As we go to press tonight, the horrific and heartbreaking terrorist attacks are unfolding in Paris. We are saddened and sickened by what is taking place and our thoughts are first and foremost with the victims and their families.

Just yesterday I arrived back in the States after spending two weeks globetrotting and attending international investing conferences, first in New Orleans, then in Lima, Peru.

Most recently I was in Melbourne, Australia, for the International Mining and Resources Conference, one of the largest and most distinguished in the world, attended by not only top economists, geologists and CEOs of mining companies but also mining ministers from all corners of the globe.

I was encouraged to see that sentiment for gold was very positive. There’s a gold bear market here in North America, where the yellow metal has plunged to a six-year low of $1,083 per ounce on the strong U.S. dollar. But when priced in the weaker Aussie dollar, the precious metal is sitting at $1,520. As recently as last month, it touched $1,642.

This, combined with lower fuel costs, has been a huge boon to many gold companies in the world’s second-largest gold-producing nation after China. The country has excellent sponsorship by both the Australian and state government of Victoria, where Melbourne was built like San Francisco in a Gold Rush.

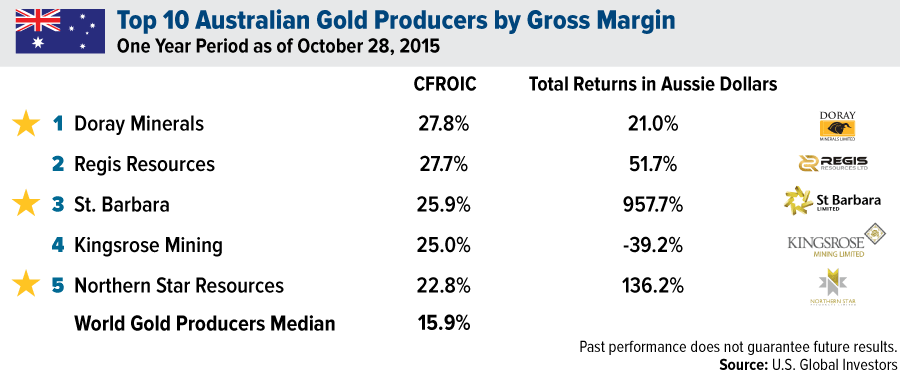

Strong Gross Margins and Cash Flow Returns

For the one-year period, the Australian dollar has fallen about 20 percent against the U.S. greenback, so gold looks very attractive—especially compared to iron ore and copper—and has lots of upside potential.

As a result, if you look at the top Aussie gold producers by gross margin, they all beat the median for world gold producers, currently at 15.9 percent. We own the names with a star next to them. Also note the total returns for the one-year period, shown in Aussie dollars.

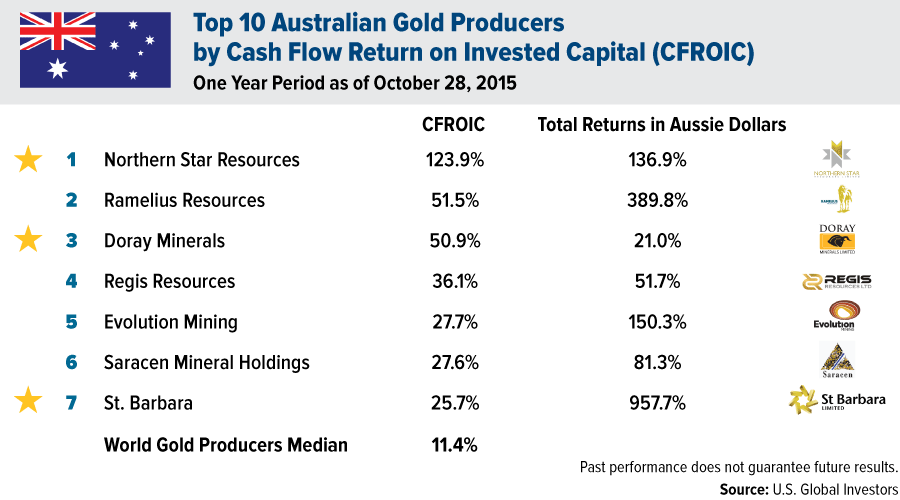

A similar story emerges when you look at the top Aussie gold producers by cash flow return on invested capital (CFROIC). The median is 11.4 percent, whereas Newcrest Mining, the lowest on the list, has a CFROIC of 12.9 percent.

We like to focus on stocks that offer high reserves per share, growth in sales, low debt to equity and high returns on invested capital. Australia has many outstanding companies whose financial fortunes have improved with a decline in the Aussie dollar. There’s little hope for iron ore to outperform due to China’s slowdown in mega-infrastructure projects, which means fewer imports.

