Ahead of the Chinese New Year, China was very much a topic of discussion this week at Harvard Business School, where I attended and participated in a seminar for global CEOs.

From eight in the morning until midnight, 150 fellow chief executives and I studied and debated a number of case studies in leadership, marketing, finance and government reform. It was humbling to be in the company of so many world-class leaders and professors from all over the globe.

The weeklong event took place in Harvard’s Tata Hall, named after Ratan N. Tata, the Indian businessman and global investor. Today the snow fell hard in Boston, and I was lucky to fly out on American Airlines.

Among the distinguished speakers during the seminar was former Secretary of the Treasury and Harvard President Emeritus Larry Summers, whom I found both articulate and witty. Mr. Summers led us in a discussion of three countries presently undergoing reform—Colombia, Italy and China.

Colombia seeks tax reform and a peace resolution with FARC, the extremist rebel group, whereas Italy—led by Matteo Renzi, the country’s youngest-ever prime minister—strives to streamline bureaucracy and socialist unionism, which has constricted job creation. Its young people are currently struggling with a dismal 40 percent unemployment rate.

As for China, it has plans to deepen economic reforms to facilitate foreign investment. On countless occasions, the Asian giant has proven itself a dynamic nation, and today it continues to go through dramatic changes. No one can deny that challenges lie ahead, but huge opportunities still abound.

With this in mind, I’ve put together 10 figures to know as China enters a new year.

9th

As the ninth animal in China’s 12-zodiac cycle, the monkey is considered confident, curious and a great problem-solver. But 2016 is also the year of the Fire Monkey, which adds a layer of strength and resilience.

2.9 Billion

It’s been called the world’s largest annual human migration. “Chunyun,” or the Spring Festival, refers to the period around the Chinese New Year when people travel by plane, train and automobile to visit friends and family. Between January 21 and March 3, nearly 3 billion trips will be made, exceeding the number of Chinese citizens. Close to 55 million of these trips are expected to be made by air.

For the third straight year in 2015, China topped the list of international outbound travelers, with 120 million people heading abroad. Collectively, they spent $194 billion across the world.

6 Million

Not all destinations are within China’s borders, however. According to CTrip, a Chinese online travel service, Spring Festival tourists have booked a record 6 million outbound trips. As many as 100 different countries will be visited, with the farthest region being Antarctica.

180 Tonnes

A shaky stock market, depreciating renminbi and low global prices have spurred many Chinese consumers to turn to gold. Imports of the yellow metal are way up. Last month I wrote that 2015 was a blowout year, with China consuming more than 90 percent of the total annual global output of gold. In December, the country imported 180 tonnes from Switzerland alone, representing an 86 percent increase over December 2014. This news supports the trend we’ve been seeing of gold moving West to East.

The precious metal is currently trading at a three-month high.

49.4

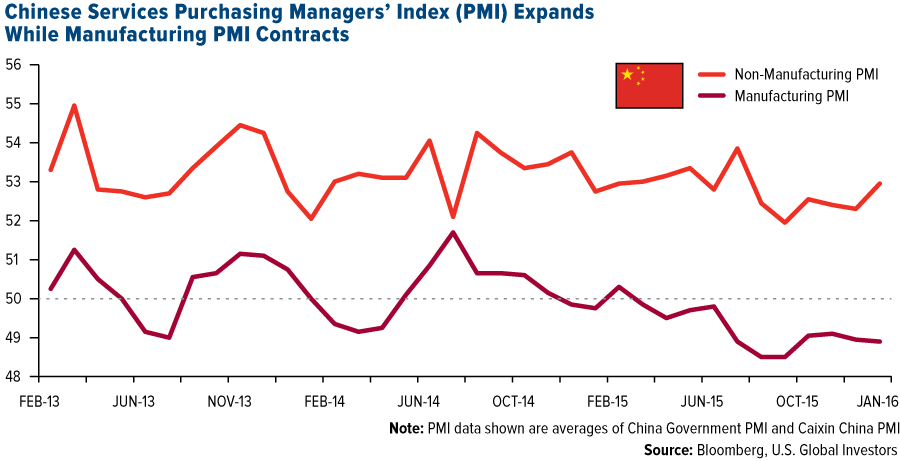

For the month of January, the Chinese government purchasing managers’ index (PMI) eased down from 49.7 in December to 49.4 in January, indicating further contraction in the country’s manufacturing sector. The reading remains below its three-month moving average. More easing from China’s central bank, not to mention liberalization of capital controls, could be forthcoming this year to stimulate growth and prop up commodities demand.

