- Oil Hits a New Low

- The ECB Overpromises and Underdelivers

- November Employment: A Green Light for the Fed

Clients of the bank may have noticed slower response times last week when trying to access information on our web site. It was all my fault: I was running a model to help me determine the sleeping arrangements in my house during the Thanksgiving weekend.

Two of my children brought significant others home for the holiday, and we had to reconcile the number of bedrooms with house rules on fraternization. The calculations reached equilibrium (boys in the basement; girls upstairs; barbed wire in between), but only after using up many megabytes of memory on our servers.

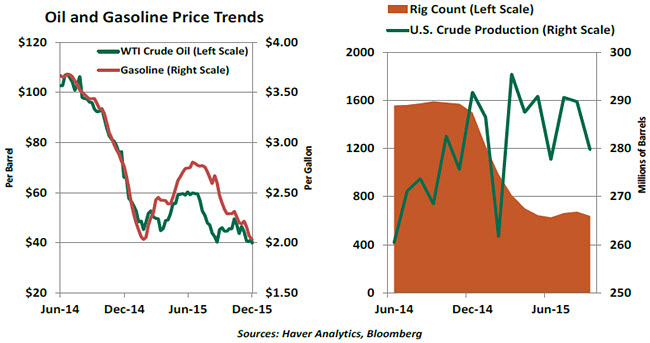

While that puzzle got solved, another one is complicating the current economic calculus. Oil prices remain at very low levels, defying the expectations of many analysts. And the economic reaction to low oil prices has also defied expectations. It seems appropriate to take a fresh look at what’s happening in this very critical world market.

Last June, the Blue Chip Economic Consensus asked its panel for a forecast of oil prices. The group’s estimates for the end of 2015 averaged nearly $60 per barrel. In the interim, petroleum prices have established new lows for the year, falling below $40 per barrel in recent trading.

Among the leading causes of this unexpected outcome is U.S. oil production that has been much more robust than expected. The number of rigs actively producing petroleum has fallen by almost two-thirds since the middle of 2014, yet monthly production has actually increased by around 10% over that interval. Drillers have consolidated their operations, focusing on the most- fertile fields and reducing their costs aggressively.

International supply dynamics have added to the current glut. Iraq’s oil-producing capacity has been recovering more rapidly than expected, and sanctions limiting Iran’s ability to sell its oil on world markets are close to being removed. Saudi Arabia has continued to produce aggressively, to gain market share and to disadvantage its adversaries in the region. OPEC met at the end of this week to discuss the state of world supply. Many members are desperate for higher prices, which would close gaping holes in their national budgets. But the group is in deep disagreement over how production reductions should be shared, and many non-OPEC producers (including Russia, Canada and the United States) will not be party to any agreement. There is no end in sight to oversupply.

OPEC met at the end of this week to discuss the state of world supply. Many members are desperate for higher prices, which would close gaping holes in their national budgets. But the group is in deep disagreement over how production reductions should be shared, and many non-OPEC producers (including Russia, Canada and the United States) will not be party to any agreement. There is no end in sight to oversupply.

On the demand side, international factory activity has been ebbing. The Chinese manufacturing retreat has been a long-running story, but more recently the dollar’s strength has hindered U.S. manufacturers. Commodity-producing nations have also been impaired.

While persistently low oil prices were unexpected, U.S. consumer reaction to them was equally surprising. U.S. gasoline prices are currently 40% lower than they were 18 months ago, yet personal consumption is growing at its slowest pace since 2013. The only place where any “energy dividend” is at all apparent is in auto sales, which are at levels not seen for 10 years. Larger vehicles are selling especially well.

Coming into this year, Federal Reserve officials had suggested that falling energy prices would be a decided net positive for U.S. economic growth. It hasn’t turned out that way. Further, the energy price component of the American consumer price index is down 20% over the last year, keeping inflation far from the Fed’s 2% target. These are among economists’ biggest forecast misses this year.

While chastened by this experience, we must dust ourselves off and try to anticipate what might play out next year. Here are a few factors that will bear heavily on the outcome.

- Crude oil inventories are at record levels. It may take some time to work them down to a point where prices will increase.

- It is unclear how long Saudi Arabia will be willing to maintain its production levels. While current oil prices are significantly in excess of extraction costs in Saudi Arabia, the country needs to generate revenue to defend itself and provide benefits to its citizens. For the time being, the Saudis have been selling some of their substantial foreign reserves to compensate for the lost income, but there may be limits to how far it is willing to pursue this policy.

- U.S. production should eventually decrease. Investments in equipment and exploration have diminished significantly, and a steady stream of new reserve discoveries is needed to sustain output.

Oil prices have a substantial impact on the global outlook. For producers, current price levels are introducing various degrees of trauma. Those with diversified economies and plenty of reserves are feeling less pain, while some emerging markets are suffering significant hardship. Energy users are enjoying a dividend and should be expected to spend some of it. But the savings may be seen as more of a windfall and used to pay down debt instead of increasing consumption. And energy prices are a central determinant of inflation, which in turn is a central determinant of monetary policy around the world. Some firming in oil prices would certainly help central banks in developed nations to reach 2% inflation targets.

And energy prices are a central determinant of inflation, which in turn is a central determinant of monetary policy around the world. Some firming in oil prices would certainly help central banks in developed nations to reach 2% inflation targets.