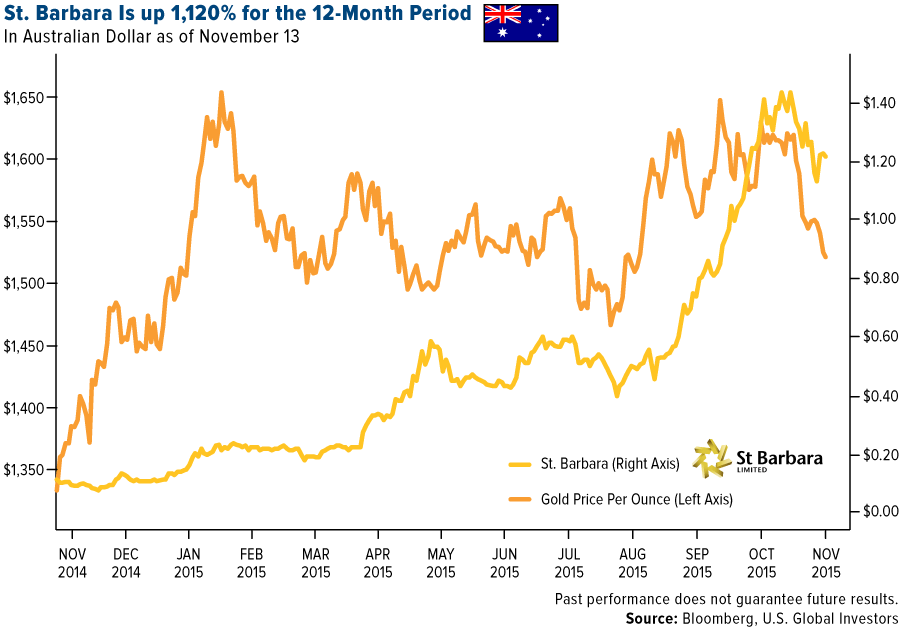

St. Barbara, one of our holdings, is up 1,120 percent for the 12-month period. The company operates in Western Australia and has a project in the New Zealand province of Papua New Guinea.

But gold companies aren’t the only ones reaping the benefits of a weak Aussie dollar and low fuel prices. Qantas Airways, Australia’s flagship airline, was up nearly 150 percent for the 12-month period.

Sights and Sounds of the International Mining and Resources Conference

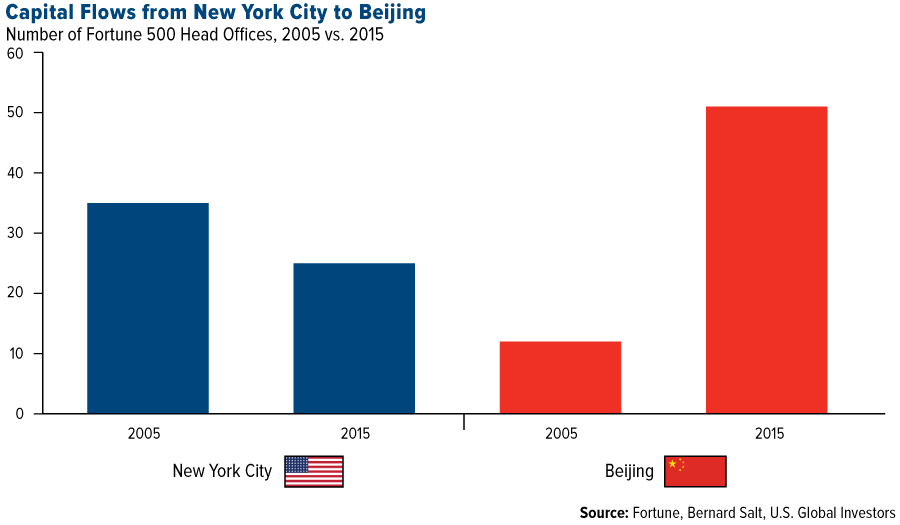

During the conference, I had the pleasure to meet Bernard Salt, a columnist for The Australian and a popular social commentator who has written widely on changes in demographics and social behaviors. His presentation focused on how shifting demographic trends are shaping the demand for commodities.

|

In a fascinating article published last month in The Australian, Salt shows that there’s a “tectonic shift in corporate power” happening right now, from New York City to Beijing. The number of head offices of Fortune 500 companies in New York has dropped from 36 to 25 between 2005 and 2015, while the number has risen in Beijing during the same time period, from just 12 to 51.

What’s going on? It’s not that the U.S. economy is struggling, Salt argues. It’s that China grew more rapidly over these 10 years—especially its middle class, a topic I’ve written and spoken about numerous times.

