In the summer of 1885 William R. Travers, prominent NYC businessman and builder of Saratoga Race Track, was vacationing in Newport, Rhode Island. He pointed out a long line of beautiful yachts tied up in the harbor. When he was informed that they all belonged to Wall Street brokers he simply asked,

“Where are their clients’ yachts?”.

When it comes to investing, there is nothing more dangerous to an individual’s future outcomes than falling prey to the many myths perpetrated on them by Wall Street. The investment business is, after all, just that – a business.

What Wall Street has learned, as the days of commission-based trading have been relegated to computerized trading, is that fee based management is a very profitable annuitized business model. The only trick is keeping individuals fully invested at all times so fees can be collected. This need has generated some of the biggest “myths”in the investment world to keep investors piling money into mutual funds, hedge funds and advisory accounts. Here are 5-myths worth thinking about.

1) Stay Invested – The Market Always Returns 10%

You have heard this one plenty. “Over the long-term” the stock market has generated a 10% annualized total return. So, just plunk your money down and you will be wealthy.

The statement is not entirely false. Since 1900, stock market appreciation plus dividends has provided investors with an AVERAGE return of 10% per year. Historically, 4%, or 40% of the total return, came from dividends alone. The other 60% came from capital appreciation that averaged 6% and equated to the long-term growth rate of the economy.

However, there are several fallacies with the notion that the markets long-term will compound 10% annually.

1) The market does not return 10% every year. There are many years where market returns have been sharply higher and significantly lower.

2) The analysis does not include the real world effects of inflation, taxes, fees, and other expenses that subtract from total returns over the long-term.

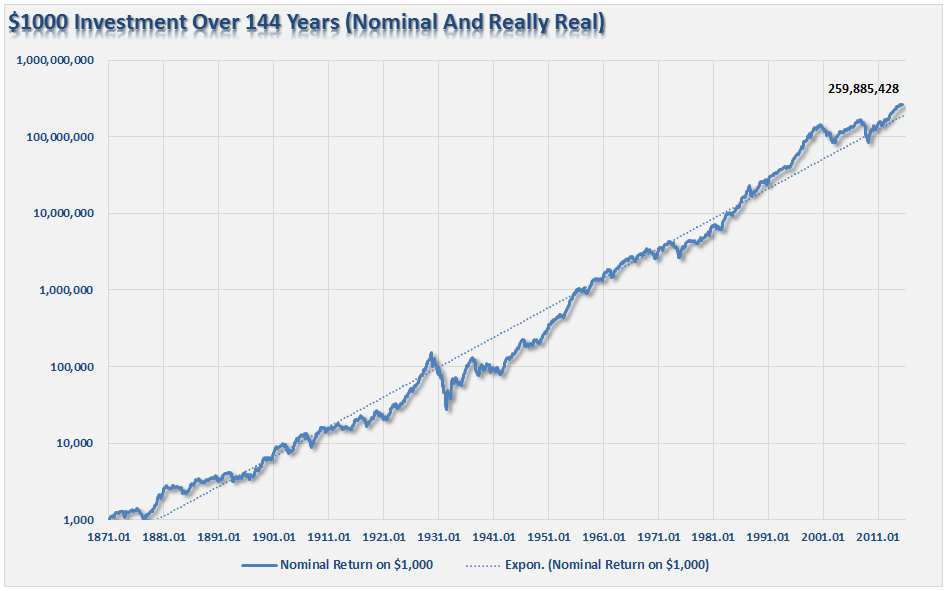

3) You don’t have 144 years to invest and save.

