This Industry Is Set to Post Record Profits on Lower Fuel Costs

Everyone knows there are winners and losers in any bear market, including the recent commodity rout. Low crude oil prices have definitely hurt explorers and producers. Airlines, on the other hand, appear to be thriving.

According to the International Air Transport Association (IATA), a global airlines trade group, the industry is set to post a collective $33 billion in net profits this year—a record—on fuel cost savings and stronger passenger flight demand.

Want to know how significant a record this is? In 2014, profits came in at $17.4 billion—about half of what they are today.

What’s more, profits are expected to be even larger next year.

World demand grew 6.7 percent from a year ago, the IATA says, and is estimated to rise a further 6.9 percent in 2016. And with oil likely to stay relatively low, the group forecasts that airlines will spend $135 billion on fuel in 2016, down nearly a quarter from $180 billion in 2015.

This, coupled with improved fuel efficiency, is expected to contribute toward the group ending next year with estimated total net profits of $36.3 billion.

You can see below that global airline stocks have soared in recent years, especially in response to flagging oil, airlines’ largest expense.

In the past, airlines were notorious for their inefficiency and tendency to destroy capital. These claims were probably exaggerated, especially by Warren Buffett, who has repeatedly decried the industry as a money-loser. What a lot of people don’t realize is that Buffett didn’t do as bad as he claimed.

Former US Airways CEO Ed Colodny explained in 2013 that after Buffett’s shares didn’t appreciate, he wrote down his investment and got out when he could.

“I think at the end of the day, he got all his dividends paid and his principal back,” Colodny said.

In any case, airlines are now going into their third year of the present secular bull market. These often last much longer. We believe this cycle is different, in that the U.S. airline industry could easily create $20 billion of free cash flow this year and next. Low fuel costs have been the cherry on top.

Where Does Oil Go from Here?

|

Indeed, 2015 was not kind to oil and other commodities, with many of them slumping to multiyear and, in some cases, multi-decade lows.

Back in August, the cover of Bloomberg Businessweek featured a whole gaggle of bears, which delighted bulls. (There’s an old belief that the market will soon do the exact opposite of what the press predicts.) Yet here we are four months out, and the commodities rout has only extended itself further.

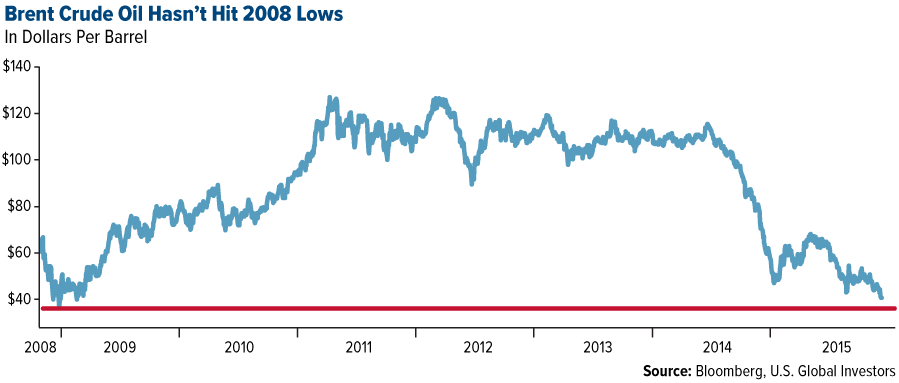

Crude oil is presently testing financial crisis support levels, making many investors wonder whether the bottom for black gold has been reached—or if more pain is to be expected.

There’s no shortage of analysts and experts right now sharing their (wildly divergent) predictions of where oil might be headed from here. Some are calling for $20 per barrel; others, such as legendary hedge fund manager T. Boone Pickens, $70 or more in the next six months.

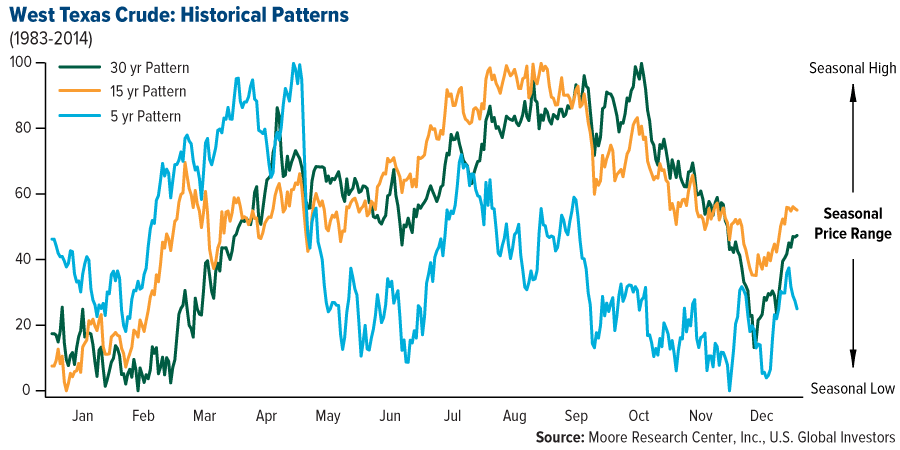

We can’t say whether Pickens is right or wrong. It’s worth pointing out, though, that crude has pretty closely followed its five-year trading pattern, with 52-week lows reached in late November, early December. The short-term trend shows oil rallying sharply starting in January, according to Moore Research analysis.