In any case, it appears as if Greater Beijing is now the world’s most powerful corporate city.

|

I also had the chance to hear Mark Bennett, managing director and CEO of S2 Resources, on the ingredients of a successful mining entrepreneur. The two-time recipient of the AMEC Prospector of the Year Award, he once served as chief geologist for LionOre Mining, which we used to own.

He’s also a phenomenally talented money manager, just as capable in a New York boardroom as he is in the Australian Outback. In 2009, Mark seeded gold and nickel miner Sirius Resources with $5 million, and soon before it merged with Independence Group this year, it was valued at $1.5 billion. You expect to see this kind of growth with a tech startup, not a mining company! This is just further proof of how exceptional Mark is.

|

Also presenting was Jim Askew, Chairman of the Board of Directors of OceanaGold. Jima is a mining engineer with over 40 years of international experience as a director and CEO. He also serves on the Board of Evolution Mining, one of Australia’s leading mining companies.

Another notable speaker was Dr. Mehdi Karbasian, Iran’s deputy minister for industry, mining and trade, whose presentation on investment opportunities in the country’s mining sector drew a packed house. (Iran is seeking $29 billion of investment, following the lifting of sanctions.) To me, what really stood out was how inexpensive labor and energy in Iran were. According to Karbasian, skilled labor costs about $300 per month, whereas in Australia it’s closer to $300 per day. And as for energy, a kilowatt hour (kWh) will set you back only a penny and a half. (In the U.S., it’s between 5 and 15 cents on average.) Meanwhile, Iran sits atop the second-largest natural gas reserves in the world, following Russia.

My question, then, is this: If energy is already so cheap and abundant, what does Iran possibly want with a nuclear power plant? It makes you wonder.

Central Banks and Retail Consumers Gobble Gold at Near-Record Pace

I want to end by sharing with you some good news. Judging from a new report from the World Gold Council (WGC), global central banks’ appetite for gold remains insatiable. In the third quarter, net purchases rose to 175 tonnes. This is the second-highest level ever recorded, nearly equaling the all-time high of 179.5 tonnes in the same period last year.

Russia and China were the top buyers, but we also saw some central banks return to the list of those that hold gold. The United Arab Emirates (UAE), for instance, reports that it now has 5 tonnes of the yellow metal, after holding none since 2003. The only net-seller for the quarter was Colombia.

Relatively low prices no doubt factored into the buying spree, but more than that, central banks recognize gold’s ability to hedge against inflation and monetary instability. It’s probably not appropriate to have 72 percent of your portfolio in gold, as the Federal Reserve does, but investors should nonetheless take note of what the banks are doing.

In fact, this might be what was on U.S. investors’ minds in the third quarter. Sales of American gold eagle coins shot up a whopping 200 percent year-over-year to 32.7 tonnes, a five-year record. I always recommend having around 10 percent: 5 percent in gold stocks, the other 5 percent in bullion or gold jewelry.

This never changes, whether we’re in a bear market or, in the case of Australia, a bull market.

Finally, just a reminder that on November 23, I’ll be giving the keynote address at the Silver Summit and Resource Expo in San Francisco. I invited you once before to attend the conference as my guest, and the response was very positive. But there’s still room for more! If you’d like a complimentary registration, send me an email.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 3.71 percent. The S&P 500 Stock Index fell 3.63 percent, while the Nasdaq Composite fell 4.26 percent. The Russell 2000 small capitalization index lost 4.43 percent this week.

- The Hang Seng Composite lost 2.22 percent this week; while Taiwan was down 4.19 percent and the KOSPI lost 3.32 percent.

- The 10-year Treasury bond yield fell 5 basis points to 2.28 percent.

Domestic Equity Market

Strengths

- The utilities sector was the best performer for the week, increasing by 0.33 percent versus an overall decline of -3.63 percent for the S&P 500. The sector saw increased investor interest amidst a flight to safety stemming from weak oil prices and soft readings on the health of the consumer.

- Plum Creek Timber was the best performing stock for the week, increasing 14.64 percent. The company will be bought by Weyerhaeuser for $8.4 billion. Under the terms of the deal, Weyerhaeuser will pay 1.6 shares of its stock for every Plum Creek Timber share. The new company will operate as a real estate investment trust with a combined equity value of $23 billion and control over 13 million acres of timberland.

- Brewing giant Anheuser Busch InBev officially announced its $105.5 billion plan to buy fellow brewer SAB Miller. As part of the deal, SABMiller will sell its 58-percent share in MillerCoors to its partner Molson Coors for $12 billion. The proposed brewing behemoth would have a major presence in the United States, China, Europe, Latin America and Africa.