$6.5 Trillion

Although manufacturing has cooled, domestic consumption in China is following a staggering upward trajectory. In 2015, total retail sales touched a record, surpassing 30 trillion renminbi, or about $4.2 trillion. By 2020, sales are expected to climb to $6.5 trillion, representing 50 percent growth in as little as five years. This growth will “roughly equal a market 1.3 times the size of Germany or the United Kingdom,” according to the World Economic Forum.

109 Million

One of the main reasons for this surge in consumption is the staggering expansion of the country’s middle class. In October, Credit Suisse reported that, for the first time, the size of China’s middle class had exceeded that of America’s middle class, 109 million to 92 million. As incomes rise, so too does demand for durable and luxury goods, vehicles, air travel, energy and more.

But middle-income families aren’t the only ones growing in number. The World Economic Forum estimates that by 2020, upper-middle-income and affluent households will account for 30 percent of China’s urban households, up from only 7 percent in 2010.

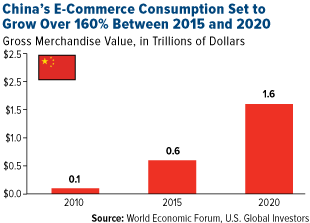

$1.6 Trillion

|

Consumption has also benefited from the emergence of e-commerce. Not only are younger Chinese citizens spending more than ever before, they’re doing it more frequently, as e-commerce allows for convenient around-the-clock spending. Such sales could grow from $0.6 trillion today to a massive $1.6 trillion by 2020.

Mobile payments will continue to play a larger role as well. Purchases made on a smartphone or tablet are expected to make up three quarters of all e-commerce sales by 2020.

24.6 Million

With a population of more than 1.3 billion, China is the world’s largest automobile market. The country certainly retained the title last year, selling 24.6 million vehicles, an increase of 4.7 percent over 2014. The U.S., by comparison, sold 17.2 million. According to China’s Ministry of Public Security, the Asian country added a staggering 33.74 million new drivers last year, which is good news for auto sales going forward.

6.5 Percent to 7 Percent

Many China bears point out that GDP growth in the Asian country has hit a snag. There’s no denying that its economy is in transition, evidenced by the government’s 2016 growth range of between 6.5 and 7 percent, a demotion from 2015’s target of 7 percent. But it’s important to acknowledge that China is still growing at an enviable rate.

Here’s one way to look at it, courtesy of Jim O’Neil, the commercial secretary to the British Treasury and the man who coined the acronym BRIC (Brazil, Russia, India, China). O’Neil calculates that even if China grows “only” 6.5 percent this year, the value is still equivalent to India growing 35 percent or the United Kingdom growing 22 percent.

For this reason and more, China remains a long-term growth story, and “there are many reasons to expect that in 10 or 15 years, China will be a greater, not a lesser, power than it is today,” says Stratfor Global Intelligence.

To all of my friends and readers both here and abroad, I wish you copious amounts of happiness, health and prosperity this Chinese New Year!

Index Summary

- The major market indices finished down this week. The Dow Jones Industrial Average lost 1.59 percent. The S&P 500 Stock Index fell 3.10 percent, while the Nasdaq Composite fell 5.44 percent. The Russell 2000 small capitalization index lost 4.81 percent this week.

- The Hang Seng Composite Index lost 1.94 percent this week; while Taiwan was down 0.22 percent and the KOSPI rose 0.30 percent.

- The 10-year Treasury bond yield rose 8 basis points to 1.84 percent.

Domestic Equity Market

Strengths

- The best performing sector this week was materials, increasing by 4.76 percent versus an overall decline of 3.27 percent for the S&P 500.