Here’s another way of looking at it. The following heat map shows that, in the last five years, the oil price historically popped in February after months of losses. What this means is that January might be a good time to buy.

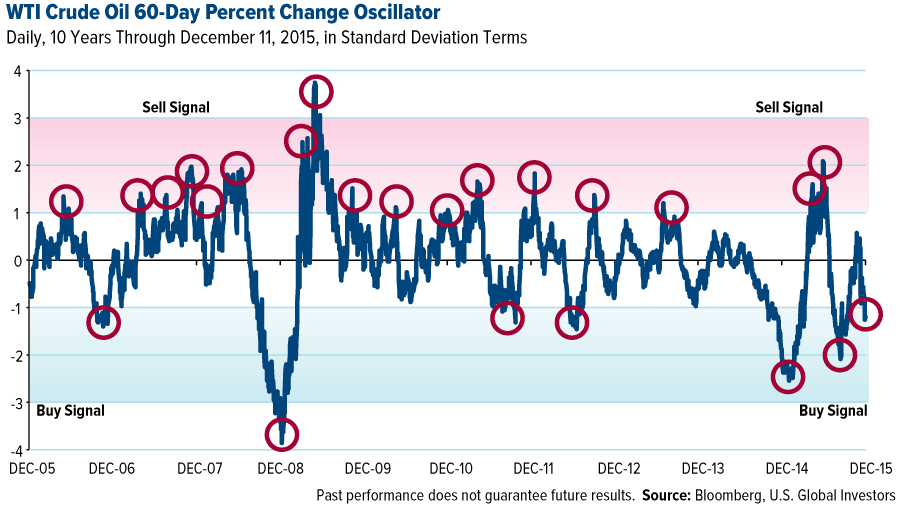

The oscillator below confirms that. Right now crude is down 1.2 standard deviations—already signaling a buy, but it might have further to fall, based on past incidences.

One of the more balanced perspectives comes from energy strategist Dr. Kent Moors, who tempers his optimism with a dose of reality:

|

We are not racing back to $100 a barrel oil. Absent the outlier of a geopolitical event that impacts supply, more subdued rises are in order. But we certainly do not need triple-digit oil to make some nice investment returns, especially in a sector that has been so oversold.

I agree. I’m not interested in adding my own forecast to the ever-lengthening list so much as I am in finding ways to make money at current prices.

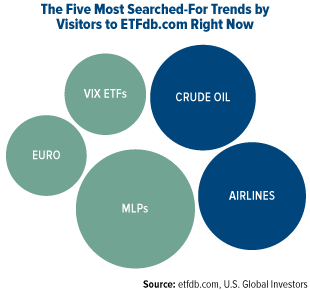

As are other investors. Based on the most searched-for trends on ETFdb.com right now, you can clearly see what’s on their minds.

OPEC Members Revolt against Saudis as Oil Slips

One of the main reasons why prices are so depressed, of course, is that the world is awash in the stuff. The Organization of Petroleum Exporting Countries (OPEC), responsible for about 40 percent of global supply, just had its most productive month since 2012, pumping 31.7 million barrels in November. That’s 1.7 million barrels over its “official” production ceiling.

Crude slipped below $37 per barrel on the news, a seven-year low, which is about as low as prices can go for most American companies to stay profitable. (As of this writing, WTI crude sits at $35.36, Brent at $37.88.)

As expected, OPEC announced last Friday that it would keep oil production levels the same in its bid to force higher-cost producers (re: American frackers) to trim their own operations. Solidarity among its members has weakened further, however, as it becomes clearer and clearer to them that they underestimated the resilience of American oil producers.

Five OPEC members—Venezuela, Nigeria, Libya, Iran and Ecuador—are now in open opposition to the Saudi policy of unchanged production. That the cartel as a whole exceeded its production ceiling last month suggests that each member-nation is making its own rules up anyway, regardless of what was decided.

It’s estimated that OPEC is already pumping about 900,000 barrels a day more than is needed next year. And with international sanctions against Iran about to be lifted—in exchange for an agreement to halt its nuclear program—the country has promised to increase its own production from 3.3 million barrels a day to as many as 4 million barrels a day by the end of 2016.

Venezuela in particular is in deep turmoil. Low oil prices have battered its currency and left its economy in tatters, with food shortages worsening every day. The International Monetary Fund (IMF) expects the South American country—which has the largest proven oil reserves in the world—to contract 10 percent this year and has declared it the worst-performing economy in the world right now.

In the recent parliamentary elections, rightfully fed-up Venezuelans responded by ousting members of Hugo Chavez’s United Socialist Party of Venezuela (PSUV), giving the opposition party, the more-centrist Democratic Unity Roundtable (MUD), a supermajority that could challenge President Nicolás Maduro.

