Hope for the New Year: 3 Asset Classes for 2016

By Frank Holmes

CEO and Chief Investment Officer

U.S. Global Investors

Last week, I reflected back on 2015 by revisiting the 10 most popular posts of the year. Today I’d like to look ahead to 2016 by pinpointing three asset classes that I believe hold opportunities for investors.

Gold

Going forward, gold prices will largely be affected by U.S. monetary policy. The Federal Reserve began its interest rate-normalization process with a small but significant 0.25 percent increase, and unless the Fed has reason to mark time or reverse course in 2016, rates should continue to rise steadily.

This will bump up not just the U.S. dollar—which historically shares an inverse relationship with gold, since it’s priced in dollars—but also real interest rates. As I’ve discussed many times before, real rates have a huge effect on the yellow metal.

Real interest rates are what you get when you deduct the rate of inflation from the 10-year Treasury yield. For example, if Treasury yields were at 2 percent and inflation was also at 2 percent, you wouldn’t really be earning anything. But if inflation was at 3 percent, you’d see negative real rates.

When gold hit its all-time high of $1,900 per ounce in August 2011, real interest rates were sitting at negative 3 percent. In other words, if you bought the 10-year, you essentially lost 3 percent a year on your “safe” Treasury investment. Since gold doesn’t cost anything to hold, it became more attractive, and the metal’s price soared.

But today, the U.S. has virtually no inflation—the November reading was 0.5 percent—so real rates are running at less than 2 percent.

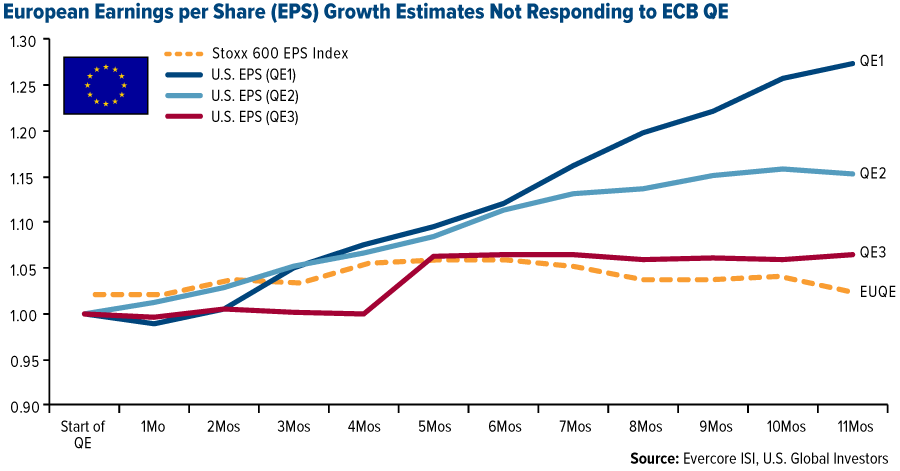

Across the Atlantic, many investors are now realizing that Europe’s quantitative easing (QE) programs have failed to improve market performance in any substantial way. Earnings per share growth estimates in the European stock market have not budged. The lack of real growth in this market is a compelling argument for global investors to own gold for the long term.

Low interest rates, higher taxes and tariffs and more labyrinthine global regulations since 2011 are all contributing to the global slowdown. Neither QE3 in Europe nor QE3 in the U.S. has led to a marked improvement in growth. What markets need now to ignite growth are fewer taxes, tariffs and regulations and smarter fiscal policies.

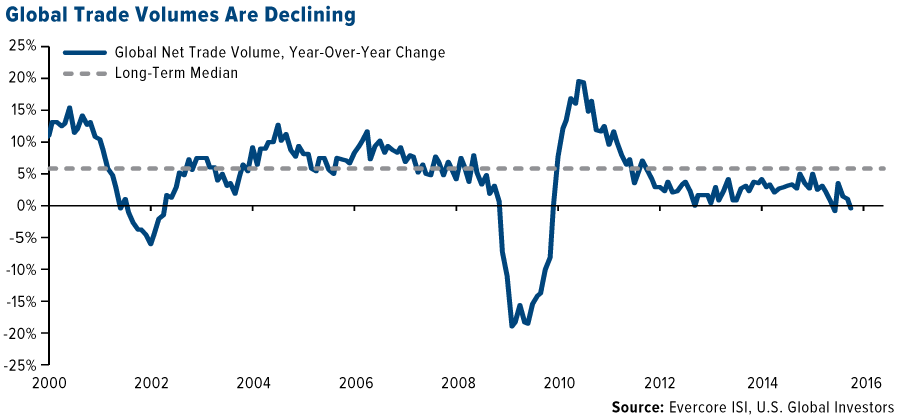

The chart below, courtesy of Evercore ISI, helps to illustrate some of the challenges we’ve faced in 2015 in terms of the investments we manage. Growth remains scarce globally. M2 money supply in the U.S. also looks dim.

