On U.S. Growth: Near-Term Concern, Long-Term Optimism

“Humans are pattern-seeking, storytelling animals, and we are quite adept at telling stories about patterns, whether they exist or not.” —Michael Shermer, science writer

We’d be more worried about the economy’s effect on the market if the market hadn’t already corrected. Maybe the lion’s share of market movement from August to October wasn’t so much about the market reflecting upon itself as it was about the market anticipating an economic slowdown.

That notion seems reasonable: Investors are forward looking. Of course, the idea of the market anticipating a slowdown reminds us of economist Paul Samuelson’s quote about the stock market predicting “nine of the last five recessions.” Forecasting can bring a lot of false positives, where there’s a signal that sends the wrong message. The U.S. economy has proven pretty resilient and increasingly so in the face of variables such as low energy prices dragging on energy sector employment and a stronger dollar hampering export competitiveness.

Still, the latest employment report gave us a sense of foreboding. This could be because we spend too much time reading market news and tweets. It’s hard to not get caught up in the pundits’ calls for decline, secular stagnation, and any other sensational headline. It could also be because we don’t want to be the last ones to see—or admit—that something is wrong.

Why we’re near-term pessimists but long-term optimists

We’re optimistic for the growth outlook over the long term. Secular stagnation typically ends up being more cyclical than structural. Demographic challenges tend to turn into demographic dividends as different parts of the population enter the workforce or hang on in the workforce longer than many expected. Technological innovation also tends to cover up a multitude of messes.

So, it’s not the long term that we worry about. It’s the near term. If you can be a Rip Van Winkle investor, all the more power to you. We get caught up in the day-to-day turmoil, so forgive our shortsightedness as we contemplate the following market challenges.

The U.S. economy is not a rock, nor is it an island

To start, the U.S. is not as well insulated from a global slowdown or a stronger dollar as we’d like.

- There has been persistent weakness in the U.S. manufacturing sector.

- Employment has declined two months in a row.

- Factory orders have fallen 9 out of the past 12 months.

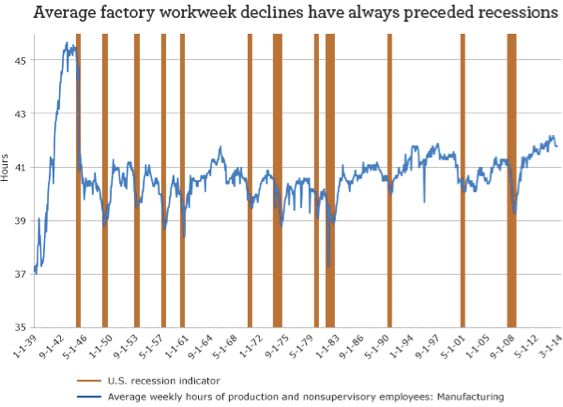

Those aren’t good developments, and they don’t look to be improving. The decline in the average manufacturing workweek was particularly troubling; it’s an indicator that always works but is often wrong. There have been many times when the average manufacturing workweek declined and there wasn’t an impending recession. However, there has never been a recession that wasn’t preceded by an average workweek decline.

Source: Bureau of Labor Statistics

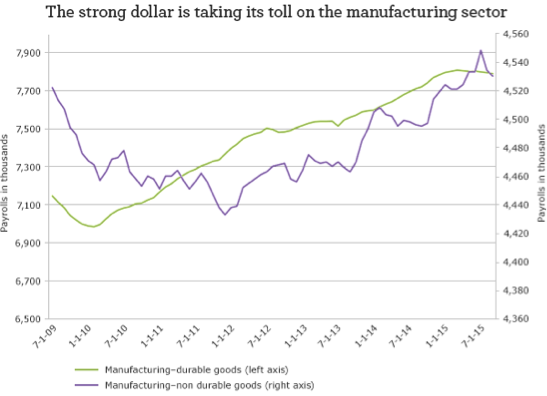

It shouldn’t be a surprise to anyone that low oil prices are spoiling the employment bonanza in the oil industry and the industries that support mining activities. However, low oil prices aren’t the only factor weighing on employment growth. The stronger dollar is also taking its toll, and that’s showing up in the manufacturing sector broadly.

Source: Bureau of Labor Statistics

Thankfully, the U.S. economy is bigger than manufacturing and factory output. Consumer spending and residential real estate are asserting themselves as the drivers of growth. We’re just not sure if the magnitude of growth from household spending will be enough for investors to pay up for earnings. It could be a challenging time for investors to get multiple expansion, where stock prices go up because the price/earnings ratio is increasing. Earnings will likely have to do the heavy lifting to push stocks higher, and third-quarter earnings season isn’t looking all that rosy.