This countrywide rejection of failed, far-left leadership is an encouraging sign that Latin America’s political ideology is finally shifting away from European-style socialist economic models of no growth. We’ve seen South American countries tax away growth and impose envy policies on the financial sector. Mining and oil executives have seen their cash flow confiscated by value-added taxes, leading to drops in capex and job creation.

But just last month we saw Argentina elect its first business-friendly president, Mauricio Macri, in decades. And now Venezuela is demanding change, so there’s hope.

As head of the cartel, Saudi Arabia hasn’t gone unscathed in the oil rout either. For the first time, the kingdom will tap international bond markets to make up for lost oil revenues.

Also in the hard-to-believe category is Alaska’s plan to institute an income tax for the first time in 35 years to “close a $3.5 billion dollar deficit the state is carrying,” according to Zero Hedge. The Last Frontier is known, of course, for giving all Alaskan residents an annual dividend based on oil revenue. In 2015, that amount was $2,072.

But since oil revenue has been cut in half, hard measures must be taken to keep the dividend running, Alaska Governor Bill Walker argues.

“This plan keeps the permanent fund permanent,” Walker tweeted on Wednesday.

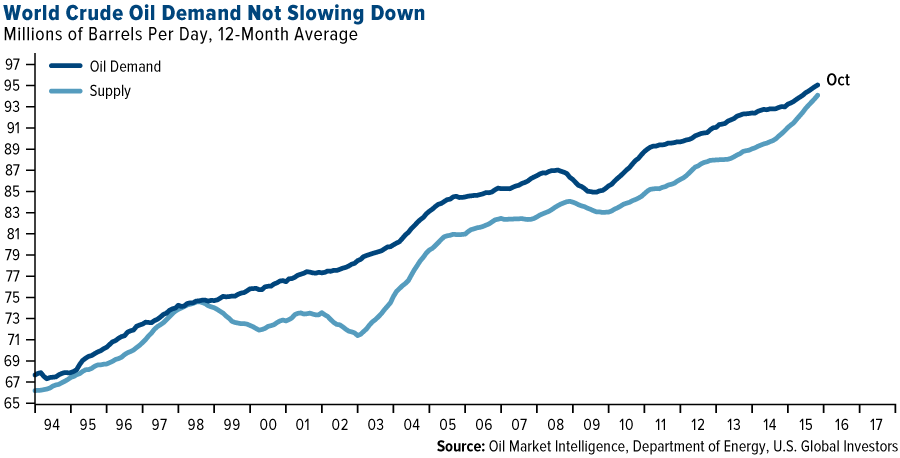

And Yet Oil Demand Is Still Outpacing Supply

Crude oil reserves here in the U.S. are currently at levels not seen since 1972. That’s with a 65 percent decline in rigs in operation from a year ago, a clear indicator of how efficient American producers have become.

But some analysts have suggested the oversupply isn’t as bad as we might think. Tom Kloza, head of energy analysis at the Oil Price Information Service (OPIS) told CNBC this week that it’s important to think of oil supply in the context of population growth:

This is a glut in terms of the most crude oil we’ve ever had in North America. But if you measure it versus the population, it’s not altogether that much. We’ve had much more crude-per-population back in previous decades.

Kloza has a fair point. In 1970, at the height of U.S. oil production, the country’s population was just over 205 million and the total number of registered vehicles—passenger cars, motorcycles, trucks and buses—was 111 million, according to the Department of Transportation. Today the population hovers just north of 319 million and, as of 2013, the number of registered vehicles has more than doubled to 255 million.

It’s worth reminding ourselves that the U.S. isn’t the only growing country. Population is booming all over the globe. People continue to have babies—Chinese couples even more so now that the one-child policy has been lifted—and the global middle class is swelling rapidly. This helps oil demand continue to rise, as well as air travel demand.

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 3.26 percent. The S&P 500 Stock Index fell 3.79 percent, while the Nasdaq Composite fell 4.06 percent. The Russell 2000 small capitalization index lost 5.05 percent this week.

- The Hang Seng Composite lost 3.64 percent this week; while Taiwan was down 3.37 percent and the KOSPI fell 1.31 percent.

- The 10-year Treasury bond yield fell 13 basis points to 2.14 percent.

Domestic Equity Market

Strengths

- Keurig Green Mountain, Inc. was the best performer in the S&P 500 this week, as its price increased by 72.07 percent. The coffee and coffee maker company posted positive performance following the announcement that it would be acquired by JAB for a reported $13.9 billion.

- Utilities was the best performing sector in the S&P 500, retreating 1.67 percent, the mildest among the sectors. The consumer staples and health care sectors also performed well relative to their peers as investors returned to defensives amid economic and political uncertainties.

- Airline earnings are expected to increase by 10 percent in 2016 to a record $36.3 billion, according to the IATA. Although declining fuel prices will likely aid the industry in its goal, growing economies all around the world also contribute to airlines’ positive forecast, making it now possible for more people to travel by air.

Weaknesses

- Southwestern Energy Co. was the worst performing stock in the S&P 500 this week, losing 23.77 percent. The company’s stock price has fallen as oil prices hit new seven-year lows.

- Energy was the worst performing sector in the S&P 500 this week, slipping 6.4 percent as many of the companies that comprise that sector are finding it difficult to navigate through the plummeting price of crude oil.

