachs is expecting the Federal Reserve to hike rates in December and sees gold suffering as a result. The bank sees gold falling to $1,000 over the next 12 months.

- Faced with significant debt repayments, the Venezuelan government may tap into its gold reserves to generate sufficient cash. Venezuela dumping its gold could put negative pressure on global prices. Venezuela also made the news when the country notified Guyana Goldfields that its mine, which is nearly finished with construction, is on land claimed to be owned by Venezuela and not Guyana.

Energy and Natural Resources Market

Strengths

- Base metals stocks continue to lead all natural resources sub-sectors this week. News from China concerning interest rate cuts gave confidence to traders that the government is committed to providing stimulus to revive the economy. The S&P/TSX Metals & Mining Index gained 2.6 percent during the week.

- Paper and forest products stocks gained 4 percent on stable pricing and positive sentiment for continued growth in the housing market.

- Rail stocks were among the top three industries within the natural resources sector this week as constructive earnings releases within the group improved investor sentiment. The S&P 500 Rail Index gained 3.6 percent this week.

Weaknesses

- Oil and gas income stocks retreated from prior gains on a combination of profit taking and slightly disappointing earnings reports. The Yorkville Royalty Oil & Gas Index fell 1.7 percent and the Alerian MLP Infrastructure Index fell 6.3 percent.

- The Bloomberg Tanker Index declined 4.1 percent this week along with the price of crude oil, as concerns regarding overcapacity in the product market negatively impacted share prices.

- Crude oil and related equities fell late in the week by -5.5 percent and -5.2 percent, respectively. Inventory levels in the U.S. continue to swell and onshore product remains resilient, despite a historically low rig count.

Opportunities

- Plenty of economic releases are scheduled for next week that could move natural resources on better-than-expected news. New home sales, durable goods orders, the Richmond Federal Manufacturing Index and the FOMC rate decision could be meaningful for commodities next week.

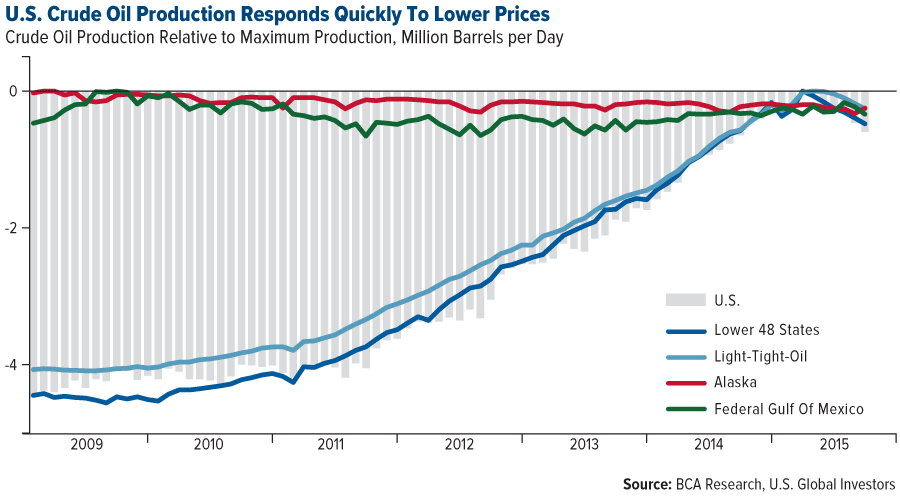

- Deutsche Bank expects further U.S. rig count declines to eventually prove positive for the crude oil price outlook. The research team expects another 50 to 100 rigs could be removed from service next year for operators to be cash-flow neutral next year. Accordingly, the bank sees further downside to its expectation of a 650 kb/d decline in U.S. production in 2016.

- While it remains unclear who will win Sunday’s presidential election in Argentina, one thing is already decided: farmers are poised to benefit as both leading candidates plan to eliminate wheat and corn export taxes and cut a soybean levy, according to Barclays.

Threats

- MDA Weather Services forecasts higher-than-usual temperatures to cover much of the U.S. through November 6, helping to push the price of natural gas to a three-year low as stockpiles build toward record levels.

- The strongest hurricane ever recorded in the Western Hemisphere is set to strike near Mexico’s biggest port and vacation resort this weekend, threatening massive damage to property and lives of anyone in the area.

- Predictions for the third strongest El Nino season since 1950 appear to be gaining momentum. Pacific typhoons, droughts and floods throughout the world have already begun causing havoc in agriculture and infrastructure, according to Bloomberg.

China Region

Strengths

- Indonesia was the best performing market in the region this week, driven by the government’s announcement to nullify double taxation on REITs and lower tax rates for asset revaluation. This came in a fifth round of policy measures aimed to facilitate investment. The Jakarta Composite Index was up 2.90 percent for the week.

- Health care was the best performing sector this week, a rebound from being a laggard the previous week. The MSCI Asia Pacific ex Japan Healthcare Index rose 0.35 percent for the week.

- The Chinese renminbi was the best performing currency this week, approximately flat versus the U.S. dollar, as the country’s third-quarter GDP growth came out marginally better than expected at 6.9 percent. Additionally, expectations rose for the currency’s inclusion in the IMF’s currency basket this year.

Weaknesses

- Malaysia was the worst performing market in the region this week, as both the Malaysian ringgit and crude oil pulled back for a second week from the recent surge. The FTSE Bursa Malaysia Index was down 0.34 percent for the week.