- Michael Kors was the best performing stock for the week, increasing 29.92 percent. The company reported better-than-expected results for the third quarter of its fiscal year 2016. For the quarter ended December 26, the luxury lifestyle brand reported total revenue of $1.40 billion, up from $1.31 billion a year earlier, while its profit advanced to $1.59 per share from $1.48 a year earlier. Moreover, the results exceeded analysts’ estimates by $0.13 in EPS and $40 million in revenue.

- This week ChemChina announced the largest foreign acquisition ever by a Chinese firm. The company agreed to acquire Swiss agrichemical firm Syngenta in a deal valued at $47.9 billion, including debt.

Weaknesses

- Consumer discretionary was the worst performing sector for the week, falling 5.43 percent versus an overall decline of 3.27 percent for the S&P 500.

- Marathon Petroleum was the worst performing stock for the week, falling 22.71 percent. The company’s shares fell in tandem with oil as overproduction continues to push oil prices down. Additionally, the company was downgraded by JPMorgan because of weak quarterly results from MPLX, the master limited partnership formed by Marathon Petroleum.

- Fifty-nine percent of S&P 500 companies have reported fourth-quarter 2015 earnings as of February 4, according to Lipper. The blended earnings growth estimate is - 4.2 percent. Stripping out the beleaguered energy sector, it is 2 percent. The fourth-quarter blended revenue growth estimate is -3.6 percent. Excluding the energy sector, the revenue growth estimate is 0.9 percent.

Opportunities

- Stronger-than-expected profit results have propelled the S&P leisure products group higher in recent trading sessions. Despite the sharp gains that have already accrued, stocks in the group could continue to see meaningful upside potential. The plunge in oil prices and rising income growth are pushing up spending on leisure products, while retail sales and toy and hobby stores are booming.

- With the broad market struggling to find a floor in the midst of a disappointing earnings season, it still pays to play defense. This week’s ISM releases reinforce that a defensive-over-cyclical portfolio bias is still warranted.

- Equities are attempting to find support. This year’s savage downward adjustment has created short-term oversold conditions and pushed sentiment gauges to depressed levels. These circumstances can often presage violent countertrend rallies.

Threats

- Only about 5 percent of S&P 500 stocks are above their 20-day moving average, a bearish signal for the market.

- Bank shares continue to get pounded as economic growth (and demand for credit) expectations shift lower and the yield curve flattens, reducing bank interest margin.

- Tightening credit conditions in U.S. corporate lending, along with contracting profits, threaten the liquidity and cash flow of companies, thereby putting buybacks and dividends at risk.

![[thumb]](/images/content_image/data/50/50d661c2ce1139af80afe015f5c0f17c.gif)

February 4, 2016What Could Trigger Gold To Take Off In 2016? |

![[thumb]](/images/content_image/data/02/0236942cdca76257f1916e7aef32c5a7.jpg)

February 4, 2016Ralph Aldis: This Is the Key to Building Wealth |

![[thumb]](/images/content_image/data/30/3023794da86cc0385b0b56dfff592456.jpg)

January 28, 2016Will Oil Markets Rebalance in 2016? |

The Economy and Bond Market

Strengths

- The unemployment rate dipped to 4.9 percent in January from 5.0 percent in December.

- Average hourly earnings advanced 0.5 percent in January, up from a flat reading in December.

- Annualized total sales of vehicles in the U.S. came out to 17.46 million in January, up from 17.22 million in December.

Weaknesses

- Nonfarm payrolls rose by 151,000 in January, which was a lower-than-expected number. Revisions to prior months also subtracted 30,000 jobs from last month's 292,000 total.

- The ISM non-manufacturing report missed consensus. While the weakness in manufacturing can be dismissed as being a relatively small portion of GDP, slower growth in services got everyone's attention. Business activity, exports and even employment growth weakened.

- China's official purchasing managers' index (PMI) fell for a sixth straight month to a three-year low. The January reading came in at 49.4, down from 49.7 in December.

Opportunities

- In spite of recent trends, median analyst forecasts are projecting a 50 percent increase in oil by the end of the year.