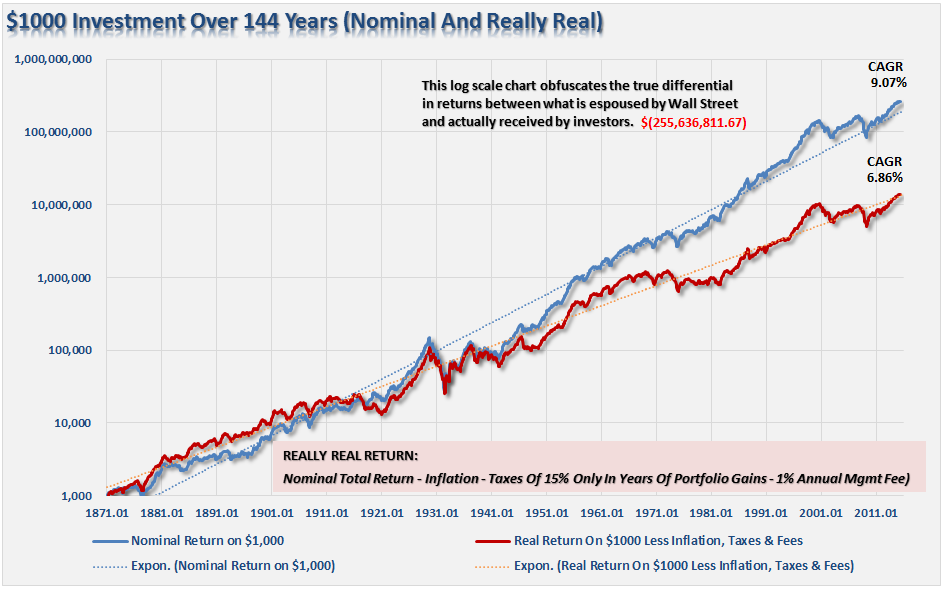

The chart below shows what happens to a $1000 investment from 1871 to present including the effects of inflation, taxes, and fees. (Assumptions: I have used a 15% tax rate on years the portfolio advanced in value, CPI as the benchmark for inflation and a 1% annual expense ratio. In reality, all of these assumptions are quite likely on the low side.)

As you can see, there is a dramatic difference in outcomes over the long-term.

From 1871 to present the total nominal return was 9.07% versus just 6.86% on a “real” basis. While the percentages may not seem like much, over such a long period the ending value of the original $1000 investment was lower by an astounding $260 million dollars.

Importantly, as stated previously, and as I will discuss more in a moment, the return that investors receive from the financial markets is more dependent on the “WHEN” you begin investing.

2) I Can Beat/Outperform The Stock Market

No, you can’t and the data proves it.

