How to Diversify into International Growth Cycles

Today we have a joint blog post by Jeff Everett, Dale Winner, and Venk Lal with the EverKey Global Equity team, which manages the Wells Fargo Advantage International Equity Fund.

When it comes to portfolio diversification, the dialogue tends to focus on the domestic side of investing: market-cap size, stocks versus bonds, or sector exposure. What’s often missed is the need to think regionally, particularly regarding international equities. We believe global markets have reached an inflection point and are poised to top U.S. markets, fueled by central bank stimulus, regional reforms, resulting economic recoveries, and attractive valuations. In this blog post, we’ll discuss the importance of positioning your portfolio to capture overseas opportunities and look at three types of companies that position themselves to capitalize on improving business climates.

Diversifying into divergence

The word divergence sometimes brings to mind negative connotations, from discrepancies to disagreements. But when it comes to diversifying into overseas markets, divergence can be a positive driver of risk-adjusted returns. The reason: International equities allow investors to tap into diverging market conditions.

Let’s look at Europe, Japan, and the U.S. Each of these regions is operating within a different cycle in terms of economic recovery, stock valuations, corporate earnings, and liquidity, as influenced by central bank policies. For example, one region’s companies may be experiencing the benefits of economic growth, while another region’s companies are preparing themselves for when conditions improve. Here are a few examples of divergence at work:

- Valuation cycles:Japanese and European equities currently trade at 52% and 42% discounts to U.S. equities, respectively.

- Earnings cycles:Japanese and European companies currently benefit from earnings tailwinds, such as low currency value, which tilts exports to their advantage, versus U.S. companies.

- Liquidity cycles:Europe’s and Japan’s quantitative easing (QE) programs are new and ongoing, respectively, with room to expand, if necessary. Meanwhile, QE has ended in the U.S.—and with it, extra liquidity for business lenders.

When considering international diversification, it’s not enough to simply choose a few countries and sit idle. For investors, thinking regionally also requires paying attention to companies that are making strategic moves to prepare for their regions’ evolving market conditions. From here, we’ll look at examples of such companies in three countries: Germany, Italy, and Japan.

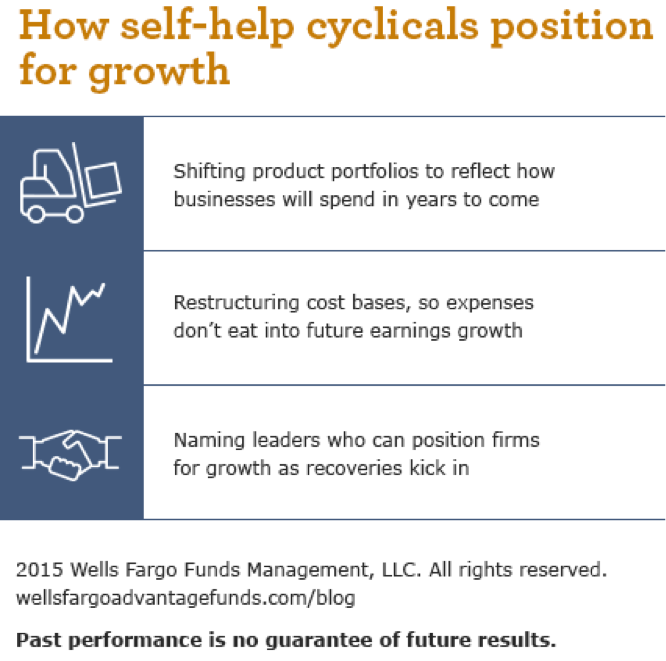

Positioning for growth through self-help

It’s hard to believe Germany was once considered the sick man of Europe, with an almost 12% unemployment rate a decade ago. However, after a decade of reforms, central bank stimulus, and government-led fiscal stability, Germany’s economy is considered Europe’s economic powerhouse. Wages have increased, unemployment has fallen, and business confidence has shown steady improvement in 2015 despite a slight October dip.

Here’s the thing: While business confidence is rising, business investment is still pent-up. But we believe capital expenditures are poised to rebound; we just can’t pinpoint the exact date when this rebound will occur. Therefore, investors considering Germany’s markets should look at companies that make strategic operational changes so that when the economy kicks into full-growth mode, they’ll be at an optimal position to grow as well. We call these companies self-help cyclicals. For example, a large German industrial recently named a new CEO who is taking steps to improve the firm’s operating margins through cost restructuring. He’s also reshaping the firm’s product portfolio to focus on businesses that reflect how companies will invest in years to come, thinking ahead to when capital expenditures rise.