Looking forward, we’re hopeful that these two indicators—global trade volume and money supply—will turn up. Both are necessary to improve commodity and emerging market investments.

On the upside, gold demand in China remains strong. It’s important to remember that more than 90 percent of demand comes from outside the U.S., in China and India in particular. Precious metals commentator Lawrie Williams reports that Chinese gold withdrawals from the Shanghai Gold Exchange (SGE) crossed above 51 tonnes for the week ended December 18.

Already Chinese demand is higher than the previous annual record set in 2013, and if total withdrawals for 2015 climb above 2,500 tonnes, as Lawrie expects, this will be “equivalent to around 80 percent of total global annual new mined gold production.” We expect demand to rise even more as we approach the Chinese New Year—historically a key driver for gold’s Love Trade—which falls on February 8 in 2016.

Oil

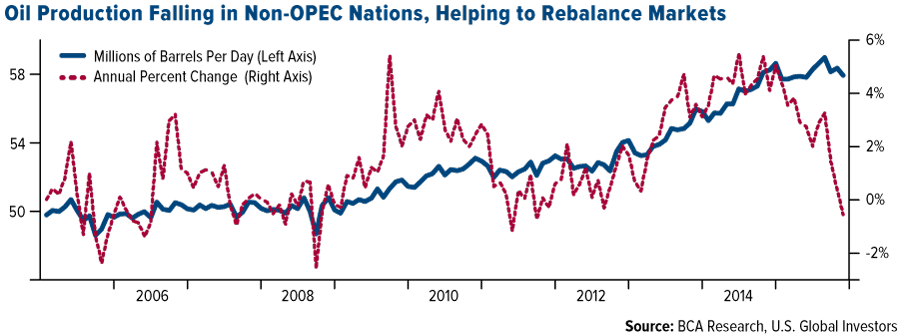

BCA Research believes oil markets will rebalance in 2016, not because of a price collapse but because production will continue to slide and consumption, grow. Most of these adjustments are being made in nonmembers of the Organization of Petroleum Exporting Countries (OPEC). In the U.S. alone, over 600,000 barrels per day have fallen out of the market as the rig count falls.

Russia, however, is unwilling to cut its production in a bid to compete with OPEC. In November, the country hit a post-Soviet record of 10.8 million barrels produced per day. And even more oil is expected to come out of Iran in 2016 once international sanctions are lifted.

For these reasons, Moody’s recently trimmed its 2016 oil forecast. West Texas Intermediate (WTI) crude will average $40 per barrel, down from $48, according to the ratings agency. The projection for Brent was slashed even more significantly, from $53 to $43.

To put this in perspective, oil averaged $55 per barrel in 2015, compared to $85 in 2014.

In all likelihood, then, oil prices probably need to remain lower for longer in order to rebalance the market.

Airlines

Last month I shared the latest report from the International Air Transport Association (IATA), which states that global airlines will post record net profits of $33 billion for 2015. Because fuel prices are expected to stay low, airlines could very well hit another record at the end of 2016—$36.3 billion, according to the IATA.

Savings from lower fuel prices are partially to thank for these profits. Goldman Sachs points out, however, that we shouldn’t expect prices to fall at the same magnitude as they did in 2014 and 2015.

As a result of lower fuel prices and airlines’ improved discipline in capacity growth and capex spending, the group is poised to see increased operating margins in the coming years, according to Morgan Stanley.

In short, operating margin tells you what percentage of every dollar made the company keeps as revenue before taxes. The higher the operating margin, the better off the company is.

Ancillary revenue is also contributing more to airlines’ bottom line. Such revenue comes from non-ticket fees such as baggage and handling, cancellations, seat upgrades, meals and the like. According to ancillary revenue expert IdeaWorks, the total global amount generated from these fees is estimated to rise to a whopping $59.2 billion in 2015, up from $49.9 billion in 2014. That accounts for 7.8 percent of global airline revenue, an improvement from the 6.7 percent in 2014.

The increased revenue is helping to boost domestic airlines’ free cash flow. Bank of America Merrill Lynch has forecast that airlines will see the highest free cash flow in years, one of the best indications of a company’s ability to generate cash.

Managing Expectations in 2016, a Presidential Election Year

As we reflect back on 2015, it’s important to remember that everything happens in cycles—from the presidential election cycle to the gold seasonality cycle and even to weather patterns. Similarly, every asset class has its own DNA of volatility.

By recognizing these cycles and patterns, it becomes easier to manage your expectations and become more proactive than reactive. With that in mind, I’d like to focus specifically on opportunities and threats for the coming year.

1. 2016 is the fourth year of the presidential election cycle. According to research by market historian Yale Hirsh—and later his son Jeffrey—markets have tended to perform well in presidential election years. Between 1833 and 2012, the Dow Jones Industrial Average rose on average 5.8 percent during election years.

