What We’re Paying Attention to Following the Paris Attacks

A week ago today, 129 lives were brutally cut short when assailants affiliated with the terrorist group ISIS, also known as the Islamic State, stormed Paris in a series of coordinated attacks. Along with the rest of the world, we were shocked and saddened as the tragic news unfolded, worsening as the night progressed. Our thoughts are with the victims’ families and friends.

For us, the atrocity struck especially close to home, as one of our portfolio managers, Xian Liang, was in the city at the time of the attacks. We’re extremely grateful he and his wife returned home safe and sound. I wish the same could be said for the victims in Paris that day, the 224 on the Russian jet brought down by an ISIS-built bomb, the hostages in Mali today, and for many others whose lives have been affected by the global scourge of terrorism.

We Take Our Role as Fiduciaries Seriously

As money managers, it’s our duty and responsibility to be cognizant of such geopolitical events—large and small, good and bad—and to consider all of the possible ramifications. The consequences often reach far and wide, and can be felt in the short-term (changes in investor confidence) as well as the long-term (changes in government policy).

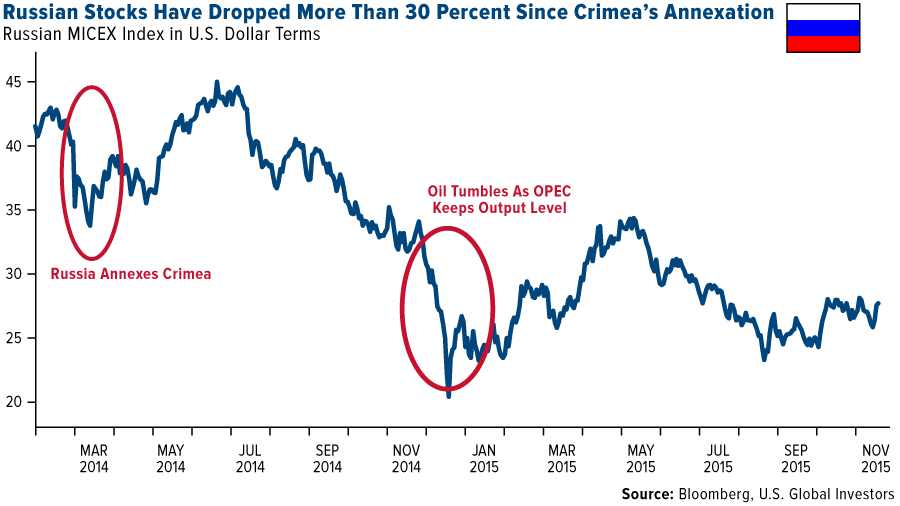

Early last year, for instance, we were quick to adjust asset allocations when Russia invaded and annexed Crimea. We anticipated that sanctions would be imposed on the country, and indeed they were, by the U.S., European Union, Australia and other international organizations. These sanctions, coupled with falling oil prices, contributed to the Russian ruble’s dramatic breakdown.

|

Against these challenges, I’m impressed by how strongly Russian stocks have performed lately. On Tuesday, the Micex Index jumped to an eight-month high in ruble terms. This is especially interesting since both Brent oil and the ruble are way down. It suggests that investors are showing approval of President Vladimir Putin’s involvement in Syria.

Putin is also benefiting from a strong public relations push. The Daily Mail writes: “Russia has shown its solidarity with the people of France in an unusual way—by donating a new puppy to carry on the memory of Diesel, the police dog killed by a suicide bomber.”

It should come as a surprise to no one that, following the tragedy in Paris, defense spending will likely increase. French President François Hollande has already told Parliament that France is at war and will “be merciless” in its pursuit of justice. The country wasted no time in striking back against ISIS and has begun bombing raids in Syria.

As early as Monday, stocks of companies that manufacture weapons and fighter jets traded up.

We own Lockheed Martin, manufacturer of the F-35, F-22 and F-16 fighters; Boeing, manufacturer of the Tomahawk cruise missile, F-18 fighter and more; and Northrop Grumman, which was recently awarded the contract to build America’s next generation of long-range strike bombers. Raytheon develops and manufactures guided missiles.

International Travel to Be Hit

Understandably so, the terrorist attacks will have an impact on international travel, immigration and border security. France immediately tightened its borders, and other European countries quickly followed suit. Meanwhile, Poland’s newly-elected government rejected the European Union’s quotas for accepting refugees from Syria, an attitude that’s echoed by more than 30 U.S. states. The House of Representatives just passed legislation to suspend the admittance of 10,000 Syrian refugees, though it’s likely to be vetoed.