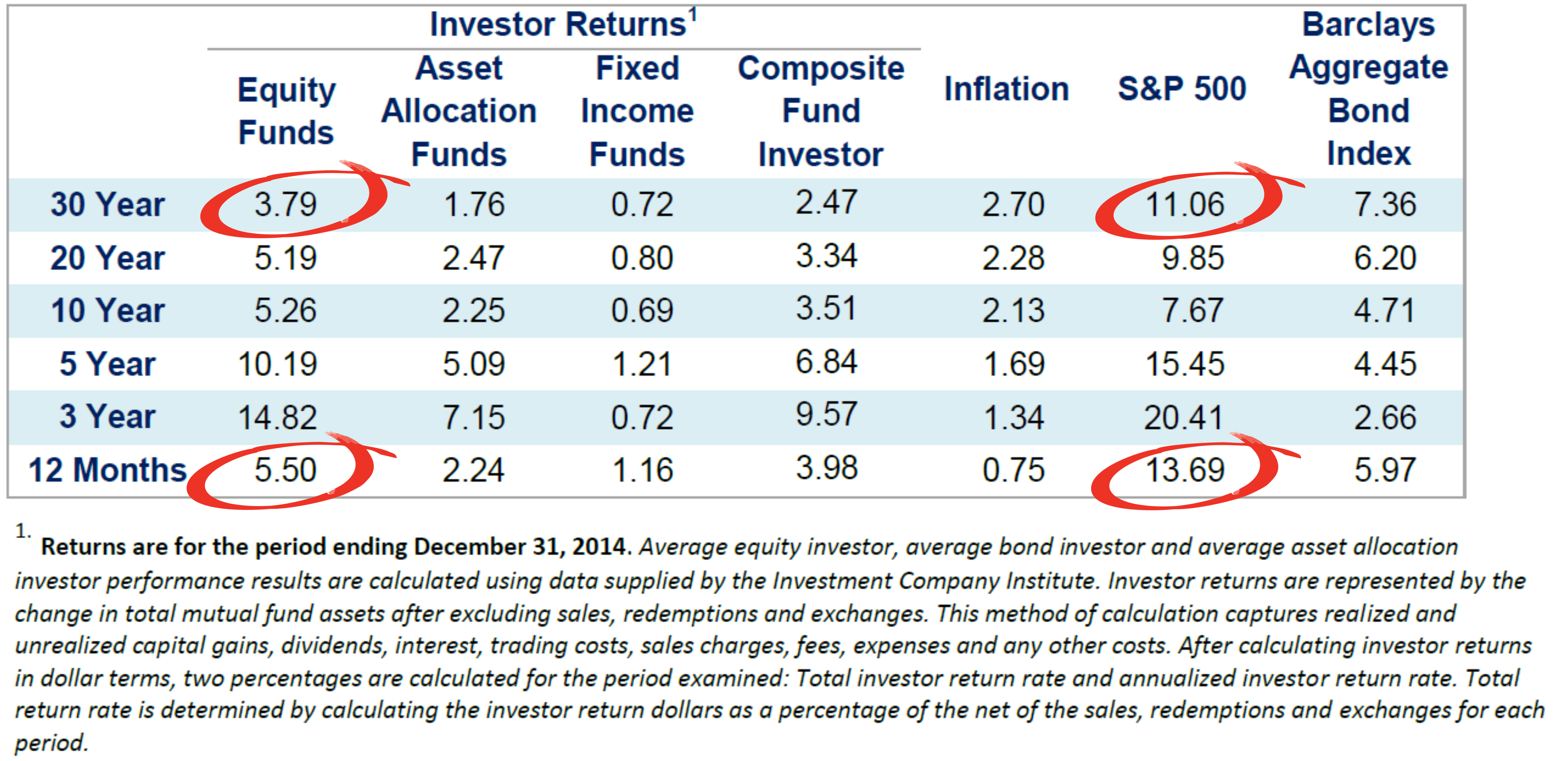

Dalbar recently released their 21st annual Quantitative Analysis Of Investor Behavior study which continues to show just how poorly investors perform relative to market benchmarks over time and the reasons for that under performance.

It is important to note that it is impossible for an investor to consistently “beat” an index over long periods of timedue to the impact of taxes, trading costs, and fees. Furthermore, there are internal dynamics of an index that affect long term performance which do not apply to an actual portfolio such as share repurchases, substitution, and replacement effects.

However, even the issues shown above do not fully account for the underperformance of investors over time. The key findings of the study show that:

- In 2014, the average equity mutual fund investor underperformed the S&P 500 by a wide margin of 8.19%.The broader market return was more than double the average equity mutual fund investor’s return. (13.69% vs. 5.50%).

- In 2014, the average fixed income mutual fund investor underperformed the Barclays Aggregate Bond Index by a margin of 4.81%. The broader bond market returned over five times that of the average fixed income mutual fund investor. (5.97% vs. 1.16%).

-

Retention rates are

- slightly higher than the previous year for equity funds and

- increased by almost 6-months for fixed income funds after dropping by almost a year in 2013.

- In 2014, the 20-year annualized S&P return was 9.85% while the 20-year annualized return for the average equity mutual fund investor was only 5.19%, a gap of 4.66%.

- In 8 out of 12 months, investors guessed right about the market direction the following month. Despite “guessing right” 67% of the time in 2014, the average mutual fund investor was not able to come close to beating the marketbased on the actual volume of buying and selling at the right times.

