- In Defense of 2%

- Does the Dollar or Demand Drive Exports?

- U.S. Debt Ceiling Jitters Put to Rest, for Now

The October release of the consumer price index (CPI) is used to set cost-of-living adjustments for Social Security recipients. My mother is one of them, and she is convinced that the economists who measure the price level are cheating her out of a decent retirement. No amount of inflation seems to be enough for her.

So imagine the depth of my mother’s unhappiness a few weeks ago when the year-over-year change in the CPI was announced at 0.0%. After directing me to call Washington immediately to get this fixed, she asked a very cogent question. “Isn’t the Fed supposed to get me 2% every year?” she asked.

They are indeed. But the Fed, like central banks in other major markets, has struggled to meet its inflation mandate despite years of low interest rates and massive quantitative easing programs. The futility has prompted some to question whether central banks should continue pushing so hard to reach 2%, especially since lower inflation is beneficial for consumers.

Vítor Constâncio, the vice president of the European Central Bank (ECB) gave an impassioned defense of the 2% target during the ECB’s press conference last week. He noted four points:

a) Inflation has often been found to be overstated. Constâncio cited the work of the Boskin Commission, which reviewed the mechanics of the U.S. CPI 20 years ago. Up until that time, the price level was based on a fixed basket of goods which was updated infrequently. The Commission found that consumers substitute away from expensive goods and toward cheaper goods very interactively. As a recent example, high prices for beef in the United States have led to a shift toward chicken. Consumers also shift to lower-priced outlets to purchase the same product more cheaply. These behaviors limit increases in the cost of living.

The Boskin Commission found that inflation was systematically being overstated by more than 1% annually. Which means that reported inflation of 2% might actually be closer to 1%, further from the desired result.

If anything, the phenomena discussed in the Boskin report have become more powerful today. With a smartphone and the appropriate app, you can scan an item in a store, use the web to comparison shop and place an order in a matter of seconds. If this were properly captured by economic statisticians, “core inflation” (which excludes volatile components like food and energy) could be running close to zero at the moment.

b) Central bankers generally believe that deflation is much more dangerous, and much more difficult to dislodge, than excessive inflation. This is a main reason why monetary authorities decline to pursue price stability in the purest sense, which would be an inflation target of zero.

b) Central bankers generally believe that deflation is much more dangerous, and much more difficult to dislodge, than excessive inflation. This is a main reason why monetary authorities decline to pursue price stability in the purest sense, which would be an inflation target of zero.

This bias is rooted in the Japanese experience, where broad-based deflation set in and embedded itself in expectations. Some of the circumstances surrounding Japan’s struggles (adverse demographics, higher propensities to save, cultural rigidity) are not present in other markets. But policymakers are loathe to test whether the price level can be allowed to fall for any length of time without initiating a prolonged economic malaise.

It should be noted that several markets around the world have seen deflation over the past 12 months. Inflation in the United Kingdom and the eurozone is -0.1% over that interval, and Switzerland’s price level is lower by 1.4%. But for now, deflation is confined to a small group of products whose prices are not likely to continue downward at the same pace.

That fact has prevented inflation expectations from dropping too far. So the pernicious psychology of persistent deflation isn’t close to setting in.

c) Falling inflation raises the real value of debt, making it harder to repay. Said differently, it is easier to repay a fixed amount of borrowing with income that is growing by the rate of inflation. Since household and public debt in most parts of the world remain elevated, a stagnant price level makes a challenging situation worse.

d) Low inflation similarly raises real interest rates. This serves to tighten monetary policy at a time when central banks are trying to sustain easy credit conditions. Some have suggested that recent economic activity is being restrained in some markets as disinflationary forces increase real borrowing costs.

There is certainly logic in setting an inflation target, and 2% is not necessarily a bad objective. The challenge in the current environment is that global forces are pressing down on prices, and individual central banks are limited in their ability to press back. Doing so effectively might require levels of interest rates and quantitative easing that could create substantial distortions in markets and behavior.

There is certainly logic in setting an inflation target, and 2% is not necessarily a bad objective. The challenge in the current environment is that global forces are pressing down on prices, and individual central banks are limited in their ability to press back. Doing so effectively might require levels of interest rates and quantitative easing that could create substantial distortions in markets and behavior.

Further, deflation may not be such a bad thing in limited doses. If low prices are viewed as temporary, they can accelerate consumption as people sense a bargain. Money saved on things like gasoline, for example, is money that can be spent elsewhere. In light of this, the best central bank posture might be one which is not overly aggressive.

My mother would disagree. She doesn’t drive much anymore, so she doesn’t benefit from falling fuel prices. She doesn’t use the Internet to get the best prices on things. She’s frustrated by the low rates she is getting on her certificates of deposit. I can only imagine the abuse I am going to get on this front at Thanksgiving … better get an extra bottle of wine.

Understanding the Constraints on U.S. Exports

U.S. real gross domestic product (GDP) grew at an annual rate of 1.5% in the third quarter following a strong 3.9% increase in the prior quarter. A large reduction of inventories held down the result, but inventories record large swings in both directions and are not a source of concern going forward. But the soft trend of exports may persist and begs a solid explanation.

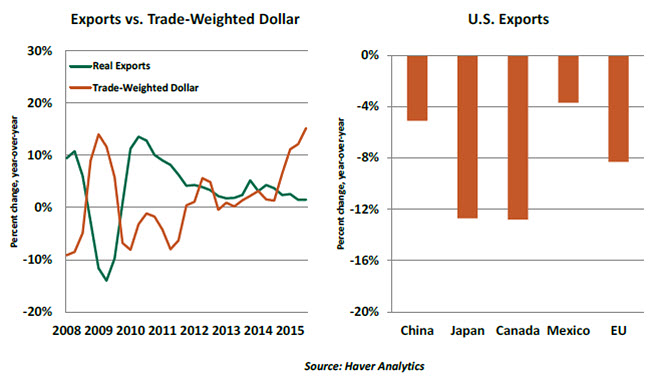

Exports of goods and services constitute 13% of U.S. GDP, but they grew only 1.5% from a year ago in each of the last two quarters. The West Coast port strike was responsible for the decline in exports during the first quarter. The deceleration of export growth in the latest quarter stems from the strength of the dollar and poor economic conditions abroad.