- According to a Bank of America Merrill Lynch survey, January saw a significant shift into cash by investors. This could prove to be a bullish sign for equities if economic turmoil fades.

- Slow interest rate tightening cycles have historically been positive for equity markets during the first year following an initial hike.

Threats

- The Treasury curve is now the flattest since early 2008, reflecting increasing concern about a slowdown in the economy, market volatility and tightening financial conditions.

- A more pronounced, dovish shift in Federal Reserve rhetoric amid weak economic data could fan further U.S. dollar weakness. Janet Yellen testifies to U.S. Congress mid-week.

- This week the European Union (EU) tabled a set of proposals designed to help avoid the UK voting to leave the EU. The plan was greeted in the UK press as “too little, too late.” A referendum on the matter has not yet been scheduled, but is widely expected to take place in June.

Gold Market

This week spot gold closed at $1,173.82, up $55.65 per ounce, or 4.98 percent. Gold stocks, as measured by the NYSE Arca Gold Miners Index, jumped 18.80 percent. Junior miners underperformed seniors for the week as the S&P/TSX Venture Index traded up just 1.73 percent. The U.S. Trade-Weighted Dollar Index slumped 2.65 percent for the week.

| Date | Event | Survey | Actual | Prior |

|---|---|---|---|---|

| Jan-31 | China Caixin China PMI Mfg | 48.1 | 48.4 | 48.2 |

| Feb-1 | U.S. ISM Manufacturing | 48.4 | 48.2 | 48.0 |

| Feb-3 | U.S. ADP Employment Change | 195k | 205k | 267k |

| Feb-4 | U.S. Initial Jobless Claims | 278k | 285k | 277k |

| Feb-4 | U.S. Durable Goods Orders | -4.5% | -5.0% | -5.1% |

| Feb-5 | U.S. Change in Nonfarm Payrolls | 190k | 151k | 262k |

| Feb-11 | U.S. Initial Jobless Claim | 280k | -- | 285k |

| Feb-12 | Germany CPI YoY | 0.5% | -- | 0.5% |

Strengths

- Silver was the best-performing precious metal for the week with a gain of 5.05 percent. Perhaps the brewing controversy over the most recent price fixing accusations, discussed below under “Threats,” is starting to draw more eyes upon this process and the banks accused of manipulating the price will have to back away.

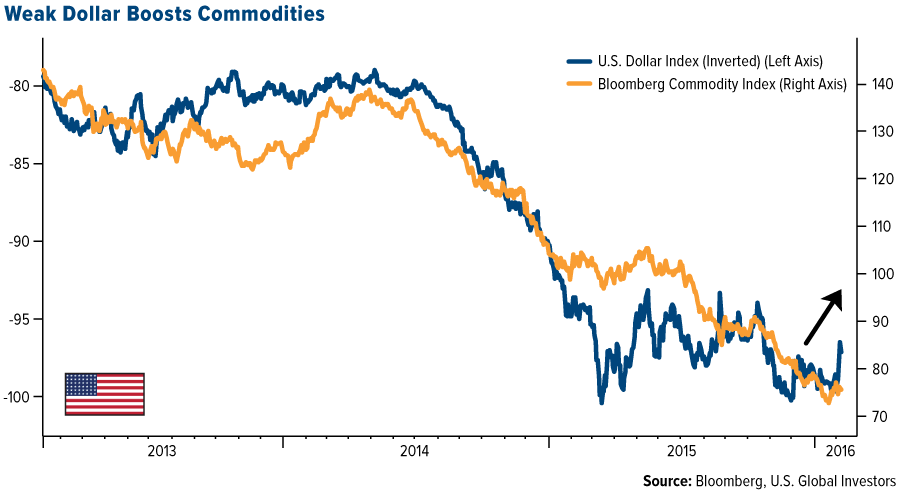

- The U.S. dollar is having a rough ride, reports Bloomberg this week. The currency dropped following a report showing service industries expanded in January at the slowest pace since 2014, a sign that manufacturing weakness is “starting to creep into the rest of the U.S. economy.” Even New York Fed governor William Dudley warned of “significant consequences” for the economy if the dollar were to strengthen further, according to MacroStrategy.