Most importantly, despite what Wall Street and advisors want you to believe, 50% of the shortfall was directly attributable to psychology – both theirs and yours. The other 50% came down to lack of capital to invest.

So, the next time you hear the mainstream media chastise investors for not beating some random benchmark index, just realize they didn’t either.

3) Your Financial Plan Says You Will Be Just Fine

One the biggest mistakes that investors make are in the planning assumptions for their retirement. As I discussed previously:

“There is a massive difference between compounded returns and real returns as shown. The assumption is that an investment is made in 1965 at the age of 20. In 2000, the individual is now 55 and just 10 years from retirement. The S&P index is actual through 2014 and then projected through age 100 using historical volatility and market cycles as a precedent for future returns.”

“While the historical AVERAGE return is 7% for both series, the shortfall between ‘compounded’ returns and ‘actual’ returns is significant. That deficit is compounded further when you begin to add in the impact of fees, taxes and inflation over the given time frame.

The single biggest mistake made in financial planning is NOT to include variable rates of return in your planning process.”

So, look at your financial plan projections. If they are a smooth curve upwards, you are going to be very disappointed.

4) If You’re Not In, You’re Missing Out

It is often stated that you should remain invested in the markets at all times because there has NEVER been a 10-year period that has produced negative returns for investors. That is simply not true.

Okay, but over 20-years investors have never lost money, right? Not really.