This is the climate we find ourselves in right now. It has a huge effect, at least in the near-term, on perceptions of international travel.

“Most people are risk-averse,” Xian says. “When my wife and I left for the airport by taxi the morning after the Paris attacks, we agreed not to travel to Europe again any time soon.”

Others share Xian’s attitude. Paris has for years been the world’s top tourist destination, but the City of Lights has already seen a huge drop-off in tourists as people have delayed or cancelled travel plans. Hotel stocks were up 10 percent in October but will likely face headwinds as a result of Paris and Mali.

Gold, Diamond and Oil Declines Good for Manufacturers

Xian stresses the importance of having gold exposure as diversification. A good diversifier is any investment that’s expected to have a low correlation with the rest of your portfolio, and gold historically has little to no correlation with equities.

The yellow metal has traditionally been seen as a safe haven in times of war, but so far we’ve seen little movement. Year-to-date, gold is down nearly 9 percent, and it could possibly end 2015 in negative territory for the third straight year.

Even so, the yellow metal has performed better than other select world currencies for the year, including the Russian ruble (-10 percent), Australian dollar (-11 percent), euro (-12 percent) and Canadian dollar (-13 percent).

Diamonds have likewise struggled over the past four years, but with the recent news that Canadian miner Lucara discovered the largest diamond in 100 years, investors might show renewed interest. The massive 1,111-carat diamond was unearthed in Lucara’s Botswana project. Although the stone has yet to be assessed, it’s worth noting for comparison that a 100-carat diamond sold at Sotheby’s in April for $22 million.

These declines over the past three and four years have been good for jewelry companies such as Tiffany, which I wrote about last December. Gold and diamond supply is less expensive, so the company has margin expansion.

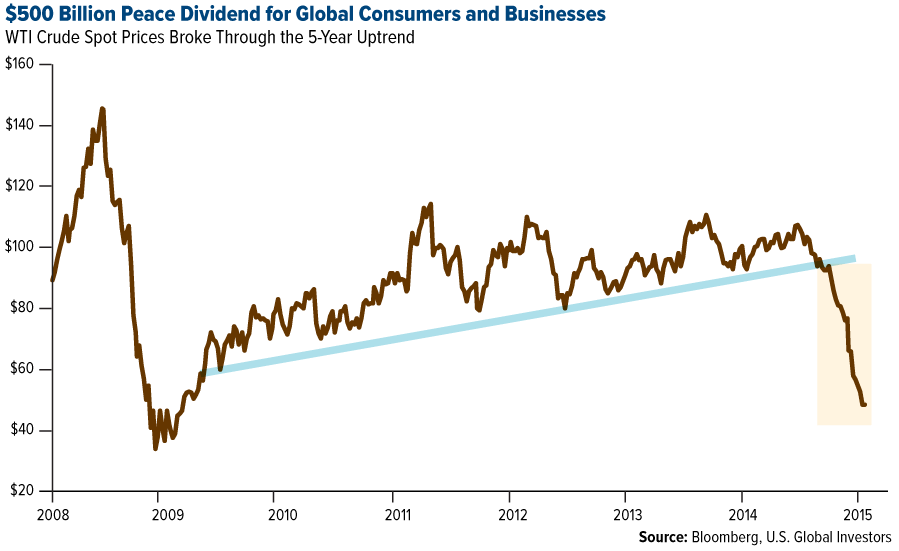

The same can be said of oil. Low prices have hurt South Texas, the Middle East, Russia and Colombia, not to mention drillers and explorers, but they’ve been a windfall for the end consumer, including manufacturers and airlines. Falling energy prices are finding their way into the global engine of growth.

Many analysts expect to see crude oil prices tick up on mounting tension in the Middle East. During past military engagements, oil has typically performed well since a lot is required to fight a war. We haven’t seen prices move just yet—oil still sits at $40 per barrel—but it’s something we’ll monitor closely. As I said earlier this month, the global purchasing managers’ index (PMI) turned up in October after bottoming in September, and in the past this has been followed by a jump in oil prices.

Inflation Rousing from Sleep

We learned this week that the consumer price index (CPI) rose 0.2 percent in October, suggesting that inflation is finally picking up steam in the U.S. and giving the Federal Reserve further excuses to raise rates next month.

Based on the 2-year Treasury yield (0.89 percent) and the headline CPI (0.20 percent), real rates now stand at 0.69 percent. (Real interest rates are what you get when you subtract the CPI from the Federal funds rate.) I’ve often explained that gold responds positively when real rates turn negative, as you can clearly see in the chart below, so we’re eagerly awaiting stronger inflation.

