Why Reforms Are Sparking Growth in These Two Regions

By Jeff Everett, Dale Winner, and Venk Lal with the EverKey Global Equity team, which manages the Wells Fargo Advantage International Equity Fund.

If you’re reluctant to consider opportunities in foreign companies, you’re not alone. Many investors find it hard to gauge the risks and rewards of investing outside the U.S. In the news, we see other countries’ economic developments play out in snapshots or opinion pieces—often focusing on short-term data or what’s perceived to be wrong. But here’s what the headlines may not be telling you: Non-U.S. regions from Asia to Europe are home to economic comebacks and companies that are growing their earnings.

Many investors may be surprised to learn that:

- Japan’s equity market has outperformed the U.S. equity market over the past 3 years after an almost 20-year economic struggle.

- Italy’s equity markets have topped the U.S. over the past 12 months after three consecutive recessions.

These numbers don’t represent an overnight phenomenon. Rather, they’re the result of two factors: monetary policies designed to jump-start bank lending and business investment and reforms designed to make the art of doing business more efficient, transparent, and unhindered by red tape. So let’s take a closer look at developments in Japan and Italy and then contrast the risk/reward dynamic with the current market environment in the U.S. You might be surprised at what you see.

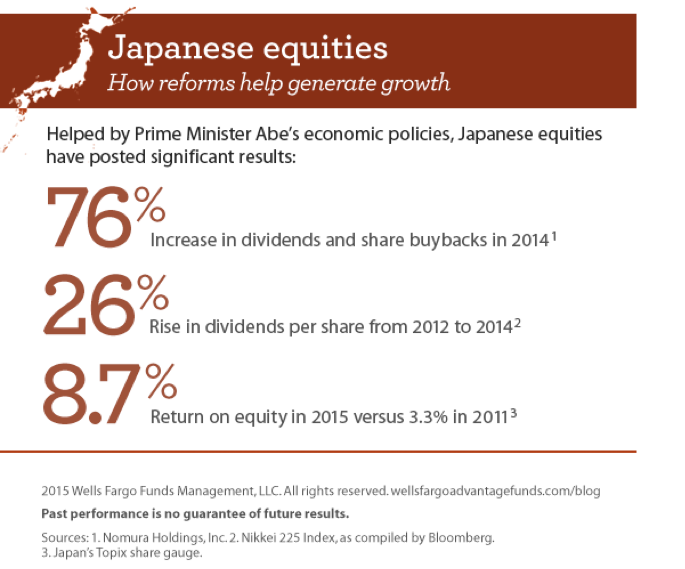

Japan: A case study in reform-based growth

When it comes to Japan’s economy, experts love to focus on short-term data. Many investors question whether Prime Minister Shinzo Abe’s growth-centric policies have worked. Our take: Don’t be misled by the myopic headlines. Abenomics involves multiyear changes from the financial, government, and private sectors. While economic recoveries take time, a host of data-driven evidence already points to improving profitability for Japanese companies. Consider these statistics:

What’s driving results for Japanese equities? Here are just a few of Abe’s policies that are creating a foundation for growth:

- Accountability: Abe’s reforms are making companies more accountable for their balance sheets in a broader effort to improve transparency and responsiveness to shareholders. This is a main driver behind Japanese equities’ increased dividends and stock buybacks. Now, companies are less inclined to hoard capital and more inclined to give it back to investors.

- Board reform: Continuing Abe’s accountability theme, Japanese companies are now required to name at least two independent directors within six months of their next shareholder meeting. By last June, nearly 75% of the 1,800 companies listed on the Tokyo Stock Exchange’s first section had at least one outside director, up from less than one-third a decade earlier.

- Strategic zones: Abe designated six strategic economic zones with loosened regulations to rekindle capital investment, spark new development projects, and improve labor conditions for foreign firms’ employees. The zones include Japan’s capital, Tokyo, home of 37.8 million residents and 51 of the Fortune Global 500’s companies.

These examples are just the beginning in Japan. In the coming year, Abe also intends to lower the nation’s corporate tax rate by 3.3 percentage points to help spark business investment.

Italy: A long-overdue comeback story

Investors may wonder how Italian equity markets could have outperformed U.S. equity markets over the past year. Until recently, Italy’s economy was in such dire straits that economists lumped it in with the beleaguered economies of Portugal, Greece, and Spain. Thanks to the European Central Bank (ECB) and Italy’s reform-minded prime minister, the country—and many Italian companies—are staging a long-overdue comeback.

Let’s start with the fundamentals. As with Japan and other nations, Italy’s economy is benefiting from:

- Lower currency versus the U.S. dollar, which helps tilt export profits in Italian companies’ favor

- Lower commodity prices, which bolster Italian industries such as manufacturing and petroleum refining

- Lower credit rates stemming from central bank policies to increase business lending

On that last point, the ECB’s 1.1 trillion euro quantitative easing program has injected extra liquidity—and much-needed confidence—into Europe’s banking system. Looking at the entire eurozone, nearly 40% of European banks have used funds from the ECB’s program to lend to companies. Our hope is that Italian companies will take full advantage of lending opportunities and in turn allocate capital toward growing their businesses.