Weaknesses

- Energy was the worst performing sector for the week, falling -5.97 percent versus an overall decline of -3.63 percent for the S&P 500. U.S. oil prices dropped near $40 a barrel Friday for the first time in three months as traders worried about growing crude oil inventories and slowing demand growth.

- Fossil Group was the worst performing stock for the week, falling -41.24 percent. The company’s stock suffered the worst decline in more than three years after its sales missed analysts’ estimates, fueling concern that the watch industry is mired in a slump and losing ground to wearable technology.

- Credit rating agency Fitch downgraded Volkswagen’s long-term debt by two levels, from A to BBB+. Fitch said the automaker’s wide-scale emissions fraud called into question its corporate governance and culture.

Opportunities

- A number of operating metrics are past the point of maximum pain in the telecommunications services sector. Sales growth has troughed. Consumer spending on telecom services is growing at a mid-single digit rate and grinding higher relative to total spending. Consumption trends drive sales growth and are tightly correlated with relative performance. As such, sales growth seems close to breaking into positive territory. Furthermore, pricing power pressure appears to be easing while the CPI for both wireless and traditional phone services has recovered to positive territory on a six month rate-of-change basis. Meanwhile, the strength of the U.S. dollar which depresses inflation expectations and thus, Treasury yields, could further highlight the sector’s yield appeal and domestic focus. The rising dollar hurts foreign-exposed sectors disproportionately. Relative valuations have typically been positively correlated with the currency. However, a gap has opened between relative valuations and the currency, which should close as profits outperform.

- The Federal Reserve’s determination to move away from the zero bound has turbo-charged the U.S. dollar. In turn, this will ensure that inflation expectations stay depressed, keeping financial conditions tight. Consequently, economic and profit backlash is probable if current trends persist. That would raise the appeal of utilities profits, which are already outperforming as electricity production climbs. As a result, the utilities sector is likely to regain relative strength

- An aging population and economic growth in the developing world will continue to create an almost insatiable demand for health care services and products.

Threats

- The biggest relative performance risk for banks may be the credit cycle. So far, there is not much evidence that credit quality is deteriorating outside of the energy sector. However, GDP growth is barely above Treasury yields, an indication that debt-servicing capacity may become more burdensome. Corporate bond spreads have broadly widened, suggesting that non-performing loans may begin to increase from historically low levels. When combined with tightening lending standards, loan loss reserving could accelerate in the coming quarters, dampening bank profitability. Furthermore, while an interest rate move away from the zero-bound would provide a positive sentiment lift to bank stocks, any real net interest margin benefit could be offset by a decline in longer-term yields. Expectations in forward markets are for a substantial yield curve flattening, given that the Fed will be draining liquidity while the economy is slowing and inflation expectations are depressed. Thus, net interest margins are likely to remain thin.

- Equity investors should prepare for volatility in the lead-up to the first Fed rate hike. While ECB President Mario Draghi talked up the possibility of further quantitative easing (QE) in the euro area today, Fed official Bullard made the case for a Fed rate hike in December. Additionally, the lack of support from profit fundamentals remains a headwind for equities.

- Following the U.S. equity market trough at the end of September, cyclical sectors have bounced the most, defensive sectors have fared the worst, except for health care, while interest rate sensitive sectors have remained stable. However, it could be dangerous to extrapolate the latest sector performance swings given the lack of corroborating evidence of any turning point in the global economy.

The Economy and Bond Market

Global equity markets stumbled this week as China reported continued weakness while expectations rose for a U.S. Federal Reserve interest rate hike in December. Germany’s slowing growth highlighted its vulnerability to China’s weakness and increased the likelihood of more European Central Bank (ECB) stimulus in December. U.S. stock volatility rose, with the Chicago Board Options Exchange Volatility Index (VIX) climbing sharply from 15 to around 20 during the week. The yield on 10-year U.S. Treasuries fell below 2.30 percent on Friday. As commodity prices fell near multiyear lows, the price of crude oil tumbled close to $40 and $44 per barrel for WTI and Brent, respectively.

Strengths

- The University of Michigan preliminary consumer sentiment index rose to 93.1 in November from 90 in October. The improvement was driven by a firming labor market and low fuel prices.

- The Labor Market Conditions Index came in at 1.6 for October, above the expected 0.9 and up from 1.3 in September (revised up from 0.0). August was also revised up to 1.9 from 1.2, July was revised up to 1.6 from 1.1, June was revised up to 1.8 from 1.5, and May was revised up to 1.7 from 1.6. All in all, this report is consistent with the solid employment report in October.

- Initial jobless claims were reported at 276,000 for the week ending November 7, in line with the expected 270,000 and unchanged from the prior week. The four-week moving average moved up to 267,750 from 262,750 in the prior week. This is still a low level of claims, suggesting little firing.

