My friend and colleague, Michael Lebowitz of 720 Global Research, recently penned a response to Larry Summers commentary on the economy’s weakened ability to withstand higher interest rates. To wit:

“In his Dec. 7 op-ed, ‘Before the next recession,’ Lawrence Summers correctly said the economy’s weakened ability to withstand higher interest rates is based on the fact that lower rates in the past have pulled forward demand for goods and services, thereby leaving less demand in the future. This holds true for personal consumption, but, just as important, low rates have allowed weak, unproductive companies to stay in business and continue producing. Put these two factors together and one realizes the economy is plagued with weak demand and oversupply. Anyone who has taken a basic college economics course knows that translates into lower prices and weaker economic growth.

This is important to understand because Mr. Summers asked how Federal Reserve policy can “delay and ultimately contain” the next recession. This long-held mentality of constant growth, with no tolerance for recession, has not allowed the economy to perform its Darwinian function and weed out excesses.

Today’s economy has a massive level of indebtedness from consumption of days past and a long history of misallocated capital that has tied up funds that could have otherwise been chasing the next great innovation and propelling our economy forward. “

Michael makes an important point that is often forgotten by the Federal Reserve’s desire to try and manipulate economic cycles.

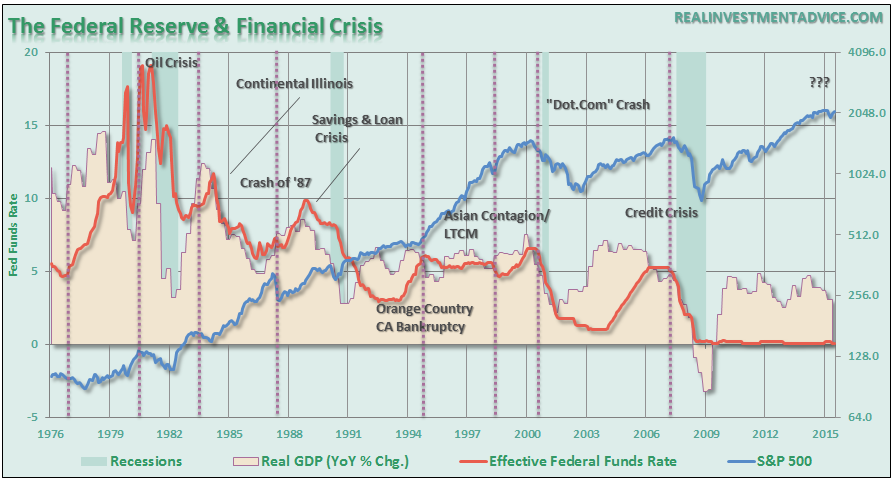

If we take a look back at recent history, it is more than just coincidence that the Fed’s not-so-invisible hand has left fingerprints on previous financial unravellings.

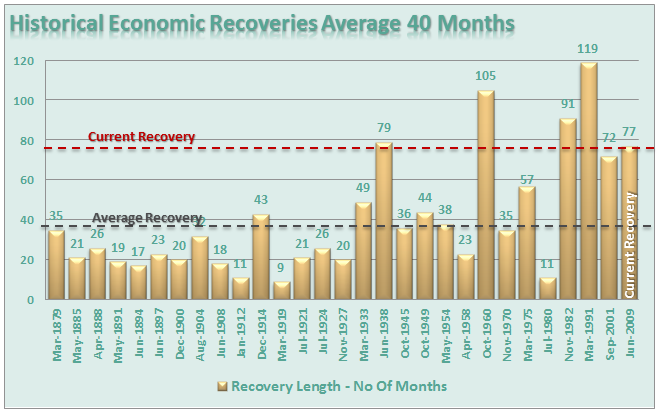

The problem for the Federal Reserve at this juncture is that despite hopes of a “recession free” economy over the next several years, the current economic cycle is already very long historical standards.

Given the years of “ultra-accommodative” policies following the financial crisis, the majority of the ability to “pull-forward” consumption appears to have run its course as witnessed by plunging rates of imports, surging levels of inventories and deteriorating profit margins even outside of the energy related sector.

Austrian’s Had It Right

According to Keynesian theory, some microeconomic-level actions, if taken collectively by a large proportion of individuals and firms, can lead to inefficient aggregate macroeconomic outcomes, where the economy operates below its potential output and growth rate (i.e. a recession). Keynes contended that “a general glut would occur when aggregate demand for goods was insufficient, leading to an economic downturn resulting in losses of potential output due to unnecessarily high unemployment, which results from the defensive (or reactive) decisions of the producers.” In other words, when there is a lack of demand from consumers due to high unemployment then the contraction in demand would, therefore, force producers to take defensive, or react, actions to reduce output.