2. After a flat year, 2015 being one of them, the market has historically been up, as you can see in the table below:

| Following Year | ||

|---|---|---|

| Flat Year | S&P | Earnings |

| 1970 | +11% | +25% |

| 1978 | +12% | +6% |

| 1984 | +26% | +5% |

| 1987 | +12% | +16% |

| 1994 | +34% | +11% |

| 2005 | +14% | +9% |

| 2011 | +13% | +9% |

| Average | +17% | +12% |

| Source: Evercore ISI, U.S. Global Investors | ||

3. The Trans-Pacific Partnership (TPP) should help spark a light under global trade by eliminating thousands of tariffs and other barriers that currently stand in the way of foreign investment.

4. China, an essential market for commodities demand growth, continues to stimulate its economy with low interest rates and financial stimulus.

5. As for potential threats, the biggest one in the new year continues to be global terrorism. Aside from the fact that it has increasingly made society feel less safe, terrorism reportedly cost the world $53 billion in 2014 alone, according to the latest data from the Institute for Economics and Peace. That’s the highest amount since 9/11.

I want to wish all of our readers and shareholders the very best in 2016!

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 0.72 percent. The S&P 500 Stock Index fell 0.83 percent, while the Nasdaq Composite fell 0.81 percent. The Russell 2000 small capitalization index lost 1.63 percent this week.

- The Hang Seng Composite lost 0.89 percent this week; while Taiwan was up 0.16 percent and the KOSPI fell 1.47 percent.

- The 10-year Treasury bond yield rose 2 basis points to 2.27 percent.

Domestic Equity Market

Strengths

- Netflix was the best performing stock in the S&P 500 Index, returning 134.4 percent this year. In the first four months of 2015 the company’s shares rose 60 percent, appreciating on growth in its subscribers and an ongoing plan to expand globally.

- The best performing sector this year was consumer discretionary as weak energy costs allowed shoppers to spend more and pay less at the pump.

- The unemployment rate in the United States was recorded at 5 percent in November, the same as previous the month and the lowest in more than seven years. The unemployment rate in U.S. averaged 5.83 percent from 1948 until 2015, reaching an all-time high of 10.8 percent in November of 1982, and a record low of 2.5 percent in May of 1953.

Weaknesses

- Chesapeake Energy was the worst performing stock in the S&P 500 Index, returning negative 77 percent this year. 2015 was the worst year for Chesapeake Energy since 1998. Halting dividend payouts, slashing drilling budgets, and cutting one of every six employees failed to rescue the energy explorer from the deepest gas-market rout in 16 years.

- The worst performing sector this year in the S&P 500 Index was the energy sector. The price of WTI crude oil declined by 30.58 percent over the past 12 months.

- Earnings growth has been weak in recent quarters. Earnings growth was negative for the S&P 500 Index in each of the last two earnings seasons, and likely won’t improve in the next quarter. The S&P 500 earnings are expected to be down 7.3 percent from the same period a year ago.

Opportunities

- Consumer confidence in December beat expectations as more Americans became optimistic about the current state of economy and the job market. The Conference Board’s Consumer Sentiment Index increased to 96.5 from a revised November reading of 92.6.

- The consumer discretionary sector may further benefit from weaker energy prices as oil and natural gas prices are reaching record lows. As the costs of energy and gas decline, consumers have extra money to spend on goods and services.

- Very low inventories of homes for sale are pushing home prices higher. Home values in October were 5.2 percent higher than in 2014, according to the S&P/Case-Shiller National Home Price Index. This is stronger than the 4.9 percent annual gain in September.

Threats

- Pending home sales, a measure of signed contracts, fell 0.9 percent compared to an upwardly revised October reading, according to the National Association of Realtors. Sales were 2.7 percent higher than in November 2014, but saw the smallest annual increase in over a year. November’s number was the third monthly decline in the past four months.

- The Chicago purchasing managers’ index (PMI) missed estimates for December, hitting 42.9 and down from 48.7 the previous month. A significant move in this regional survey is seen as having predictive value for the national index. Markit’s U.S. Manufacturing PMI will be released on Monday next week.

- BCA research recommends S&P Investment Banks & Brokerages to be cut to underweight. Domestic financial conditions are tightening while the corporate sector is struggling to generate profit growth

The Economy and Bond Market

Strengths

- Trading within this final, quiet and holiday-shortened week of 2015 saw yields on the U.S. two-year notes rise to new, 52-week highs as investors continue to digest the Federal Reserve’s recent rate hike, a sign of the Fed’s confidence in the strengthening U.S. economy.

- The S&P/Case-Shiller Composite 20 City Home Price Index continues to show appreciating U.S. home prices, rising 0.8 percent in October, while year-over-year prices came in at a steady 5.54 percent.

- Money supply in the eurozone continues to indicate the expansion of credit in the Euro-area economies. The annual growth rate of M3 in the eurozone came in at 5.1 percent this week.

Weaknesses

- Initial jobless claims rose this week to their highest levels since July. At 287,000, the actual number missed analysts’ collective expectations of 270,000.