Weaknesses

- The Organization for Economic Cooperation and Development trimmed its global economic growth forecasts. Worldwide GDP is now expected to grow 2.9 percent in 2015 and 3.3 percent in 2016, down from the OECD’s earlier forecasts of 3 percent and 3.6 percent, respectively.

- U.S. import prices fell 0.5 percent in October, a bigger decline than expected as the strong U.S. dollar and weak global demand continue to push down the prices of imported goods, including petroleum. For the 12 months through October, prices fell 10.5 percent.

- U.S. retail sales edged up 0.1 percent in October, below a median forecast of 0.3 percent. Automobile sales fell 0.5 percent after rising 1.4 percent in September, contrasting with industry reports of robust October auto sales of more than 18 million units annualized. Core retail sales –– excluding autos, gasoline, building materials and food services –– rose 0.2 percent after an upwardly revised 0.1 percent gain in September.

Opportunities

- Historically, Federal Reserve tightening cycles typically unfold in two distinct phases. The first phase begins with a surprise moment where the reality of rate hikes sinks in and bonds sell off. The second phase is one where short-term rates grind higher, but long-term bond yields stabilize or even decline. For example, in the last tightening cycle, bond investors suffered losses totaling 5.4 percent between March and May 2004. However, by the time the Fed hiked rates for the first time in June 2004, treasuries had already resumed their bull market.

- Government leaders will gather for a G20 meeting November 15-16. The meeting comes amid economic turmoil in emerging markets and uncertainties about the direction of economic policy in the better-performing developed countries. It will be important to be attentive for clues about whether fiscal spending is back on the global agenda.

- The price action in Treasuries over the last few weeks has challenged the downtrend in yields, especially the post-payrolls reaction that saw the two-year Treasury yield reach 0.90 percent, a five-year high. However, the U.S. dollar is now higher than it was in August, which is key for the Treasury market. If the dollar continues to shoot higher in response to rising Fed liftoff probabilities, it will eventually drag down U.S. growth and inflation, limiting the number of Fed rate hikes. Although the Fed is likely to hike in December, slow growth and a strong currency mean that the odds of "one and done" are high. This favors lengthening the duration further if the 10-year Treasury continues to move higher in the coming weeks.

Threats

- Both the Federal Open Market Committee (FOMC) and European Central Bank (ECB) will release the minutes of their latest meetings on Wednesday and Thursday, respectively. The two central banks are on very different policy courses, which is likely to translate to currency volatility.

- While incoming U.S. data is unlikely to sway the Fed much (CPI and the survey of homebuilders released on Tuesday, housing starts on Wednesday), a further rapid strengthening in the U.S. dollar could interfere with Fed's intentions to hike this year.

- The Philadelphia Fed Business Outlook will be released next Thursday. With the one-month trend below the three-month trend, odds are that the results will disappoint the expected -0.3 percent decrease.

![[thumb]](/images/content_image/data/f1/f19f7cb63eb0d38085e0c94f2029117a.jpg)

November 10, 201511 Numbers that Explain the World’s Largest Shopping Holiday |

![[thumb]](/images/content_image/data/2d/2d7875063703ca1c9dbdeccca247abad.jpg)

November 9, 2015Get Ready for Commodity Liftoff: Global Manufacturing Just Made a HUGE Move! |

![[thumb]](/images/content_image/data/9c/9c5091a90380565198c13bb733b3c1b3.jpg)

November 4, 2015How Rare Are Municipal Bankruptcies? A Lot Rarer Than You Think |

Gold Market

For the week, spot gold closed at $1,082.31 down $7.49 per ounce, or 0.69 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, actually lifted a bit gaining 0.37 percent. Junior miners underperformed seniors for the week as the S&P/TSX Venture Index lost 1.94 percent. The U.S. Trade-Weighted Dollar Index backed off 0.25 percent for the week.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Nov-10 | CH Retail Sales YoY | 10.90% | 11.00% | 10.90% |

| Nov-12 | GE CPI YoY | 0.30% | 0.30% | 0.30% |

| Nov-12 | US Initial Jobless Claims | 270k | 276k | 276k |

| Nov-13 | US PPI Final Demand YoY | -1.20% | -1.60% | -1.10% |

| Nov-16 | EC CPI Core YoY | 1.00% | -- | 1.00% |

| Nov-17 | GE ZEW Survey Current Situation | 55.2 | -- | 55.2 |

| Nov-17 | US CPI YoY | 0.10% | -- | 0.00% |

| Nov-18 | US Housing Starts | 1160k | -- | 1206k |

| Nov-19 | US Initial Jobless Claims | 270k | -- | 276k |

Strengths

- Gold remained the strongest of the precious metals this past week, seemingly stuck in a narrow trading range for much of the week. Silver did a little worse, falling 3.52 percent, perhaps related to Bank of America warning that silver could hit $12 per ounce on weak industrial and investment demand.