In a note this week, Drew Matus, an economist at UBS, wrote that inflation in U.S. is poised to jump in the next couple of months. The CPI measures the price of a basket of goods to the price of the same goods a year ago, so inflation fell dramatically between November 2014 and January 2015 as energy prices plunged.

But “absent a similar move this year, those sharp price declines will drop out of the year-over-year data, resulting in a rapid, technical acceleration in overall inflation measure,” Matus says.

If such inflation occurs—possibly as soon as January or February, Matus points out—real rates could have a better chance of dipping into negative territory, which would be constructive for gold prices.

Thanksgiving is next week, and in light of recent events, I think we all have ample reason to express gratitude to friends and loved ones. Everyone have a blessed weekend and Thanksgiving week!

Index Summary

- The major market indices finished up this week. The Dow Jones Industrial Average gained 3.35 percent. The S&P 500 Stock Index rose 3.27 percent, while the Nasdaq Composite climbed 3.59 percent. The Russell 2000 small capitalization index gained 2.49 percent this week.

- The Hang Seng Composite gained 1.56 percent this week; while Taiwan was up 1.63 percent and the KOSPI rose 0.84 percent.

- The 10-year Treasury bond yield fell less than 1 basis point to 2.26 percent.

Domestic Equity Market

Strengths

- Consumer discretionary was the best performing sector for the week, increasing by 4.52 percent versus an overall advance of 3.23 percent for the S&P 500. A number of retailers posted better-than-expected earnings reports, fueling momentum for the sector amidst anticipation of strong consumer spending during the holidays.

- Airgas was the best performing stock for the week, increasing 36.33 percent. The company is being acquired by Air Liquide for $143 per share in cash, or a total enterprise value of $13.4 billion. The deal, which is subject to Airgas shareholders’ approval and the receipt of necessary antitrust and other regulatory approvals, is touted to be the largest takeover in the industrial gases space in recent years.

- Announced corporate takeover deals have crossed the $4 trillion mark for 2015, second only to the amount for 2007. A record 128 deals each worth more than $5 billion have been announced.

Weaknesses

- Energy was the worst performing sector for the week, increasing 1.31 percent versus an overall advance of 3.23 percent for the S&P 500. Global oil prices remain volatile as ample global supplies of crude continue to pressure the market.

- Southwestern Energy was the worst performing stock for the week, falling 17.97 percent. The stock slumped as oil prices slipped below $40 per barrel earlier in the week and saw further selling pressure after Sterne Agee downgraded the name to “underperform” with an $8 price target.

- Hotel giant Marriott plans to buy Starwood Hotels & Resorts for $12.2 billion, creating the world’s largest hotel company. Starwood had been in merger talks with Hyatt Hotels. Shares of Hyatt rose after the deal was announced, while the stock of both Marriott and Starwood fell.

Opportunities

- According to BCA, REITs outperform more often than not leading up to, and after, the Fed begins to raise interest rates. The key to outperformance is for the group to be undervalued at the time of lift-off, as is currently the case. Of note, deflation in the rest of the corporate sector has not infected the REITs group. The CPI for homeowners’ equivalent rent continues to accelerate, even as multifamily home construction has risen in recent years. Moreover, their composite for Commercial Real Estate pricing power is advancing much faster than overall pricing power. With the REITs Demand Indicator shifting back into growth territory, the odds of sustainable price hikes have improved. Net asset values continue to be bolstered by rising underlying property prices. Against this backdrop, the REITs group is well positioned to experience a narrowing risk premium, even if the Fed raises rates next month.

- Retail drug store sales are reaccelerating which partly reflects robust demand for drugs, as the number of prescriptions written is climbing steadily alongside hospital and doctor visits. This has positive implications for the pharmaceuticals group. Burgeoning drug consumption is driving up selling prices. This trend should be sustainable, as there is no indication that high prices are choking off demand. On the contrary, pharmaceutical shipment growth continues to boom. That is supportive of industry profits, and by extension, the bull market in pharmaceuticals.

- In the past, Fed rate hikes have led to cyclical sector outperformance. However, past tightening cycles occurred within the context of rising inflation, signaling that the economy was overheating, which is a boon to cyclical sector profits. Moreover, the debt super-cycle was alive and well. Today, the Fed’s primary motivation is simply to remove what it sees as emergency level policy accommodation. The output gap, inflation, inflation expectations and utilization rates suggest that the economy is still operating with slack that is hardly pointing towards overheating. Consequently, automatically equating rate hikes to cyclical sector outperformance based on historic relationships is a risky proposition. It is more likely that the shift in correlations since 2008 persists, with defensive sectors maintaining market leadership.

