The IT Sector: Where Growth and Value Meet

The IT sector: where growth and value meet

By Dr. Brian Jacobsen, CFA, CFP®

Value and growth are held up as the two ends of a spectrum. On one side, you have companies that have low valuations, and—ostensibly—on the other end, you have companies with high valuations. The origin of this view comes from academic research showing that stocks with low price/earnings (P/E) ratios tend to outperform stocks with high P/E ratios (that is, there’s a value premium). That same research showed that smaller companies tended to outperform larger companies (that is, there’s a small-cap premium).

This is the genesis of that all too familiar style box many investors have seen where investments are classified as value/growth and small/mid/large. Personally, I think graphically depicting the investment universe as a fill-in-the-box chart is misleading. There are myriad ways to measure value. For example, growth stocks can be highly correlated with value stocks, meaning their corresponding style boxes may give you a false sense of diversification. Moreover, what’s large in one industry might be small in another. Plus, if people actually took the aforementioned academic research seriously, everyone would pile into small-cap value stocks rather than use the style boxes to build asset allocations.

Instead of thinking of value and growth investing as polar opposites, think of them as complementary approaches to investing. A value manager who buys simply because valuations are low might get stuck in a value trap. A growth manager shouldn’t pay just any price for growth. What I find fascinating is when value managers and growth managers uncover similar opportunities, and the information technology (IT) sector is a great example of where this crossover occurs. IT is a place where growth and value meet.

There are many different index providers, and each has its own methodology of classifying stocks as being value or growth. Some indexes allow stocks to be both value and growth stocks; others make the two categories mutually exclusive. Some indexes look at price/book; others look at P/E or composite measures to delineate between value and growth. In this post, I’ll use the Russell 3000® Value Index and the Russell 3000® Growth Index for illustrative purposes.