- Low gold prices in the third quarter attracted bargain hunters, with U.S. buyers buying up far more coins and bars than they did in any other quarter over the past five years. Demand surged by 207 percent from a year ago.

- Central banks and other institutions boosted gold purchases to the second-highest level on record in the third quarter as countries including China and Russia sought to diversify their foreign-exchange reserves. Net purchases were 175 metric tons, nearing the record 179.5 tons in the same quarter a year earlier, and up from 127.9 tons in the preceding three-month period. Further, China probably boosted central bank gold holdings yet again in October, raising them by about 14 metric tons.

Weaknesses

- Palladium tumbled 13.24 percent and platinum followed with a loss of 8.27 percent for the week. Total known holdings in palladium and platinum ETFs fell 9.38 percent and 6.78 percent, respectively, in October. The slide continues in November with palladium and platinum holding down another 6.27 percent and 6.00 percent, respectively. Pent up demand for autos are thought to have peaked industrial demand in China has been slack.

- In the past several months, Venezuela has liquidated about 19 percent of its gold holdings as a result of the plunge in their oil related revenue, which accounts for 95 percent of the country’s exports, with upcoming bond payments fast approaching.

- Chow Tai Fook, the world’s largest jewelry retailer, issued a profit warning saying it expects net profit for the half year ended September to fall by 40-50 percent from a year ago. However, this might relate mostly to their operations earlier in the year as the World Gold Council reported that the gold market started the third quarter with a jolt. Further, they noted China’s historic devaluation of the yuan during the summer fueled a gold bar and coin buying spree in the country as investors sought to protect themselves from further market volatility. On a separate note, Canaccord Genuity reported that Alamos Gold’s third quarter results represented a miss relative to their forecasts and consensus on most metrics. Consolidated production was lower than their forecast and total cash costs were higher, which in turn resulted in lower than expected earnings and cash flow. Alamos Gold is also the worst performing North American gold miner this year, falling over 50 percent year to date. While this could prompt bargain hunting speculators, the effect of tax loss selling as the year closes out could dampen the stock further.

Opportunities

- A recent report by Paradigm Capital notes that gold’s recent meltdown will likely define the bottom of this cycle and sets the stage for a significant late 2015/early 2016 rally for the metal. This is important for the equities as historically they have anticipated the upturn. With that in mind, Klondex Mines reported very positive results for third quarter. They generated operating cash flow of $13.3 million, increased cash by $5.8 million, and eliminated its senior notes. Further, they raised annual production guidance for the second consecutive quarter.

- Integra Gold reported that its Triangle resource deposit estimate exceeded expectations. The company reported a revised indicated and inferred resource estimate based on an additional 27km of drilling. The indicated resource increased 14 percent while the inferred resource increased 344 percent. These results are very positive and validate the 15 percent stake taken in the company by Eldorado Gold earlier in the year. Separately, Gold Standard Ventures announced a substantially higher grade oxide gold zone north of its Dark Star Deposit in Nevada, including 157 meters of 1.51 grams per gold ton. The company said the new gold zone has an order of magnitude better grade and thickness than anything previously drilled at Dark Star. This is another junior explorer which has seen a senior miner take a significant stake in it, in this case by Oceanagold.

- Barrick reached an agreement to sell certain non-core Nevada assets for $720 million, above the higher end of market expectations. Barrick’s focus on balance sheet recapitalization has merit and shares could provide investors attractive beta as gold prices recover from recent lows.

Threats

- According to UBS, the recent gold monetization schemes launched in India have high chances of succeeding. While the rupee has depreciated by 47 percent against the U.S. dollar over the past five years, gold in rupee terms is up 28 percent. This could prompt locals to monetize their gold holdings.

- In India, a country where an estimated 800 million people depend on agriculture and many revere gold as ornament and store of wealth, farmers flush with cash during harvest season have historically been big buyers of bullion. Sales usually surge this month in the main festival season of Diwali. However, this year the El Nino weather pattern has led to the driest monsoon season in six years, reducing farm output and incomes. Demand is so weak among the rural Indians who make up almost 60 percent of domestic gold consumption that dealers who stocked up before Diwali are offering some of the biggest discounts in decades.