Threats

- Energy stocks have given up almost all of the relative gains since the late September reflex rebound. Looking further out, the odds are high that the sector represents a value trap. Deteriorating balance sheets caution against the ability to replace production and growth while heavy debt burdens are a further cause for concern, especially in view of the spike in debt servicing costs. Moreover, the dividend payout ratio of many companies in the sector is closing in on 100 percent, warning that payout cuts loom. Thus, low price-to-book values may be misleading, because book value itself is at risk.

- Previously, five out of 10 sectors were suffering from falling prices, but following the latest release of both the CPI and PPI inflation reports, six sectors are now cutting selling prices. The biggest negative shift was in the domestic consumer discretionary sector. While pricing power is still positive, it is moving toward negative territory. Automobiles, media, retail and even housing are contributing to the loss of sector pricing power momentum.

- Media sales are coming under pressure owing to shifting consumer spending patterns, which implies a deflationary transition. Consequently, extrapolating current 20 percent operating margins in an environment of sales contraction and pressure to boost investment is overly optimistic. Furthermore, balance sheet health has eroded as evidenced by net debt/EBITDA which stands at a post-crisis high. Media corporate bond spreads are widening steadily, suggesting that an appetite for media debt is waning. Now that share prices are also under pressure, a broad-based rise in the cost of capital risks is dampening key media stock supports.

The Economy and Bond Market

Global financial markets rose, unaffected by last Friday’s terrorist attack in Paris. Investors were comfortable with growing signs of a U.S. Federal Reserve interest rate hike in December. Japan had a second straight quarter of contraction, while the European Central Bank is leaning towards expanding its stimulus program in December in response to deflationary risks. Overall, equity markets advanced strongly and the Chicago Board Options Exchange Volatility Index (VIX) fell below 16 from 20 last week. The yield on U.S. 10-year Treasuries ended the week at 2.26 percent. The price of crude oil hovered near $40 and $44 per barrel for U.S. West Texas Intermediate and Brent, respectively. The price of an ounce of gold fell to a five-and-a-half year low of $1,065 before rebounding slightly.

Strengths

- The October Federal Open Market Committee (FOMC) minutes covered a wide-range of views among the Committee, with arguably a few more dovish comments than the market anticipated. Nonetheless, most Fed officials thought the conditions to hike could well be met by the next meeting. Specifically, the cumulative improvement in the labor market and reduction in global risks should give many FOMC voters great confidence in the outlook. That said, it was notable that most voters still were not yet reasonably confident on their inflation outlook. The expectation remains that conditions should allow the FOMC to hike rates come the December meeting.

- The U.S. Consumer Price Index rose a seasonally adjusted 0.2 percent in October. Core prices, excluding food and energy, also gained 0.2 percent. Core prices were up 1.9 percent from a year ago. Real average hourly earnings climbed 0.2 percent in October and were up 2.4 percent from October 2014.

- The latest data on household formation has shown an exceptional recovery. Based on the Q3 Housing Vacancy Survey from the Census Bureau, the U.S. is on track to see 1.5 million new households this year. That would be the fastest growth since 2005 and significantly above the annual pace of about 650,000 since the recession struck.

Weaknesses

- Industrial production fell 0.2 percent month-over-month for the second straight month in October, disappointing expectations of a 0.1 percent pick-up. The biggest drags on the headline index were in utilities and mining, which plunged month-over-month 2.5 percent and 1.5 percent, respectively. Warm weather in October likely weighed on utilities, reducing the need for heat. We could see further weakness in heat demand as the outlook is for a warm winter due to El Nino effects. Meanwhile, the mining sector continues to suffer amid lower energy prices.

- The Empire manufacturing index remained quite weak in November, inching up to -10.7 from -11.4. This disappointed expectations of -6.4, and marks the worst 4-month period for the survey since the recession.

- Japan’s gross domestic product shrank at an annualized rate of 0.8 percent in the third quarter, the second straight quarter of diminished economic activity, a technical recession. Economists had forecast a 0.2 percent to 0.3 percent contraction. The recession is Japan’s fifth since the financial crisis of 2008. Japan has had six quarters of growth and five quarters of contraction since Prime Minister Shinzo Abe took office in December 2012.

Opportunities

- U.S. third-quarter GDP is set for revision on Tuesday. Confirmation of the expected 2.1 percent growth would add impetus to the Fed’s December rate hike intentions.

- The October print of core PCE inflation, the Fed’s favored measure of underlying inflation, will be released Wednesday. Although moderate, the recent pickup in some inflation measures could foreshadow a stronger report.