Maybe we’re less pessimistic than the consensus

Oddly, we seem to be not as pessimistic about earnings as the consensus. In a warped way, our less-pessimistic pessimism might mean third-quarter earnings season could be good for stocks. While the consensus seems to be calling for a 4% to 5% drop in year-over-year earnings for the S&P 500 Index, we think the drop may be closer to 1% to 2%. Where we see a lower hurdle to clear, though, is in non-U.S. markets.

What could go wrong?

We may be wrong. And the things that could really make us wrong are:

- If the Federal Reserve (Fed) decides to hike interest rates despite the slowdown in growth

- If the European Central Bank (ECB) doesn’t signal a willingness to combat deflation with an extension or expansion of its asset-purchase program, which could augur poorly for equity markets

- If the Chinese government doesn’t give a resounding affirmation it will continue the important market reforms it announced a few years ago, that could be a real negative

This is why we are not ringing the recession bell, but we are saying the risks are now higher without further policy support from China, the ECB, and the Fed.

Emerging markets, emerging debt issues

There are also issues in many emerging markets. Lately, people seem to be talking more about the amount of dollar-denominated debt issued by emerging markets companies and their governments. This isn’t a new phenomenon; things really began to take off in 2011. Most of the rapid run-up in debt balances was in the Chinese economy (mainly construction) and Latin America (to support commodity exploration and production). Unlike previous episodes where debt accumulation and dollar strength conspired to create a debt crisis, the conditions are very different now; not only is the debt binge concentrated in certain countries and sectors, but exchange rates are more flexible than they were in, say, 1997 to 1998. Flexible exchange rates can serve as a shock absorber for some of these credit issues, turning what would have been a violent break into a slow bend.

What’s also not talked about enough is how that debt went to finance investment in property, plants, and equipment. Debt accumulation isn’t a bad thing if the debt is being used to acquire productive assets. However, not all the assets acquired will be productive. The Chinese government can build only so many vacant buildings, but perhaps that’s partially why China’s stock market bubble popped. Because assets were acquired instead of having debt-fueled consumption, debt ratios actually haven’t deteriorated significantly.

Portfolio implications for investors

Our near-term hesitation and long-term optimism can create a bit of cognitive dissonance for us, but it can also inform how you position a portfolio in these markets.

- We think that if we make it through October’s earnings season with better-than-consensus earnings, then we can breathe a sigh of relief.

- We’d slowly put cash to work and shift out of defensive sectors into more cyclical sectors.

- We’d also shift out of fixed income into equities as the month progresses. But, don’t be in a hurry. As the evidence trickles in on the health of the U.S. and Chinese economies, we’d take positive signs of life as reasons to build confidence in positioning more for growth.

- Conversely, without signs of renewed vigor, we’d keep it conservative.

Regardless of where you look for opportunities, we think international markets are the place to be. The growth slowdown worries are somewhat new to the U.S. Emerging markets and non-U.S. developed markets have been wrestling with this for years. Investors shouldn’t try to fight last month’s (or the past few years’) battles; there are plenty of new ones to fight. Positive signs of growth will likely emanate from non-U.S economies. Those will likely be the first beneficiaries of those signs.

This economic cycle is very different than previous ones. Global competition is fiercer now than ever. Our advocacy for international investing is just a way to get people to where we think the opportunities are. A U.S.-centric portfolio is way too narrow in scope. International markets corrected before, and more severely than, U.S. markets. Any recovery should play out in reverse.

Please visit our blog, AdvantageVoice, for additional viewpoints from Wells Fargo Asset Management’s investment strategists, portfolio managers, and practice management experts. You can also follow us on Twitter at @WFAssetMgmt for real-time updates. Are you an advisor or institutional investor? Check out our website for investment professionals.

The views expressed are as of 10-5-15 and are those of Dr. Brian Jacobsen, CFA, and John Manley, CFA, and Wells Fargo Funds Management, LLC. The information and statistics in this report have been obtained from sources we believe to be reliable but are not guaranteed by us to be accurate or complete. Any and all earnings, projections, and estimates assume certain conditions and industry developments, which are subject to change. The opinions stated are those of the authors and are not intended to be used as investment advice. The views and any forward-looking statements are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally, or any mutual fund. Wells Fargo Funds Management, LLC, disclaims any obligation to publicly update or revise any views expressed or forward-looking statements.

Wells Fargo Funds Management, LLC, a wholly owned subsidiary of Wells Fargo & Company, provides investment advisory and administrative services for Wells Fargo Advantage Funds®. Other affiliates of Wells Fargo & Company provide subadvisory and other services for the funds. The funds are distributed by Wells Fargo Funds Distributor, LLC, Member FINRA, an affiliate of Wells Fargo & Company.

Not FDIC Insured • No Bank Guarantee • May Lose Value

© Wells Fargo Asset Management