- Gold rallied early in the week after data showed a further contraction in China’s manufacturing data, adding to the case for haven assets, reports Bloomberg News. In fact, according to a report from the Perth Mint, gold sales rose to 47,759 ounces from last month. The sales for January climbed 250 times the amount of sales in December. January sales reached 124,000 ounces, up 53 percent since last January.

- Wedding season demand has also driven this uptrend in gold sales.

Weaknesses

- The worst-performing precious metal for the week was again - palladium. Perhaps markets are expecting car sales to not be as strong this year, due to the recent weak economic data.

- Primero Mining Corporation closed the week down 35.20 percent. The precious metal producer and its advisers believe that a legal claim made by the Mexican Tax Authorities (SAT) is without precedent, according to Canaccord Genuity. Primero reported that its Mexican subsidiary received a legal claim from the SAT aiming to nullify a 2012 APA (Advance Pricing Agreement) ruling. The ruling allowed the company to pay taxes on realized silver prices as opposed to spot silver prices between 2010 and 2014.

- Bloomberg reports that Indian gold imports in January could drop 25 percent from December, along with inbound shipments falling to 80 tons in January (from 106 tons the prior month). Unofficial gold trade in the country has also been boosted, according to the Times of India. Rather than promote transparency, a new rule to force buyers of high-value jewelry to disclose their tax code, has actually increased unofficial trading. Looking to Venezuela’s gold market, Reuters reports that the country’s central bank has begun talks with Deutsche Bank AG, noting that the talks are focused on gold swaps to improve the liquidity of its foreign reserves.

Opportunities

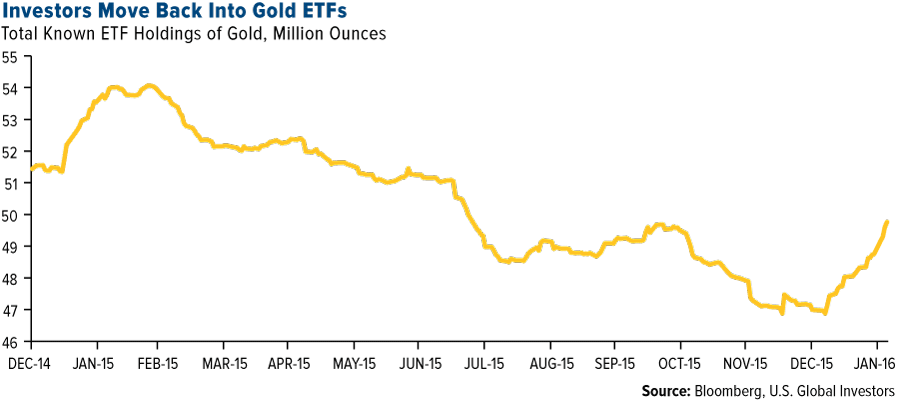

- Assets in gold-backed exchange-traded products have jumped 4.9 percent in the past month, reports Bloomberg News, making this the longest “fund-buying run in three years.” Traders are betting on less than a 50 percent chance of a rate increase by the Federal Reserve this year (gold tends to fare well when rates are low), yet another sign pointing to the metal’s resilience this year.

- The China Gold Association believes the country’s gold demand will keep expanding as investors seek safe-haven assets and jewelry buying increases. Consumption in China climbed 3.7 percent in 2015 from a year earlier, while gold output in 2015 was down 0.4 percent. As Lawrie Williams points out, this means China’s gold output faltered for the first time in 20 years. China’s flatting production profile seems to reinforce the notion of “peak gold production” may be upon us.

- Lake Shore Gold jumped nearly 10 percent on Friday due to an Internet posting on rumors that the company is in late-stage talks to be acquired by Tahoe Resources. Earlier this week Lakeshore confirmed the expansion of its high-grade Whitney mineralization project. The deal could bring a politically safe Canadian asset into Tahoe Resources’ fold. In addition, the Lake Shore assets are surrounded by Goldcorp properties that might not be core to Goldcorp. Thus perhaps there is a bigger opportunity for Tahoe to later strike a friendly deal with Goldcorp where Tahoe acquires a strategic position in the Timmons Gold Camp and Goldcorp sells non-core assets and pays down debt. Integra Gold also made headlines this week after the company was rated a “strong buy” by Raymond James. Equity analyst David Sadowski placed Integra’s 12-month target price at C$0.70 per share.