- Pending home sales in the U.S. for November also missed analysts’ expectations, declining 0.9 percent month-over-month and falling short of surveys that anticipated a rise of 0.7 percent.

- Chicago PMI missed expectations—at 42.9, MNI’s Chicago Business Barometer came in much lower than anticipated, and fell to levels not seen since 2009. Expectations for December were 50.0.

Opportunities

- While lower oil prices undoubtedly weigh upon much of the energy sector, consumers enjoy much lower prices at the gas pump, and continued low prices mean more discretionary dollars in consumers’ pockets.

- The Conference Board’s Consumer Confidence number came in at 96.5, beating expectations of 93.5. This follows on the heels of positive numbers from the University of Michigan’s Consumer Sentiment Index last week.

- 2016 marks a U.S. presidential election year. From a seasonality standpoint, some investors view election years as historically strong ones for market performance. On the other hand, an election year could present headline risks.

Threats

- As investors look forward to 2016, the potential for policy errors within stimulative economies like Europe’s and China’s will be closely monitored. At the same time, and even as the U.S. Federal Reserve attempts to guide the U.S. economy out of the Great Recession, U.S. markets could be subjected to headline risks or policy scares as the presidential election cycle and primaries get under way.

- Global stimulus and devaluation in the face of competition and fears of deflation may elevate uncertainty and volatility. Other complicating factors like Euroscepticism, terrorism, and potential geopolitical differences may further complicate views on the FX markets.

- Rising rates, or the expectation of higher rates, may threaten bond prices.

Gold Market

For the trailing week, spot gold closed at $1,061.42, down $14.73 per ounce, or 1.37 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, fell 3.73 percent. Junior miners underperformed seniors for the week as the S&P/TSX Venture Index climbed only 1.69 percent. The U.S. Trade-Weighted Dollar Index rose 0.65 percent since last Friday.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Dec-31 | US Initial Jobless Claims | 270k | 287k | 267k |

| Jan-3 | Caixin China PMI Mfg | 0.6% | -- | 48.6 |

| Jan-4 | US CPI YoY | 0.6% | -- | 0.4% |

| Jan-4 | US ISM Manufacturing | 49.0 | -- | 48.6 |

| Jan-5 | US CPI Core YoY | 1.0% | -- | 0.9% |

| Jan-6 | US ADP Employment Change | 198k | -- | 217k |

| Jan-6 | US Durable Goods Orders | -- | -- | 0.0% |

| Jan-7 | US Initial Jobless Claims | -- | -- | 287k |

Strengths

- The best-performing precious metals as we close out 2015 were gold and silver with returns of minus 10.47 percent and minus 12.45 percent, respectively. The NYSE Arca Gold Miners Index was down 24.51 percent for the year.

- Klondex Mines, one of the few gold stocks to deliver positive returns each of the last three years, finished the year up 21.90 percent in U.S. dollar terms. A star performer over the last two years has been Northern Star, which was up 70.54 percent just over the trailing year. Another turnaround this year was led by Bob Vassie, the new CEO of St. Barbara Ltd., for a 1,111.70 percent gain. These kinds of outcomes don’t come randomly. The management teams at Klondex, led by CEO Paul Huet, CEO Bill Beament at Northern Star, and Bob Vassie at St. Barbara all have the expertise and skillset needed to execute for shareholders and to deliver positive outcomes.

- India’s silver import is set to post a new record this year, according to Business Insider. Total silver import for calendar year 2015 is estimated at 7,759 tonnes (on an annualized basis), which registers a rise of around 10 percent from 2014.

Weaknesses

- The worst-performing precious metals for 2015 were platinum and palladium with returns of minus 26.07 percent and minus 29.43 percent, respectively. The platinum mining stocks in Southern Africa were off on average by more than 70 percent for the year.

- The worst-performing gold mining stocks in larger capitalization names were Cia de Minas Buenaventura S.A.A. minus 55.23 percent, Yamana Gold minus 45.20 percent, Alamos Gold minus 45.18 percent, and Eldorado Gold minus 42.09 percent.

- The Bloomberg Commodity Spot Index has witnessed its worst performance since 2008, dropping 19 percent this year. A significant reason for the disappointing performance in commodities, reports Bloomberg, has been the strong U.S. dollar which is up 9.40 percent for 2015 against a group of other global currencies. Many of the gold stocks are now trading below the levels they plummeted to in 2008.

Opportunities

- Some big names still have big holdings in gold. The Moltly Fool points out that John Paulson and his hedge fund group Paulson & Co. own about $900 million worth of shares of the SPDR Gold Trust. Another investor showing confidence in gold is Ray Dalio, founder of Bridgewater Associates, who has said, “If you don’t own gold, you know neither history nor economics.” Paulson and Dalio seem to be demonstrating gold’s use as a hedge against uncertainty in fragile markets.