- Domestic equities continued to weaken this week as optimism over the economy’s strength gave way to anxiety over the Federal Reserve’s imminent rate hike, which many believe will happen next week. The S&P 500 Index fell 3.8 percent this week, ending at a two-month low.

Opportunities

- Defensive sector earnings continue to remain steady and valuations are still attractive when compared to cyclical sectors. Thus, in a world where companies are struggling to generate profit growth, defensive sector stocks seem to have the upper hand.

- According to BCA, defense contractors appear to be on the cusp of a multiyear expansion in defense spending. There are high odds that 2016 will mark an inflection point in the Department of Defense (DOD) budget, regardless of who moves into the White House. The public is ramping up its support of military efforts and defending against terrorism, and recent events will only solidify political support. Furthermore DOD employment growth has perked up, and may be heralding an upturn in defense outlays.

- Chemical giants Dow Chemical and DuPont announced an all-stock merger of equals. The new company eventually plans to create three businesses focused on agriculture, materials and specialty products. DowDuPont will have an estimated $130 billion market value and be dominant in industrial and agricultural chemicals, plastics and crop seeds. Because of the merged firm’s size and market dominance, antitrust regulators are expected to intensely scrutinize the deal.

Threats

- Equities are much weaker under the surface than major market averages suggest. The S&P 500 is at the top of its range of the past nine months, after having a "false breakdown" in August. While the NASDAQ 100 is close to the 1999 bubble high, the small cap S&P 600 is more than 5 percent below its high of the past year. In contrast with 2004, market breadth is eroding. Equal-weighted market indices have been falling with respect to market-cap-weighted indices for much of the past year. Furthermore, mega-cap indices like the S&P 100 have outperformed while small-cap indices like the S&P 600 have underperformed during the latest market rebound since August. These trends reflect the poor underlying quality of the rally. Consistent with this, the advance/decline line for the S&P 500 has gone sideways for the past two months.

- By signaling to the markets over the past weeks its intention to hike rates next week, the Fed has pushed forward the timing of future rate hikes. Given that the Fed's "dots" are still a fair bit higher than current market expectations, the risk is that rate expectations will continue to adjust upwards, tightening financial conditions in the process. Too abrupt of an adjustment could spike stock volatility.

- While new vehicle sales in the U.S. have boomed in the last few years, and are now sitting at pre-crisis levels, this is not necessarily a reason to be bullish on auto parts stocks. With the Fed likely to raise interest rates, and potentially pushing up borrowing costs in the coming year, auto credit is unlikely to flow as freely. If demand cools, then deflation in new car prices is likely to occur. Pricing pressure may partly reflect cheaper imports on the back of U.S. dollar strength. Auto parts companies also have sizeable foreign exposure and thus the currency is a net negative. Vehicle manufacturers are likely to demand additional supplier price concessions as their own pricing power ebbs, squeezing parts producers' profit margins.

![[thumb]](/images/content_image/data/43/43e9839bfbc29ef72366f3a847c146b1.jpg)

December 8, 2015An Illustrated Timeline of the Gold Standard in the U.S. |

![[thumb]](/images/content_image/data/77/771c9f7d4f66d3505345d376b48bb644.jpg)

December 7, 2015Sweden Declares War on Cash, Punishes Savers with Negative Interest Rates |

![[thumb]](/images/content_image/data/c6/c6594548b204ee8009a04f95854a687b.jpg)

December 2, 2015This Chinese Sector Continues to Score |

The Economy and Bond Market

The price of crude oil fell to seven-year lows as concerns about oversupply pushed U.S. West Texas Intermediate and Brent to near $36 and $39 per barrel, respectively. That along with related worries over slowing global economic growth sent stocks retreating across major markets. The so-called fear gauge, the Chicago Board Options Exchange Volatility Index (VIX), rose to a month-long high of above 20. U.S. Treasuries were in demand, reflecting a desire for safe havens and driving down the yield on U.S. 10-year notes below 2.15 percent, despite expectations that the U.S. Federal Reserve will hike short-term interest rates next week.

Strengths

- November retail sales grew 0.2 percent month-over-month in November, coming in a touch below expectations of 0.3 percent. However, this miss primarily owed to a 0.8 percent plunge in gas station sales, as gas prices have continued to head lower. Looking at the core control group measure, sales growth was a robust 0.6 percent month-over-month, beating consensus forecasts of 0.4 percent. This ended a string of sluggish results in the prior three months.

- Producer prices appreciated 0.3 percent month-over-month in November, surpassing expectations of a modest 0.1 percent increase. Core Producer Price Index (PPI) also grew 0.3 percent, while “core-core,” which excludes trade services, inched up 0.1 percent month-over-month.

- The University of Michigan’s preliminary consumer sentiment index rose to a four-month high of 91.8 in December from 91.3 in November. The rise in confidence was tied to cheaper gasoline and brighter job prospects.

Weaknesses

- The prices for U.S. imported goods fell in November for the fifth straight month as a result of cheap oil, a strong U.S. dollar and slow global growth. Import prices were 0.4 percent lower than October and 9.4 percent off from a year earlier. Petroleum import prices plummeted 44.5 percent from November 2014 while nonfuel import prices fell just 3.2 percent.