- Fed officials have recently been drawn from just two backgrounds – academics and alumni of Goldman Sachs. The announcement that Neel Kashkari will become president of the Federal Reserve Bank of Minneapolis marked the third Goldman Sachs alumnus in a row to be picked to become a Fed bank president. Of the 17 Fed officials in office next year, all but three will have professional backgrounds as academics or with Goldman Sachs. This poses a serious risk of groupthink within the Fed. The narrow range of backgrounds may lead to a central bank that is thin on expertise when it comes to the responsibilities that extend beyond monetary policy.

Energy and Natural Resources Market

Strengths

- Railroads were the best performers this week. The group experienced a mild pullback following news of the Keystone Pipeline XL rejection. The S&P Supercomposite Railroads Index fell just 0.4 percent this week.

- Chemicals were also a strong performer this week, as global demand for agricultural chemicals continues to grow. The S&P Supercomposite Chemicals Index retreated 2.0 percent.

- Iron and steel stocks performed strongly this week relative to their peers, as the industry’s fundamentals remain healthy. The Bloomberg World Iron/Steel Index fell 2.1 percent this week.

Weaknesses

- Metals and mining underperformed this week in response to a strong U.S. dollar and increased interest rates. The S&P/TSX Capped Metals & Mining Index fell 14.5 percent this week.

- Energy stocks suffered this week as oil headed toward a second weekly decline, trading near its lowest level in two months. The S&P/TSX Capped Energy Index retreated 8.2 percent.

- Clean energy stocks slumped this week, as they currently cost more than energy from fossil fuels and rely heavily on government subsidies. The Nasdaq Clean Energy Index fell 7.5 percent this week.

Opportunities

- According to Saudi Arabia’s deputy oil minister, “Oil prices may rebound as investments will be durably cut worldwide. Just like expectations in 2008 that prices would rise to $200 a barrel were proved wrong, the recent assertion that the oil price has shifted to a new low, structural equilibrium will also turn out to be wrong.”

- China continues to stimulate its slowing economy and many analysts are expecting even larger stimulus packages to be implemented in the near future.

- Natural gas futures climbed as colder weather was forecast to creep across the U.S. Midwest and Southeast, potentially strengthening demand for the power plant and heating fuel. According to CWG Weather Group, temperatures will likely be lower than normal across the U.S. heading into Thanksgiving week.

Threats

- The Federal Reserve’s comments this week, along with further foreign easing particularly in China and the eurozone, will likely put further upward pressure on the dollar.

- A contraction in China’s trade flows shows little alternative for the nation’s leaders other than injecting support for domestic demand as they struggle to achieve their growth target. Overseas shipments dropped 6.9 percent in October in dollar terms, a bigger decline than estimated by all 31 economists surveyed, according to Bloomberg. This could lead to a weaker demand for coal, iron and other commodities.

- Global growth remains unimpressive and there has yet to be an effective catalyst to spur it.

China Region

Strengths

- China A Shares was the best performing market in Asia this week, as PMI trends improved and the market entered a technical bull market, more than 20 percent higher from the August 26 low. The Shanghai SE Composite Index fell 0.25 percent this week, the mildest pullback among Asian markets.

- Financials was the best performing sector in Asia this week, following China’s decision to resume initial public offerings in its domestic A Share market by year end after a five-month freeze. The MSCI Asia Pacific ex Japan Financials Index fell 0.58 percent this week, the mildest pullback among the sectors.

- The Hong Kong dollar was the best performing currency in Asia this week, remaining unchanged despite other Asian currencies weakening.

Weaknesses

- Taiwan was the worst performing market in Asia this week, as Taiwanese exports have continued to contract sharply. The Taiwan Stock Exchange Index retreated 4.19 percent this week.

- Materials was the worst performing sector in Asia this week, with copper smelters and iron ore miners taking a hit. The MSCI Asia Pacific ex Japan Materials Index lost 4.41 percent this week.

- The South Korean won was the worst performing currency in Asia this week, weakening by another 1.87 percent, as China’s slowing economy, falling commodity prices and a looming U.S. interest-rate increase all took their toll on the currency.

Opportunities

- Tangibly recovering new home sales in the context of continued decline of land purchases and housing starts in Chinese major cities should bold well for future pricing power of Chinese property developers by shrinking market supply, given the lengthy lead time from land acquisition to new supply launches. Relaxed approval of local corporate bond issuance for developers should also help reduce funding costs for developers, given falling interest rates domestically and less risk associated with foreign currency debt. Quality Chinese property developers should continue to benefit from tighter supply expectations and favorable government policy.

- Beijing is continuing to announce more targeted fiscal measures in order to lift economic growth. According to EvercoreISI, this week, Chinese Premier Li said China will increase tax cuts, and that the deficit can be expanded. Although the yuan has weakened in recent days as the Fed hike is contemplated, many analysts do not believe China’s currency will be dragged materially higher by U.S. rate hikes.