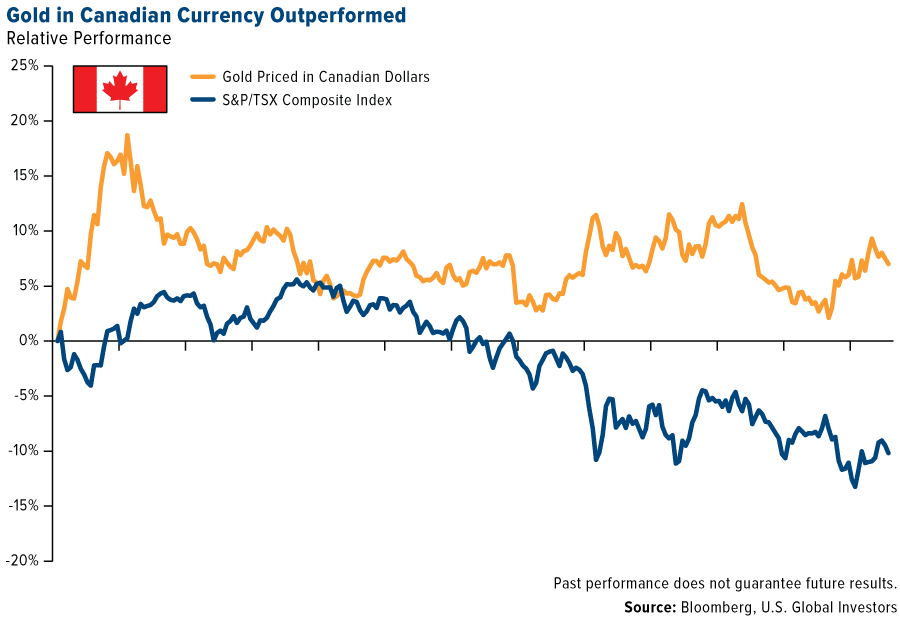

- Gold has been falling hard since 2013, being pulled down right alongside the rest of the commodities complex. However, as John Rubino points out in a Seeking Alpha article, this is only in U.S. dollar terms. As seen in the chart below, gold is behaving just fine in Canadian dollar terms, up 7 percent over the past year and which helped offset the negative returns of Canadian stock market which fell 11 percent. Rubino writes, “Protection from currency trouble is why people own it (gold), and why in the vast majority of places its owners are very happy.”

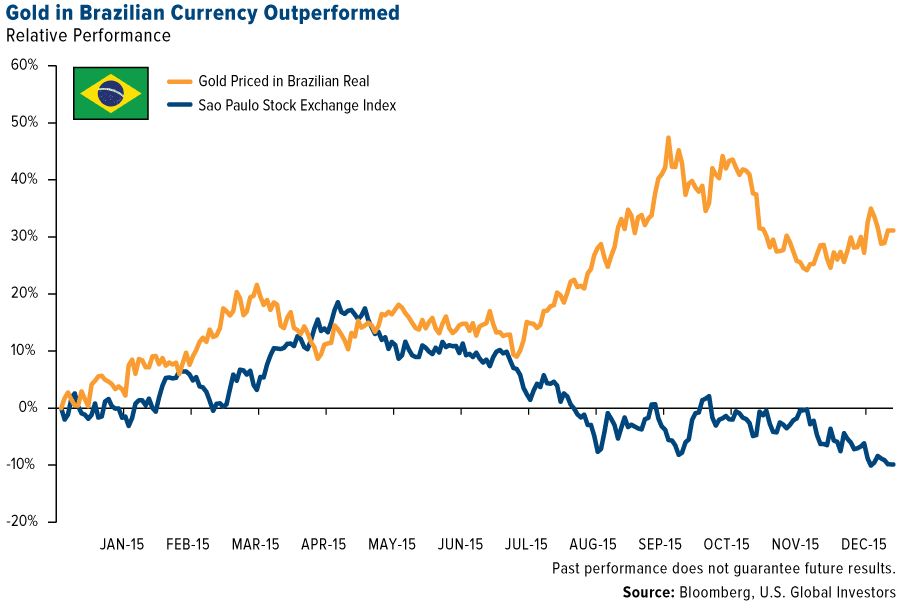

- The same holds true for many other weak domestic currencies. Gold priced in Brazilian real surged 31 percent while the Brazil’s top 100 stocks lost 10 percent as shown in the chart below. While the U.S. dollar strengthened with the much-hyped Fed hike in interest rates, history shows that the dollar typically does not get stronger after the first rate hike, so for U.S. investors, now could be an opportune time to rebalance your portfolio of assets.

Threats

- Gold bears are claiming that the major banks haven’t been buying gold. Zero Hedge reports that Goldman Sachs expects the price of gold to fall to $1,000 per ounce, while others, including BNP Paribas and ABN Amro expect gold to fall even lower. Zero Hedge points out that when popular sentiment has shifted away from gold.