- The November Consumer Confidence Index reading will be released on Tuesday and a confirmation of the expected increase to 99.2 from the previous 97.6 would be a positive sign of economic momentum as we head into the Thanksgiving/Christmas retail shopping holidays.

Threats

- An increased concentration of bonds held in products such as ETFs and mutual funds has led to worries that a sharp outflow from these funds could create a liquidity mismatch, forcing bond managers to sell securities at fire sale prices in order to raise cash to meet redemptions. These worries may have some merit, as fund flows have become a more important influence on near-term returns in bond markets in recent years.

- Japan releases its flash manufacturing PMI on Monday. Amidst a technical recession, the report will be an important milestone in gauging the degree of the slowdown.

- Euro area growth has been losing some steam recently. It will be important to monitor the euro area credit data released on Thursday. Other key releases next week include the euro area flash PMI and the German IFO survey, both of which provide useful clues about business sentiment.

![[thumb]](/images/content_image/data/06/0662f39e4fcc29ecbb9df503a50f1c33.jpg)

November 18, 20155 World Currencies That Are Closely Tied to Commodities |

![[thumb]](/images/content_image/data/43/433c5bc602371f970fbf7a5af2fe5eba.jpg)

November 16, 2015The Bullish Case for Aussie Gold |

![[thumb]](/images/content_image/data/f1/f19f7cb63eb0d38085e0c94f2029117a.jpg)

November 10, 201511 Numbers that Explain the World’s Largest Shopping Holiday |

Gold Market

For the week, spot gold closed at $1,078.09 down $5.83 per ounce, or 0.54 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, fell 0.75 percent. Junior miners outperformed seniors for the week as the S&P/TSX Venture Index lost just 0.63 percent. The U.S. Trade-Weighted Dollar Index gained 0.62 percent for the week.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Nov-16 | EC CPI Core YoY | 1.00% | 1.10% | 1.00% |

| Nov-17 | GE ZEW Survey Current Situation | 55.2 | 54.4 | 55.2 |

| Nov-17 | GE ZEW Survey Expectations | 6 | 10.4 | 1.9 |

| Nov-17 | US CPI YoY | 0.10% | 0.20% | 0.00% |

| Nov-18 | US Housing Starts | 1160k | 1060k | 1206k |

| Nov-19 | US Initial Jobless Claims | 270K | 271K | 276K |

| Nov-24 | US GDP Annualized QoQ | 2.10% | -- | 1.50% |

| Nov-24 | US Consumer Confidence Index | 99.2 | -- | 97.6 |

| Nov-25 | US Durable Goods Orders | 1.60% | -- | -1.20% |

| Nov-25 | US Initial Jobless Claims | 271K | -- | 271K |

| Nov-25 | US New Home Sales | 500k | -- | 468k |

| Nov-26 | HK Exports YoY | -4.00% | -- | -4.60% |

Strengths

- Palladium was the best performing precious metal this week, up 4.45 percent. Trade data shows that China’s palladium imports surged 33 percent sequentially in September as the metal’s price plunged 30 percent from a year ago. In addition, there is an obvious strong correlation between a low gold price and the number of Chinese consumers searching online for “gold jewelry,” as seen in the chart below. According to the World Gold Council, this relationship ultimately paints a picture of a Chinese consumer who is acutely aware of changes in the gold price.

- Canadian mining company Lucara Diamond Corp. recovered a massive, 1,111-carat diamond this week from its Karowe mine in Botswana. The diamond is thought to be the second-largest, gem-quality stone ever found, after the infamous Cullinan diamond recovered in 1905 in South Africa. The diamond is sure to sell for a massive price at auction, which will be positive for Lucara.

- Gluskin Sheff reports that wage inflation is back, after the recent U.S. payroll report indicates that the wage inflation rate is 2.5 percent year-over-year. Historically inflation is good for gold, as gold is typically seen as a hedge against inflation.

Weaknesses

- Platinum did not follow palladium prices higher this week but instead was the worst performing precious metal, down 0.99 percent. HSBC suggested physical demand may have been stronger for palladium. Not far behind were gold and silver, down 0.56 percent and 0.51 percent, respectively.

- In a corporate update from Atico Mining, the company announced that Colombian subsidiary Minera El Roble has received notice of a claim from the mining authority in Colombia. The claim requests payment of royalties related to past copper production and is based on the current mining law. The current mining law in Colombia explicitly states that it does not affect contracts executed prior to this law entering into force. Atico Mining has taken the position that the authority’s claim is not legitimate.

- Silver has been on a 15-day losing run this week, according to Bloomberg. Following the Federal Reserve minutes on Thursday, however, the precious metal added 0.2 percent to $14.21 an ounce. Perhaps this will snap the metal out of its longest losing streak on record, based on data starting in 1950.