- Malaysian policy makers have been struggling to boost confidence in its economy and finances since oil prices started to fall last year and as allegations of financial irregularities at a state investment company hurt sentiment. According to central bank Governor Zeti Akhtar Aziz, the Malaysian ringgit remains, “significantly undervalued and the risks to economic expansion are unlikely to materialize with exports still strong.” The ringgit doesn’t reflect fundamentals with the nation’s current account in surplus, unemployment at about 3 percent and inflation within Malaysia’s long-term average. Export growth remains strong, while exports and industrial production beat economists’ estimates in September.

Threats

- According to Mohamed El-Erian, chief economic advisor at Allianz and chair of President Obama’s Global Development Council, there is a 70 percent chance that the Fed will hike rates in December. This dynamic may add to the positive momentum of a strengthening U.S. dollar in the short term, and rekindle volatility in emerging Asian currencies and equities as a result of further liquidity exodus from the region.

- The Bank of Korea left its benchmark repo rate unchanged at 1.5 percent for the fifth consecutive month as expected. Analysts predict that the BoK is expected to hold until at least after the U.S. Fed’s December meeting. Although the central bank said that the economy was on a recovery track, it has since revised its 2015 GDP forecast down 10 basis points to 2.7 percent.

- According to Bloomberg, China’s broadest measure of new credit slumped to the lowest in 15 months in October, adding to evidence six central bank interest-rate cuts in a year have yet to spur a sustained pick up in borrowing. Aggregate financing fell to 476.7 billion yuan ($75 billion), according to a report from the People’s Bank of China on Thursday. That was lower than all 25 economists’ projections and less than half the median forecast 1.05 trillion yuan. The data rounds out a week of mixed readings that have showed falling exports, tame inflation, slowing industrial output, and a rare bright spot in the form of increased retail spending. The readings underscore the government’s challenge to kick start growth in an economy weighed by overcapacity and debt.

Emerging Europe

Strengths

- Hungary was the best performing market this week, gaining 49 basis points. Third quarter gross domestic product was reported at .5 percent, in line with expectations. However, the year-over-year change in GDP was reported at 2.3 percent, below the expected growth of 2.5 percent. Year-over-year inflation increased to .1 percent from zero.

- The Turkish lira was the best performing currency this week, gaining 1.9 percent against the dollar. There are still uncertainties on the macro front in Turkey, but as the AKP party moves forward with formation of its government, the lira is strengthening.

- Healthcare was the best performing sector among Eastern European markets this week.

Weaknesses

- Greece was the worst performing market this week, losing 3.66 percent. For the second straight week, the Hellenic exchange was dragged down by banks, continuing its sell off during the recapitalization process.

- The Russian ruble was the worst performing currency, losing 3.5 percent against the dollar, pulled down by the Brent crude oil price which was down 8.6 percent in a week. Car sales in Russia dropped by 38 percent year-over-year, suggesting weakening consumer spending. The Russian gross domestic product fell 4.1 percent in the third quarter vs economists’ estimates of 4.4 percent.

- Telecommunication services was the worst performing sector among Eastern European markets this week.

Opportunities

- Turkey posted a positive current account balance for a second straight month. September surplus was reported at $95 million, beating a median estimate in a Bloomberg survey for $80 million deficit. Turkey strongly relies on capital inflow to finance its current account deficit, much better than expected data is an encouraging signal for the lira.

- Industrial output in the eurozone fell for a second straight month in September and gross domestic product for the third quarter was reported at .3 percent vs prior .4 percent. Weaker economic data points to a slowdown in economic growth, putting pressure on the European Central Bank to expand its stimulus program in December.

- Poland’s new party Law & Justice proposed Mateusz Morowiecki, the chief executive officer of Bank Zachodni, for the post of deputy prime minister in charge of economic affairs which could smooth investor worries about the party’s budget policies.

Threats

- Russia’s trade surplus narrowed in September to the lowest in seven months as sanctions and failing oil prices cut export revenue. The World Bank predicts Russia will experience, for the first time since the 1998-1999 financial crisis, a significant increase in the poverty rate, which declined significantly since 2000 when President Vladimir Putin assumed power and oil prices began to rise.

- The European Commission, in its annual report on the progress of Turkey and other membership candidates, criticized Turkey for backsliding on key democratic reforms, including the independence of the judiciary, freedom of the media and the protection of human rights. The EU and Turkey have been in membership talks since 2005 but progress has been minimal in recent years.

- After a good start, the Greek government fell behind schedule with the approval of the legislative changes to the foreclosure laws. European Union financial aid valued at Eur 2 billion was delayed but will be released to Greece after delivery of new foreclosure rules and other promised overhauls.

(c) US Global Investors