- According to a Bloomberg report, the U.S. dollar is headed for its biggest monthly loss since August (against the yen) and since April (versus the euro) following the Federal Reserve’s decision to hike interest rates for the first time since 2006. At the same time, the Surprise Index which is a Citigroup measurement of how U.S. economic indicators compare with forecasts, heads for a second monthly decline.

- A group of 10 Wall Street strategists announced their forecasts for 2016, as published on Zero Hedge this week. Five strategists say to avoid materials, four strategists warn against energy, while nearly all were bullish on financials and technology. The forecasts, originally sourced in Barron’s, were brought to light during a Bloomberg TV interview with Marc Faber earlier in the week. Faber stated that the U.S. is headed into recession and rather than be bullish on U.S. equities (as a majority of the strategists were), to instead “be realistic.”

![[thumb]](/images/content_image/data/05/059f610c2ef22a1f3e67949cf86c0b65.jpg)

December 28, 2015Christmas Edition: 2015 in Review |

![[thumb]](/images/content_image/data/85/85010d5f5c4cd080d15f747be64066a2.jpg)

December 21, 2015The Fed Awakens: A New Hike |

![[thumb]](/images/content_image/data/33/33540ab5f74f33c84fa4c814ac386eef.jpg)

December 16, 2015Chinese Railway Stays On Track |

Energy and Natural Resources Market

Strengths

- Metals at the London Metal’s Exchange are poised for their first monthly gain since last April as investors cite minor improvements in Chinese data. Prices have advanced amid speculation that Chinese demand has begun to stabilize as smelters scale back production to stem loses.

- Vestas, Gamesa and Nordex, Europe’s three publicly-traded wind-turbine makers, all doubled in value in 2015 after record industry installations for the year. According to a Bloomberg report these companies have benefitted from a 30 percent rise in wind power installations globally in 2015. The growth trend is expected to continue, boosted by the Paris Climate Change Summit and the extension of incentives for renewable power by the U.S. Congress.

- The best-performing stock in the broader natural resource space this week was Parsley Energy. The oil producer, with operations in the Permian Basin, rose 5 percent on Thursday as oversold E&Ps rallied into the end of the year aided by a last minute rebound in crude oil prices.

Weaknesses

- Oil will post its second consecutive annual decline, the first back-to-back loss since 1998, as record levels of U.S. production exacerbate a global supply glut. U.S. inventories rose by more than 100 million barrels for the year, a greater than 25 percent increase. The expected supply response has not materialized, with OPEC effectively abandoning its production target to accommodate increasing production out of Iran, pointing to a longer wait before a global supply and demand rebalance occurs.

- The rally in natural gas prices snapped this Wednesday on new forecasts for warmer U.S. weather, sliding nearly 7 percent after prices had reached a six-week high on inventory drawdowns.

- The worst performing stock for the week in the S&P Global Natural Resources Index was Freeport McMoran. The company announced that its Chairman and Co-founder James Moffett will resign his board seat and leave the company, a result that many have attributed to Carl Icahn’s activist plan to cut costs at the executive level.

Opportunities

- The seasonality of commodity investing suggests that such investors will have the wind at their sail for the next four months. According to a study published by VTB Capital, over the past 20 years the Bloomberg Commodity Index has posted strong rallies in the first four months of the year, as demonstrated by the chart above. The report goes on to suggest that despite the ongoing negative investor sentiment toward the sector, there is reason to believe the seasonal pattern will play again in 2016.

- $10 trillion is the level of investment needed by 2040 to supply the oil and gas market, this according to OPEC’s World Oil Outlook for 2015. OPEC expects global oil demand to reach 110 million barrels per day in 2040, a volume that current fields could not come even close to supplying. As a result, the organization believes investments of $10 trillion will be necessary to ensure adequate infrastructure and supply.

- Glencore’s John Mack is still bullish on China and its appetite for commodities. In an interview discussing the company’s financial expectations, Mack, a legendary New York broker, admitted Chinese demand has not lived up to expectations in recent years, but stressed that China’s growth engine is still powerful enough to drive another wave of demand for raw materials in the long term.

Threats

- Coal’s favor among investors and regulators continues to drop as China unveiled legislation that will introduce a three year moratorium for new coal mine approvals. With the measure, the government aims to curtail production capacity and reinforce its commitment to shift away to cleaner fuels and cut pollution in major cities.

- Iron ore prices may dip into the $20 range in 2016 before rallying to end the year higher, according to a recent report by Capital Economics. The report suggests prices will drop initially as more low cost supplies help majors expand their market share. Following this initial response, higher cost production will be cut aiding a price rebound into year end.

- Crop prices head for a third straight annual loss as abundant supplies flood the market. Corn dropped nearly 10 percent for the year, while soybeans dropped 15 percent. Notwithstanding this year’s drops, the U.S. Department of Agriculture expects global inventories of both commodities to climb in the mid-single digits in 2016.