- The NFIB small business optimism index fell to 94.8 in November from 96.1 in October, below the expected 96.4. Measures of conditions, expectations and plans were largely less positive in the month.

- Reflecting the continued rout in commodities, mining giant Anglo American announced it plans to shed 60 percent of its mining operations and cut 85,000 jobs in a massive business reorganization. Anglo is the world’s fifth-largest mining firm by market value.

Opportunities

- According to BCA, government spending might give the euro area economy some much-needed support over the coming quarters. In the near term, the refugee crisis and counter-terrorism security provide a clear and urgent rationale for more government spending. Although such spending means that euro area governments will stray from the Commission's official deficit targets, Brussels has nonetheless given its tacit approval. Brussels is showing leniency because, after five years of centrally-imposed austerity, the euro area is now close to a structural budget balance. The IMF forecasts the euro area fiscal impulse to stabilize in 2016 and turn positive in 2017. Any additional spending on the refugee crisis and counter-terrorism security will simply accelerate this rebound in government spending.

- In a year of severe price collapses in commodities markets, grains have held up particularly well falling only 12.8 percent thus far. This likely will continue to be the case in the current crop year that goes through mid-2016. The International Grains Council (IGC) estimates total grains production will be around 2 percent lower than the 2014/15 crop, led by decreases in global corn production. This estimate is supported by USDA data. Global consumption will inch higher as food demand continues to increase. This will be supportive of grain prices over the next six months, particularly corn.

- Negotiators at the Paris summit aim to wrap up a global agreement to curb climate change on Saturday. The summit is entering a final push to try to secure a global agreement that would stake out a long-term strategy for dealing with climate change.

Threats

- Soft U.S. domestic data prints would increase concerns that the Fed is making a policy mistake by initiating the policy renormalization process too early. Consumer prices and homebuilders' sentiment releases on Tuesday and housing starts on Wednesday will be relevant data releases.

- The Investment Grade index spread has been trending higher since last year, but has only recently returned to its historical average. Investment grade spreads excluding the distressed energy sector have also been rising, though not as sharply. Recent trends in ratings migration confirm that spread widening is reflective of deteriorating corporate credit quality. Since the beginning of August, Moody's has downgraded 21 Investment Grade rated issuers and upgraded only 13. If we include both Investment Grade and High Yield issuers, downgrades have almost doubled upgrades over the past three months. The combination of tightening monetary conditions, high and rising corporate balance sheet leverage, worsening corporate profitability and tightening bank lending standards is a precarious mix for corporate credit performance.

- The high-yield corporate bond market has historically been an early warning indicator for equities. Both floating-rate leveraged loan prices and fixed-rate high-yield corporate bond spreads have been worsening for more than a year. In contrast, both leveraged loans and junk bonds appreciated in the run-up to the June 2004 first Fed rate hike. Importantly, these trends do not change if the energy sector is excluded. This is not surprising given that none of the signs of strength in profits, economic growth and corporate health that existed in 2004 are evident right now. Furthermore, back then a falling dollar also lent support.

Gold Market

For the week, spot gold closed at $1,074.74 down $12.10 per ounce, or 1.11 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, fell 3.09 percent. Junior miners just slightly outperformed seniors for the week as the S&P/TSX Venture Index slipped 2.91 percent. The U.S. Trade-Weighted Dollar Index fell 0.76 percent for the week.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Dec-10 | US Intial Jobless Claims | 270k | 282k | 269k |

| Dec-11 | GE CPI YoY | 0.40% | 0.40% | 0.40% |

| Dec-11 | US PPI Final Demand YoY | -1.40% | -1.10% | -1.60% |

| Dec-11 | CH Retail Sales YoY | 11.10% | -- | 11.00% |

| Dec-15 | GE ZEW Survey Current Situation | 54.2 | -- | 54.4 |

| Dec-15 | GE ZEW Survey Expectations | 15 | -- | 10.4 |

| Dec-15 | US CPI YoY | 0.40% | -- | 0.20% |

| Dec-16 | EC CPI Core YoY | 0.90% | -- | 0.90% |

| Dec-16 | US Housing Starts | 1140k | -- | 1060k |

| Dec-16 | US FOMC Rate Decision (Upper Bound) | 0.50% | -- | 0.25% |

| Dec-17 | US Initial Jobless Claims | 272k | -- | 282k |

Strengths

- Although gold was down for the week it was the best performing precious metal. Perhaps gold was underpinned by the news that China added the most to its central bank gold reserves in five months, according to Bloomberg. Gold prices saw the biggest drop in more than two years, plunging 6.8 percent in November. Data from the People’s Bank of China (PBOC) this week shows the value of gold assets at $59.52 billion at the end of last month.

- Shanghai Gold Exchange withdrawals could be heading for a record year, says Lawrie Williams. Total withdrawals so far this year have amounted to a little under 2,405 tonnes, and with four more weeks of withdrawals still to come, Williams notes that this year’s total could be heading for the high 2,500s. This would be nearly 400 tonnes more than in the previous record year.