Opportunities

- Banks that handle commodities could be required by the Fed to increase their capital cushions as a hedge against accidents, reports the Financial Times. “Accidents” would include things like tanker spills or gas pipeline explosions. Fed Governor Daniel Tarullo stated last November that the U.S. central bank was considering such rules in order to increase capital and insurance requirements, limit the size of operations, or prohibit firms from holding certain commodities. Hopefully with banks being required to hold more capital they will be less likely to engage in what has been argued as price manipulation in the metals market.

- Now might be the time to buy gold, according to Ken Goldberg of TheStreet. Gold, along with silver, copper, platinum and palladium are in what appears to be the final stages of corrective declines, meaning they may be due for technical relief. The chart below from Scotiabank highlights that after a set of third-quarter reports showing the significant cost improvements at the operational level, the market may want to take this improvement in the fundamentals to rotate from gold to gold stocks (or into the sector as a whole). Investors could benefit from this extremely oversold position in the stocks relative to the commodity.

- South African miner Gold Fields climbed the most in 16 years as improvements to its South Deep mine lowered costs, according to Bloomberg. In a statement on Thursday the company said that cash outflows at South Deep, which were affected by delays, fell 26 percent to $20 million in the third quarter. The mine’s production climbed 42 percent.

Threats

- During the course of 2015 gold has lost around 9 percent, dropping to a five-year low and losing some of its appeal as the Fed prepares to hike interest rates for the first time since 2006. Last month Goldman Sachs reiterated that a rate hike in December would likely hurt bullion, and forecasted the precious metal at $1,050 in six months and $1,000 in a year. However, the Fed has argued that it has gone to extraordinary steps to prepare the market for a rate hike over the last several years and gold prices have likely already factored in such a hike.

- According to the World Gold Council’s latest report, a growing middle class in China will spur growth in demand for gold over the next five years. Despite the encouraging forecasts, Jack Klein, executive chairman of Evolution Mining, says not to bet on the Asian middle class to boost gold prices. Klein argues that, “Yes there’ll be increased physical demand, but the gold market is so dominated by financial issues, inflation and the U.S. dollar, that it’s not going to make a huge difference.”

- BMI Research believes that bullion could fall below the $1,000 level during the first half of 2016 once the Fed raises rates and the dollar gains. John Davies, global head of commodities research, says that expectations for gradual tightening will cushion the fall however, with prices returning to about $1,000 and above.

Energy and Natural Resources Market

Strengths

- Construction materials companies performed well this week. The S&P Supercomposite Construction Materials Index rose 5.28 percent this week after the U.S. House of Representatives passed a bill that would increase spending to $42.5 billion by 2021.

- Chemicals were also a strong performer this week, as global demand for agricultural chemicals grows. PhosAgro jumped the most in two months after the company announced its profits had more than doubled. The phosphate fertilizer producer’s EBITDA more than doubled, to 62.8 billion rubles in the first three quarters of the year, while net income increased by more than 500 percent, to 31.6 billion rubles.

- Railroad stocks performed well this week, as the industry’s fundamentals remain healthy. This week Canadian Pacific Railway went public with an offer of about $28 billion for Norfolk Southern Corporation. According to Edward Jones & Co. analyst Logan Punk, “If they get a hold of Norfolk’s assets, there’s a lot of opportunity to really make them more efficient. With Norfolk struggling to lower its operating ratio and CP doing just fine, it’s ripe with opportunity.”

Weaknesses

- The Baltic Dry Index fell to its lowest levels since 1985. The Baltic’s BDI Index, which gauges the cost of shipping resources including iron ore, cement, grain, coal and fertilizer, has dropped to 498 points and is over 95 percent down from its all-time high of 11,793 points in 2008 before the financial crisis. The slowdown in the world economy coupled with a drawback in coal and iron ore demand from China have negatively impacted the sector.

- Base and other industrial metals continued to plummet this week. Zinc dropped to its lowest point in more than six years, with signs of a healthy supply but diminishing demand from industrial China. Other metals, such as copper, lead and aluminum have also been hammered to six-year lows.

- Oil prices have continued to slip as it becomes clear that supply is far greater than current demand. The U.S. and Iraq, whose extra crude this year equates to about 80 percent of the global surplus, are forecasted to maintain output in 2016 rather than boost it, in order to curb the excess supply. The Generic 1st CL Future closed at $40.39 this week, the lowest since late August.