Threats

- According to a Sharps Pixley article this week, 10 times in the last six months the silver price has been “fixed” outside the trading range of the spot price for that day, which is making some scratch their heads. The LBMA Silver Price, or the new silver fix, had the spot markets “fixed” last Thursday at $13.58, yet silver traded between $14.40 and $14.10 in the spot markets. As ZeroHedge points out, this “hugely controversial silver price benchmark was set some 6 percent below the prevailing spot price on Thursday.”

- The German government is considering introducing a limit of 5,000 euros (or in U.S. dollars, $5,450) on cash transactions, reports the New York Times, in an effort to combat money laundering and the financing of terrorism. ZeroHedge writes that these cash controls come at a “rather convenient time for policy makers in Europe,” pointing out that rates are already sitting at -0.30 percent (and likely to be cut an additional 10 basis points in March). The article continues on to state that “in a cashless society with a government-managed digital currency there is no effective lower bound” to how governments could control your wealth.

- Bloomberg Business reports that a handful of companies that have dominated nearly every kind of raw-material business in Japan for decades, could take as much as $13 billion in charges during the current fiscal year. General trading houses, or “sogo shosha,” that supply everything from gasoline to noodles, have been squeezed by the global commodity slump. With raw material prices falling, reports Bloomberg, the focus has shifted to other businesses.

![[thumb]](/images/content_image/data/fa/fa2fca0ada0a82fd0aa313d798124428.jpg)

February 3, 2016Muni Bonds Have Performed Well in Volatile Times |

![[thumb]](/images/content_image/data/ab/ab47339a4c4f8b2ef93c622264860d05.jpg)

February 1, 2016Recession on the Horizon? Look at the Big Picture |

![[thumb]](/images/content_image/data/52/521832fb79a3fdd6ca2f50cd0a421c3b.jpg)

January 25, 2016Comparisons to 2008 Spark Gold’s Fear Trade |

Energy and Natural Resources Market

Strengths

- Gold had its best weekly advance since 2013, rising nearly 5 percent this week, as investors showed concern that the health of the U.S. economy is deteriorating because of the strong dollar. Investors’ holdings of gold in exchange-traded products (ETPs) posted the longest continuous increase since 2012, leading gold to outperform all major commodities year-to-date.

- The best performing sector for the week was gold mining. Gold miners rallied 18.8 percent for the week with strong gold prices providing a boost, as futures for the metal broke above the 200-day moving average, a key technical indicator.

- The best performing stock for the week in the broader natural resource space was Newmont Mining. The largest U.S. gold producer rose 22.3 percent in New York as gold rose to a three-month high.

Weaknesses

- Crude prices dropped further this week as Saudi Arabia confirmed it lowered March pricing on its oil for customers in Asia. The price adjustment confirms investor speculation that the kingdom is not letting up on its campaign to keep market share, especially in Asia as Iran attempts to boost exports.

- The worst performing sector for the week was oil refining. Despite strong earnings across the board for the fourth quarter, the sector declined on speculation that some refiners could be forced to increase dropdowns to their affiliated MLPs after growth prospects slow with lower oil prices.

- The worst performing stock for the week in the S&P Global Natural Resources Index was ConocoPhillips. The oil and gas producer dropped 15.8 percent this week after it slashed its dividend 66 percent to withstand lower commodity prices and tightening credit markets.

Opportunities

- Recent weakness in the U.S. dollar has given a boost to commodities. The latest batch of economic data from the U.S. showed continued weakness in manufacturing, and a significant deterioration in the services industry. Investors now expect a delay on additional interest rate hikes, which has resulted in the U.S. dollar weakening and giving a much needed boost to commodity prices.

- Utilities are rallying this year as investors speculate dividends of natural resource companies might be at risk. Utility companies pay out high dividends and rely on more dependable sources of revenue.