We continue to think that oil will eventually rise from the current lows. Projections for the very long-term highlight depleted reserves and increasing demand from new markets. But given current reserve and production levels, progress over the next 12 months may remain slow.

It will take a lot of computing power to solve all the oil-related equations. To avoid taxing our technology, I’ve been advised to run the model later this month, when many are taking time off for the holidays. Just don’t try to do any cyber shopping right before Christmas; response times will be slow

.

The ECB Disappoints

Last week, we awarded President Mario Draghi of the European Central Bank (ECB) our economic “man-of-the-year” award. This week, Draghi and the ECB underperformed.

On Thursday, the ECB moved to accelerate the progress of eurozone inflation toward the central bank’s target. The term of the ECB’s quantitative easing program was extended by six months to March 2017, the deposit rate was lowered by 10 basis points to -0.30%, and the asset purchase program was broadened to include state and local government debt.

The financial markets were clearly hoping for more. 2015 began with a “bazooka” from the ECB; the program announced at its January meeting was more substantial than expected. Draghi’s recent remarks seemed to suggest that another significant salvo was coming. But this week’s rate cut was modest, and the decision not to increase monthly bond buying was at odds with market expectations.

Draghi tried to ameliorate critics by stressing the ECB’s decision to reinvest principal payments. But the average life of its bond holdings is close to 8 years. Therefore, the impact of reinvestment is likely to be visible only much later.

After the announcement, the euro strengthened significantly, and European equity prices fell sharply. The ECB’s quantitative easing program aims to devalue the euro and boost stock markets, so this outcome is counterproductive. The extent of the equity correction was a bit alarming; expectations of monetary policy action seem to be playing an outsized role in asset valuations across markets.

There was clearly some disagreement within the ECB’s governing council over the proper course of policy. At present, eurozone growth shows a moderate upward trend; the ECB’s staff forecast projects real economic activity to advance 1.5%, 1.7% and 1.9% during 2015-2017, respectively. Bank lending has been strengthening, and surveys reveal increasing levels of confidence over the outlook. If continued, these trends (along with some normalization in energy prices) should put upward pressure on eurozone inflation. This leads some to think that no further aid is called for.

But current inflation, at 0.1% over the past year, is far below the central bank’s target. Core inflation, which excludes food and energy, is only 0.9%. And there are doubts about the growth outlook for Europe. Structural factors and fiscal austerity will dampen economic activity, despite some recent relaxation in spending targets. Exports account for about 45% of eurozone gross domestic product, and projections of modest global growth suggest that export-led advances are unlikely. The region remains vulnerable to the performance of its trading partners; risks are tilted to the downside.

In this post-crisis world, it can take a very long time for inflation to return to normal. Britain and the United States have expanded for most of the past seven years, but the price levels in both markets have fallen short of central bank expectations. In light of these precedents, it is far too early for the ECB to claim victory.

The media was quick to pillory Draghi for raising expectations that were ultimately unfulfilled. But his governing council may have limited what he was able to deliver. Diverging economic performance among eurozone members explains part of the dissonance, and diverging philosophy explains the rest. This may limit Draghi’s effort to do whatever it takes.

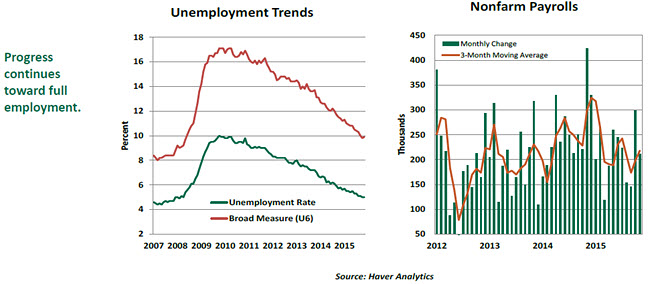

Jobs Well-Done

Labor market conditions continue to improve in the United States. Doubts about the pace of hiring that surfaced in August and September have been laid to rest.

The unemployment rate held steady at 5.0% in November, reflecting an improvement in the participation rate (62.5% versus 62.4%). The unemployment rate would have edged down had the participation rate held steady.

The broad measure of unemployment, at 9.9%, is down from 10.5% six months ago. Although part-time employment rose slightly in November, there is a strong downward trend in place. The share of long-term employment (25.7%) is at the lowest point in the expansion. In sum, other labor market measures from the household survey that Fed Chair Janet Yellen tracks closely send a unified message of improving conditions.

Details from the establishment survey paint a picture of widespread improvements. Total payroll employment rose 211,000 in November, putting the 3-month moving average at 218,000. Upward revisions to payroll estimates for the prior two months added 35,000 new jobs.

Construction employment rose 46,000 in November, one of the best gains in the current expansion. Factory jobs and employment in oil-related industries remain muted. The private sector employment diffusion index rose in November, implying broad-based gains in hiring.

The closely watched measure of average hourly earnings rose 4 cents last month, putting the year-to-year gain at 2.3%. This is a tad lower than the October reading, but it does appear that we’ve finally moved confidently above the 2% level that prevailed for several years. This reflects decreasing labor market slack and sets the stage for inflation to get a little closer to its targeted level.

Summing it up: the November employment report supports a tighter monetary policy at the next Fed meeting on December 15-16. We’ll have a preview of that session next week.

(c) Northern Trust