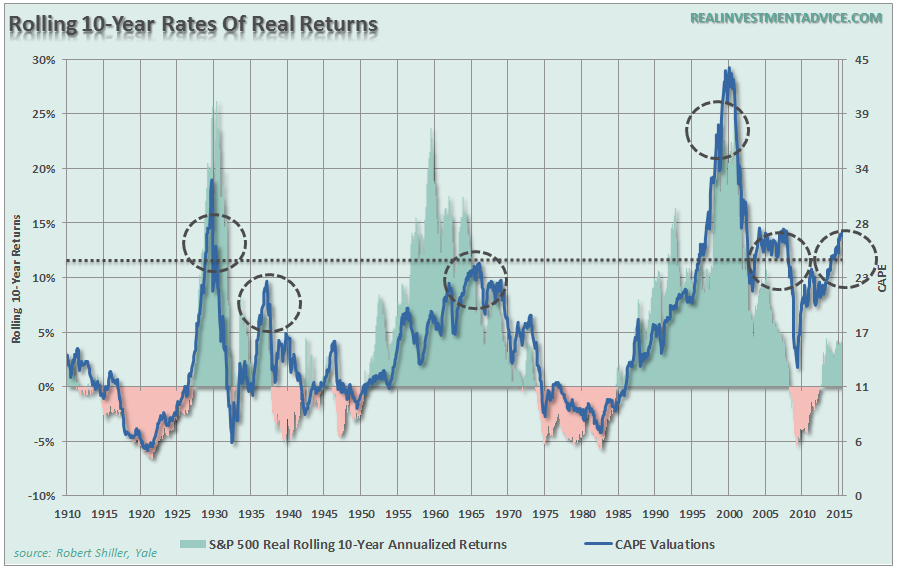

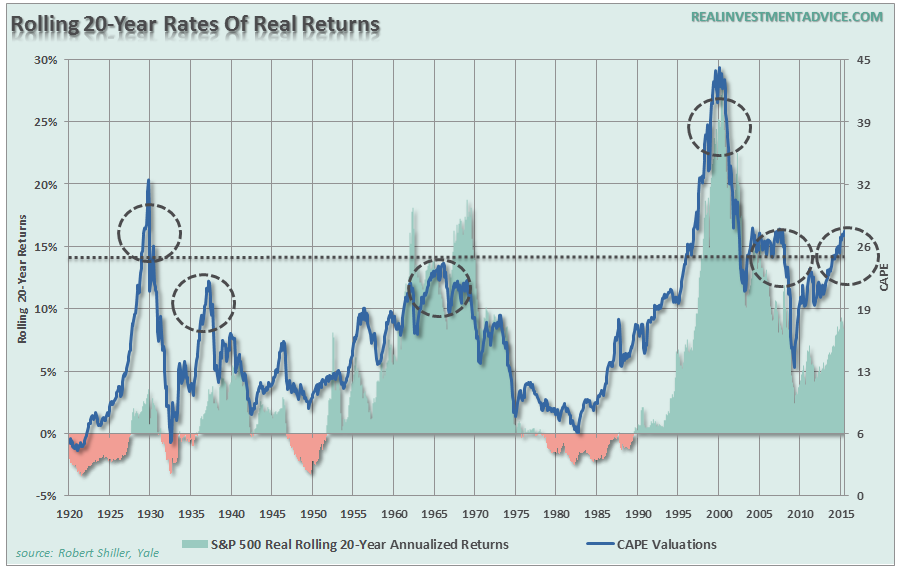

There are two important points to take away from the data. First, is that there are several periods throughout history where market returns were not only low, but negative. Secondly, the periods of low returns follow periods of excessive market valuations.

In other words, it is vital to understand the “WHEN” you begin investing that affects your eventual outcome.

The chart below compares Shiller’s 10-year CAPE to 20-year actual forward returns from the S&P 500.

From current levels history suggests returns to investors over the next 20-years will likely be lower than higher. We can also prove this mathematically as well as shown.

From current levels history suggests returns to investors over the next 20-years will likely be lower than higher. We can also prove this mathematically as well as shown.

Capital gains from markets are primarily a function of market capitalization, nominal economic growth plus the dividend yield. Using John Hussman’s formula we can mathematically calculate returns over the next 10-year periodas follows:

(1+nominal GDP growth)*(normal market cap to GDP ratio / actual market cap to GDP ratio)^(1/10)-1

Therefore, IF we assume that GDP could maintain 4% annualized growth in the future, with no recessions, AND IF current market cap/GDP stays flat at 1.25, AND IF the current dividend yield of roughly 2% remains, we get forward returns of:

(1.04)*(.8/1.25)^(1/10)-1+.02 = 1.5%

Regardless, there are a “whole lotta ifs” in that assumption. More importantly, if we assume that inflation remains stagnant at 2%, as the Fed hopes, this would mean a real rate of return of -0.5%. This is certainly not what investors are hoping for.

5) You Can’t Time The Market – Just Buy And Hold

There are no great investors of our time that “buy and hold” investments. Even the great Warren Buffett occasionally sells investments. Real investors buy when they see value, and sell when value no longer exists.