In such a situation, Keynesian economics states that government policies could be used to increase aggregate demand, thus increasing economic activity and reducing unemployment and deflation. Investment by government injects income, which results in more spending in the general economy, which in turn stimulates more production and investment involving still more income and spending and so forth. The initial stimulation starts a cascade of events, whose total increase in economic activity is a multiple of the original investment.

This seemed to work. From the 1950’s through the late 1970’s interest rates were in a generally rising trend with the Federal Funds rate at 0.8% in 1954 and rose to its peak of 19.1% in 1981. When the economy went through its natural and inevitable slowdowns, or recessions, the Federal Reserve could lower interest rates which in turn would incentivize producers to borrow at cheaper rates, refinance activities, etc. which spurred production and ultimately hiring and consumption.

As the economy recovered and began to grow again, the Fed would need to raise interest rates. This program seemed to work fairly well as interest rates went to a level higher than the last as the economy grew at an increasingly stronger level. This provided the Federal Reserve with plenty of room to maneuver during the next evolution of the business cycle.

However, beginning in 1980 that trend changed as we discovered the world of financial engineering, easy money, and the wealth creation ability through the abuse of leverage. However, what we did not realize then, and are still ignoring today, is that financial engineering had a very negative side effect of deteriorating economic prosperity.

The Austrian business cycle theory attempts to explain business cycles:

“As the inevitable consequence of excessive growth in bank credit, exacerbated by inherently damaging and ineffective central bank policies, which cause interest rates to remain too low for too long, resulting in excessive credit creation, speculative economic bubbles and lowered savings.”

In other words, the proponents of Austrian economics believe that a sustained period of low interest rates and excessive credit creation results in a volatile and unstable imbalance between saving and investment. In other words, low interest rates tend to stimulate borrowing from the banking system that in turn leads, as one would expect, to the expansion of credit. This expansion of credit then, in turn, creates an expansion of the supply of money.

Therefore, as one would ultimately expect, the credit-sourced boom becomes unsustainable as artificially stimulated borrowing seeks out diminishing investment opportunities. Finally, the credit-sourced boom results in widespread malinvestments.

When the exponential credit creation can no longer be sustained a “credit contraction”occurs which ultimately shrinks the money supply and the markets finally “clear” which then causes resources to be reallocated back towards more efficient uses.

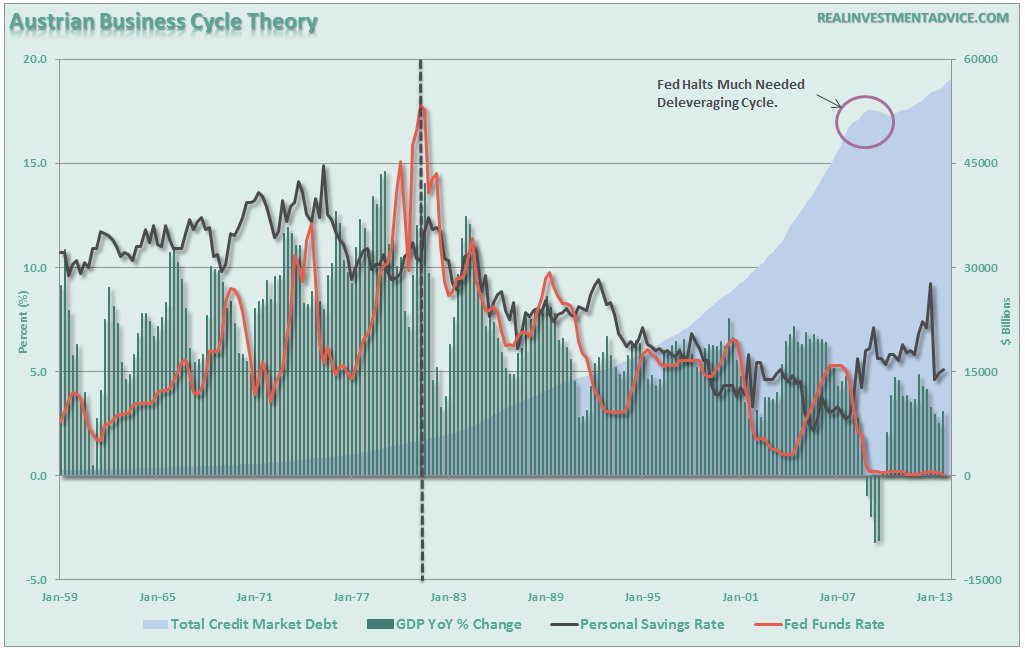

As shown in the chart above, actions by the Federal Reserve halted the much needed deleveraging of the household balance sheet. With incomes stagnant and debt levels still high, it is of little wonder why 80% of American’s currently have little or no “savings” to meet an everyday emergency.