In the meantime, Italy’s Prime Minister Matteo Renzi continues implementing reforms to generate growth—and tackle the nation’s most vexing obstacles to doing business. This includes:

- Employment: Renzi passed several reforms to help Italian companies manage their workforces, such as tax incentives that encourage companies to offer permanent job contracts versus temporary contracts that have left employees working in uncertainty for years.

- Privatization: Renzi is privatizing government-owned enterprises, which creates opportunities for Italian businesses. Renzi’s 40% privatization of Italy’s postal service paved the way for an Italian asset management firm to sell financial products to consumers through regional post offices.

Next up for Renzi’s reform agenda: a 35 billion euro ($38 billion) tax-cut plan for 2016 to 2018, which includes relief for businesses as well as privatization plans for air and rail transportation agencies.

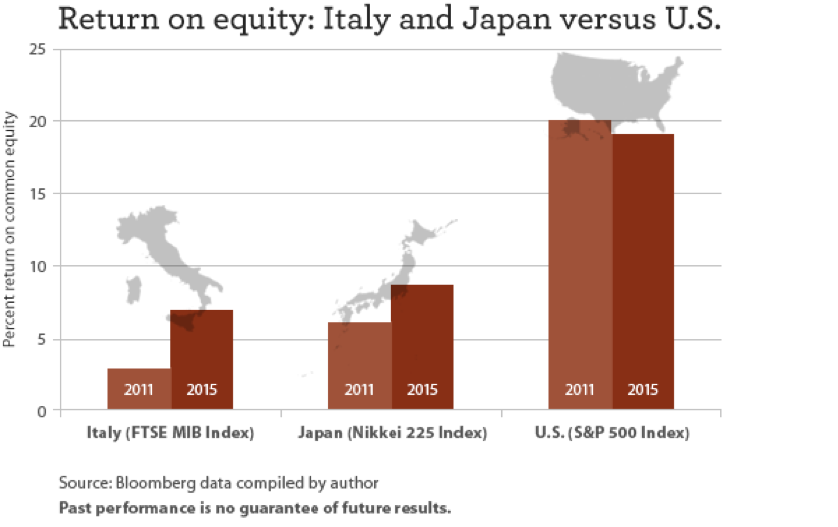

Risk or reward? How international and U.S. markets stack up

For many U.S. companies, profit margins have reached all-time highs and return on equity is approaching peak levels. Valuations, while not excessive, are high, as we believe U.S. equities are currently priced not to perfection but to a continuation of extremely good times. Compared with businesses in other regions of the world, U.S. firms face earnings headwinds in the form of rising wages, rising interest rates, and no immediate sign of lower corporate taxes. Lower energy prices remain a bright spot for U.S. manufacturers.

Contrast those conditions with companies in Italy and Japan, where return on equity has risen, stocks trade at lower valuations than the global average, margins have improved and continue to improve, and there’s still significant room for earnings growth—all while regional governments are passing reforms to foster improved business climates.

In our next blog post, we’ll discuss how investors should factor regional thinking into their diversification strategies, to capitalize on diverging economic conditions. We’ll also explore how companies in regions such as Italy, Japan, and Germany have been making strategic moves, to position themselves for success, when their respective countries’ recoveries kick into full gear.

Please visit our blog, AdvantageVoice, for additional viewpoints from Wells Fargo Asset Management’s investment strategists, portfolio managers, and practice management experts. You can also follow us on Twitter at @WFAssetMgmt for real-time updates. Are you an advisor or institutional investor? Check out our website for investment professionals.

The views expressed are as of 11-17-15 and are those of Jeff Everett, Dale Winner, Venk Lal, and Wells Fargo Funds Management, LLC. The information and statistics in this report have been obtained from sources we believe to be reliable but are not guaranteed by us to be accurate or complete. Any and all earnings, projections, and estimates assume certain conditions and industry developments, which are subject to change. The opinions stated are those of the authors and are not intended to be used as investment advice. The views and any forward-looking statements are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally, or any mutual fund. Wells Fargo Funds Management, LLC, disclaims any obligation to publicly update or revise any views expressed or forward-looking statements.

Wells Fargo Funds Management, LLC, a wholly owned subsidiary of Wells Fargo & Company, provides investment advisory and administrative services for Wells Fargo Advantage Funds®. Other affiliates of Wells Fargo & Company provide subadvisory and other services for the funds. The funds are distributed by Wells Fargo Funds Distributor, LLC, Member FINRA, an affiliate of Wells Fargo & Company.

Not FDIC Insured • No Bank Guarantee • May Lose Value

© Wells Fargo Asset Management