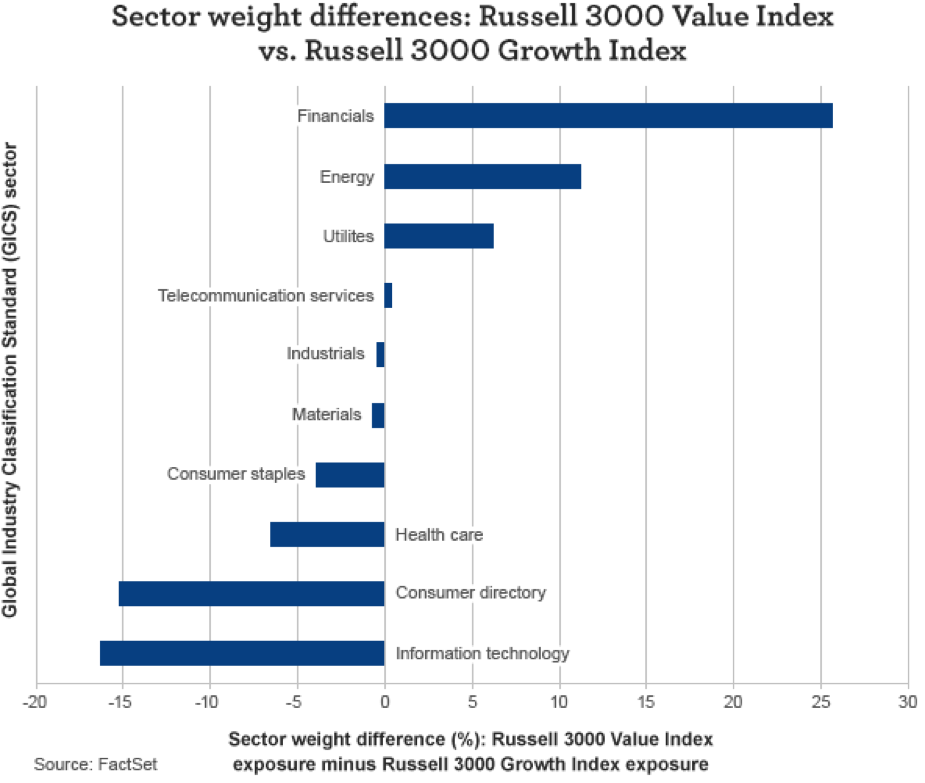

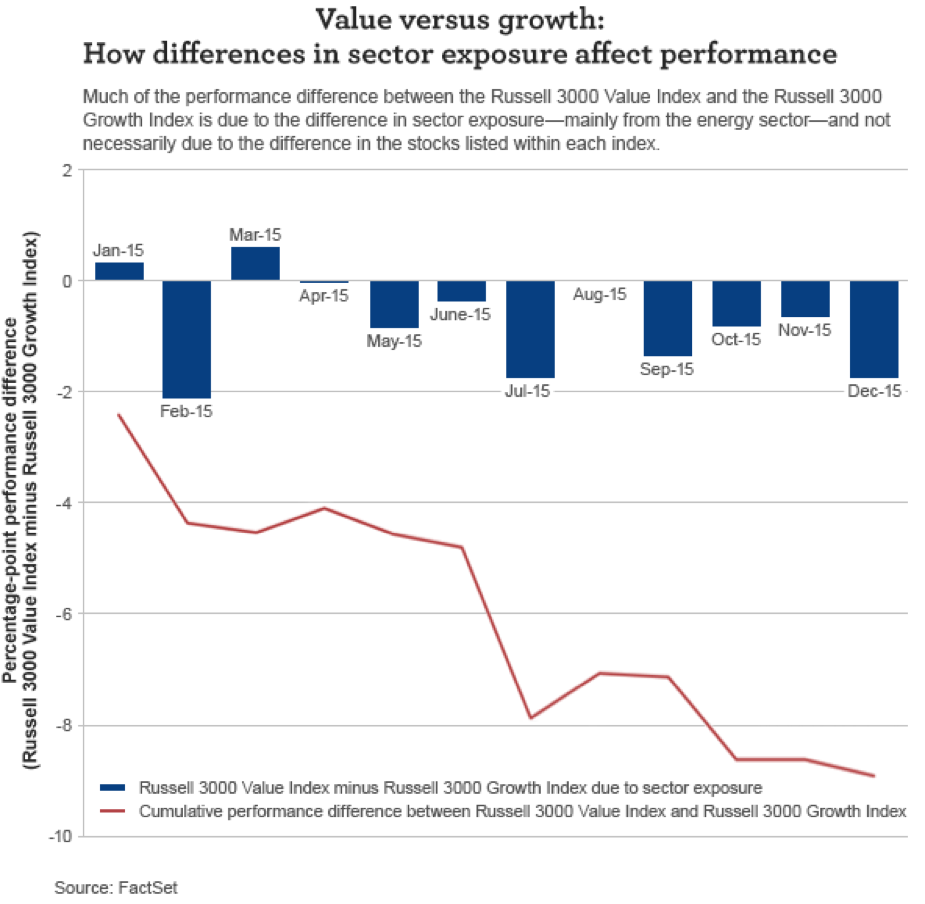

As of December 26, 2015, IT made up 11.56% of the Russell 3000 Value Index and, in contrast, 27.87% of the Russell 3000 Growth Index. Considering that growth stocks are allegedly supposed to grow into their valuations and the IT sector tends to be home to many companies where investors have high hopes of high earnings growth, it should make sense that IT is the biggest sector in the growth index and relatively better represented there. The differences in sector composition between the value and growth categories can explain a lot when it comes to value’s underperformance in 2015, as shown in the charts below.

The fact that energy comprises about 11.52% of the value index but only 2.55% of the growth index explains nearly two-thirds of the value category’s underperformance in 2015. For a portfolio manager in 2015, the sector allocation decision could have trumped any security selection decision. Freeing a manager from having to track a particular index’s sector allocation could have helped in avoiding the oil slick of 2015. Looking ahead to 2016, a value manager who overallocates to IT or a growth manager who employs a good valuation discipline could be poised to capitalize, as good valuations and attractive growth prospects meet in IT.