China Region

Strengths

- Chinese A-Shares was the best performing market in Asia this year, despite tremendous volatility during the year driven by waxes and wanes of leveraged trading and unprecedented government intervention. The Shanghai Composite Index gained 11.15 percent in 2015.

- Health care was the best performing sector in Asia this year, as companies with higher growth visibility associated with secular demographic trends were better received by investors in a broad-based economic slowdown in Asia. The MSCI Asia Pacific ex Japan Healthcare Index retreated only 5.57 percent in 2015.

- The Hong Kong dollar was the best performing currency in Asia this year, remaining flat in 2015, thanks to the longstanding peg to the U.S. dollar in a year when the greenback is the only major currency that has appreciated.

Weaknesses

- Singapore was the worst performing market in Asia this year, driven by substantial declines of companies in the industrials sector (specifically those exposed to commodities and marine shipping businesses) in another year of slowdown in Chinese demand and global trade. The Straits Times Index lost 11.35 percent in 2015.

- Materials was the worst performing sector in Asia this year, led by a considerable decline from industrial metals to construction materials in response to an unambiguous slowdown in the Chinese fixed investment cycle, most particularly, its property sector. The MSCI Asia Pacific ex Japan Materials Index finished down 22.24 percent this week.

- The Malaysian ringgit was the worst performing currency in Asia this year, weakening by 18.54 percent in 2015, as the currency of the only net energy exporting country in Asia depreciated along with crude oil prices.

Opportunities

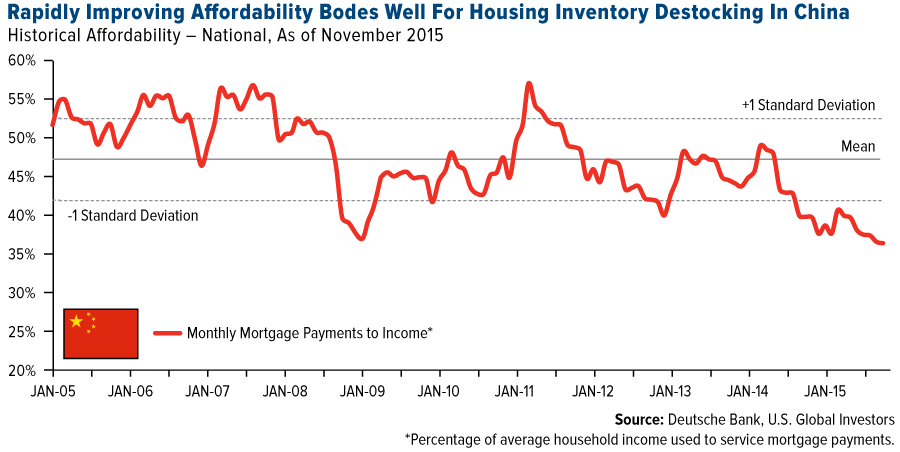

- Unbeknownst to the casual China watcher, national average affordability of new homes in the country (calculated as the percentage of average household income used to service monthly mortgage payments), has dropped significantly in the past year to an 11-year low. At 36.4 percent in November, this number is substantially below the historical average of 47.3 percent and even lower than in 2008, according to Deutshce Bank. This is due to falling interest rates, stagnant home prices in non-major cities, and resilient income growth. This should bode well for demand from housing upgraders in China, and facilitate further inventory destocking for quality residential property developers.

- South Korean equities should prove relatively resilient after the U.S. Federal Reserve raised interest rates, given the country’s robust fiscal status, recovering domestic demand, rising shareholder returns, and attractive valuation. Indeed, index-dominant technology exporters in Korea are likely to benefit from potential further strength in the U.S. dollar, and based on the last five years, according to Morgan Stanley, a weaker Korean won against the U.S. dollar tends to correlate with outperformance of Korean equities versus the rest of Asia, with a three month time lag.

- As global investor risk appetite retrenches after the Federal Reserve’s decision to hike interest rates and China’s decision to allow the renminbi to continue on a depreciation path, cash as the ultimate defensive asset class may once again outperform as volatility picks up in various asset classes around the world.

Threats

- Lingering uncertainties about Macau casinos’ business model against rising new gaming supply amid unabated demand pressure from slower Chinese economy, weaker Chinese currency, and lengthier anticorruption campaigns should continue to weigh on Macau casino stocks next year.

- Luxury goods companies listed in Hong Kong may continue to underperform next year, not only because China’s anticorruption campaign would remain a discouragement for conspicuous consumption, but also because luxury brands which underwent significant store expansion in recent years may have to resort to price cuts and store closures to adapt to today’s reality. This means profit margins for luxury brands are likely to deteriorate while valuations stay unattractive.

- The local economy of Hong Kong, which has synchronized monetary policy with the U.S. because of a pegged Hong Kong dollar, is likely to be more vulnerable than during the 2004-2006 Federal Reserve tightening cycle, given the over 200 percent private sector debt-to-GDP, a peaking property cycle, and a continuously slowing Chinese economy. Equities of Hong Kong real estate and retail-oriented sectors might bear the brunt of any negative impact from even a gradual pace of interest rate hikes.