Positioning for growth by seizing local opportunities

Led by reform-minded Prime Minister Matteo Renzi, Italy’s government is creating growth prospects for the country’s businesses through reform policies, privatization of government enterprises, and infrastructure upgrades. We think investors should pay attention to firms that are poised to capitalize on these opportunities.

For example, Italy recently privatized 40% of its national postal service through an initial public offering. Similar to U.S. bank branches, Italy’s post offices sell bonds and certificates of deposit. But the region’s triple-recession and low interest rates hurt these products’ return. To help customers gain exposure to potentially higher return investments, the newly privatized postal service signed a deal with one of Italy’s largest asset managers to sell equity-based products at post office locations.

Italy’s capital-equipment sector provides another promising example. Amidst pent-up business investment, European telecom firms have fallen behind on upgrading their networks. Italy’s Prime Minister is spearheading apublic/private collaboration to bring high-speed internet to 85% of the country. Within that plan is a project to build a 4G fiber optic network in Northern Italy. And right in that project’s backyard is an Italian industrial company that manufactures cable equipment for telecoms.

Positioning for growth by embracing reform

In our last blog post, we discussed a series of reforms from Japan’s Prime Minister Shinzo Abe to make businesses more profitable, transparent, and accountable to shareholders. Also on Abe’s reform radar: unwinding the decades-long practice of cross-held shares, which, in Japan, has led to businesses owning large quantities of shares in each other, locking up trillions in capital that could be applied to the economy.

Abe’s goal is for Japanese companies to make better use of their capital, be it through business investment or through buybacks and dividends to benefit investors. Bloomberg reports that Japanese companies could unload as much as 8.5 trillion yen ($71 billion) in cross-held shares the next few years.

Another example of a reform-embracing firm is a Japanese conglomerate whose product portfolio touches several components of Japan’s economy, from transportation to technology. In recent years, the firm introduced aperformance-based pay and promotion system to replace the former system in which salaries were based on age and length of service. For that company, these changes coincide with results that include doubling profits over the past 3 years and posting 10-year-high operating margins.

Why long-term thinking is essential

One last point about diversifying in overseas markets: Amidst the divergence of market events, one country may operate at a different speed than another.

For example, in the U.S., our liquidity cycle was initiated quickly in 2008 through the Federal Reserve’s QE program. Europe’s liquidity cycle, however, moved at a slower pace, as planning, debating, and passing a QE program took more time. But just because Europe’s program advanced at a slower pace doesn’t mean it will be any less effective in sparking business investment. Already, almost 40% of eurozone banks say they have used added liquidity from the European Central Bank’s QE program for lending to businesses.

Therefore, it’s essential to take the long view when thinking regionally. This applies to the patience and foresight needed to diversify into non-U.S. regions and for researching non-U.S. companies that are likewise taking the long view as they prepare themselves for growth.

Please visit our blog, AdvantageVoice, for additional viewpoints from Wells Fargo Asset Management’s investment strategists, portfolio managers, and practice management experts. You can also follow us on Twitter at @WFAssetMgmt for real-time updates. Are you an advisor or institutional investor? Check out our website for investment professionals.

The views expressed are as of 12-8-15 and are those of Jeff Everett, Dale Winner, Venk Lal, and Wells Fargo Funds Management, LLC. The information and statistics in this report have been obtained from sources we believe to be reliable but are not guaranteed by us to be accurate or complete. Any and all earnings, projections, and estimates assume certain conditions and industry developments, which are subject to change. The opinions stated are those of the authors and are not intended to be used as investment advice. The views and any forward-looking statements are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally, or any mutual fund. Wells Fargo Funds Management, LLC, disclaims any obligation to publicly update or revise any views expressed or forward-looking statements.

Wells Fargo Funds Management, LLC, a wholly owned subsidiary of Wells Fargo & Company, provides investment advisory and administrative services for Wells Fargo Advantage Funds®. Other affiliates of Wells Fargo & Company provide subadvisory and other services for the funds. The funds are distributed by Wells Fargo Funds Distributor, LLC, Member FINRA, an affiliate of Wells Fargo & Company.

Not FDIC Insured • No Bank Guarantee • May Lose Value

© Wells Fargo Asset Management