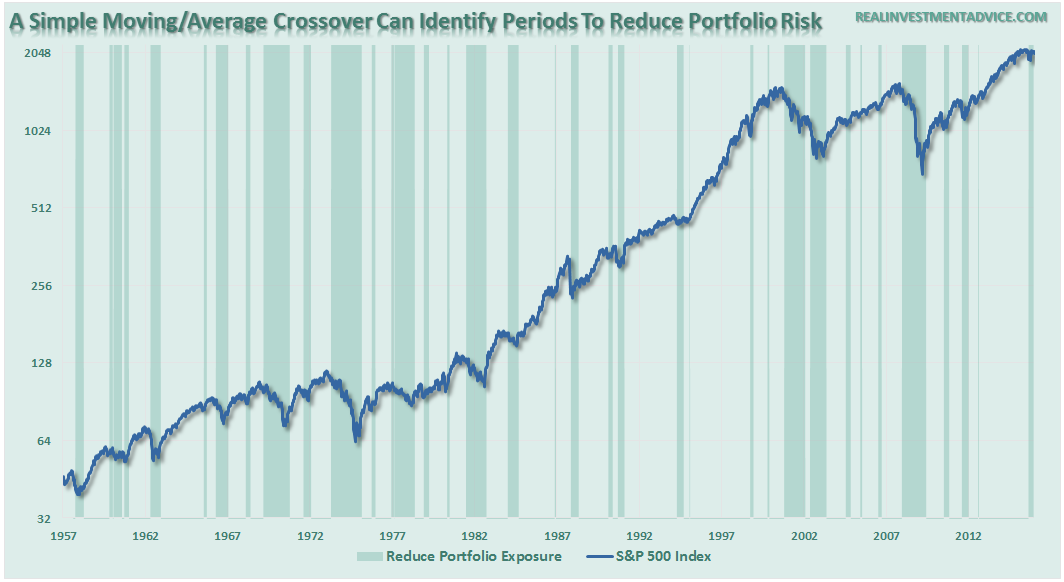

While there are many sophisticated methods of handling risk within a portfolio, even using a basic method of price analysis, such as a moving average crossover, can be a valuable tool over the long term holding periods. Will such a method ALWAYS be right? Absolutely not. However, will such a method keep you from losing large amounts of capital? Absolutely.

The chart below shows a simple moving average crossover study. The actual moving averages used are not relevant, but what is clear is that using a basic form of price movement analysis can provide a useful identification of periods when portfolio risk should be REDUCED.

Importantly, I did not say risk should be eliminated; just reduced.

Again, I am not implying, suggesting or stating that such signals mean going 100% to cash. What I am suggesting is that when “sell signals” are given that is the time when individuals should perform some basic portfolio risk management such as:

- Trim back winning positions to original portfolio weights: Investment Rule: Let Winners Run

- Sell positions that simply are not working (if the position was not working in a rising market, it likely won’t in a declining market.) Investment Rule: Cut Losers Short

- Hold the cash raised from these activities until the next buying opportunity occurs. Investment Rule: Buy Low

The reason that portfolio risk management is so crucial is that it is not “missing the 10-best days” that is important; it is “missing the 10-worst days.” The chart below shows the comparison of $100,000 invested in the S&P 500 Index (log scale base 2) and the return when adjusted for missing the 10 best and worst days.

Clearly, avoiding major drawdowns in the market is key to long-term investment success. If I am not spending the bulk of my time making up previous losses in my portfolio, I spend more time growing my invested dollars towards my long term goals.

Chasing A Unicorn

There are many half-truths perpetrated on individuals by Wall Street to sell product, gain assets, etc. However, if individuals took a moment to think about it, the illogic of many of these arguments are readily apparent.

Chasing an arbitrary index that is 100% invested in the equity market requires you to take on far more risk that you realize. Two massive bear markets over the last decade have left many individuals further away from retirement than they ever imagined. Furthermore, all investors lost something far more valuable than money – the TIME needed to achieve their goal.

To win the long-term investing game, your portfolio should be built around the things that matter most to you.

- Capital preservation

- A rate of return sufficient to keep pace with the rate of inflation.

- Expectations based on realistic objectives. (The market does not compound at 8%, 6% or 4% every year, losses matter)

- Higher rates of return require an exponential increase in the underlying risk profile. This tends to not work out well.

- You can replace lost capital – but you can’t replace lost time. Time is a precious commodity that you cannot afford to waste.

- Portfolios are time-frame specific. If you have a 5-years to retirement but build a portfolio with a 20-year time horizon (taking on more risk) the results will likely be disastrous.

The index is a mythical creature, like the Unicorn, and chasing it has historically led to disappointment. Investing is not a competition, and there are horrid consequences for treating it as such.

So, the next time a financial professional encourages you to just “buy and hold” for the long-term, maybe you should question just who’s “yacht” are you buying?

Lance Roberts

Lance Roberts is a Chief Portfolio Strategist/Economist for Clarity Financial. He is also the host of “The Lance Roberts Show” and Chief Editor of the “Real Investment Advice” website and author of “Real Investment Daily” blog and “Real Investment Report“.