- South Africa’s President Jacob Zuma fired his finance minister this week, and replaced him with a little-known lawmaker, according to Bloomberg. The South African rand plunged against the dollar on this news, causing South African gold miners to surge in reaction due to the margin expansion from a falling rand.

Weaknesses

- Platinum was the worst performing precious metal this week. Johnson Matthey noted that platinum remains more expensive than gold jewelry at the retail level in China and that could be hurting its demand.

- According to The Statesman out of Mumbai, the Sri Siddhivinayak temple in India is the first religious trust/institution in the country to respond to the government’s call to invest in Prime Minister Modi’s Gold Monetization Scheme. The institution had an initial investment of 40kg of gold from its chest. It’s clear that there is a continued political push to support the scheme. The Statesman article notes that the famous Mumbai temple has 165kg gold in its vault.

- Barnabas Gan, an economist at Oversea-Chinese Banking Corp., believes that gold bullion will drop each quarter to $950 an ounce by the end of 2016. Gan’s prediction puts gold at the end of 2016 about 12 percent below prices now, according to a Bloomberg article.

Opportunities

- Pessimism by hedge funds came at the wrong time last week, with money managers boosting their gold net-short position to the highest ever just prior to the precious metal’s biggest rally since September, according to Bloomberg. George Zivic, a New York-based portfolio manager at Oppenheimer Funds, thinks Yellen spoke a bit more dovish than people expected. “I think less people are now willing to take the long-dollar, short gold trade,” Zivic said. “It was a very crowded trade.”

- What will happen after the Federal Reserve hikes interest rates? According to Macro Risk Advisors’ (MRA’s) Daily Note, one chart that has been making the rounds, and shows average performance of the U.S. dollar after the Fed hikes, explains a lot. MRA explains that for the past six rate hike cycles, the U.S. dollar has traded lower on average after the Fed starts hiking.

- According to American-German researcher, historian, and strategic risk consultant F. William Engdahl, a gold-backed ruble and a gold-backed yuan could start a “snowball exit” from the U.S. dollar. Engdahl explains that if this happens it would “diminish America’s ability to use the reserve dollar role to finance overseas wars.” He adds that the irony here is the central banks of China, Russia, Brazil and others (that are opposed to U.S. foreign policy course), are forced to stockpile dollars in the form of “safe” U.S. treasury debt. More recent trade deals between China and Russia have specified that either the yuan or ruble would be used to settle balances and not the dollar.

Threats

- Bank of America’s metal analyst Michael Widmer says gold prices could end up falling below $1,000 an ounce in the first quarter of the year. Despite the painful forecast for the precious metal, BofA expects rising inflation in the second half of the year to be “supportive of the beleaguered market,” and says gold could jump to $1,250 an ounce in the fourth quarter.

- There seems to be a peculiar divergence emerging between the High Yield Index and the S&P 500 Index, which have previously followed one another closely. As of late, the High Yield Index has plunged but the S&P 500 has largely held up. While the energy sector has dominantly been the source of the stress, this discontent could easily spill over into the banks which lent the energy companies the money to drill. While the broad market has been flirting with all-time highs and gold prices already down significantly, the threat of a market correction could be buffered by rebalancing towards a higher precious metals exposure which is out of favor right now.

- On Friday, prices on junk-bond securities sank to levels not seen in six years, according to Bloomberg. Adding to the shocking news (which comes a day after a well-known Wall Street firm froze withdrawals from a credit mutual fund), billionaire investor Carl Ichan wrote the following on his Twitter account: “The meltdown in High Yield is just beginning.” Gluskin Sheff noted that the corporate bond default rate has jumped to 2.6 percent, the highest in six years, and is poised to rise further to 4.6 percent next year.

Energy and Natural Resources Market

Strengths

- The continued downtrend in the price of crude oil has weighed heavily on the energy sector, however not everyone in the energy patch is witnessing a decline in revenue. As oil supply continues to grow with no sign of demand turning up, oil tankers have been performing very well, as many of them have recently become the equivalent of offshore storage platforms where oil sits until better times emerge. According to Bloomberg, this week oil tanker rates soared to the highest in seven years, with many of the tankers waiting days, if not weeks, for space to clear in on-land storage tanks.

- Gold stocks were the best performing sector in the global resources universe for the week, retreating 3.06 percent, the mildest among its peers. The yellow metal is often regarded as a safe haven asset alternative, and with the dollar’s poor performance recently coupled with increasing certainty that the Fed will raise rates next week, many investors turned to gold again.

- Diamondback Energy was the best performing stock this week, with a contribution to return of 0.15 percent, alongside news that J.P. Morgan had named the energy company one of its top small- and mid-cap picks.

Weaknesses

- This week, oil closed at the lowest level in more than six years. Oil’s continued retreat was partly fueled by speculation that OPEC would do nothing material to curb the markets’ current oversupply. Additionally, OPEC’s November production levels were above its “official” cap of 31.5M bbl/day. Furthermore, the Organization of the Petroleum Exporting Countries does not compromise to abide to production targets going forward.