- Natural gas prices could continue to rise on further cold weather. Gas prices rebounded mid-week from a six-week low as weather forecasts show colder fronts moving into the Eastern U.S.

Threats

- Purchasing managers’ index (PMI) data for January suggests global manufacturing, a key driver of commodity demand, didn’t worsen but continues to flirt with recession. A report by Macquarie Research analysts highlights that that global manufacturing PMI sat barely above the contractionary level for a third consecutive month.

- Copper lagged its metals peers this week as inventories in Shanghai surged ahead of the Chinese New Year celebrations. Copper stocks jumped 29,317 tonnes, a 13.8 percent increase over previous levels.

- Soybeans posted their biggest weekly drop this year as favorable weather forecasts in South America should improve Brazilian and Argentinean crop yields and lead to increasing competition for U.S. growers.

China Region

Strengths

- Indonesia’s fourth-quarter GDP beat analysts’ expectations, coming in year-over-year at just above 5 percent, and ahead of survey results anticipating 4.8 percent. The Jakarta Composite Index was the strongest performer in the region over the last week, rising to multi-month highs and soaring back above its 200-day moving average.

- China further loosened mortgage requirements for non-Tier 1 cities.

- Nearly all regional currencies finished the week stronger against the U.S. dollar. In the face of a weaker Japanese yen, and as expectations for a March rate hike from the U.S. Federal Reserve continue to diminish, Indonesia’s rupiah and the Singapore dollar, in particular, both rose more than 1 percent for the week.

Weaknesses

- China’s official Manufacturing PMI missed expectations, coming in at 49.4, below expectations. While the more export-oriented Caixin China Manufacturing PMI did come in slightly higher than expectations, both Manufacturing PMI readings are below the 50 mark, signaling contraction. Services have managed to remain above 50, signaling China’s continued evolution into a more services-oriented economy and away from traditional manufacturing.

- Retail sales numbers in Hong Kong fell 3.7 percent to HK$475 billion last year, as a weaker yuan and lower tourist visits weighed upon Hong Kong’s luxury purchases in particular.

- Hong Kong property prices are weaker, down some 10 percent since September of last year, and monthly sales in January fell to the lowest level in 25 years.

Opportunities

- M&A continues to heat up in China and with ChemChina’s pending $43 billion acquisition of Syngenta, 2016 continues apace to another record-setting year.

- As the Lunar New Year celebrations begin this weekend, mainland China goes on holiday for the entire upcoming week. Taiwan closed earlier this week and will also be closed all of next week, as will Vietnam, and Hong Kong and South Korea for the first three trading days of the week. The lengthy holiday period may bring some pause to the negative sentiment and uncertainty marking global and regional markets of late.

- China announced a ban on any new additions to steel capacity, and while a newly-announced blueprint for additional capacity reduction fell somewhat short of expectations, China still expects to reduce up to 150 million tons over the next five years.

Threats

- Investors continue to remain focused upon recent questions concerning the pace of capital outflows and FX reserves in China. This weekend China will release its FX reserve levels for the end of January, giving investors and China-watchers the chance to quantify what many expect has been a costly defense of the yuan.

- Although Chinese news sources late this week denied any need for concern over capital outflows, earlier this week mainland news sources reported that the government will cap the use of UnionPay bankcards for purchasing overseas insurance products, which weighed upon insurers like AIA (1299 HK), Manulife (945 HK), and Prudential (2378 HK).

- Recent or continued volatility may continue to weigh upon the region and sentiment.

Emerging Europe

Strengths

- Romania was the best performing country this week, gaining 1.8 percent. Strong economic data was released for the country, the December unemployment rate was reported at 6.7 percent and retail sales grew 13 percent year-over-year. Romania is one of the fastest growing regions in the European Union. The country is in the process of reversing one of the EU’s toughest austerity programs that helped narrow the budget deficit to 1.5 percent of economic output last year from about 7.2 percent in 2009.

- The Romanian leu was the best performing currency this week, gaining 4.4 percent against the U.S. dollar. The Central Bank of Romania left its main interest rate unchanged at 1.75 percent, as predicted by Bloomberg economists.