- Materials was the worst performing sector this week, as growth in China’s industrial production and fixed asset investment in September disappointed investors. The MSCI Asia Pacific ex Japan Materials Index fell 2.32 percent for the week.

- The Malaysian ringgit was the worst performing currency in the region this week, losing 1.82 percent, due in part to political uncertainties and a renewed downward pressure on crude oil prices.

Opportunities

- While uncertainties remain whether China’s economic growth is indeed stabilizing, it is irrefutable that the country’s services industry has overtaken manufacturing in recent years and surpassed 50 percent of total GDP for the first time in history in the first nine months of 2015. Retail sales have been the most resilient among all macroeconomic indicators amid China’s ongoing slowdown. Consumer-oriented goods and services sectors should present more sustainable opportunities for investors going forward.

- China’s central bank cut its benchmark interest rate by 25 basis points this week and announced its decision to cut the reserve requirement ratio (RRR) for banks by 50 basis points after the local market close on Friday. The interest rate cut represents the sixth reduction since November 2014 and drove the real deposit rate, or inflation-adjusted deposit rate, into negative territory again. Rate-sensitive sectors in China such as property and insurance should benefit most in the short term from monetary policy easing.

- South Korea’s better-than-expected GDP growth at 2.6 percent in the third quarter, thanks to a strong rebound in private consumption and government spending, should reinforce investors’ preference for Korean sectors geared toward domestic demand rather than global demand. Financials, consumer staples and pharmaceuticals could continue to outperform electronics and industrials exporters.

Threats

- Rising residential property supply in Hong Kong in the next few years comes at the same time that local housing demand has turned decidedly weaker, as reflected in both transaction volume and prices. Combined with an upcoming adverse interest rate cycle when the U.S. Federal Reserve embarks on monetary tightening, property developers in Hong Kong are set to face more headwinds than tailwinds.

- Mixed third-quarter earnings releases from Macau casinos do not assuage investor concerns over the secular appeal of the casino gaming industry, against no fundamental change in Chinese anticorruption policy direction and little proof of valuation distress. The bear market in Macau casino stocks has shown little signs of being over.

- Renewed weakness in crude oil prices and imminent November cuts in domestic natural gas prices in China do not bode well for its energy sector in general, and upstream natural gas producers in particular.

Emerging Europe

Strengths

- Greece was the best performing market this week as eurozone officials continue to highlight the progress of the negotiations. The next phase will be to tackle recapitalization of the banking system. The Athens Stock Exchange General Index closed up 3.87 percent.

- The Russian ruble was the worst performing currency this week as crude oil prices fail to make any constructive progress. The ruble fell 1.47 percent against the dollar.

- Health care was the best sector among eastern European markets this week as U.S. health care names face the threat of tighter regulation.

Weaknesses

- The Czech Republic was the worst relative performing market this week, although the PX Index closed up 1.61 percent, getting a rally along with the rest of the region.

- The Polish zloty was the worst performing currency in the region this week as concerns increase leading up to the parliamentary elections. The zloty fell 3.54 percent against the dollar.

- Energy was the worst performing sector in the region this week as crude oil prices dipped further.

Opportunities

- Activity in the eurozone’s private sector picked up in October. Markit’s composite purchasing managers’ index (PMI), a measure of activity in the manufacturing and service sectors, rose to 54.0 in October from a prior reading of 53.6. A reading below 50 indicates activity is slowing down, while a reading above that level indicates it is increasing.

- Emerging market share price could advance further as equites may be testing a resistance level that acted as a support for several years. If equites break though the resistance level more upside is coming.

- ECB President Mario Draghi sent a strong signal Thursday that the bank is prepared to increase its bond-buying program. The main interest rate, the rate that is charged on regular loans to banks, was left unchanged at .05 basis points. The rate on overnight deposits also remained at -.2 percent, meaning banks continue to pay to park excess deposits at the central bank.

Threats

- The Polish zloty may weaken if the Law & Justice party wins majority seats in Sunday’s general election. The party seeks to boost spending on family benefits, cut the retirement age and reduce taxes for smaller companies. The current Prime Minister, Ewa Kopacz, whose Civic Platform is trailing in opinion polls, has warned that the spending promises could destabilize public finances and increase a budget gap. Civic Platform reduced the budget gap to below 3 percent of economic output from 7.8 percent five years ago.

- Foreign airlines continue to cancel flight to Moscow. In January, EasyJet scaled back its London-Moscow service from two daily flights to only one. Then Delta, a U.S. airliner, announced that it will not fly to Moscow in the winter. Additionally, Lufthansa scaled back its number of flights to 63 to Moscow and St. Petersburg, down from 153 to nine Russian destinations four years ago. The poor economy has forced Russians to cancel vacations and the sanctions from Russia’s war in Eastern Ukraine have kept business people away from the country.

- According to Citigroup, economic expansion in most emerging markets lagged behind developed markets for the first time in 14 years in the second quarter of this year. Developing economies, excluding China, expanded 1.8 percent in the three months ended June, compared to 2 percent in advanced nations. Citigroup lowered its forecast for global growth in 2016 to 2.8 percent from 2.9 percent, making this the fifth-consecutive reduction this year.

(c) US Global Investors