Why Investors Shouldn't Wait for Rate Hikes

By Dr. Brian Jacobsen, CFA

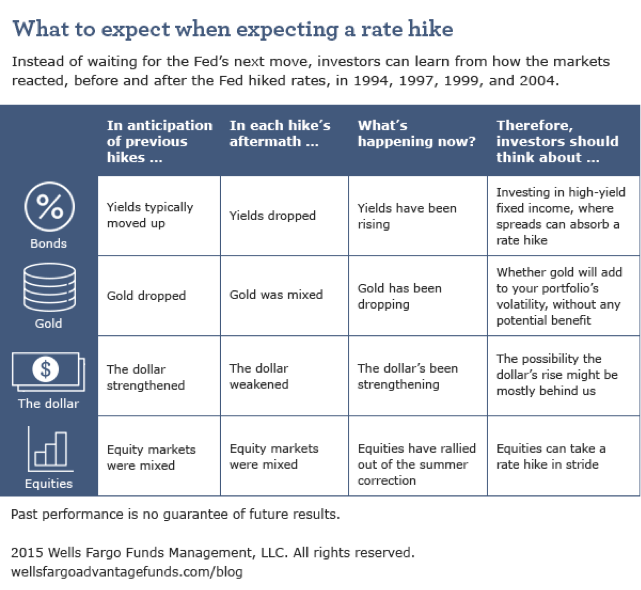

Summary: Don’t let “waiting on the Fed” postpone when you realign your portfolio. The markets have already priced in an interest-rate hike. Learning about how the markets moved before and after past rate increases can help investors.

It wasn’t a huge surprise when the Federal Open Market Committee left its target for the federal funds rate unchanged between 0.00% and 0.25% at its October meeting. What was surprising was the Fed clearly putting a rate hike on the table for its December 15–16 meeting. A rate increase in December looks all but certain now. Concerns about a faltering labor market can no longer be used as an excuse not to hike, given the outstanding employment report released last Friday.

Now that a rate hike looks all but inevitable, what does that mean for investors? Let’s look at how rate increases in 1994, 1997, 1999, and 2004 affected the markets across four key categories:

Compared with previous rate-hike cycles, bond yields across the board are now lower and the markets are starting from a lower yield-base. Of course, that’s not necessarily a bad thing, considering the Fed will likely move slower in the upcoming rate-hike cycle than in cycles past. In the historical examples, prior to a rate hike, yields typically moved up, gold moved lower (except in 1994), and the dollar strengthened. Interestingly, equity markets didn’t tell a very consistent story. In 1994, 1997, and 1999, the S&P 500 Index moved up in the 60 days prior to a hike, but in 2004, the S&P 500 Index dropped.

Emerging markets moved up at least 10% prior to previous hikes, except in 2004 when they dropped 11% in the run-up to a hike. I think we’ve already seen a lot of weakness in emerging markets, effectively pricing in any sort of doom and gloom that could emerge from a stronger dollar or lower commodity prices. As in 2004, when emerging markets dropped prior to a rate hike but bounced 6.7% in the 60 days following the hike, we could see a similar pattern play out this time.

What about after a rate hike? Well, the reverse typically happens. While in the run-up to a hike, yields rose and the dollar strengthened, after the Fed hiked rates, yields dropped and the dollar weakened. It seems like the markets did a pretty good job—though imperfect—of pricing in rate hikes, effectively creating a situation in which people would buy on the rumor and sell on the news or sell on the rumor and buy on the news.

Rate hikes seem to have been in play ever since June 2015. Shifting expectations over when precisely the Fed will commence liftoff have likely contributed to market volatility, although I think you’d be hard pressed to say the majority of investors haven’t been expecting something within the next year. I think a rate hike will happen, and when it does, I don’t think it’s much to worry about. Any pain has likely already happened. It’s time to look forward. Provided the Fed is hiking into economic strength rather than weakness, I see little to worry about.

The Fed will still be accommodative, even as it lifts rates. Thus, I think there’s nothing wrong with taking on risk as the Fed approaches liftoff. In fixed-income markets, I’d look for generous spreads, which are more accessible from taking on credit risk versus taking on duration risk. A greater source of opportunities, however, lies in the international equity markets—especially emerging markets. The consensus seems to be that emerging markets valuations are attractive, but it might be too soon to jump in; people are waiting for commodities to stabilize or for China to post better growth numbers. I’m just afraid that by the time you wait for confirming evidence, the opportunities will have mostly passed.

In Lewis Carroll’s “Through the Looking-Glass,” the White Queen offers Alice jam every other day, as an enticement to keep working—and to keep waiting: “The rule is, jam tomorrow and jam yesterday, but never jam today.” For investors, this story offers a lesson about waiting for something, even when the signs tell you there’s no certain reward to waiting. Today’s markets are well-positioned for a rate hike. Don’t let waiting for the Fed lead to missed opportunities.

Please visit our blog, AdvantageVoice, for additional viewpoints from Wells Fargo Asset Management’s investment strategists, portfolio managers, and practice management experts. You can also follow us on Twitter at @WFAssetMgmt for real-time updates. Are you an advisor or institutional investor? Check out our website for investment professionals.

The views expressed are as of 11-10-15 and are those of Dr. Brian Jacobsen, CFA, and Wells Fargo Funds Management, LLC. The information and statistics in this report have been obtained from sources we believe to be reliable but are not guaranteed by us to be accurate or complete. Any and all earnings, projections, and estimates assume certain conditions and industry developments, which are subject to change. The opinions stated are those of the authors and are not intended to be used as investment advice. The views and any forward-looking statements are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally, or any mutual fund. Wells Fargo Funds Management, LLC, disclaims any obligation to publicly update or revise any views expressed or forward-looking statements.

Wells Fargo Funds Management, LLC, a wholly owned subsidiary of Wells Fargo & Company, provides

investment advisory and administrative services for Wells Fargo Advantage Funds®. Other affiliates of Wells Fargo & Company provide subadvisory and other services for the funds. The funds are distributed by Wells Fargo Funds Distributor, LLC, Member FINRA, an affiliate of Wells Fargo & Company.

Not FDIC Insured • No Bank Guarantee • May Lose Value

© Wells Fargo Asset Management