Opportunities

- Earlier this month, Congress approved a bill to spend up to $325 billion on transportation projects, with $261 billion of that on highways. Companies such as Vulcan Materials, Martin Marietta and U.S. Concrete will likely benefit from this legislature, along with their peers in the Construction Materials space.

- PMI correlations may appear to fail initially, but in longer context they are undeniable. In previous cycles, it took oil a few months to recover after global PMIs bottomed. Presently, Global PMI turned up in October.

- Raw sugar has been the top performing commodity this quarter and one reason driving its performance may be Brazil’s recession. Brazilian motorists are turning to ethanol, a fuel produced from sugar cane, which is cheaper than traditional gasoline. More ethanol consumption means higher demand for sugar cane, helping send the commodity’s price near its highest in three months.

Threats

- Weather forecasts are one of the few available data points providing insight into winter demand changes for natural gas. This week, the National Oceanic and Atmospheric Administration (NOAA) released its three-month weather forecast, in which they project warmer temperatures among many of the regions in the U.S., with a combined population of nearly 165 million people. Natural gas closed at 2.13, which is less than half the price it was a year ago.

- Even with most metal prices hovering around the price they were in 2011, some companies aren’t willing to ramp down production. Absent any consistent indicators for a Chinese stimulus in the near future, more than two-thirds of mined nickel, about 60 percent of aluminum production, and a quarter of zinc supply is now losing money, according to Standard Chartered.

- Global growth remains unimpressive and commodities across the board have suffered this year. This week, Goldman Sachs thinks the downward pressure on the asset class could continue for another 12 months.

China Region

Strengths

- Indonesia was the best performing market in Asia this week, as its central bank surprisingly cut the required reserve ratio by 50 basis points while keeping the benchmark interest rate unchanged. The Jakarta Composite Index rose 1.99 percent this week, the largest gain among Asian markets.

- Materials was the best performing sector in Asia this week, driven largely by chemicals producers in the region. The MSCI Asia Pacific ex Japan Materials Index gained 2.49 percent this week.

- The Malaysian ringgit was the best performing currency in Asia this week, strengthening by 2.08 percent and rebounding along with other commodity currencies globally.

Weaknesses

- Vietnam was the worst performing market in Asia this week, as a widening budget and trade deficit weighed on investor sentiment. The Ho Chi Minh Stock Index retreated 1.11 percent this week.

- Consumer discretionary was the worst performing sector in Asia this week, led by renewed weakness from Macau casinos. The MSCI Asia Pacific ex Japan Consumer Discretion Index rose 0.55 percent this week, the mildest gain among the sectors.

- The Chinese renminbi was the worst performing currency in Asia this week, weakening by another 0.17 percent, as China’s slowing economy, falling commodity prices and a looming U.S. interest rate increase all took their toll on the currency.

Opportunities

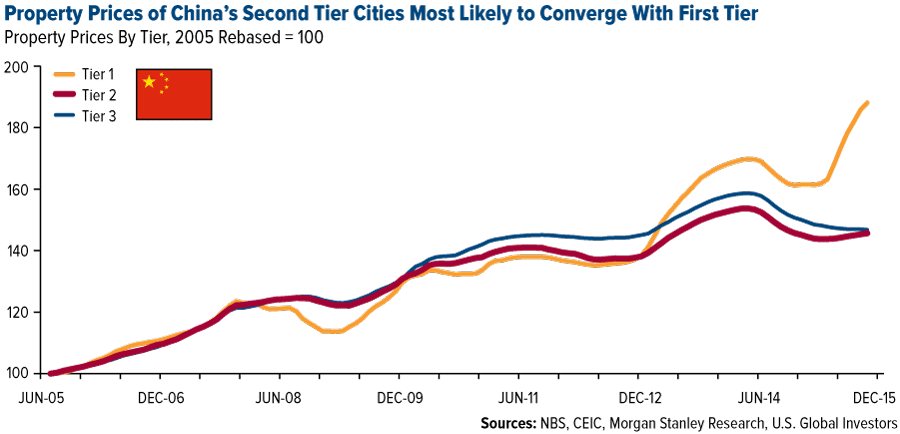

- While the pace of property price increases in China slowed mildly in October, market expectations remain alive for further government policy relaxation in the property market. This would cushion the “considerable downward pressure” on economic growth which President Xi Jinping admitted in this week’s Asia-Pacific Economic Cooperation summit in Manila. Ongoing bifurcation of the country’s property prices (strengthening in top tier cities and weakening in lower tier cities) reflects much leaner housing inventory in the former than the latter. Within the top level, tier two city prices have plenty of room to catch up with tier one and face less risk of overheating. Therefore, Chinese property developers with high exposure to tier two cities should be in the best position to benefit in today’s environment.