Emerging Europe

Strengths

- Hungary was the best performing market this year, gaining 45.7 percent. The best performing company trading on the Budapest Stock Exchange was Budapest Electricity, a regional electricity distributor.

- The Czech koruna was the best relative performing currency in 2015 despite losing 8 percent against the U.S. dollar. The Czech Republic has been growing at 4.6 percent, the highest GDP among central emerging European countries. The central bank of the Czech Republic has kept its main interest rate at record low levels at 35 basis points.

- The health care sector was the best performing sector among eastern European markets this year.

Weaknesses

- Greece was the worst performing market this year, losing 26 percent. Greek banks were the biggest decliners on the Athens Stock Exchange, losing about 95 percent of their value on average.

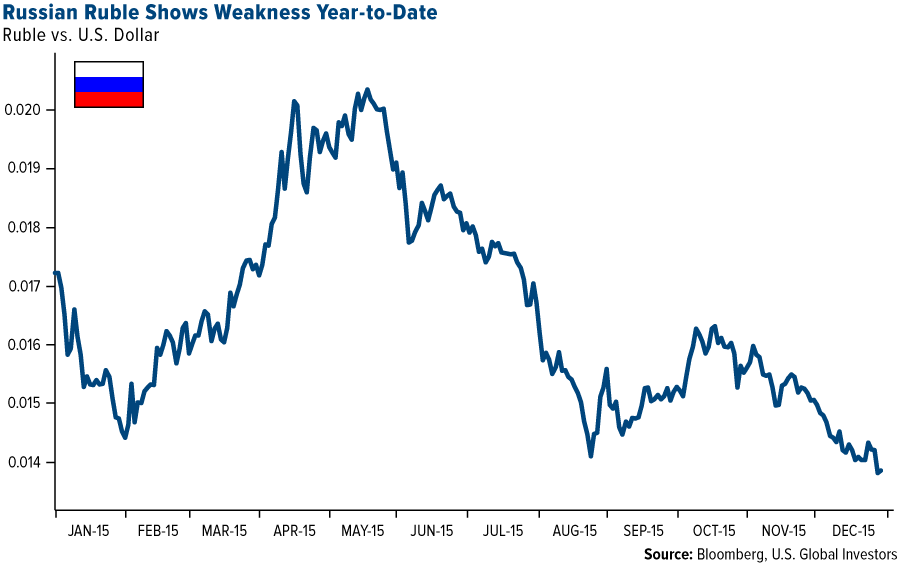

- The Russian ruble was the worst performing currency this year, losing 21 percent against the U.S. dollar. Since January, Russia’s Central Bank has spent about $70 billion defending the country’s currency, which has been hurt by Western sanctions over the Russia’s involvement in Ukraine, along with falling oil and natural gas prices.

- The utilities sector was the worst performing sector among eastern European markets this year.

Opportunities

- Lending to the eurozone’s private sector continued to expand in November. Loans to households increased by 1.4 percent in during the same month after growing 1.2 percent in October. Lending to non-financial corporations expanded by 0.9 percent in November following a 0.6 percent increase the month before.

- Poland’s ruling party softened a tax on its financial industry, helping to rally government bonds intra-week. Parliament’s public finance committee excluded banks’ roughly $41 billion in government-bond holdings from taxable assets. The levy will bring 4.4 billion zloty ($1.1 billion) per year to the budget, 400 million zloty less than earlier estimated.

- According to the International Monetary Fund (IMF), emerging markets grew at about 3.9 percent in 2015, about half the growth seen in 2010. The IMF expects emerging markets to rebound next year and growth at 4.5 percent.

Threats

- Nick Kounis, head of macro and financial markets research at a Dutch state-owned bank ABN Amro, told the Financial Times that the most important effect of the rate hike in the U.S. will be a weaker euro against the dollar (which should push import prices and help inflation). Overall, 18 of the 31 economists polled by the Financial Times said that the euro will be pushed down to the equivalent of $1 at some point in 2016.

- Vnesheconombank (VEB), a Russian state-owned bank used by Vladimir Putin to pay for “special projects,” like the Sochi Olympics, may need a rescue plan. Sanctions imposed in 2014 over the Ukraine crisis cut off VEB’s access to international financial markets, leaving it without a source of cheap funding and facing as much as $16 billion in foreign-currency debt as the ruble continues its plunge.

- Polish President Andrzej Duda signed a law that makes it harder for the constitutional court to overturn legislations. The bill increased the number of judges needed to pass a ruling and the majority required for the verdict. The Law and Justice party, Duda’s party, proposed the legislation after overturning the previous parliament’s appointment of judges to the tribunal, which the current panel deemed illegal. Critics say the law eliminates the court as a check on the power of the government, which controls both houses of the parliament after the October elections.

(c) US Global Investors