The trade-weighted dollar has risen 15% from a year ago; the magnitude of dollar appreciation is one of the largest in the last 25 years. Consistent with textbook explanations and historical experience, the growth of U.S. exports has moderated importantly and may fall off further if past intervals are any guide.

The strengthening of the dollar commenced in July 2014 when the trade-weighted dollar stood at 102.13 compared with the 120.37 mark as of this writing. The “price effect” from an appreciation of the dollar eventually makes U.S. products more expensive. The timing of this impact can be influenced by the degree to which producers have hedged currency risk and locked in prices. Exporters may also choose to accept lower profit margins to keep up market share for a time.

The top five export destinations for U.S exports are Canada (15% of total exports), Mexico (12%), China (7%), Japan (5%) and Germany (4%). U.S. exports to the European Union make up the lion’s share (22%). Export growth to each of the five top trading partners of the United States shows a decelerating trend.

The weakness in exports is not entirely due to the “price effect,” but it also reflects an “income effect.” A significant number of major U.S. trading partners are experiencing poor-to-soft overall economic performance. Their overall consumption of both domestic and imported products is growing very modestly. This further hinders growth of U.S. exports.

There may be hope that this “income effect” will ease going forward. Canada, the largest export market for the United States, registered a drop in real GDP in the first half of 2015. Economic conditions are projected to improve, particularly given the goals of the newly elected Canadian government to move away from fiscal austerity.

There may be hope that this “income effect” will ease going forward. Canada, the largest export market for the United States, registered a drop in real GDP in the first half of 2015. Economic conditions are projected to improve, particularly given the goals of the newly elected Canadian government to move away from fiscal austerity.

On October 23, the People’s Bank of China put in place the sixth round of monetary policy easing in the past year to support economic activity. Last week, the European Central Bank presented a dovish stance and indicated it stands ready to engage in additional monetary policy support to spur growth and lift inflation toward its target. The Bank of Japan remains in a supportive mode to ensure economic growth and an upward trend of prices.

These recent developments at the five top export markets of the United States suggest that underlying economic conditions of these economies are likely to show improvements. This should pare back the bite from a strong dollar and set the stage for better export growth in the coming year.

Debt Ceiling Drama Is Postponed, but Reforms Are Missing

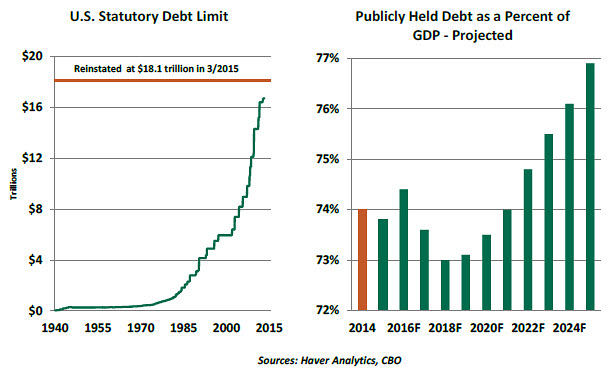

The debt ceiling drama took a temporary constructive turn this week as Congress passed the Bipartisan Budget Act of 2015 that suspends enforcement of the federal debt limit through March 2017. In other words, the federal government can pay its bills and debt ceiling confrontations will not feature until a new president is in office. A better solution would have been a permanent fix to arrest the growth of debt with consistent tax and spending changes.

The debt ceiling is the legal limit on the amount of federal debt the government can accrue. The limit applies to the sum of total publicly held debt outstanding (about $13 trillion) and debt incurred by borrowing from Social Security and Medicare trust funds (roughly $5 trillion).

The debt ceiling was enacted in 1917 to forego the requirement to pass legislation for each issuance of debt. More recently, the Budget Control Act of 2011 set the limit at $16.39 trillion, which was modified again to $18.1 trillion in March 2015. Since this change, the U.S. Treasury used extraordinary measures to borrow within the limit. A new deal was necessary as the Treasury ran out of options to prevent a debt default and/or a government shutdown.

The debt ceiling was enacted in 1917 to forego the requirement to pass legislation for each issuance of debt. More recently, the Budget Control Act of 2011 set the limit at $16.39 trillion, which was modified again to $18.1 trillion in March 2015. Since this change, the U.S. Treasury used extraordinary measures to borrow within the limit. A new deal was necessary as the Treasury ran out of options to prevent a debt default and/or a government shutdown.

There is more in the deal. Federal government spending declined each year between 2011 and 2014 and held back growth of real GDP, partly due to the caps on spending implemented in 2011. The latest agreement relaxes these caps, and federal government spending in 2016 and 2017 will increase by $80 billion, split between non-defense and defense expenditures.

The settlement also postpones reductions in Social Security Disability Insurance until 2022. A huge increase in Medicare deductibles and premiums that nearly a third of Medicare recipients would face is put off for another day. Early estimations suggest the new expenditures will add 0.1%-0.2% to growth of real GDP in the next two fiscal years.

The reprieve from debt ceiling drama is welcome. Congress working on reducing debt as a percent of GDP (projected to grow each year after 2018) would be a more productive approach. Tax and entitlement reforms in place of sequester caps is the way to go.

(c) Northern Trust