- The worst performing sector this week was oil & gas exploration and production, which fell 8.35 percent, while WTI crude fell an additional 10.83 percent, ending the week at $35.27 per barrel.

- This week’s worst performing stock in the SPDR S&P Global Natural Resources Index was Anglo American. The stock plummeted 22.1 percent this week, following news that the company would cut its employee workforce from 135,000 to nearly 50,000 over the next few years in addition to suspending dividend payments for the second half of 2015 and 2016 in an effort to cope with the recent collapse in commodity prices.

Opportunities

- Many of the world’s largest mining companies are restructuring their businesses and fighting deteriorating profits as commodities across the globe continue to fall. Glencore announced that it would reduce its debt even further, scale back select operations, and sell more assets. The firm is the latest company in the mining space that has been forced to choose more aggressive measures in response to the downward trend in commodities.

- Last Friday, Dow Chemical and DuPont announced their agreement to combine in what will be an all-stock merger. Most analysts expect this merger to bode well for both companies, citing the creation of a stronger agrochemical asset, a mutual solution to several structural challenges, as well as added pressure for further consolidation in the agrochemical section. With activists’ pressure set to create the largest chemical company in the world, we may see more value creation in the global resources spaces via activist investors.

- Global growth will pick up in 2016 leading to the global purchasing managers’ index (PMI) data to post its first year-over-year improvement since 2013, according to a report by Scotiabank Portfolio Strategist Vincent Delisle. The report argues that global growth can pick up given that global monetary conditions will remain accommodative. Further to this, Delisle argues that “commodities don’t need a super-cycle to rebound in 2016,” and could rebound from oversold levels as Chinese growth stabilizes, a more likely outcome after the recent easing measures implemented to stem the slide.

Threats

- While many investors believe that China’s appetite for industrial raw materials drive global economic growth, the Baltic Dry Index may tell a different story. Last month, the index of shipping rates for bulk materials fell to an all-time low, as China’s current demand continues a downward trend. This weakening demand affects ships’ rates, which then have a negative effect on subsequent asset values.

- Natural gas continued its five-month decline in price as the commodity’s deliveries in January fell 2.3 percent, to $2.015 per million British thermal units. In addition to tumbling prices, natural gas producers often find themselves with a sizable debt, and their excess inventories make it more difficult for the producers to pay down that debt.

- Since the beginning of the year, 18 oil and gas drillers have begun the process of filing for bankruptcy protection. Many of these companies have seen a correspondence between their falling revenues and the ongoing decline in the price of crude oil, which has fallen more than 33 percent year-to-date.

China Region

Strengths

- South Korea was the best performing market in Asia this week, as its central bank left the benchmark interest rate unchanged ahead of the Federal Reserve decision next week. The Korea Stock Exchange KOSPI Index lost only 1.31 percent this week.

- Technology was the best performing sector in Asia this week, driven largely by a rebound in large cap Korean electronics makers after its central bank’s rate decision. The MSCI Asia Pacific ex Japan Information Technology Index lost only 1.34 percent this week.

- The Philippine Peso was the among the best performing currencies in Asia this week, weakening by just 0.28 percent, as the country remains better shielded in an Asian context from a potential start of tightening cycle by the Federal Reserve next week.

Weaknesses

- Thailand was the worst performing market in Asia this week, as the energy heavy Thai equity index made a fresh 52-week low affected by crude oil prices after the OPEC meeting. The Stock Exchange of Thai Index retreated 3.95 percent this week.

- Energy was the worst performing sector in Asia this week, as the decline in crude oil prices intensified on global supply concerns after OPEC reaffirmed its determination to maximize production. The MSCI Asia Pacific ex Japan Energy Index lost 7.47 percent this week.

- The South Korean won was the worst performing currency in Asia this week, weakening by 1.95 percent, as worries linger over potentially larger Chinese renminbi depreciation which might rekindle competitive devaluation given Korea’s significant overlap with China in exports product category.

Opportunities

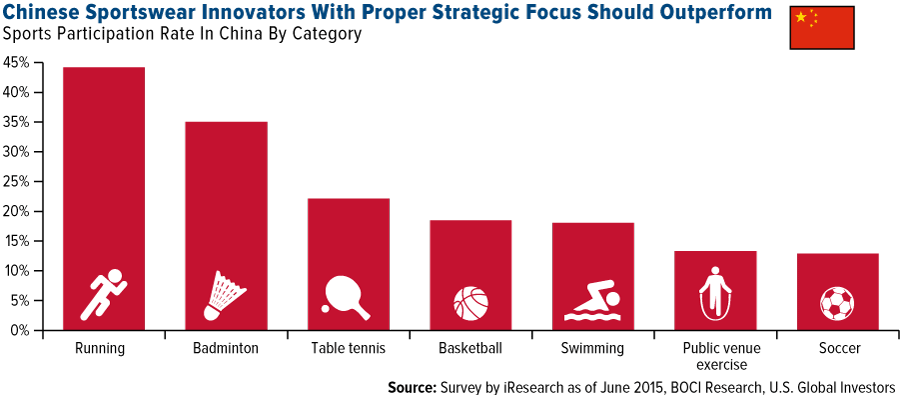

- Rising health consciousness among China’s urban middle class and government policy support via accelerating construction of and allowing access to more public sports facilities should continue to drive the rising trend of sports participation in the country. Chinese sportswear innovators who are capturing both mass market, popular categories such as running, and emerging, niche categories such as soccer, with high quality, value products should be able to sustain their outperformance.

