Adverse financial market developments have led to an overflow of bearish analyses. It is certainly dangerous to ignore market signals, but they aren’t always conclusive. There are some positive fundamentals in place that provide some reassurance around the outlook.

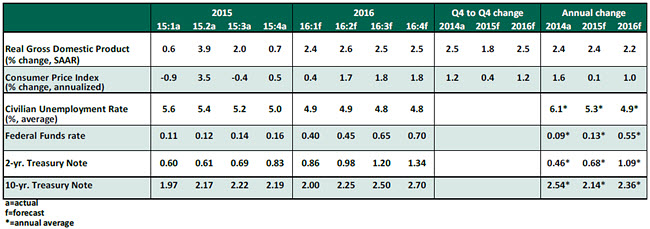

The U.S. economy grew at an annual rate of only 0.7% in the fourth quarter, following a 2.0% increase in the previous three-month period. The pace of expansion in 2015 (2.4%) matches the momentum seen in 2014. This trend is higher than the potential growth of the U.S. economy, which the Fed estimates at 2.0%.

The fourth quarter’s weakness was marked by large negative contributions from inventories and exports. While neither is the brightest spot on the outlook, it is unlikely that they will remain as depressed in the quarters ahead. A constructive labor market, with growing spending power, supports our view that economic activity is unlikely to be derailed in the near term.

Key Economic Indicators

Key Elements of Forecast

- Consumer spending growth slowed in the final three months of the year, a bit disappointing given the strength of the labor market. Auto sales moved up in January (17.5 million units versus 17.2 million in December), employment compensation picked up, and consumer confidence indicators have held up in the face of weak equity market conditions. These factors suggest that consumer purchases are most likely to grow at a decent clip.

- A sharp drop in durable goods orders in oil-related industries was visible in the November and December reports. There was weakness in non-oil-related capital goods orders also. The increase in new orders in the Institute of Supply Management’s manufacturing survey is positive news. Business spending, as reported in gross domestic product data, slipped in the fourth quarter (-2.5%), but a turnaround is predicted for the first quarter.

- Progress in bank lending is noteworthy, with recent growth hovering slightly above the historical median. All categories of bank lending – commercial and industrial loans, consumer loans, mortgage loans, and commercial real estate loans – show gains. The absence of a negative signal from lending trends supports expectations of continued growth.

- Residential investment spending rose 8.2% in the fourth quarter, which puts the annual average gain at 8.7%, significantly better than the tepid 1.8% increase seen in 2014. The increase in permit extensions during December for single-family homes bodes well for home construction activity. Sales of new home sales rose nearly 11% in December, while purchases of existing homes surged nearly 15%. The homeownership rate increased two notches (63.7%) in the second half of 2015. In all, the housing sector appears to be stabilizing and could offer upside to the outlook.

- The trade-weighted dollar is about 6.5% higher than a year ago. This is a noteworthy loss in strength, as it recorded double-digit increases last year. In light of this change, net exports should be less of drag on the economy, particularly if growth abroad picks up due to the central bank policy support in the eurozone and Japan.

- Productivity of the U.S. economy is lackluster; it rose only 0.3% in 2015. Consequently, unit labor costs moved up 2.8%. Unit labor costs and core inflation have a strong positive relationship; the Fed may see higher inflation soon.

- The labor market continues to improve. The unemployment rate at 4.9% is the lowest in nearly eight years, and about 230,000 jobs were created, on average, in the last three months. Hourly earnings rose 2.5% from a year ago, breaking the stubborn 2.0% trend, just what the Fed was looking for. But labor market conditions are not entirely perfect; the recent uptick in initial jobless claims suggests close scrutiny. There are a large number of part-timers seeking full-time employment, and there is significant long-term unemployment.

- The core Consumer Price Index, which excludes food and energy, is above 2.0%. However, the Fed’s preferred price gauges, the personal expenditure price index and the core measure, are both still below its target. Oil prices are low, and the dollar holds at an elevated level. But both are likely to moderate in the near term.

- The financial market turmoil is casting a shadow on the global economy. A significant risk-off sentiment has driven the 10-year U.S. Treasury note yield to 1.73%, down 25 basis points since the Fed’s January meeting and close to the low seen last year. The bond market’s current view may be a reflection of fear rather than fundamentals.

- The Fed’s risk-management acumen is being tested. It is in a tricky spot, with near full employment conditions and moderate inflation combined with financial market instability. The market view is a patient Fed throughout 2016; markets can quickly change this assessment. We continue to predict modest monetary policy tightening limited to a total of two moves in June and December.