- Consumer discretionary was the best performing sector among Eastern European markets this week.

Weaknesses

- Greece was the worst performing market this week, losing 8.9 percent. The Athens Stock Exchange was pulled down by banks, with four major Greek banks, on average, losing 24 percent over the past five days. Greek banks recently went through a recapitalization process but the European Central Bank (ECB) has raised the issue again of a comprehensive assessment of the way banks are being managed.

- The Russian ruble was the worst relative performing currency this week, losing 2.3 percent against the U.S. dollar. The ruble extended a weekly loss as Brent crude oil declined 1.8 percent. The ruble/oil correlation reached a new high on Friday of 0.79; a reading of 1 would indicate these two assets are moving in lockstep.

- Consumer staples was the worst performing sector among Eastern European markets this week.

Opportunities

- Inflation in Russia declined to 9.8 percent from 12.9 percent in December. The year-on-year rate failed for a fifth-straight month to the lowest level since November 2014. Russian monetary policy makers seek to lower inflation to 4 percent in the medium term. In recent months, currency weakness and high inflation have prevented the Central Bank of Russia from lowering the main interest rate.

- After the S&P cut Poland’s credit rating last month, the Finance Ministry was able to sell all of the 7.5 billion zloty ($1.7 billion) of long maturity debt offered at an auction (with yields comparable to previous auctions), suggesting that investors are optimistic about the country’s future.

- Russia announced a privatization plan in an effort to raise about 1 trillion rubles ($13 billion) of selling stakes in state companies over two years in order to close the widening budget gap. President Vladimir Putin will allow foreign investors to bid for a stake in some of Russia’s largest companies.

Threats

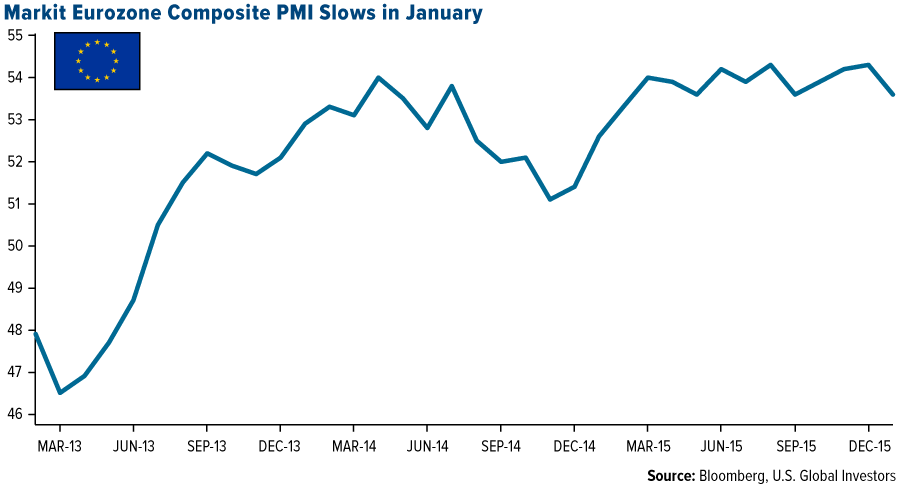

- Markit Economics said its composite purchasing managers’ index (PMI) for January was “disappointing.” The PMI declined to 53.6, a four-month low, from 54.3 in December. This reading suggests that further stimulus plans might be coming to the eurozone area to stimulate the economy.

- The Greek government is discussing the fiscal gap with creditors that stands at 1-1.2 billion euros. Recent talks on pension reform and new tax revenue sent many Greeks to the streets protesting against the government’s proposed austerity measures.

- The EU and the United Kingdom are making progress in negotiations on Britain’s membership in the eurozone, but a number of important questions are yet to be answered. UK Prime Minister David Cameron is asking the EU for restrictions on welfare benefits for migrants from other EU countries, exclusion from cash contributions to eurozone bailouts, as well as for the eurozone to be known as a multi-currency union. No country has ever left the eurozone. French Prime Minister Manuel Valls said last month that “nothing could be worse than to see a member state leave.”

(c) US Global Investors