- The Chinese renminbi further depreciated this week, to a level lower than late August when a sudden devaluation of the Chinese currency spooked global equity, currency and commodity markets.

- Sustained market expectation of further government policy accommodation for the Chinese residential property market after President Xi Jinping’s recent emphasis on the importance of new home inventory de-stocking should keep investor sentiment buoyant towards quality local developers. Latest reports of insurance companies raising equity stakes in major city developers and market chatter of potential introduction of rural stimulus also bode well for the sector.

- As global investor risk appetite retrenches ahead of Federal Reserve’s rate decision next week and intensifying declines in crude oil sent U.S. junk bond spreads soaring, cash as the ultimate defensive asset class may once again outperform as volatility picks up in various asset classes around the world.

Threats

- Further depreciation of the Chinese renminbi this week to a level lower than late August when a sudden devaluation of the Chinese currency, which spooked global equity, currency, and commodity markets. This same reaction could weigh on investor sentiment ahead of Federal Reserve’s rate decision next week. So far, there is little convincing sign of a sustainable recovery in Chinese economic activity from this week’s release of the country’s November economic data.

- The latest news on additional Chinese efforts to crack down on illegal activity related to bank card use in Macau reinforces market concerns that China’s vigilance against further capital flight may continue to worsen the liquidity situation in Macau and, coupled with unabated anticorruption measures, to add to uncertainties in the operating environment for casino operators in Macau.

- The recent mini-recovery in Malaysian stocks might not be sustainable, given the prospect of slowdown in both private consumption, led by weaker income growth and high household indebtedness, and public investment due to fiscal retrenchment next year. Lingering uncertainties on crude oil prices and domestic political scandal might continue to weigh on the Malaysian ringgit and investor sentiment.

Emerging Europe

Strengths

- Romania was the best relative performing market this week, losing 1.08 percent. GDP expanded 3.6 percent in the third quarter and 3.7 percent during the first nine months of this year. Many economists predict strong economic growth next year for Romania, driven by private consumption and recovering investment.

- The Czech koruna was the best performing currency this week, gaining 95 basis points against the U.S. dollar. Inflation unexpectedly slowed in November, adding to the argument that the central bank delay exit from its near-zero policy rates. Czech year-over-year inflation slowed to 0.1 percent in November from 0.2 percent in October.

- Health care was the best performing sector among eastern European markets this week.

Weaknesses

- Turkey was the worst performing market this week, losing 5.4 percent. Turkey announced a new economic program that disappointed many investors. Financial markets have been awaiting a program that focuses on fiscal discipline and plans to boost labor productivity and household savings. Instead, the new reform plan is in line with populist, consumption-led policies favored by President Tayyip Erdogan. Turkey could see a higher budget deficit than 0.7 percent of GDP, which was the initial announcement.

- The Russian ruble was the worst performing currency, losing 3.3 percent against the U.S. dollar. Brent crude oil lost 11.8 percent during the past five days, closing at a new low of $37 per barrel. On Friday, the Central Bank of Russia extended its pause on the easing cycle and left the key interest rate unchanged at 11 percent due to higher inflation risk.

- Consumer discretionary was the worst performing sector among eastern European markets this week.

Opportunities

- Eurozone investor confidence rose for a second straight month in December to its highest level in four months. This came on the European Central Bank's (ECB’s) move to add more stimulus in order to boost the region's economy. The Sentix Investor Confidence Index climbed to 15.7 from 15.1 in November.

- According to the Global Banks Outlook 2016, published by UBS on December 6, investors could see a recovery in many regions (with exception of Poland), especially in Russia, Hungary and Turkey. Next year UBS is expecting high earning per share (EPS) growth off of a low base. Russian banks could benefit from substantial rate easing.

- The Greek parliament approved the country’s 2016 budget and the government expects zero growth in 2015 GDP numbers, compared with an earlier forecast of a 2.3 percent contraction. For 2016, the budget projects a 0.7 percent fall in GDP, less than the 1.3 percent contraction predicted earlier.

Threats

- Next week the Federal Reserve may raise interest rates for the first time since 2006. Such a move could put pressure on emerging European currencies, especially the Turkish lira, as Turkey holds large debt funded in U.S. dollars.

- Poland’s state-owned companies may continue to see management shakeups by a new government. The first leader of a state-controlled company to step down was Pawel Tamborsk, the head of the Warsaw Stock Exchange. Andrzej Klesyk, CEO of PZU, also resigned along with a few other top managers of utilities companies. With new management, the state-owned companies may alter their strategies; there is risk when markets are already depressed. The Warsaw Stock Exchange is trading at a six-year low.

- Turkey’s cost of capital is rising. The government’s 10-year dollar bond yield was 5 percent on December 4, up from 4.7 percent in 2014, and 4.1 percent just before Turkey shot down a Russian jet in November.

© US Global Investors