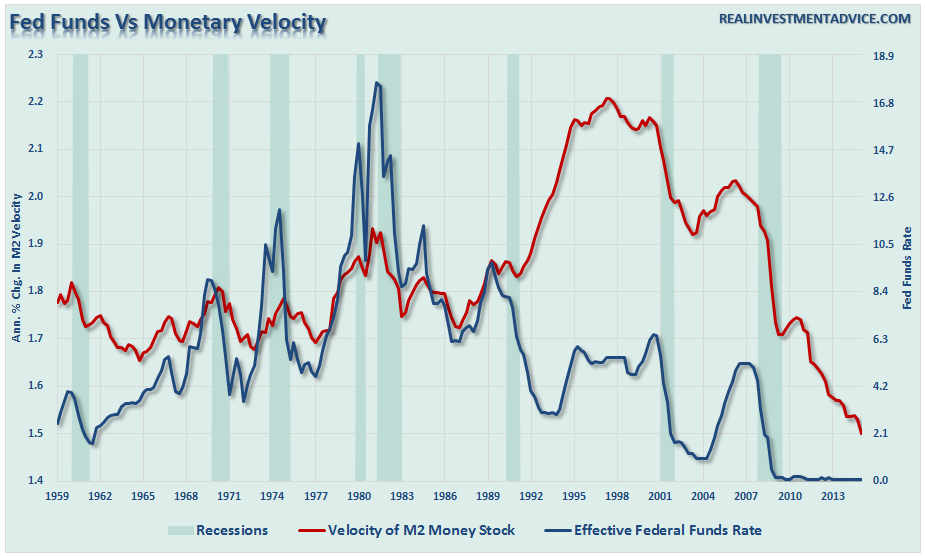

Furthermore, the velocity of money has plunged as overall aggregate demand has waned.

For the last 30 years, each Administration has continued to foster the Keynesian monetary and fiscal policies believing the model worked – when it reality most of the aggregate growth in the economy has been financed by deficit spending, credit and a reduction in savings. In turn, this reduced productive investment in the economy and the output of the economy slowed. As the economy slowed, and wages fell the consumer was forced to take on more leverage that also decreased savings. As a result, of the increased leverage, more of their income was needed to service the debt.

All of these issues have weighed on the overall prosperity of the economy and what has obviously gone clearly awry is the inability for the current economists, who maintain our monetary and fiscal policies, to realize what downturns encompass.

The Fed continues to follow the Keynesian logic, mistaking recessions as periods of falling aggregate demand, and they rush to try and stimulate demand hoping to increase the rate of consumption. However, the reason the policies that have been enacted by the current Administration have all but failed to this point, be it from “cash for clunkers” to “Quantitative Easing”, is because all they have done is either to drag future consumption forward or to stimulate asset markets that create an artificial wealth effect thereby decreasing savings that could, and should have been, used for productive investment.

The Keynesian view that “more money in people’s pockets” will drive up consumer spending, with a boost to GDP being the result, is clearly wrong. It has not happened in 30 years. What is missed is that things like temporary tax cuts or one time injections do not create economic growth but merely reschedules it. The average American may fall for a near-term increase in their take home pay and any increased consumption in the present will be matched by a decrease later on when the tax cut is revoked.

This is, of course, assuming the balance sheet at home is not broken. As we saw during the period of the “Great Depression” most economists thought that the simple solution was just more stimulus. Work programs, lower interest rates, government spending all didn’t work to stem the tide of the depression era.

The problem currently is that the Fed’s actions halted the “balance sheet” deleveraging process keeping consumers indebted and forcing more income to pay off the debt which detracts from their ability to consume. This is the one facet that Keynesian economics does not factor in. More importantly, it also impacts the production side of the equation as well since no act of saving ever detracts from demand. Consumption delayed is merely a shift of consumptive ability to other individuals, and even better, money saved is often capital supplied to entrepreneurs and businesses that will use it to expand, and hire new workers.

The continued misuse of capital and continued erroneous monetary policies have instigated not only the recent downturn but actually 30 years of an insidious slow moving infection that has destroyed the American legacy. “Recessions” should be embraced and utilized to clear the “excesses” that accrue in the economic system during the first half of the economic growth cycle. Trying to delay the inevitable, only makes the inevitable that much worse in the end.

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“. Follow Lance onFacebook, Twitter and Linked-In