Next Time You Think of Emerging Markets, Think of Dividends

By Anthony Cragg and Stephen Kinney, CFA, of the Wells Fargo Advantage Emerging Markets Equity Income Fund.

The emerging markets have spent the past few months earning their reputation as members of a more volatile asset class. China’s slowdown has dominated headlines, with concerns that economic troubles there could spill over to an entire region. U.S.-based investors could be forgiven for indulging in the well-publicized tendency to engage in home bias. While we share the appreciation for emerging markets’ volatility, we think investors who choose to entirely avoid the asset class are unhelpfully lumping together many distinct markets into a homogenous mass. Yes, emerging markets are volatile, but investors don’t have to invest in all of them.

One way to differentiate between various investments and reduce volatility is to focus on dividends. To a U.S.-based investor, the idea that the emerging markets could provide a source of dividend income might seem strange. The stereotype of the emerging markets is that, if anything, they’re the part of a portfolio that provides a hefty dose of volatile growth, not a stream of more reliable dividend income.

To an extent this stereotype is true. Some developed markets investors shy away from emerging markets given the higher volatility of the asset class, while others have a lack of confidence in the financials produced by companies in the region. Both are valid concerns. The emerging markets are approximately 50% more volatile than the S&P 500 Index in terms of standard deviation, while several high-profile cases of fraud have put investors on their guard.

On the other hand, investors can mitigate these risks by investing in companies that have proven they can pay a high and sustainable dividend, which has shown to significantly reduce volatility and is a sign of stronger corporate governance.

Dividends are more prevalent in the emerging markets than usually thought

Above-average dividend-paying companies are often overlooked in emerging markets, for readily understandable reasons. Investors are usually searching for the strong growth characteristics exhibited by emerging markets countries and companies, while there are many misconceptions regarding the characteristics of dividend-paying companies within the asset class.

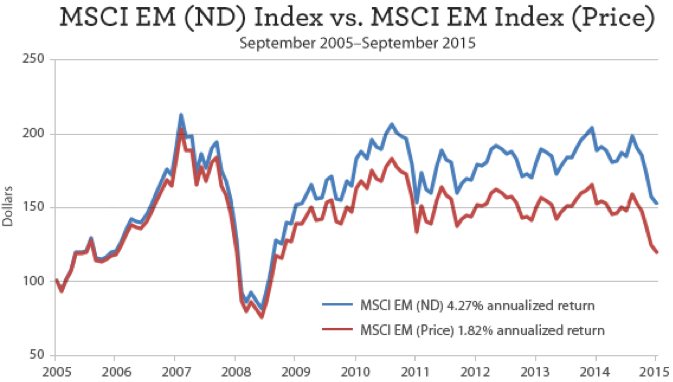

However, it’s fairly simple to show the prevalence of dividends in the asset class: Compare the emerging markets index that measures total returns (the MSCI Emerging Markets ND Index) and the index that measures the emerging markets index price (the MSCI Emerging Markets Price Index). Comparing the total return with the price index shows that dividends accounted for almost 57% of the annualized return of the asset class over the past 10 years through the end of September. (In general, the MSCI indexes do not consider regular cash dividends in price indexes, whereas total return indexes measure price performance as well as income from regular cash dividends.)

As shown below, the 10-year annualized return for the MSCI EM (ND) Index was 4.27% versus 1.82% for the price index, a difference of 2.45%.

Source: FactSet

Past performance is no guarantee of future results.

U.S.-based investors might be surprised to hear that 57% of emerging markets returns come from dividends. They might be more surprised that the comparable figure for developed countries (using the MSCI World Index) is only 45% of their total return over the same period. Dividends are arguably as important if not more important in emerging markets investing than investing in developed countries.

Not all dividends in the emerging markets are created equal

While dividends have been shown to be a substantial part of the total return in emerging markets, we do caution investors from taking a passive approach. Successful total return investing in emerging markets requires more than just buying a basket of high-yielding stocks, particularly in volatile and varied investment environments. High dividends in and of themselves are not indicators of the best investments. In fact, the opposite can be true, as high yields might indicate problems at the security, sector, or country level. Recent issues in Russia, Brazil, and more broadly in the energy sector clearly illustrate this point, given dividend yields that often reached double digits. However, a double-digit yield does not com¬pensate for huge negative returns, which in the case of Russia reached -46% in 2014. More recently, Brazil looked attractive at the beginning of the year, with an average dividend yield of 6.4%. Today, after nine months of scandals, political and economic challenges, a downgrade to junk status by Standard & Poor’s, and a -36% return in U.S. dollars, the country looks much less attractive. We want to caution that dividends will not always save the day.

The fact that not all dividend-paying companies in the emerging markets are equal, however, speaks to the broader point that investors shouldn’t paint the entire asset class with the same brush.

This website is accompanied by current prospectuses for Wells Fargo Advantage Funds®

Please visit our blog, AdvantageVoice, for additional viewpoints from Wells Fargo Asset Management’s investment strategists, portfolio managers, and practice management experts. You can also follow us on Twitter at @WFAssetMgmt for real-time updates. Are you an advisor or institutional investor? Check out our website for investment professionals.

The views expressed are as of 10-28-15 and are those of Anthony Cragg and Stephen Kinney, CFA, and Wells Fargo Funds Management, LLC. The information and statistics in this report have been obtained from sources we believe to be reliable but are not guaranteed by us to be accurate or complete. Any and all earnings, projections, and estimates assume certain conditions and industry developments, which are subject to change. The opinions stated are those of the authors and are not intended to be used as investment advice. The views and any forward-looking statements are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally, or any mutual fund. Wells Fargo Funds Management, LLC, disclaims any obligation to publicly update or revise any views expressed or forward-looking statements.

Wells Fargo Funds Management, LLC, a wholly owned subsidiary of Wells Fargo & Company, provides investment advisory and administrative services for Wells Fargo Advantage Funds®. Other affiliates of Wells Fargo & Company provide subadvisory and other services for the funds. The funds are distributed by Wells Fargo Funds Distributor, LLC, Member FINRA, an affiliate of Wells Fargo & Company.

Not FDIC Insured • No Bank Guarantee • May Lose Value

© Wells Fargo Asset Management