Why the IT sector is appealing for growth and value investors

|

Russell 3000 Value Index IT |

Russell 3000 Growth Index IT |

|

|

Market capitalization (median, millions of dollars) |

804.4 |

1,612.4 |

|

Dividend yield (%) |

2.0 |

1.0 |

|

P/E (weighted harmonic average) |

19.8 |

21.2 |

|

Price/cash flow |

8.9 |

15.1 |

|

Price/sales |

1.4 |

4.2 |

|

Historical 3-year EPS growth (%) |

6.1 |

19.3 |

|

Estimated 3- to 5-year EPS growth (%) |

5.5 |

16.7 |

|

Return on assets (%) |

7.7 |

11.5 |

|

Return on equity (%) |

19.1 |

22.6 |

|

Operating margin (%) |

21.4 |

24.0 |

|

Long-term debt/capital |

28.6 |

19.4 |

Source: FactSet

Within the IT sector, value’s underweight to internet software and services was costly in 2015 as was its underweight to technology hardware storage and peripherals. A manager who is mindful of, but not hindered by, an index’s recommended market-cap weightings can help avoid those costly mistakes.

Value managers might like companies with significant cash flows that are pivoting from declining business lines—such as physical data storage—to new blends of storage. Growth managers might look at the same companies and be attracted by secular catalysts, like increased demand for cloud computing and storage.

For a value manager, past missteps by IT company executives—perhaps due to fumbled acquisitions or challenging integrations—can create interesting turnaround stories. Growth managers can see the same company through the lens of having acquired significant intellectual property that can create a moat to protect or grow market share in network security.

Value managers can look at the market for electronic payments or data analytics and find the merger and acquisition landscape appealing. Identifying companies with strong balance sheets can help identify attractive targets or acquirers with the requisite balance-sheet flexibility to grow in leaps and bounds. A growth manager can see these companies as being positioned to launch a fledgling technology into a much bigger and broader universe.

Of course, a good sell discipline is important. While indexes only buy or sell once a year pretty mechanically, a good value manager can identify when balance sheets are becoming less flexible, cash flows are beginning to trickle, competitive advantages are eroding, or profit margins are being jeopardized. Good growth managers can identify when earnings growth is no longer robust or sustainable or when it’s no longer underappreciated by the market.

Again, instead of thinking of value and growth investing as polar opposites, think of them as complementary approaches to investing. In the IT area, there seems to be ample opportunity for good growth and a great price, which is the holy grail of investing.

Please visit our blog, AdvantageVoice, for additional viewpoints from Wells Fargo Asset Management’s investment strategists, portfolio managers, and practice management experts. You can also follow us on Twitter at @WFAssetMgmt for real-time updates. Are you an advisor or institutional investor? Check out our website for investment professionals.

The views expressed are as of 1-05-16 and are those of Dr. Brian Jacobsen, CFA, CFP®, and Wells Fargo Funds Management, LLC. The information and statistics in this report have been obtained from sources we believe to be reliable but are not guaranteed by us to be accurate or complete. Any and all earnings, projections, and estimates assume certain conditions and industry developments, which are subject to change. The opinions stated are those of the authors and are not intended to be used as investment advice. The views and any forward-looking statements are subject to change at any time in response to changing circumstances in the market and are not intended to predict or guarantee the future performance of any individual security, market sector or the markets generally, or any mutual fund. Wells Fargo Funds Management, LLC, disclaims any obligation to publicly update or revise any views expressed or forward-looking statements.

Wells Fargo Funds Management, LLC, a wholly owned subsidiary of Wells Fargo & Company, provides investment advisory and administrative services for Wells Fargo Funds. Other affiliates of Wells Fargo & Company provide subadvisory and other services for the funds. The funds are distributed by Wells Fargo Funds Distributor, LLC, Member FINRA, an affiliate of Wells Fargo & Company.

Not FDIC Insured • No Bank Guarantee • May Lose Value

© Wells Fargo Asset Management