- Thailand’s cabinet approval this week for the $10 billion Thai-Chinese railroad development project covering 867 kilometers, serves as a reminder of continued momentum in Chinese railroad orders from overseas. More contracts are expected in the next three to six months from Laos, Thailand, and from Indonesia. Leading railroad infrastructure and equipment makers in China should continue to benefit from the country’s One Belt One Road strategy going forward.

- Taiwan’s legislative decision to remove the capital gains tax for the stock market this week should serve as a near-term positive driver for investor sentiment.

Threats

- Macau’s Chief Executive Fernando Chui’s dire forecast this week for the city’s casino revenue in 2016 should reinforce investor skepticism on whether mass market gamblers and non-gaming businesses can offset the retrenchment of premium customers for casino operators. This comes against scant evidence of government policy shifts or economic growth turnaround. While the bear market in Macau casino stocks has lasted 20 months so far, sector valuation remains unappealing to investors.

- Last weekend’s terrorist attacks in Paris might further discourage typically risk-averse mainland Chinese tourists traveling to international metropolitan areas such as Hong Kong, which has already started witnessing a secular decline in tourist arrivals and per-capita tourist spending. Local retailers and hotels in Hong Kong should continue to face significant long-term headwinds.

- An anemic response to China’s partial relaxation in birth policy in the past two years is likely to recur next year after its recent abolition of one-child policy, as urbanization, rising costs, increasing population of single women, and surging divorce rates serve as significant interference to any meaningful reacceleration of the country’s birth rate. Overhyped baby product producers and dairy providers might be vulnerable once reality sets in.

Emerging Europe

Strengths

- Russia was the best performing market this week, gaining 5.7 percent. Shortly after the tragic terrorist attacks in Paris, Russian President Vladimir Putin instructed the Russian navy to work with French vessels as allies fighting against the Islamic State. The head of Duma also met with Barack Obama at the G20 Summit in Turkey this week, signaling a better relationship with the West.

- The Russian ruble was the best performing currency this week, gaining 3.4 percent against the U.S. dollar. Brent crude oil gained 2 percent during the past five days.

- The telecommunication services sector was the best performing sector among eastern European markets this week.

Weaknesses

- Turkey was the worst performing market this week, losing 1.46 percent. The market is awaiting news on the composition of the cabinet which should be announced early next week. The latest unemployment data came in at 10.1 percent versus a prior reading of 9.8 percent. The consumer confidence index was reported stronger at 77.15 versus a prior reading of 62.78.

- The euro was the worst performing currency, losing 1.2 percent against the U.S. dollar this week. The European Central Bank (ECB) minutes that were released this week signal that the bank could be preparing to increase its bond buying program in December. Such an event would put downward pressure on the eurozone currency.

- The utilities sector was the worst performing sector among eastern European markets this week.

Opportunities

- Turkey’s political drama could be ending with the upcoming announcement of new cabinet members. Most traders are rooting for the inclusion of acting Finance Minister Mehmet Simsek and former Deputy Prime Minister Ali Babacan. These two led the economy during the AK Party’s 13 years in office, helping to boost growth and lower inflation from a high of 104 percent in the 1990s.

- After the tragic events in France last week, Russian President Vladimir Putin could be finding common ground with the United States and the eurozone on fighting international terrorism. Russia could once again develop a better relationship with the West, possibly leading to the softening or lifting of sanctions imposed on Russia after the annexation of Crimea.

- Greece has reached an agreement with official creditors over home foreclosures, which is expected to free up its next tranche of funds. Greek banks would undergo a recapitalization process and once completed, investors’ confidence could be restored.

Threats

- It seems many investors think that the euro will drop moving forward, mostly on expectations of a rate hike by the Federal Reserve in December along with more easing by the ECB. Net short, euro future positions are increasing, as investors anticipate further weakness in the eurozone currency.

- Beata Szydlo was sworn in on Monday as Poland’s new prime minister. During her opening speech before parliament she held up her party’s pre-election spending promises to boost child subsidies and reduce the retirement age. These will be funded by new levies on banks and supermarkets, better tax collection and a wider budget deficit. The government will add as much as 1.5 billion zloty to the 2016 budget shortfall, currently seen at 54.6 billion zloty.

- Russian wages and retail sales declined the most since 1999, a sign that consumer demand is a weak link in the economy. Real wages fell 10.9 percent in October from a year earlier, a deeper contraction than the median estimate by economists for a 9.7 percent decrease. Sales declined 11.7 percent from a year earlier after shrinking 10.4 percent the previous month.

(c) US Global Investors